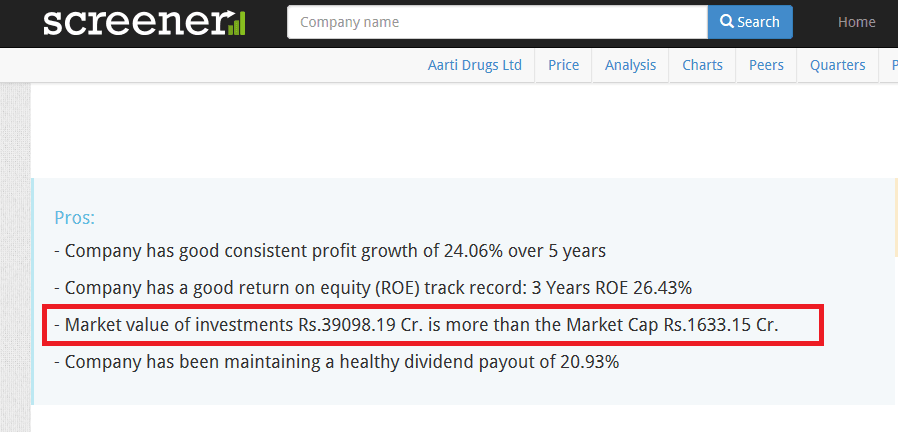

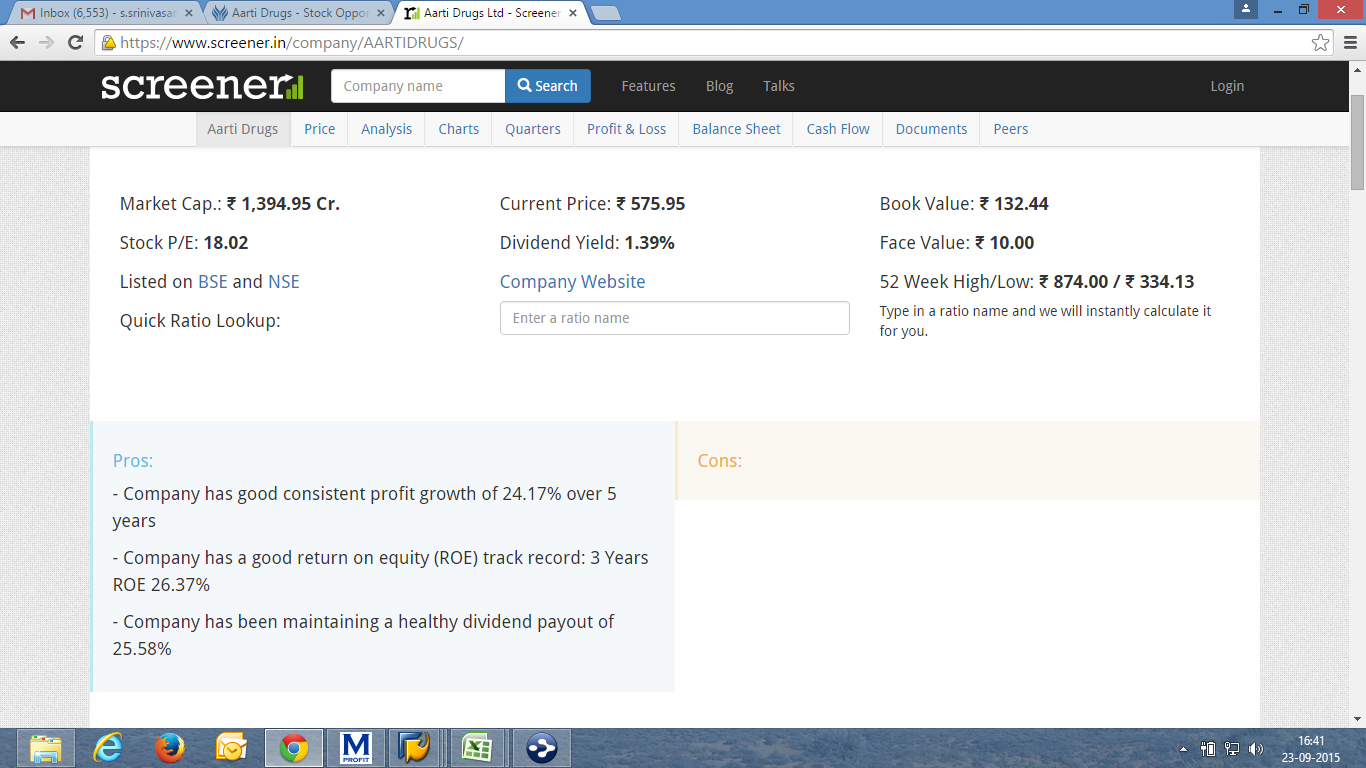

Market value of investments Rs.39098.19 Cr. is more than the Market Cap Rs.1633.15 Cr.

But in balance sheet is investments amout is 11cr.

How to find out what are the investments company made so that we can verify the current market value of the investments?

Did I miss some thing here?

** scrrener screen shot.**

@saiirfan…As u brought out in the balance sheet…trade recievables are in the range of 250-350 crores…this to me look too high…or are they normal??? Any views from seniors???

I recently started looking at Aarti Drugs and found this interesting. Thought of sharing my analysis here:

Disclosure: I already hold Aarti Drugs as a part of my core portfolio. This write up below is meant for discussion and is not to be construed as recommendation. Please do your due diligence.

Aarti Drugs Limited established in 1984 is a predominantly API manufacturer having a small presence (~15%) in Formulations & Speciality Chemicals.

In APIs they are present in the following Therapeutic Segments:

A. Active Pharma Ingredient (85%)

1. Antibiotics (47%)

2. Antiprotozoals (23%)

3. Anti inflammatory (12%)

4. Anti fungal (8%)

5. Anti diabetic (4%)

6. Cardio protectant & Others (6%) B. Formulations(8%) C. Speciality Chemicals (3%) D. Others (4%)

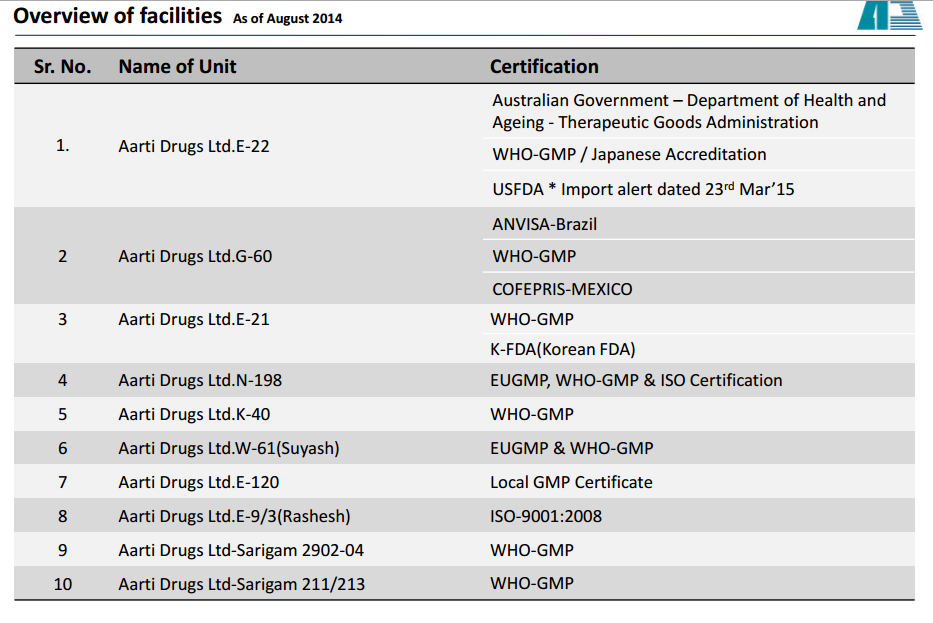

ADL’s Plants: ADL has 10 plants located across the country and the details of the plants along with the certifications are available here:

Active Pharma Ingredients:

Among the various therapeutic segments the company is already operating in, the following segments had significant capex in the last two – three years and the results of this will be visible in the #s in the next 2-3 years.

I. Antobiotics

II. Antiprotozoals

III. Antifungals

IV. Anti diabetes

V. Anti inflammatory

VI. Cardio protectant & Others

I. Antibiotics (47%)

The company is present in fluoroquinolones APIs and has developed significant research capability to develop 3rd generation fluoroquinolones. Quinolones are a broad spectrum of anti-bacterial drugs used to treat bacterial infections. 1st generation quinolones were developed in 1962, and with time we have 4th generation quinolones in the market. Higher the generation the molecule is present in, higher the margin for the company.

Note: Read the below url on Quinolone to understand more about fluoroquinolones.

2nd Generation Fluoroquinolones:

A. Ciproflaxacin

i. Constitutes 22% of revenues

ii. Recent Capacity expansion in place from 1200 to 3600 TPA

iii. Is putting up a backward integration plant and this will come up in the next one year. – Improves cost competitiveness.

iv. Current sales at 1620 TPA.

v. Global Size of this molecule - ~5000TPA

vi. Who are the other players here? –

B. Enrofloxacin

C. Ofloxacin

D. Norfloxacin

The above 3 molecules constitute 13% of the topline.

3rd Generation Fluoroquinolones: (12%)

E. Levofloxacin – 240 T to 720T

F. Molecule1* – 720 T capacity

G. Molecule2*- 720 T capacity

Current revenues ~135cr from these 3 molecules:

i. These molecules have higher margins than 2nd generation fluoroquinolones.

ii. Company has already commissioned capacity from current to 3x.

iii. Revenue potential from these 3 molecules @ 500 crores

iv. Who are the other players here? – Have to find out

*What are the names of these new 3rd generation molecules? - to find out

II. Antiprotozoals (23%)

a. Metronidazole

i. Contributes to 5% of revenues

ii. Largest producer in India

iii. Doubled Capacity for this molecule likely to come in by Q2 FY16.

iv. Currently India is importing this molecule from China. After capacity expansion, ADL aims to supply domestically.

Check the below url to understand trend of imports: Import analysis and trends of of metronidazole | Zauba

b. Metronidazole Benzoate

i. Largest producer in the world

c. Ornidazole d. Secnidazole

e. Tinidazole

i. Largest producer in the world

f. Diloxanide Furoate

Summary:

Incremental revenue potential after expansion to be around 50 crores

III. Anti diabetic (4%)

a. Metformin HCL

i. Currently Metformin molecule addresses 49% of global Anti diabetes market.

ii. Current Global Metformin Capacity – 30000 TPA

iii. Other Players: Wanbury(9000), USV(10,100), Harman (6000), Granules (2000) & Aarti has 1200 TPA

iv. Aarti has expanded capacity by 5x here – 7200TPA

v. This capacity can be doubled at minimal additional cost

vi. Reports put Metformin market growth at 9-14% p.a

b. Pioglitazone

IV Anti fungal (8%)

a. Ketoconazole

i. Capacity expanded by 50%, not able to quantify revenues here.

b. Tolnaftate

V. Anti inflammatory (12%)

a. Aceclofenac

b. Diclofenac Sodium

c. Diclofenac Pottasium

d. Diclofenac Diethylamine

e. Diclofenac Epolamine

f. Diclofenac Resinate

g. Nimesulide

h. Celecoxib

Summary Below: Triggers due to capacity expansion - Quantifiable:

Incremental Revenue potential due to recent capex(completed) in this segment stands at 750 crores (~400 crores from Ciproflaxin + ~350 crores from 3rd generation fluoroquinolones)

Incremental Revenues to come at higher margins:

Backward integration of plant for Ciproflaxin about to come in – in 1 year?

3rd Generation Molecules have higher margins.

Antiprotozoal expansion: Incremental revenue potential after expansion to be around 50 crores.

Incremental revenue potential after expansion to be around 150 crores.

a. Market leader Wanbury is currently in financial distress and is unable to meet the growing demand

Capacity of Ketoconazole expanded by 50%, not able to quantify revenues here.

USFDA Import Alert – Unquantifiable:

If USFDA lifts the import alert on one of its facilities, this will throw up more avenues. – But this is an optionality.

Currently the company has been doing a topline of about ~1000 crores, and give it three years, the company must be able to add another 1000 crores. If the topline doubles, their PAT figures should grow at a much faster rate as 75% of the incremental topline is coming from high margin molecules. From here valuation is an interesting question and is left to the individual.

What could make a mockery of these numbers: - RISKS

With Chinese economy in distress, what is the likelihood of further Chinese depreciation of Yuan? – This will erode the cost competitiveness of ADL!.

Competition behaviour – For instance, in the anti-diabetes segment, Granules currently has 2000 T. This is stronger competitor(financially also). If they also decide to expand significantly, it becomes a case of lower margin business! One has to monitor this very closely. Have to understand other players in Ciproflaxin also.

Manufacturing of APIs are a capital intensive business and will need constant capital to expand further. For the next 2 year, the company says they need about 100 crores for capex. They have sufficient free cash flows to take care of this incremental capex. (Lower risk) – I call this as a risk because continuous capex requirement is always a headache to me;-)

Latin America is about 9% of revenues so there will be a small impact on the numbers.

Below is Granules commentary from Q2FY16 concall

Metformin and Guaifenesin put together contributed 30% to our second quarter-consolidated topline. These are important products for us and we see opportunity to solidify our global position in these molecules. As we have communicated in our first quarter call, we have started working towards enhancing our Metformin and Guaifenesin API capacity by 7,000 tons per annum and 2,000 tons per annum. The construction work is progressing as per our internal estimates and schedules and we expect to initiate trial production in these blocks in the second half of the next financial year.

If aarti has already completed the expansion to 7200TPA, it could be a big trigger for them. They will have a first mover advantage. But need to understand where is the market…if its US, then FDA issue is critical.

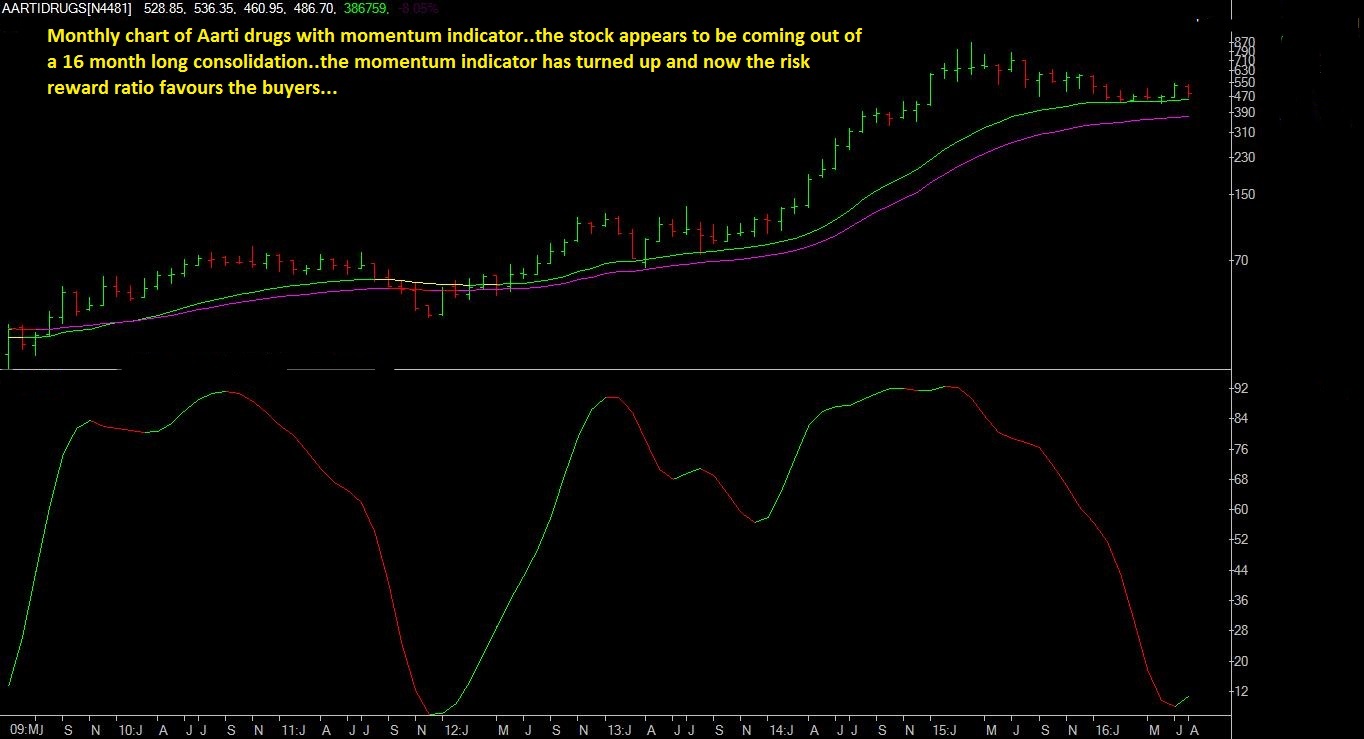

Check the price per unit in December. There is a very big jump (almost 1.8x). Difficult to say what could this means. Maybe we can ask the management.

Anyway, its a small part of the picture. Overall, it does look good but the question is when were these expanded capacities commercialized. When do you expect to see a spurt in revenues?

Below is an extract from AR FY15

The Company has carried out expansion programs in the current year and also had carried out in Year 2012-13 & 2013-14 keeping long term view in the mind, in spite of recessionary conditions prevailing in global and domestic market. Unfortunately, delay in getting Environment Clearance approval due to change in government policy regarding public hearing, hampered a bit of sales growth in the year 2014-15. However, even after expensing out the interest and depreciation cost from this project, Company has showed good margins in 2014-15. We expect good boost in the sales from this project in the year 2015-16. The Company has received an import alert for its USFDA approved unit in March 2015 which is responded to the satisfaction of the authority and we expect their feedback soon. Currently Sales to US are less than 1% of overall sales and hence impact on revenue and margin is minimal. Overall impact on growth prospects in near terms is marginal though prolonged delay can affect US revenue growth going forward.

Also…

Environmental Clearance (EC) for the new Anti-diabetic facility took more than required time due to change in government policies related to public hearing in the year 2014-15. However, EC has been obtained recently and subsequently we have also received WHO-GMP, unlocking the export potential of this Anti-diabetic drug. We expect to get more regulatory approvals for European markets as well in future.

I invested in Aarti Drugs in July’15 and have been tracking since then. I like companies which shows consistent growth and found Aarti Drugs interesting.

Company is currently trading at around 20 PE while the industry average is around 30 PE. However I feel at the current market price the company is fairly priced. Currently it forms 1.5% of my portfolio however I might look to increase exposure by another 1% once available at 425-440.

Next year can be single digit growth as per management. Annual EPS around 25-28. Sep quarter was bit subdued due to depr. and interest cost. However management was good to come out with clarification. Business to pick up from Q4. DSP has 2% stake in it. Promoters have increased stake from 59 to 61 in the latest quarter. Annual revenue above 1000 crs and margin around 7%. Growing steadily at 20% YOY for the last 5 years. NPM is also improving YOY. However interest is half of its profit, so need to keep an eye.

The Company’s R&D programs are currently focused on new products related to lifestyle related diseases like Diabetics, Cardiovascular, Dementia, Hypertension, Cholesterol, Hyperphosphatemia, etc. These products would be developed along with their DMFs in a time-horizon of 2-4 years. This falls in line with the vision of expanding ADL’s presence in the regulated markets. Company will continue to do R&D on APIs that are off patents and will work on non-infringing route of synthesis. ADL has also tied up with European distributor on profit sharing basis. Already 3 dossiers are ready and are under stability study. Though total debt of Rs. 3422.40 million as on 31st March 2014 is a concern, Aarti drugs has high growth prospects in the long term with its strong product base ranging from API, Steroids, Pharma Intermediates and Speciality Chemicals. Hardly any FII or DMF holdings. Have major pharma companies in its clientele. 60% business in Asia and Latin America.

Although the company increased its capacity specifically in metformin, during the current quarter, it did not have any impact on revenue as most of it is exported to nations in Africa and Middle East which have witnessed a demand slowdown due to decline in crude oil prices. Thus exports for the company witnessed a double digit decline. Slowdown is particularly observed in case of governments of many of these nations who are curbing imports and depleting their inventories. However domestic revenues which forms 60% of the overall topline, recorded double digit growth.

The company is likely to witness gradual improvement in topline growth from 4QFY16 onwards when it starts the sale of high value products initially in the anti-diarrheal and anti-diabetic segment viz. metformin and later in anti-biotics.

Aarti drugs fundamentally looks very strong except cash flow. Standalone CFO of last 10 years is 408 crs against the net profit of 1614 crs. Also, net cash flow is -ve most of the time.

Hey hrushkik, In last 10 years Aarti drugs never crossed the mark of 100crs as per screener, failing to understand how did you reach the figure of 1614 crs in 10 years. Please correct me if I’m missing sth.

Aarti drugs promoters have bought shares of more than 1 Cr sice 25Jan 2016 from the market. This is a good sign for the company. Disclaimer; Invested in the company…

The Company’s R&D programs are currently focused on new products development related to lifestyle related diseases like diabetics, cardiovascular, anticoagulant, cholesterol etc. These products would be developed along with their DMFs in a time-horizon of 2-4 years.

Company will continue to do R&D on APIs that are off patents and will work on non-infringing route

of synthesis. The Company has also tied up with European distributor on profit sharing basis of finished dosage sale. Already 2 finished dosage dossiers are filed with UK MHRA and 2 are under developmental stage. Strategy would be to engage in our own APIs.

The Company has started commercial operations of intermediate plant, first in India, for three of its Anti-biotic products. Majority market share and economies of scale with strong technological backup will continue to remain key strengths of the Company. Few of its expansion projects were commercialized last year, which will give good impetus to growth initially targeting domestic markets and eventually the global markets post getting necessary regulatory approvals.

Macroeconomic conditions and higher gestation period due to newer regulatory processes had caused a subdued growth in last year, however company is in advance stage to get such approvals for the last years’ expansions.

The company has shown decent growth in the last 5 years and the next 2 years will be more of a consolidation period for the company i believe. The fruits for the ongoing project will start delivering post mid of 2018 I believe.

Valuation wise it offers more comfort when compared to its peers. Regular dividend paying company. Patience will surely be rewarded is what I feel. The stock is currently 1.5% of my portfolio, I will look to add more once available between 450-475. Also once the US FDA is sorted in some months, the stock might climb back to 650 above levels.

Was reading Aarti Industries concall and there was question on pharma products and difference with Aarti drugs, so thought of noting this here -

In Aarti Industries we have anti-cancer steroidal manufacturing facility as well as we focus on anti-hypertensives and CNS products. Whereas Aarti Drugs there we have more large volume products.