Its good to see that Zydus has started filing products in animal healthcare division for the US. Earlier, they had divested their Indian healthcare business to focus on regulated markets.

Disclosure: Not invested (no transactions in last-30 days)

Its good to see that Zydus has started filing products in animal healthcare division for the US. Earlier, they had divested their Indian healthcare business to focus on regulated markets.

Disclosure: Not invested (no transactions in last-30 days)

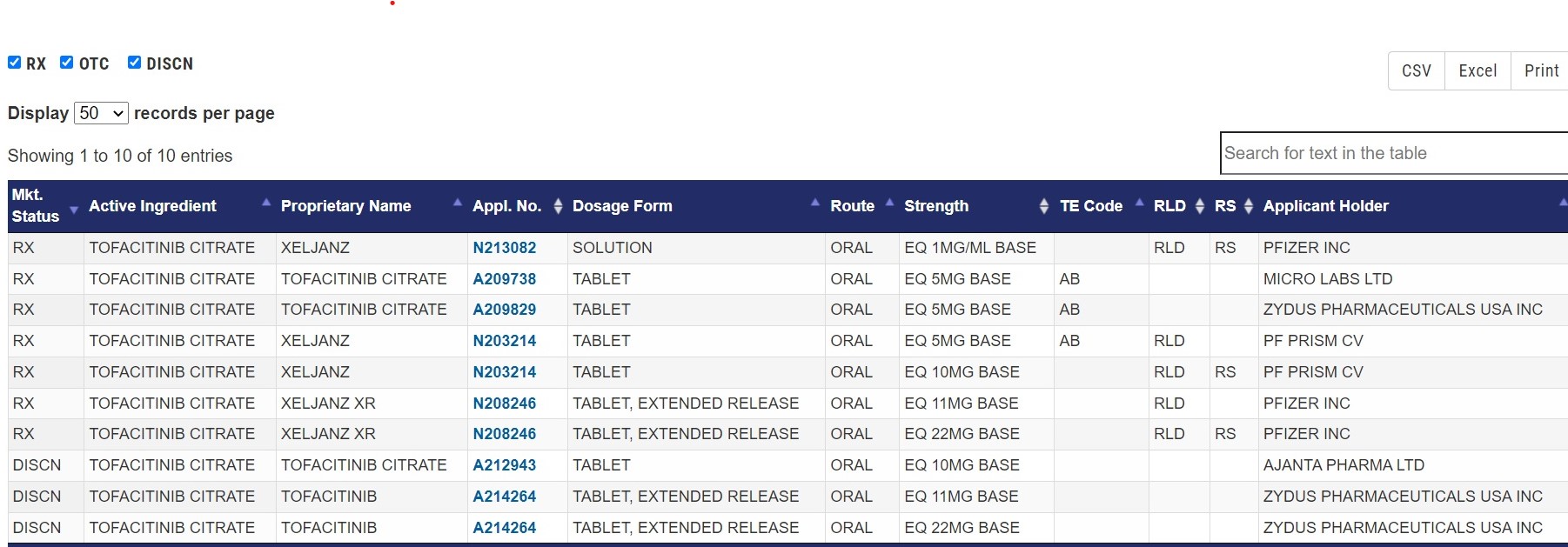

Zydus receives final approval for Tofacitininib 5 mg tablet and tentative approval for 10 mg.

It’s also eligible for 180 days of shared exclusivity for 5 mg strength.

Tofacitininib is a generic version of Pfizer”s XELJANZ which acts by inhibiting Janus kinases enzymes involved in the pathway of inflammatory process.

XELJANZ is indicated in patients with ankylosing spondylitis, moderate to severe rheumatoid arthritis, active psoriatic arthritis and moderate to severe active ulcerative colitis which are autoimmune inflammatory diseases.

Tofacitinib 5mg and 10 mg had annual sales of 900 mn in USA.(worldwide annual sales of 2.3 billion USD).

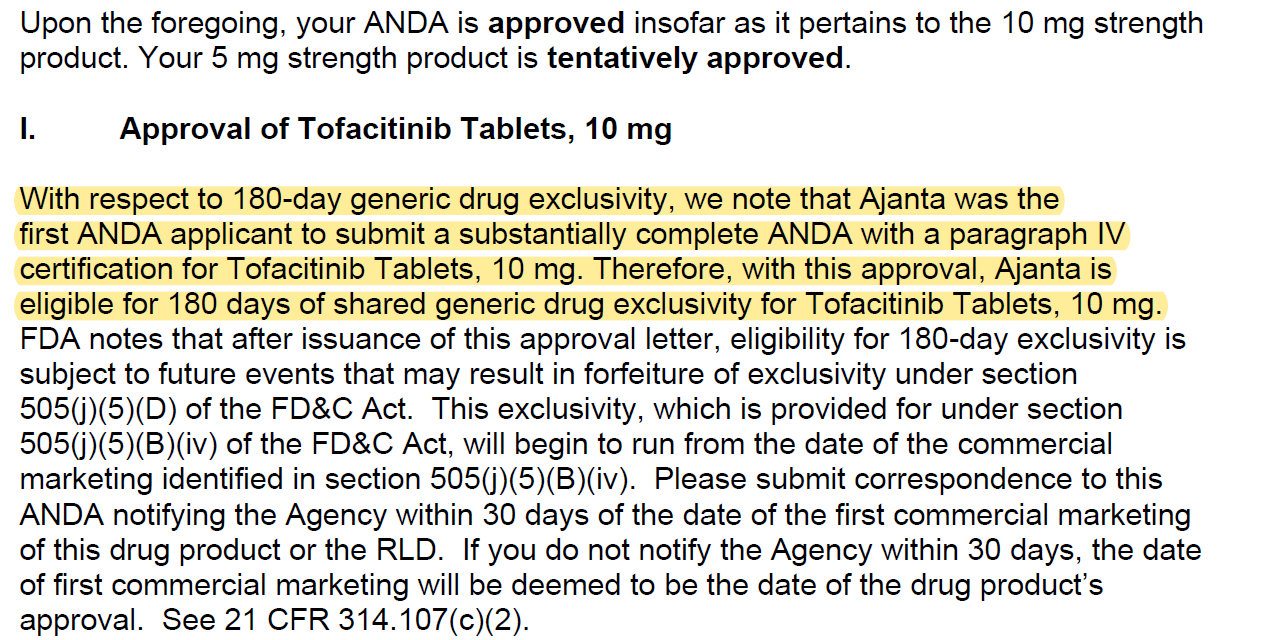

US FDA orange book shows few more approvals including Ajanta pharma and Micro Labs.

Ajanta pharma seems to have exclusivity for 10 mg tab as per below document of FDA.

Discl: invested

Zydus Lifesciences has received final approval from the USFDA to manufacture and market Estradiol Transdermal System USP, 0.014 mg/day.

Estradiol transdermal system is indicated for prevention of postmenopausal osteoporosis.

Ref: https://www.bseindia.com/xml-data/corpfiling/AttachLive/5e28376a-ff6b-4d81-b523-049d8f8c439a.pdf

Disc: Invested

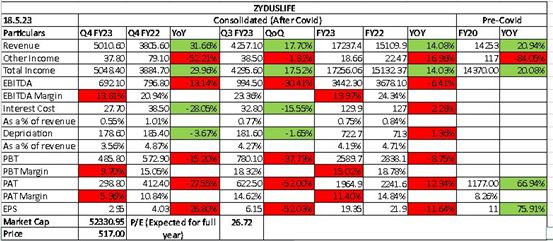

ZYDUS LIFESCIENCES -

Q2, FY 24 updates -

Sales - 4368 cr, up 9 pc

Gross Margins @ 66 pc

EBITDA - 1146 cr, up 41 pc ( margins @ 26 pc vs 21 pc YoY )

NP - 800 cr, up 53 pc

R&D expenses - 322 cr @ 7.2 pc of revenue (healthy rate)

Capex for the Qtr at 216 cr

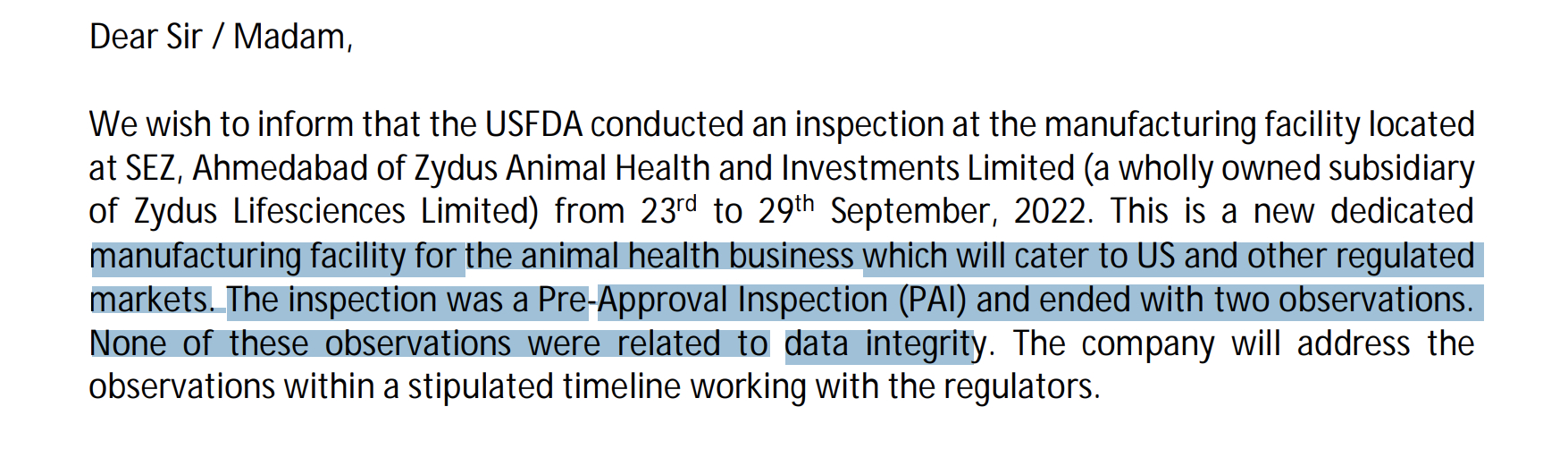

3 US FDA inspections happened in Q2 @ oral solid facilities I and III at Ahmedabad SEZ, Biologics fill-finish facility at Zydus Biotech park - all received EIR

Geography wise sales breakup -

India branded formulations - 32 pc - grew by 5 pc YoY despite delayed monsoons and hence the delay in acute season . Maintained leadership in Nephrology space. Grew strongly in Oncology space. Company’s biggest segments - Cardio, Respiratory, Anti-Infectives. Company has 08 brands among top 300 brands in India

India consumer wellness - 10 pc - grew by 3 pc YoY. Own some category leading brands - Everyouth, SugarFree, Glucon D, Nycil. Also own - Complain ( no 3 in its category )

US business - 44 pc. Grew 9 pc YoY. Filed 4 new ANDAs. Launched Indomethacin suppository in Q2 - granted 180 days exclusivity

EM + EU - 10 pc. Grew 17 pc YoY in Q2

APIs - 3 pc

Alliances - 1 pc

Other comments -

Company has already launched 13 Biosimilars in India

Acquired UK based LiqMeds group - for a total consideration of 690 cr. LiqMeds specialises in Oral Liquid dosage forms mostly targeted at geriatric and pediatric patients

LiqMeds has 05 - 505 b(2) approved products in US to be commercialised in future. Also has 16 approved products in UK - yet to launch most of them

Zydus has a 505 b(2) approval for Sitaglaptin. The company has exclusivity for the foreseeable future. However, since it’s not a substitutable product, it will take time for the company to ramp it up. Since it is not a generic approval, don’t see any pricing pressure

Speciality products in US / Europe - company focussing on rare/orphan disease and other unmet needs. Company already has approval for 01 product - NULIBERY - an injectable used to prevent mortality in a rare paediatric disorder. Another asset/product is awaiting approval. Aim to acquire at least 2 more products ( late stage / awaiting commercialisation ) going forward. Aim to scale this speciality business to $ 100 million kind of annual sales run rate in medium term (next 3 yrs). Also have 02 more products under own development

Revlimid sales shall accrue to the company only in Q1, Q4 every year till FY 26. Gross margins in Q2 were strong despite NIL sales from Revlimid

Company is building in one competitor for this FY and one more competitor by next FY for its product - ASOCOL in US

Very likely to clock double digit growth in US business in this FY

Company has 6500 MRs in India. Likely to add more in next FY

Lower RM costs have helped company’s Gross Margins

Launching 02 transdermal products in US in this FY. Likely to add 02 more in the next FY. Also expected to launch 01 exclusive product/yr for FY 25,26,27 subject to approvals, litigations etc

Disc: hold a small tracking position. Will add only if there are triggers like successful speciality / exclusive launches. Biased. Not SEBI registered

Zydus Lifesciences ( Very Bullish commentary and important business developments ) -

Q3 results and concall highlights -

Sales - 4505 vs 4257 cr

Gross margins @ 67 vs 64 pc

EBITDA - 1102 vs 956 cr ( margins @ 24.5 vs 22.5 pc )

R&D expenses at 314 vs 344 cr ( @ 7 pc vs 8 pc of sales )

PAT - 789 vs 622 cr

Q3 Capex @ 213 cr. 9M FY 24 capex @ 650 cr

Region wise performance -

India -

Sales @ 1427 vs 1231 cr, up 16 pc

Branded India business and new Innovative portfolio grew strongly. Witnessed strong growth in Cardiac, Anti-Infective and Anti-Diabetic portfolio

Continue to maintain leadership in Nephrology

Company has 8 brands in top 300 brands in India. Also has a commercial portfolio of 13 Biosimilars in India. Has 09 more biosimilar molecules in pipeline

Company has also commercialised 03 NCEs in India - Saroglitazar ( for NAFLD ), Twinrab ( a biologic drug used for treatment in Rabies ) and Desidustat ( for Anemia )

India - FMCG segment -

Sales @ 397 vs 412 cr

FMCG segment witnessed weak demand scenario

Everyouth, Nycil - witnessed strong growth

Sugarfree, Nycil, Glucon D, Everyouth (peel-off) maintained their market leadership positions

US formulations -

Sales @ 1842 vs 1925 cr

Base business saw strong volume growth. Launched 11 new products including - ZITUVIA ( a 505(b)(2) product )

Emerging Markets -

Sales @ 493 vs 378 cr

Witnessed strong growth in Asia Pacific, Africa and Europe

Innovation -

Commenced phase II trials for ZYIL 1 for Parkinson’s. Phase II trials are also on for this molecule in India for ALS ( a rare neurodegenerative disease )

Completed phase II trials in India for ZY9489, an anti-malarial drug

NCE - Saroglitazar Magnesium ( already approved in India for non-alcoholic fatty lever disease ) - commenced recruitment of patients for Phase II trials in US

Completed asset transfer of CUTX - 101, a Copper Histidinate product for treatment of Menkes Disease. Rolling out NDA application for the same in US

Company is presently in the process of adding 700 MRs in India to accelerate the formulations business. Full effects should be visible by Q1 FY 25

Acquisition of LiqMeds ( a UK based company ) specialising in Oral Liquid formulations - Zydus Life acquired LiqMeds in Oct 23 for 700 cr plus yearly payouts till FY 26 on achievement of certain performance liked milestones. It’s already a profitable business. Most of their products are based on 505(b)(2) opportunities. The business is expected to scale up over next 1-2 yrs

All three NCEs launched in India are doing really well. Company expects, Saroglitazar to become its biggest brand in times to come !!!

Company expects a slow pickup for ZITUVIA in US. It’s an important launch for the company. Should add significant value in FY 25

Company continues to enjoy exclusivity for Asacol ( used to treat inflammatory bowel diseases ) in US mkts

Company reported strong numbers and healthy margins even without Revlimid sales in Q3. Revlimid sales are expected to be recorded in Q4 and Q1 FY 25

Have a good pipeline of exiting launches in US till FY 27

EM business momentum is likely to sustain going fwd. Likely to keep growing in double digits

Company has launched a bunch of transdermal products in US in FY 24. Over next 2-3 yrs, these can generate 400 - 500 cr topline for the company

Disc: holding, inclined to add more, biased

Can anyone suggest, what is the quantum of Zydus sales from Asacol?

Zydus Lifesciences -

Q4 and FY 24 results and concall highlights -

Q4 outcomes -

Revenues - 5533 vs 5010 cr, up 10 pc

Gross Profit - 3922 vs 3314 cr ( margins @ 71 vs 66 pc )

EBITDA - 1630 vs 1255 cr, up 30 pc ( margins @ 29 vs 25 cr )

PAT - 1182 vs 879 cr, up 32 pc

FY 24 outcomes -

Revenues - 19547 vs 17237 cr

Gross Profit - 13319 vs 10927 cr ( margins @ 68 vs 64 pc - big improvement )

EBITDA - 5384 vs 3859 cr ( margins @ 27 vs 22 pc - big improvement )

PAT - 3873 vs 2564 cr

R&D spends - 1309 cr @ 6.7 pc of sales

Capex spends - 862 cr

Segmental breakup of revenues -

India branded generics - 5369 vs 4911 cr, up 9 pc

Share from chornic therapies @ 41 pc

9 brands with sales > 100 cr

11 brands with sales between 50-100 cr

India consumer wellness - 2301 vs 2233 cr, up 3pc

Gross margins of consumer business expanded by 377 bps

Growth driven by brands like - Everyouth and Nycil

US formulations - 8685 vs 7445 cr, up 16 pc

Launched 5 new products in US in FY 24

Base business grew sequentially every qtr driven by volume growth

Europe and EMs - 1929 vs 1579 cr, up 22 pc

Demand scenario remained strong across key emerging mkts and Europe

Updates on innovations -

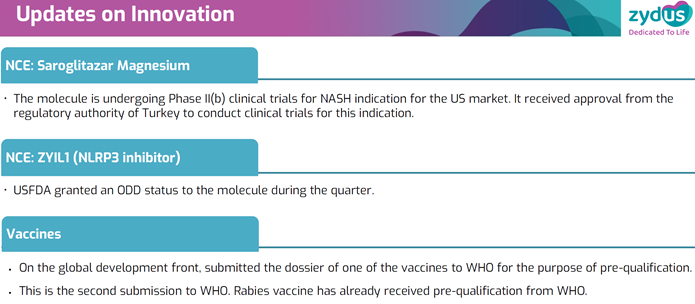

NCE - Saroglitazar Magnesium - recruited patients for phase - II(b)/III trials for PBC indication. Phase - II(b) trials for NASH indication are advancing as planned

NCE - Unsoflast - Phase II clinical trials are on for ALS indication. Also received USFDA approval to commence phase II trials iro same molecule for Parkinson’s

NCE - Desidustat - to treat Anemia in patients with Chronic Kidney Disease is expected to be granted NDA approval in China. Company has entered in an out licensing deal with China Medical Systems ltd to sell the drug in China. If the approval is received, it can potentially be a big product for the company as China is a large mkt

Company has already commercialised Desidustat and Saroglitazar in India. Both are growing well in India

Company retained its leadership in Nephrology therapy in India. In Onco, company was one of the fastest growing in India in FY 24

Company expects all its businesses to maintain double digit growth rates in FY 25 with EBITDA margins > 27 pc ( after factoring in competition for Asacol in US )

Expected to launch 30+ products in US in FY 25

Acquisition of Zokinvi ( used to treat Progeria ), scale up of LiqMeds speciality portfolio ( acquired LY ), scale up of animal health business and their pipeline of transdermal products in US should keep the growth momentum going in US

If all goes well, expecting to receive a USFDA’s NDA approval for Saroglitazar by Q2/Q3 in next FY and a potential launch in FY 27

Disc: holding, biased, not SEBI registered

Today I was analysing this company and here are my Notes

Company is confident of growing top line by 25+% this year ( 2024-25) and the EBIT margin is

going to do slightly better on a hight number of 29.5% already.

US and America are the major markets and it would stay like this , expansion to emerging

markets have started , planning to enter Europe as well.

Not keen on Generic medicines even for India thought there is growth as there is high competition and associated low margins.

Acquired LiqMeds ( from UK that can continue to focus or rear disease) , Acquired Zokinvy and it is produced by Eiger BioPharmaceuticals ( zydus is the only company that has rights to produce this medicine in the world )

Emerging / Developing markets are coming up well , introducing existing products there.

RnD Focus is on Saroglitazarv (fatty leaver disease), Desidustat (Chronic Kidney disease for

china market ), CUTX101 (Menkes disease)

Working with Accenture for ERP , Supply Chain Digitalisation with Pando are driving the

efficiency measures and helping secure good EBIT Margins.

My concerns

Ps : At the time of this post I am invested in this company .

@Aakash_Suresh Kindly dwelve on current valuation of the company also for fresh entry. Thanks

valuation is tricky I am not an advisor ![]() , I use DFC with my own growth numbers and terminal multiples and I see that for me its undervalued but I do not know how it al turns out .

, I use DFC with my own growth numbers and terminal multiples and I see that for me its undervalued but I do not know how it al turns out .

Zydus Lifesciences secures US FDA approval for generic Valbenazine

The company has received final approval to market its generic version of Valbenazine capsules in the US. This drug is used to treat tardive dyskinesia. Production will take place at its Ahmedabad facility.

Any view on the surprsing price action in Zydus? Stock is down 12% despite stellar results plus news of MSCI inclusion (although it was expected since a month). It’s not even as if it is extremely overvalued (major large cap pharma are in 25-40X P/E band). While Q1 margins are non sustainable but management has guided 28-29% for entire year.

Any news on USFDA front or something expected?

Zydus Lifesciences -

Q1 concall and results highlights -

Revenues- 6207 vs 5139 cr, up 21 pc

Gross Profits- 4621 vs 3465 cr (margins @ 74 vs 68 pc)

EBITDA- 2084 vs 1505 cr, up 38 pc ( margins @ 33 vs 30 pc )

PAT- 1419 vs 1101 cr

R&D expenses @ 392 vs 323 cr ( @ 6.3 pc of sales )

Organic Capex @ 301 cr

Net Cash on books @ 1892 cr

Company deleveraged its balance sheet by paying down the entire debt on books

Geography wise business breakup -

US - 51 pc of sales, up 26 pc. Launched 07 new products. New launches include second 505(b)(2) product - Zituvimet - should be a meaningful product for next 3-5 yrs

India formulations - 23 pc of sales , up 13 pc. Launched 10 new products ( including line extensions ) with 3 - first in India launches. Retained leadership in Nephrology, remained fastest growing company in Oncology

Share of Chronic portfolio in India formulations @ 42 pc ( up from 38 pc - 3 yrs back )

9 brands with sales > 100 cr

11 brands with sales between 50-100 cr

India Consumer wellness - 14 pc of sales, up 21 pc - driven by 17 pc volume growth

Europe and RoW formulations - 10 pc of sales, up 9 pc

APIs - 2 pc of sales, up 2 pc

Two of company’s Injectable facilities in Gujarat are under OAI classification by US FDA - a key monitorable

Q1 was exceptionally good Qtr wrt EBITDA margins. Looking to clock 28-29 pc EBITDA margins for full FY 25

Management is confident of delivering high teens topline growth in FY 25

Guiding for a full year R&D expenses of around 8 pc of sales for FY 25

Revlimid sales in US in Q1 were higher vs Q4. Also, there was a ramp up in the base business as well

Expecting to launch 25 new products in US in FY 25

Aim to use the cash on books towards building a speciality business in both US and India

Company is confident of clocking double digit revenue growth with increased / enhanced profitability in the Europe + RoW business for next 3-5 yrs. Aiming to enter more geographies and introducing new products here

Hopeful of launching Saroglitazar in US sometime in FY 27. Along with Saroglitazar, company hopes to acquire another commercial NCE asset ( in the orphan drug space ) which can be launched along with Saroglitazar so that the company’s front end can be be used effectively

Company believes that their product line up and some product settlements that are lined up in next 1-2 yrs, should allow them to keep growing even in FY 27 ( once the Revlimid opportunity is over at the end of FY 26 ). If the management is able to grow the business in FY 27/ 28 ( despite Revlimid opportunity in the base ) - that would be a big achievement - IMHO

Disc: holding from lower levels, biased, not SEBI registered, not a buy / sell recommendation

Zydus Lifesciences -

Q2 FY 25 results and concall highlights -

Revenues - 5237 vs 4368 cr, up 20 pc

EBITDA - 1461 vs 1146 cr, up 27 pc ( margins @ 27.9 vs 26.2 pc )

PAT - 911 vs 800 cr, up 14 pc ( due increased tax rate )

Geography wise sales breakup -

India formulations - 1456 cr, up 9 pc

India consumer wellness - 487 cr, up 12 pc

US formulations - 2416 vs 1864 cr, up 29 pc

International formulations - 538 vs 450 cr, up 19 pc

APIs - 119 vs 140 cr, down 15 pc

Others - 94 vs 34 cr, up 177 pc

Launched 12 new products in India in Q2. Out of these, 4 were first to mkt products

Share of chronic sales @ 42 pc vs 38 pc in FY 21

Consumer wellness business registered 8 pc volume growth

Zydus Wellness ( company’s subsidiary ) acquired - Naturell Pvt Ltd in Q2 ( for 390 cr ). It manufactures and sells Nutrition bars, protein cookies, protein chips and other health foods

Q2 capex @ 301 cr. Q1 capex spends were @ 302 cr

Cash on books @ 2590 cr

In India, 10 of company’s brands have sales > 100 cr. Another 21 brands have sales between 50-100 cr

Launched 4 new products in US in Q2. Filed 8 ANDAs and received 9 approvals ( including 3 tentative approvals )

Share of chronic sales @ 42 pc vs 38 pc in FY 21

Consumer wellness business registered 8 pc volume growth

Company acquired - Naturell Pvt Ltd in Q2. It manufactures and sells Nutrition bars, protein cookies, protein chips and other health foods

Q2 capex @ 301 cr. Q1 capex spends were @ 302 cr

Cash on books @ 2590 cr

In India, 10 of company’s brands have sales > 100 cr. Another 21 brands have sales between 50-100 cr

Launched 4 new products in US in Q2. Filed 8 ANDAs and received 9 approvals ( including 3 tentative approvals )

Entered into an exclusive licensing and supply agreement with Viwit Pharma for 02 - Gadolinium based MRI - contrast agents - to be supplied in the US mkts. These are injectables - used to increase the visibility of organs during MRI procedures. This is a niche but valuable drug. There r no generics for this drug currently in the mkt

Updates on Innovation -

Saroglitazar Magnesium - Recruited patients for phase 3 trials for the indication - Primary biliary cholangitis

Unsoflast - Completed phase 2 trials in India for the Indication - ALS ( Amyotrophic Lateral Sclerosis )

Desidustat - Initiated phase 2 trials in US for Sickle cell disease

Received WHO approval for their TCV vaccine - ZYVAC ( to prevent Typhoid )

Company has acquired 50 pc stake in Sterling Biotech for 550 cr. Currently setting up state of the art manufacturing facility to produce fermented animal free proteins. Also acquired sterling Bio’s API business that manufactures fermentation based APIs like - Lovastatin, Daunorubicin, Doxorubicin and Epirubicin

During the Qtr, 02 of company’s facilities were inspected by US FDA - Injectables facility at Jarod received a warning letter ( a key negative ), Ahmedabad SEZ facility successfully completed the inspection and received an EIR with a VAI status

Guiding for an R&D expense of 8 pc of topline for full FY 25 - a key positive ( IMO )

Maintaining high teens topline growth guidance with EBITDA margins > FY 24 margins for FY 25 ( likely to exceed their guidance )

Naturell Pvt ltd currently does an annual sales of 130 cr

Mirabegron sales in US continue to remain strong - which is why the gross margins are holding up > 70 pc despite Revlimid not contributing in Q2 ( Revlimid sales happen only in Q1 and Q4 )

Sales and pricing of Asacol are likely to get adversly affected wef Q3 { as the competitor (Teva) ramps up their product }. Zydus was the only generic for Asacol in the US mkt for quite some time now

Opportunities like - Palbociclib ( breast cancer drug ) and Riociguat ( for treatment of pulmonary arterial hypertension ) and Cabizantinib ( used to treat thyroid cancer ) generics should help them offset the loss of exclusivity on Revlimid ( to a large extent ) wef Jan 26. Company is also looking to file and launch a few more 505(b)(2) opportunities immediately. On both - Palbociclib and Riociguat - company is expected to get exclusivity for meaningful time period

Hopeful of getting a WHO approval for their MR ( measles and rubella ) Vaccine as well. Both these vaccines ( MR + TCV ) should bring in sizeable business for the company as UNICEF buys them in bulk every year ( to the tune of 8-10 cr doses ). Scale up should begin sometime in FY 26. Even if they get a fraction of this business - it can be very significant business for the company

Despite loss of exclusivity on Asacol, company is confident of growing their US business in FY 26 over FY 25

Company has won a US govt tender for supply of Sitagliptin for a 3 yr period starting next FY. This should be valuable business for the company. Company will also sell Sitagliptin in US through the 505(b)(2) route for FY 26 before it goes generic in FY 27

Company has a healthy pipeline of Transdermal and complex Injectable products to be launched in US - these should help them sustain the business momentum in the US mkt

Key things to watch out for in the Indian innovative portfolio of the company for the near future should be their mkt share in products like - Saroglitazar, Desidustat and the Biologics that the company is launching. Company’s mkt share - both in volumes and value for Ujvira ( Trastuzunab - for treatment of breast cancer ) is now higher than the innovator

Company aspires to take Saroglitazar and Desidustat to among top 50 products in IPM

If Saroglitazar is approved in US as per the expected timelines, company should be launching it in Q1 FY 28 or so

Disc: holding, biased, inclined to add more, not SEBI registered, not a buy/sell recommendation

have you looked into kind of revenue their NCE portfolio can bring in if all three are approved. Any timelines have been given for when phase 3 trials will be completed.

Thanks. Invested.

Major revenue drivers for future in USA will be

In NCE Front:

Disc: Invested, will add more