See it depends on growth rate but buying extremely expensive valuation would be too risky for retail investors and from my 8 years of experience you always get time to invest in correct valuation this because you have seen from Covid was growth into another level , see you will get the opportunities correct valuation is important take example of trend only it went to 7300 all time high and people who have invested have regretted till now so don’t directly jump into conclusion first’ do your research and then do read research reports of that company by analyst and then you can take risk but very exceptional cases are where growth sustain for higher PE of it’s getting re rated then it’s good so you have to do research otherwise wait for some time market has ample of opportunities, and it take to cool off

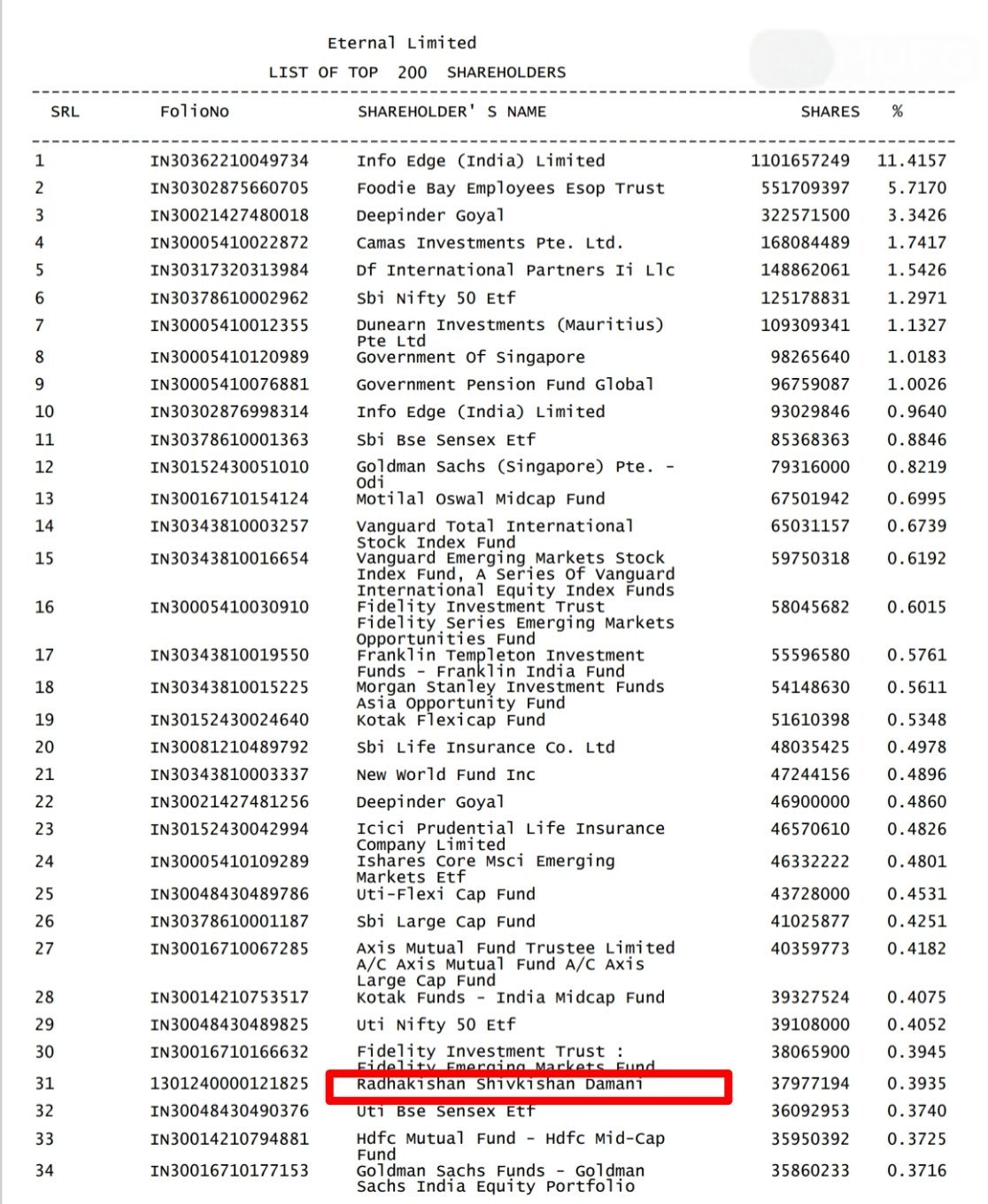

Radhakishan Damani has just taken a stake in Eternal…I think we can all agree that if Radhakishan Damani has entered he is not entering to earn 20-30% return on investment…I believe Eternal’s story has just begun.

Discl:Invested and biased.

I might be wrong in analysis but if I do the math:

RK Dhamani Net worth (2025) : 1870 cr USD ~ 1.64 Lakh Cr

His stake in Eternal using this table: 1250 Cr

So, overall, his is betting just ~0.75% of his portfolio in it. So, obviously it is not a strong bet,right?

Happy to learn if there is any other perspective from which this should be looked.

R K Damani is the promoter of Dmart so therefore most of his networth comes from dmart… dont know whether you can calculate the size of bet by dividing by networth…a more accurate measurement would be if you remove the Dmart stake and calculate Zomato as a percentage of the rest of his investments… To give you some context R K Damani’s second largest holding after Dmart is Trent which is close to 2000 cr…so Eternal is a sizable bet considering it is 1250 cr.

Why is so much importance being given to someone who has entered this stock so late ? In fact it’s a poor decision to have not entered so long.

Disclosure - Entered from Rs 50, Top 3 holding.

While I do think zomato and blinkit are good brands. There isn’t anything valuable about them to the consumer. The same product can be bought from four other apps at probably a lesser price. Now, hyperpure and District have some uniqueness to them

Disagree. Atleast Blinkit has a supply chain/logistics advantage simply because of the dark stores they’ve opened in strategic locations where there’s little space left for more. I have one close to my society and it delivers in just 5 minutes. Swiggy Instamart takes 10-15 mins.

While supply chain can be a moat. It is probably a minor one. Amazon/Flipkart/Jio with their deep pockets can def open more dark stores(of course execution does matter which Reliance doesn’t possess). Also, if the product is delivered in sub 15 min, I don’t think it would matter to the consumer whether it was 5 or 15 as much as the discount/product availability would

Dark stores are not created overnight, definitely not in places with dense population. What Blinkit has done well is to accelerate the Dark Stores tie up before competition. Despite deep pockets, competition has to wait till alternative sites are available, suitable to their standards.

Eternal q2 results were quite good.

Some positives:-

Food delivery nov grew 14% yoy, quick commerce nov grew 137% yoy, and going out nov grew 32% yoy.

Consolidated adjusted revenue grew 172% yoy, however after adjustment for inventory led model. actual consolidated revenue grew by 65% which is still a healthy number.

Will reach 2100 stores by Dec 2025 versus earlier estimates of 2000 and 3000 stores target by March 2027.

Seeing the growth in nov of quick commerce, one can assume that they have further gained market share.

Food delivery adjusted margin came in at 5.3% of nov which remains within their guided range.

Some negatives:-

Quick commerce adjusted ebitda margins came in at -1.3% of nov , lower than -1.6% reported last qtr but still far away from breakeven and eventually profitably. Mgmt has said this might take longer due to investment in higher marketing spends as well as accelerated store expansion.

Food delivery growth will take time to pick up, might be slower than earlier anticipated.

my worry is, at this rate how many years it might take for the PE ratio to come down to acceptable levels, like say under 100?

Hi so as far as calculations go…most of zomato’s business has shifted from marketplace model to inventory model…so if we consider the revenue of current quarter to be the new normal…revenue for the whole year comes out to be jun: 7167, sep:13590, dec:13590, mar: 13590…total revenue for the year :- 47937 crores. Consider zomato grows by 50% as a whole which is conservative considering 100% nov growth in qc for the next 2 years. Revenue after two years= 107859 crores. Most of the earlier dark stores have reported 3%+ adjusted ebitda margins and 5% is the stable long term guided ebitda margins. If we consider 5% ebitda margins on this we get 5392 crores. Add other income of 300 crores = 5692 remove interest of 100 crores= 5592 crores, remove depreciation of 500 crores = 5092 crores…remove tax of 24%= 3869 crores pat. PE comes out to be 84 on a 2 year fwd basis. All these numbers are conservative and I’m pretty sure revenue numbers will be much higher considering I have not done calculations for each business seperately.

Discl:- Invested and biased.

How?

| Blinkit | Revenue | YoY Growth | EBITDA% | EBITDA |

|---|---|---|---|---|

| FY26 | 45000 | |||

| FY27 | 90000 | 100% | 1% | 900 |

| FY28 | 180000 | 100% | 3% | 5400 |

| FY29 | 315000 | 75% | 4.50% | 14175 |

At 14k cr EBITDA, add another 3-4k Cr from Zomato. Eternal is at around 18k Cr EBITDA implying a 20x FY29 EBITDA valuation.

Not cheap, I agree. But if you stretch these numbers again for another 2-3 years, it’ll start looking like a bargain buy.

Also, the thing with companies like Eternal is they will continue to innovate and build muscle. That 20k cr cash on books will ultimately be put to good use.

I agree…your assumptions can be different than mine …personally i keep revenue growth conservative…you have increased the revenue…I have kept ebitda at 5% after two years…both of our absolute ebitda number is almost similiar…anyways my point is the same…this company has potential and will innovate in ways we cant comprehend currently…any company which grows at 50%+ for 3-5 years will create wealth one way or the other. Cheers! ( Done valuation as a multiple of PE , you have done on EV/EBITDA basis both are good)

Discl:Invested and biased.

Just one basic question on the above estimated sales for FY29, how much capital is required to generate the above number and from where they are going to get the capital??

The above question is based on, as I read above they changed the Blinket QC business to inventory led business model ???

Sharing an observation here

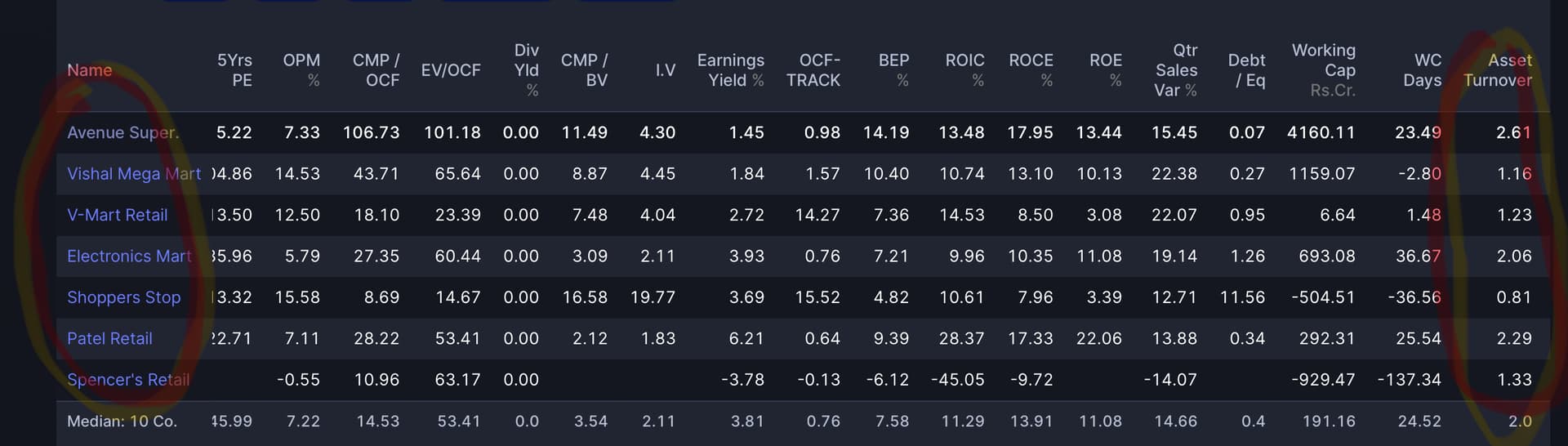

- Dmart operates at 14.5-15% gross margin, with 7-7.5% expense and Remaining 7.5% flowing to EBITDA.

- This margin is a function of the category of products you sell.

If we look at current Blinkit’s cost structures:

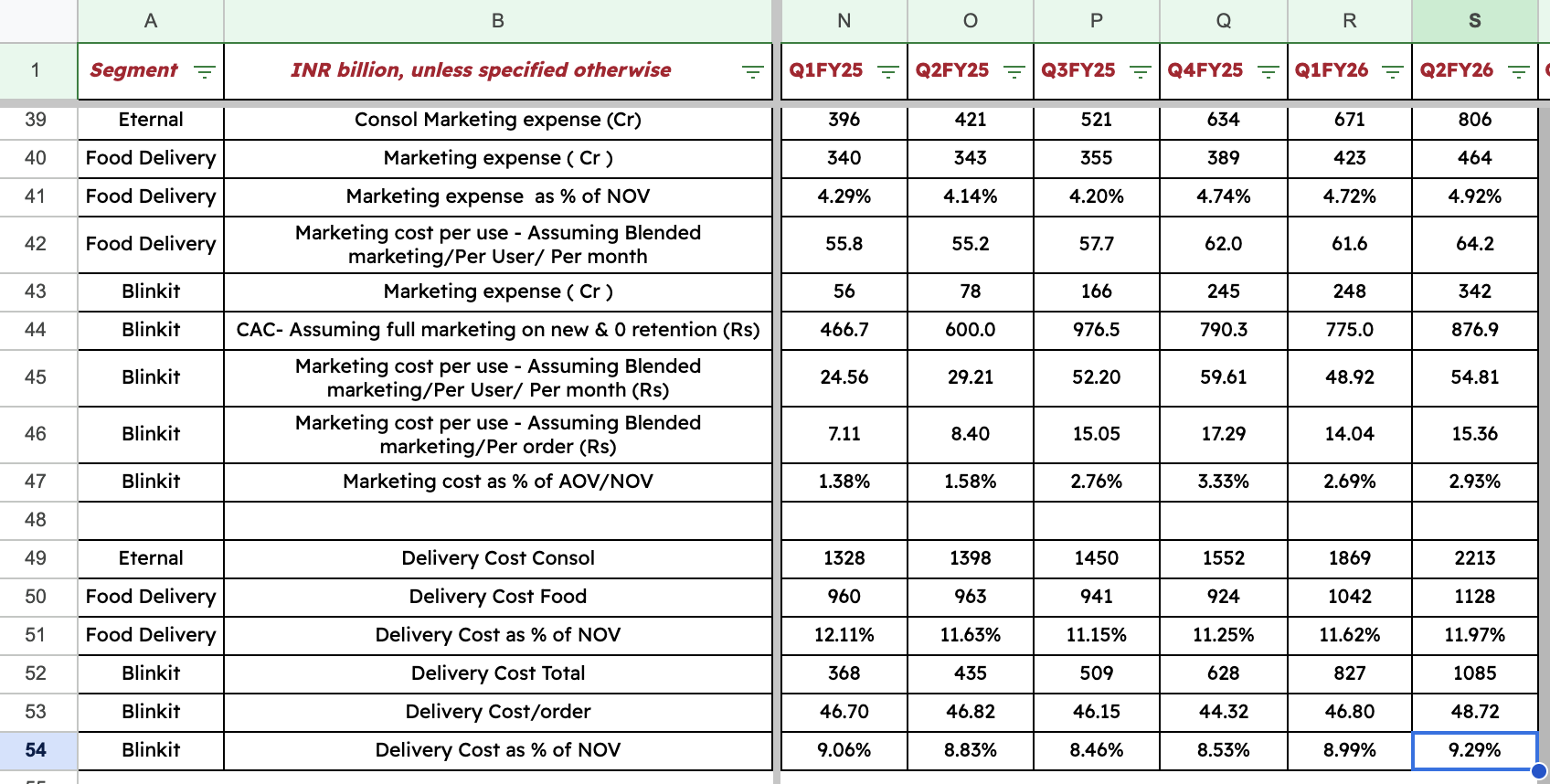

- Delivery cost as a % of NOV stands at 9% i.e 9 Rs spent on delivery for a 100rs order. [Row 54 in the image shared]

- Marketing cost as a % of NOV stands at 2.9% [Row 47 in the image shared]

- This marketing cost is a function of both New user acquisitions & retaining existing users. I believe this will stabilise at >1% of NOV at steady state.

on top of this, there is employee cost, store opex, rent etc.

Blinkit has guided for 4-5% of EBITDA on a steady state. This is only possible if Blinkit operates at 20%-25% Gross margins.

Inorder to achieve this EBITDA target they have to:

- Increases their AOV from 520’s to higher number by increasing high AOV assortments[like fashion]

- Start own brands/buying brands for expanding margins.

- Starting to own the dark stores on their books and cutting down the rental costs.

- Pump more working capital into the business and flood the vendors with advances for deep discounts.

1st & 4th item is already in play. & 2,3 are possible eventualities for increasing margins- which require a lot of cash & Blinkit have it.

Summary: Qcom is a super hard business to achieve that 4-5% EBITDA level. There is no place for No-2 here in current market economics [Only way for no:2 to survive is to limit the business to top 8 metros & going deep]

Sharing KPI tracker here for reference: Google sheets link

To achieve a revenue target of ₹3,15,000 crore, Blinkit would require a network of at least 15,000 dark stores. As of now, they operate 1,816 dark stores, with a goal to reach 2,100 by year-end. This implies they need to open approximately 12,900 new dark stores over the next 4 years.

Capex & Working Capital Requirements:

- Estimated capex per dark store: ₹1.2 crore

- Total capex for 12,900 stores: ~₹15,480 crore

- Assuming a 5% working capital requirement, the business would need an additional ₹15,000+ crore to support operations at scale.

Strategic Levers for Margin Expansion:

To improve unit economics and drive profitability, Blinkit could:

- Launch private label brands to capture higher margins

- Expand into higher Average Order Value (AOV) categories (e.g., electronics, personal care, premium groceries)

Financial Position:

- Current consolidated cash balance: ₹18,314 crore

I’m keeping revenue projections on the conservative side, given the scale and execution risk. But if they pull this off —this could be high growth ,high capex, long-term opportunity at a fair valuation.

@_atharav, Just to continue the discussion:

Let’s convert the above estimates into unit economics:

Total dark stores:15000 Nos., (also what is the basis/assumption for this number???)

Total Capex: 1.2x15000x1.05 =18,900 Crs

Per Dark store = 18900/15000 =1.26 Cr

Total Revenue = 315000 Cr

Per Dark store Revenue = 315000/15000=21Cr

Per Dark store Asset Turn over = 21/1.26 =16.667 ~ lets say 16, Very very high if we compare with retailers. off course both business models are different, still, if they can manage it will be very extra ordinary.

By the way from screener shows present working capital is 9100Crs +, off course this is for the entire business, I don’t know how much is for Blinket as on today.

so the assumption of 5% working capital that is 1.2* 15000* 0.05 =900 Crs seems very very less , to generate 315000 Crs revenue.

Am I missing some thing here.

management have explain in previous earning call why they required lower working capital then traditional players . I have personally agree on that why i think they have higher asset turnover ratio.

Eternal CFO Akshant Goyal had noted in a previous earnings call that if Blinkit fully owned its inventory in FY25, the working capital required would have been under ₹1,000 crore, which is about 3-5% of Blinkit’s gross order value.

5pc working capital is 5% of 3.15L cr which works out to 16k crores