Some of my thoughts, with all due respect to all the views and analyst who has way more knowledge than me.

Zomato is executing very well

It is profitable atleast

I track the MF investments, I see lot of MF guys are buying it, even though the high PE (They are for sure smarter than me )

Almost all players are burning cash to catch the eyeballs (So i guess if I have to choose between ‘bad’ and ‘worst’ I will choose ‘bad’)

My thesis is this ‘mindset’ rather than a company (of Indian Wives atleast)

- In small towns people say ‘zomato’ karale (means online ordering synonym is zomato like ‘google it’

Vijay sir says right chase the story

I know these points does not make a lot of sense from fundamental valuation perspective

Disc: Invested a small portion of my PF just because of high valuation

So the Q1FY26 results are out and its a 70% increase in revenues QoQ and 22% up from previous quarter driven by blinkit.

I thought of blinkit as an okayish business because I dont think zomato cant keep charging those exorbitant commissions on the products listed on blinkit from suppliers and pass it onto price sensitive customers in such a highly competitive environment but with their recent shift to a inventory-led model they might be onto something. They haven’t clarified but I think that they might be capitalising the data they have of the user order patterns and stocking up inventory accordingly. This would lead to high turnover of the inventory and less loss due to overstocking. This could significantly improve margins and if they launch their in house brands, it could be hugely profitable just like kirkland of costco. I m just taking a wild guess here but need to wait for earnings call for more clarification.

Dont know about profitability, how to judge the unit economics and then value the business. So if someone can explain the valuations it would be great.

I am surprised by how positively everyone is reacting to blinkit result. There are multiple players with deep pockets who potentially can out compete Blinkit.

There is a possibility that Blinkit can come out as a winner, but this is never a conclusion. The current market price has factored in future profitability + sustained growth.

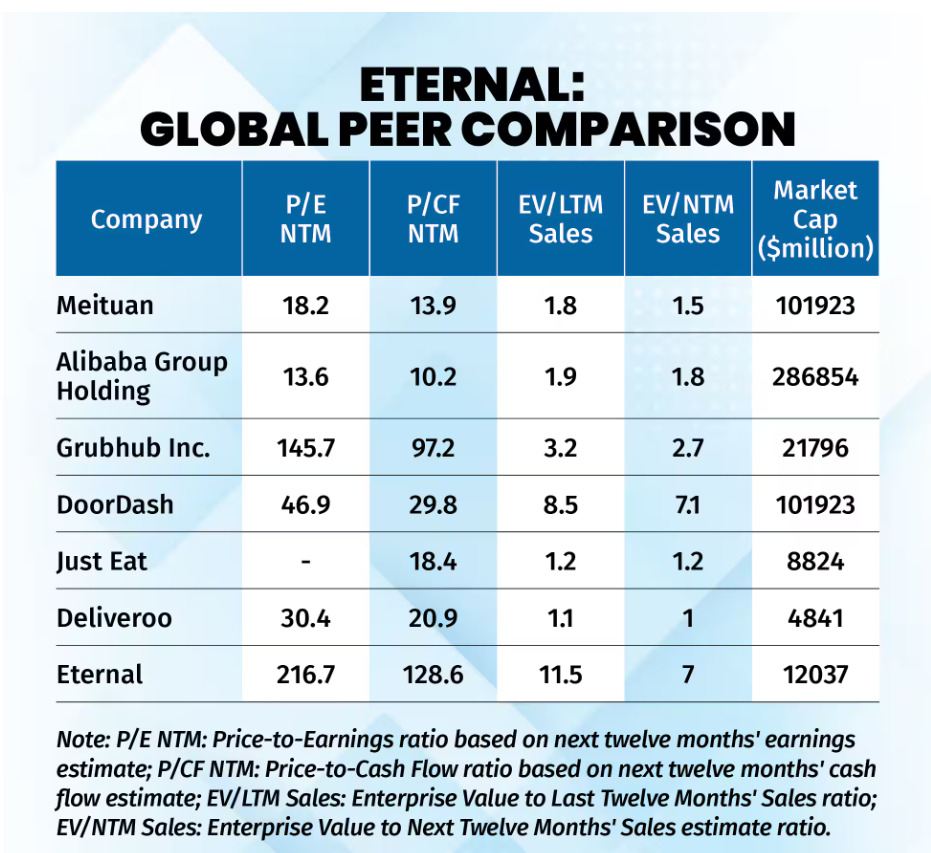

This is how eternal compares with its global peers.

Plot the growth rates of each player in another column and you’ll know why Zomato trades at a certain valuation.

Secondly, the runway for Eternal even from here is huge - they’re at 40k Cr GOV. Indian retail market is atleast 20x of that size. They can keep growing at 60/70% for atleast 5 years I feel.

Right now, Eternal only list Material Cost and Employee cost as expenses. Since, Eternal plans to shift to first party model, there will be added expense of Dark store rentals, this costs now sits on Balance sheet of Third parties.

That is exactly my point. Market has already priced in best case scenario (flawless execution, favourable enviornment). That too for next 5 years. Sustaining same growth rate for next 5 years is not easy given one or more of big giants can disrupt (Amazon, Jio, Flipkart, Tatas) and existing competition as well. Retail is too large a market for others to ignore.

And doing this at 4% EBITDA, something no one has been able to execute till now.

30x FY30 EBITDA is by no means cheap.

So current price has already factored in super best case scenario. No more upside left here and there is chances of huge downside.

IMO, they may not be able to defend their market share in the next few years

Note that in a value conscioius country like India, discounts and deep pockets will sway the market share. In the long run, its hard for any one to compete with Jio or Amazon in this space

Agree with your view that sustaining this level of growth is going to be difficult and market is pricing the bull case scenario.

However, I dont have doubts that any other big giants can disrupt zomato. Zomato’s execution if amazing and I feel their management is also hungry. My concern is how big the market is? I am not able to estimate the industry growth.

Disc: Invested but sold half of my earnings recently.

You have the right to be a pessimist and I have the right to be an optimist. We will see how Eternal executes and proves whom wrong

My thesis is simple:-

Amazon, FK, RIL, Tatas have all given up on this space in a meaningful manner.

You can’t build hyperlocal just with money. Capabilities are required at hyperlocal level. Not easy to build from scratch.

Blinkit is at k 44kCr GOV run rate and expanding fast in T2, T3 and T4 cities thereby capturing the complete low ticketed high-repeat consumption in any household. Only major categories left after a certain point would be fashion and some others.

Swiggy - its major competitor is seeing its cash reserves fall to 5k Cr with a quarterly burn of 1k Cr+ - I don’t expect Swiggy to expand as fast as Blinkit and that would mean Blinkit operating uncontested in a large number of markets, thus driving both - growth and profitability.

Cash optionality - 18k Cr cash on books with no cash burn. You don’t think they’d try their hands at other innovative businesses?

Valuations: 30x EBITDA isn’t cheap, agreed. But I’ve also been conservative in plotting only a 50/60% growth rate. Just to give you a statistic from their Q1FY26 letter - largest market of Blinkit i.e. Delhi grew 70%+ YoY for them.

I’m sure actual growth would be much much larger than what I’ve estimated. I’m not even fully baking in what District might become in future as society itself turns more experience oriented.

I also like this space, but prefer Swiggy over Zomato, purely based on how market is currently valuing the 2 companies.

Swiggy’s size is around 2/3rd of Zomato while market cap is 1/3rd. (GOV for food delivery ~2/3rd, while QC is 1/2). For QC, Instamart is 2/3rd of Blinkit on number of dark stores and pretty comparable in terms of mln sq ft of dark stores. Swiggy is also planning to liquidate stake in Rapido which would add to it’s cash balance (by ~1800 cr).

I agree that Zomato has shown splendid execution especially in Blinkit and is overall profitable. I believe Swiggy is also on the same path but with 2-3 quarter’s lag (guiding QC to breakeven in 2-4 quarters). Going forward, Zomato will continue to aggressively pursue growth in QC while Swiggy will now focus on profitability and opex/capex.

I fully agree that this QC industry has a secular growth runway for atleast a decade and both these companies will benefit and be the winners. Just that Zomato has run too much off late while Swiggy is a better proxy to play in this market given current valuation difference.

Blinkit’s pivot from a marketplace model to an inventory-led model has been key reason why their revenues are growing including 70% YoY growth in Delhi. Whatever was counted as GMV is now revenue. Earliler only take rate was revenue, now it is entire GMV They just need to extend this model to all their darkstores (and show continuous growth without real growth in GMV/marketshare)

Inventory-led models carry inherent risks (working capital, inventory write downs). But who cares, Market wants topline growth and they can deliver that despite competition. Please note that there can be no real increase in market share, despite that they can keep growing their topline. So flawlessness is deeply rooted in their strategy (and narrative). Execution is still optional to show the growth.

If you’re targeting 15% CAGR, Eternal’s share price needs to 2x in 5 years — a reasonable ask if they sustain momentum.

While it’s uncertain whether Eternal will become a ₹6 lakh crore company by 2030, they’ve successfully created the high growth narrative and the cult following which is supporting the current market price. That is all you need in today’s market.

Zomato market share by nmv:- 52%.

Swiggy market share by nmv:- 25%.

Zepto market share by nmv:- 23%.

Yet to see the so called competition by Amazon and flipkart that will destroy this players. Until then, the market will keep rewarding to those who perform well.

Agreed. Blinkit delivers to my society in 5 minutes as they have a store right behind our society.

Newer players can pump all the money they want but land is a limited commodity and first movers have a lifelong advantage.

If only it was so easy.. the value prop of apps aren’t pricing. It’s convenience. Otherwise people would have shifted to ONDC long ago. The article itself says that deliveries will be managed by restaurant partners or third party partners.. I will rest my case.

Blinkit, Zepto and Instamart all have 1,000-1,500 dark stores. Amazon probably has around 100-150 dark stores, while Flipkart might have 300 odd. So naturally these market share numbers are skewed in favour of larger incumbents and don’t really mean anything for now.

IMO, being the first mover does not give Blinkit a long-term edge over slow moving competition. There is very limited customer stickiness here, therefore slow movers can make more informed decisions by gaining insights into Blinkit’s order volumes, on-demand product categories, etc, at various locations.

Blinkit has already established dark stores in most of the rich areas in top cities. Future expansion into smaller towns would be riskier and yield lower profits per dark store due to lower spending power and tech adoption. A couple of years ago, Zomato pulled out of 200-300 smaller towns and cities due to lower traction and unviable financials.

Disc: Invested from much lower levels and trimmed holdings late last year.

I see a lot of back-and-forth on whether Eternal (Zomato) is overvalued or has years of growth ahead. Some argue it’s burning cash and valuations are unsustainable, while others point to Blinkit’s 70% YoY growth in Delhi, 52% food delivery market share, and the 18k Cr cash on books as proof that it’s executing really well.

My Thesis:

For me, technology is often a winner-takes-all play. The first movers who execute well, like Blinkit with its dark store network and speed advantage, tend to build a moat that’s not easy for late entrants like Amazon or Flipkart to replicate, even with deep pockets. Convenience and execution usually trump discounts in the long run.

There’s no single strategy in the market that makes all the money; everyone invests differently. My approach is to keep it simple:

Allocate 3–5% of my portfolio to such new-age stocks.

Keep a stop-loss to manage downside.

As conviction builds and I’m on good gains, trail a deeper stop-loss (30–35%) to protect profits while still riding the wave.

Examples from my experience:

Trent – The market kept rewarding it with a 150+ PE as long as growth was strong. When growth slowed in the last 2–3 quarters, the stock corrected. If you never entered because of “high valuation,” you’d have missed the run. My rule: add when results are strong, cut when they disappoint. Build gradually, cut or exit aggressively if the company disappoints or you find a better player in the same sector with better growth prospects and execution.

Dixon – Always considered “expensive,” yet it went from 2K to 20K (pre-split), corrected, and is back to 2K post split and now again near 20K. Margins are wafer-thin, but the company has continued to deliver and post growth, so the stock has performed well. Waiting forever for a “reasonable valuation” would’ve kept me out completely.

I could list more, but it’s off-topic, and the point is: the simpler your thesis, the fewer financial decisions you need to make. And the fewer the decisions, the fewer the mistakes.

That’s how I avoid getting stuck in endless debates on valuations, EBITDA multiples, or industry size. Instead, I just participate in the story with controlled risk and let execution decide whether Eternal ends up being one of those winner-take-all stories.

Disclosure: Invested with stoploss and max downside pre-decided.

)

)