This funding is meant to be spent slowly over time on various business items such as:

Setting up and operate warehousing/dark stores (for Blinkit, etc.)

Marketing and branding

Tech stack (software, cloud)

General business items (Wages etc)

But they are temporarily parking that money until it is all spent in:

Liquid fund, or mutual funds

Fixed deposits

G-secs, or Government Securities

Corporates deposits

Where they can at least earn some short term returns instead of in a bank account.

Is investing in mutual funds their business?

No, mutual fund investments is not their business.

Food delivery (Zomato), grocery delivery (Blinkit), and related tech/logistics platforms are still their core businesses (Eternal (Zomato)).

Any prudent business is going to invest a substantial sum of idle cash, knowing it is going to be used-- even if delayed.

Is this common?

Yes, this is typical with Treasury.

Like getting a bonus and putting it in a liquid account until you buy a car. Large companies simply do this with bigger funds.

Is This Secure?

Mostly yes:

They are investing in fixed deposits and low risk liquid funds.

ICRA is doing monitoring.

The reports showed no jumps or abuse of the declared use.

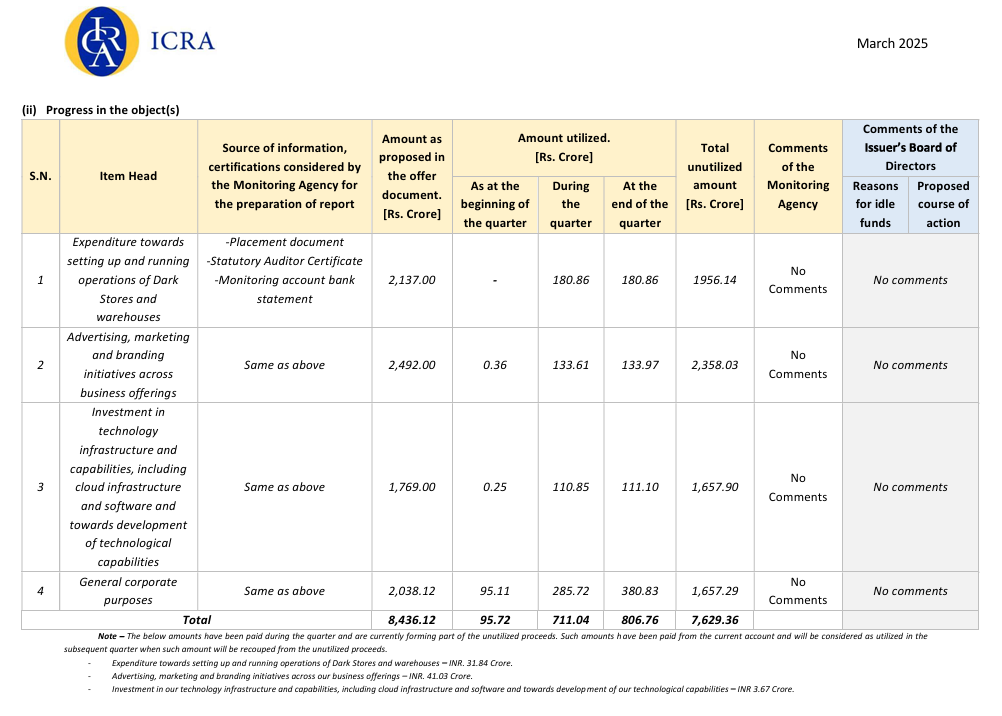

Eternal Ltd raised ₹8,500 crore in November 2024 through a Qualified Institutional Placement (QIP) in simple terms, they sold shares to large investors for capital which would contribute to their reserves while holding onto until they capex it for the business (thereby holding it in Treasuries or MF, as opposed to letting it die idle).

Their food delivery business is highly profitable…it is their qc business which is increasing losses due to which it may seem currently that most of their profits come from other income. However once qc business reaches steady state margin( 5% of gov) and food delivery business reaches maximum margin( 5.5%) , we can expect steady profits and cashflows( preferably by mid of next year since this year will go in capex). It is interesting to note that amazon followed a similiar path in late 90s where they kept on increasing market share , and at same time reported zero to very less profits.

Question is not investing in mutual funds, short term Trading in mutual funds, the amounts shown are nearly 5 times the amount raised, in yearly numbers.

Why raise so much money without concrete plans and do non core activities. It takes lot of top management bandwidth, as we are talking here Billions of Dollars.

Thank you for the detailed explanation. I guess this is how new age businesses are run now.

This shows that they have indeed spent the money on what it was intended for.

But this is only showing the amount of QIP proceeds.

Hope it was helpful.

How they got the money?

They got the money doing ipo and doing qip.

Why they invest in mutual fund?

They keep the money in liquid mutual funds. Earning intrest and very little risk with FD like return . Many companies do this who think they could need the money in immediate future.

Why they have such surplus?

because they want to be in position to have significant cash flow. As the environment is uncertain with tough competition .

Personally I don’t like the cash burning business but many do as they see potential. Since it has a potential to gain major share from unorganised business like grocery shops, restaurants etc. in high spending metro/urban areas.

Amazon is offering discounts currently to gain market share which doesn’t seem a sustainable strategy, since quick commerce is an execution heavy business. Also, zomato will soon turn into an iocc which will allow them to hold inventory which will lead to better margins than the likes of flipkart and amazon. Players like zepto and swiggy are offering discounts, burning cash with negative contribution margins while zomato has a positive cm offering least amount of discounts, this should be enough to tell you that discounts don’t work in this market.

Apart from probably first movers advantage, why is Blinkit able to grow with least discount compared to Zepto and Swiggy. where does Big basket stand among all these? For Amazon, its too early to comment on their long term strategy.

Like I said it is an execution heavy business…where the ui is better, apps which deliver faster gain market share. This is different from ecommerce where since the goods get delivered two to three days later, people spend a lot of time comparing discounts, while this is an instant purchase. Blinkit has consistently delivered a better user experience than zepto and swiggy instamart, you can check out their apps to see this. Bigbasket has 5-10 percent market share, whatever they are doing, not working currently.

NO, even if they have kinda same path, the big difference is amazon’s AWS which makes most of the money for the company, eternal currently does not have any high margin tech business. Plus amazon operated in a different socio economic market and eternal operates in a different market

I think it might be better than Amazon…blinkit has different levers like ad revenue, owning their own inventory, private labelling which when exercised could lead to massive profits for them. Currently the only reason they’re loss making is because of capex they have to incur in opening stores. Once the capex phase is over, mostly in a year, year and a half, you will see blinkit operating at a huge scale with decent profits and good cash flows being generated. Amazon on the other hand, had to work all through the 90s to generate a decent profit and they’re still loss making in india since they dont own inventory here in the ecommerce business.

im very skeptical about any of that happening too soon, zomato investors are mostly delusional and do anything to justify high valuations, the thing is their business model is flawed as it works on just giving offers, the only thing good is the advertising part where restaurants can pay them to rank higher. anyways no one is going to create any wealth at this market cap and such crazy valuations, i mean all the best 10xing your 2.2 lac cr market cap with 430+ PE and close to 28lakh other share holders.

Hearing the high PE argument since it was 40rs, now it is 240 and still the same. When will people move on from PEs and start understanding the business and growth prospects taking forward PE into account. Zomato stopped giving big discounts a long while back, can be seen in their contribution margins. Private labelling is a big opportunity close to 10 percent margins can be made there itself, owning inventory which zomato has already agreed to do will add another 1-2 percent margin. The grocery market in India is close to 800 billion dollars and growing rapidly along with the rest of the retail market. I guess it is true what they say, the pessimist sounds intelligent, while the optimist makes money.

If you search the shareholder letter for competition/competitive you’ll see those words pop up 15 times. This industry used to have fewer players, but now every big-name organization with deep pockets is jumping in. So, don’t expect the same kind of returns you got before—it’s a whole new game now.

yes nothing ever matters the pe does not matter,the roe,roce cash flow nothing,the only thing that matters is what the speculator believes right?.On a serious note,

Stock going from 40 to 240 is good, but price appreciations does not means it is fundamentaly good, meme stocks and bubbles also go up does not mean they have justified intrinsic value.Eternal run up shows momentum and big shareholder number shows speculative activities, the market cap at present means it has already discounted future profits and cash flow.

2.Forward PE is complete gueswork same as future cash flow,now nothing wrong in calculating that, but often built on management guidance or optimistic projections even forward PE in this case would be extreme,you do need to share what numbers you are expecting as i can be wrong big time.Plus there is genuinely no high margin business model like AWS visible.

3] I agree with margins improvement part but they have improved in a very modest way which is nice. the core food delivery secton is maturing and may face growth stagnation without future good discounts.

and as we all know blinkit still is negative ebitda and burns cash

4.about the private label thing,its still theoretical. Owning inventory increases working capital risk.and with ur 10% margin on items will not offset loses on core operations unless massive volumes are achieved,assuming they will achieve it as u said its a big big grocery market(TAM), the stock is already trading at that future value so the upsiode gets limited and downside is big{ talkijng about present situation}.

and the TAM is huge and growth is also 4-5% but it also comes with hyper competetive pplayers with much deeper pockets.

and last things last yes optimist do make money but you missed the catch of margin of safety, many optimist also lose money in such stocks,investing is also about combining vision with real numbers(quantitative). And yes money can be made in sustainable profits and defensible moats, not just stories.

but yes, Zomato is the next Amazon without profits,fcf and AWS riding on grocery delivery as its golden goose.for sure 10% margin on my shampoo and lays delivery will fund the multi trillion dollar empire.and yes the stock price went up, good thing buffet packed it up as valuation works on vibes and verticals,who needs profits when you got a chart breakout with 28 lakh shareholders manifesting optimism. with the number of shareholders its not even a stock anymore, its just a group therapy session with chart.

I entered this stock around Rs 45 and kept adding till it became my top 3 holding with average price 80-90. What I want to share is the thought process along the way.

The rationale initially was I saw huge opportunity in Food Delivery Growth with potential to grow in next cities. India has a huge population and some are lazy to cook or go out and eat. Home delivery addresses that segment in a big way.

Then Blinkit happened. While people debated Competition, for me they were snatching business from Kirana stores, so competition didn’t matter. Hence it was still a buy.

I kept adding as they started charging platform fees at Rs 3 and started increasing every quarter. I was sure upto Rs 10, customers won’t mind. This would boost profits.

One thing I was not sure of was economics of scale in FD, till it happened with me. I ordered two different items from different restaurants but the delivery boy was same. So they did have a model to club orders.

The bigger boys like Amazon made noise but didn’t jump in fully. So the positivity continued.

Then came what I closely follow. I look for management commentary where instead of explaining why they are doing well, they start sharing excuses which appears legitimate. That is my trigger to start selling.

Once they started giving explanations like Blinkit profitability will get pushed back due to cost of store additions, this was the time to start reducing. Also factoring in was many big players are now actually coming in which will increase discounts because there is hardly any brand loyalty in this space.

I have sold about a third of my holdings. My view is I am unlikely to double this stock even in a 2-3 year period.

Hope the rationale of Zomato journey is useful to some.

Disclosure - Invested. This is not a recommendation to either buy or sell.

I agree with some of your points. However I still feel there is ample growth left. They have set a dark store target of 2000 stores for this year and my assumption is by next year the dark store consolidation (industry consolidation) might happen among all the players since even flipkart is also opening 800 stores, zepto is opening some 1000 and swiggy also a similar number this year. Hence we see negative ebitda in quick commerce. This is not a story, but the truth of the overall business. There are quick commerce businesses like instacart globally who have made sustainable profits based on advertising income alone. My assumption is based on recent history that discounts don’t work and other ecommerce players who had 10 years to crack the traditional ecommerce model and make it profitable could’nt do so because they are unable to own inventory due to India’s FDI rules. So traditional players might have an edge and might become profitable rather than foreign players. So combined with high volumes and close to 4-5% margins we can see good profits flowing to bottom line. This is my study, won’t say I am 100 percent correct, I agree with some of your points as well, but I feel that zomato might do well in the future.

yeah,i agree to disagree, as my point is not even about zomato being a good or bad company its about making returns out of my investments,i mean why do a person invest?

to make money simply, but what if the investment is already priced in for its future earnings,all im saying is that the margin of safety is bad considering its trading at 2lac cr+ mcap with super high PE. and there could be time correction. and at the end of the day investing is all about probabilities i.e anything can happen.

plus another point on instacart, from what i understood its not same as blinkit or zepto and the operating enviroment is different (at present,ofc it will change with time) they charge good amount for delivery and subscription,most of the people in india are a bit price sensitive so even a bit change in price will make general people shift towards another platform.plus instacart is available at 1laccr+ mcap with 28k cr of revenue and 7kcr of ebitda,with a PE of around 30,i get the point of bigger market here in india but better not forget the price sensetive point,so yeah it would be interesting to watch how this unfolds.