I can see (in mumbai) that Blinkit has started levying handling charges. For orders <200 Rs.16 for > 200 Rs. 12. Has anyone else noticed this?

ive also noticed that they have introduced something in the lines of surge. Free delivery only if the order value is > 500.

2 Likes

Facinating reading of Indus Valley Annual Report 2025. One can download full reports via https://blume.vc/reports/indus-valley-annual-report-2025.

8 Likes

Nice scuttlebutt on Blinkit and Zepto from the rider POV (Twitter thread)

3 Likes

Has anyone who is invested in quick commerce industry knows how to value these companies? Definitely PE is not the answer.

2 Likes

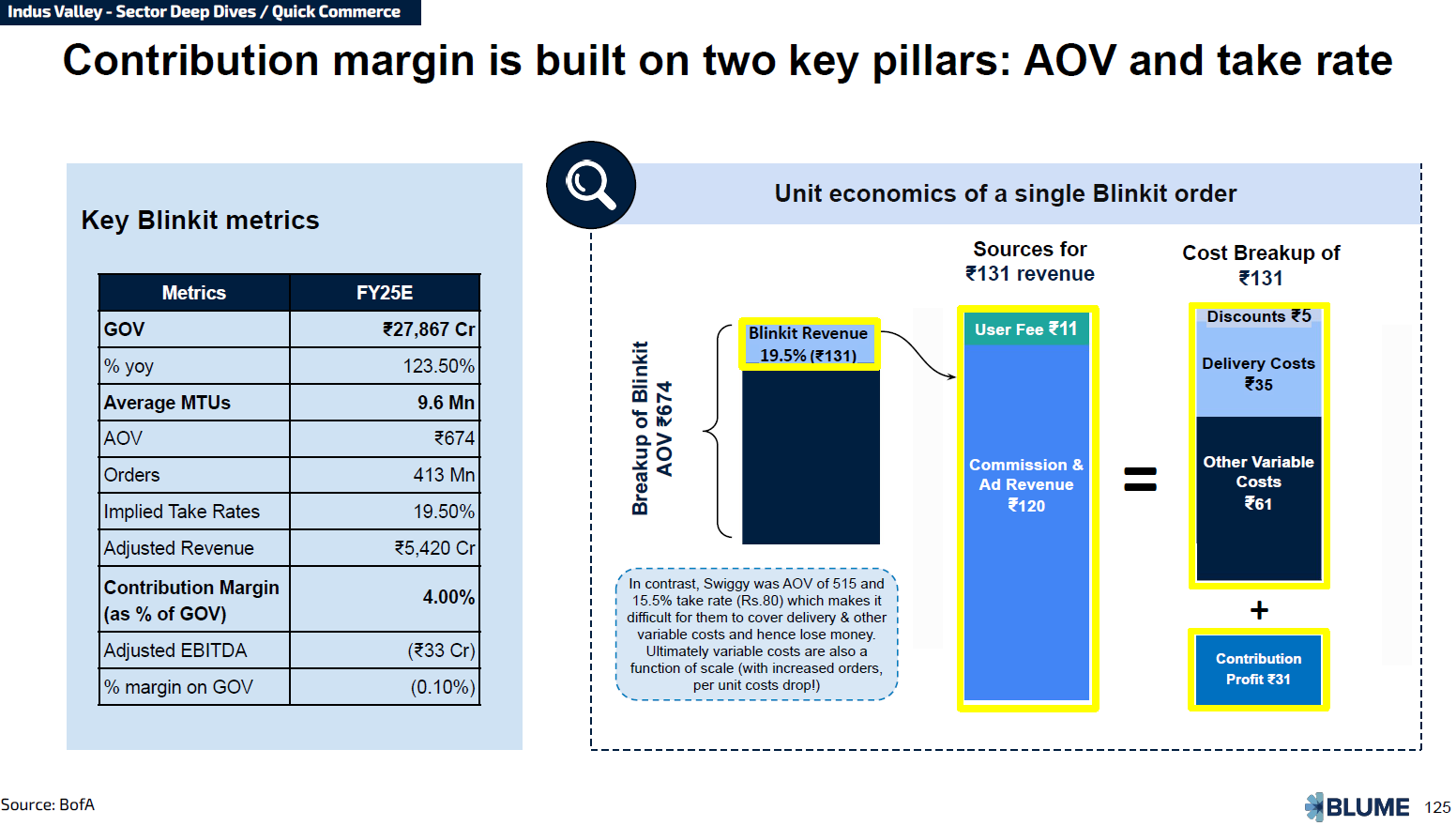

i think Blinkits current AOV is much lesser than currently reported (Rs. 700) and should not be extrapolated from here. this is due to 2 reasons:

- AOV is calculated on the MRP of the products purchased when most of the products sold are 10-15% below MRP. This means the actual average order value which the customer pays is much lesser than the reported AOV (most likely 10-15% lower).

- Q3 has higher AOVs due to festivities which must not be extrapolated for the year

Considering both the points I guess fair AOV that customer actually pays must be around 600 for the whole year for Blinkit (I may be wrong).

4 Likes

You should look at Contribution Margin. as CM is calculated after all the discounts.

if the CM is 4% of the headline number of 700 (just an example) then that gives you a better matrix to compare/evaluate.

2 Likes

Zomato is planning to cap foreign ownership at 49.5% to help Blinkit be eligible to hold inventory and improve margins as reported by news articles

How do members of VP see this? What are other implications and any possible downside from this ?

- If FII ownership goes above 50%, the company is considered as foreigner-owned. And the implication is some restrictions like FDI limit and a few more.

- Currently, FIIs own 44.36%, hence there won’t be immediate selling.

- Due to FII restriction, FIIs will stop buying above 49.5%, hence aggressive buying by FIIs is restricted in future. Sameway dii is more stable vs fii - hence extreme share price volatility may be avoided.

2 & 3 have limited impact anyway.

6 Likes

The weightage of Zomato in MSCI and FTSE index can reduce, which may led to some selling by FII and passive funds. Now when blinkit can have it’s own inventory so it’s margins may improve due to private labeling

3 Likes

6 Likes

Maybe. Isolated or individual opinions like these don’t have any effect on a business. Extrapolation is one issue with businesses like these. I run no business, no human emotions cannot be taken away running one. Even Berkshire Hathaway might have had its share of problems. If the problems are structural and powerful enough to destroy a business from within, then any name can vanish, no one is eternal.

All these are ineffective, if there are longevity and profitability. And, these can be corrected. Within a few months, it is possible to see a completely different opinion, an opinion of praise in the place of rant.

I use Zomato regularly, never faced any issues. Also have a position. Not biased, but do take my view with a pinch of salt.

3 Likes

Interesting read, maybe real interest and work going on in blinkit at present….

Over the past three months, I’ve noticed a clear shift among some of my family members who used to frequently order food online. They are now preferring offline purchases. When I asked why, they highlighted a few points:

High Delivery Fees: Delivery charges have risen sharply, and free delivery is now available only on high order values. (Platforms like Zomato and others have been increasing platform charges over the last quarter, and customers are noticing.)

Fewer Offers: Earlier, platforms gave frequent deals and cashbacks, but now these have reduced sharply. (For example, Zepto has discontinued “Zepto Cash,” and Blinkit’s convenience fees often cancel out any discounts.)

Avoiding Zomato for Fast Food: Many now order directly from restaurants or use Uber Parcel to pick up food, as prices on Zomato are often much higher than the restaurant’s menu price.

making money from Indian consumers is becoming increasingly difficult, given how price-sensitive and adaptable they are.

14 Likes

What’s happening here? I thought things would get better with Blinkit capturing the market. Looks like competition is fierce.

I’m not sure but rumor has it that they’ll shut down the 15 min delivery services. Which was their core business no? ![]()

I think they’re shutting down “Quick” which was launched 4 months ago, not their core business tho

2 Likes

FWIW - Amazon entered the quick commerce too with their recent offering “Amazon now”. Look at the cashback offer! Definitely they are going all guns blazing, I’m sure this going to drive some crowd from zepto and blinkit to Amazon. Interesting times ahead.

2 Likes

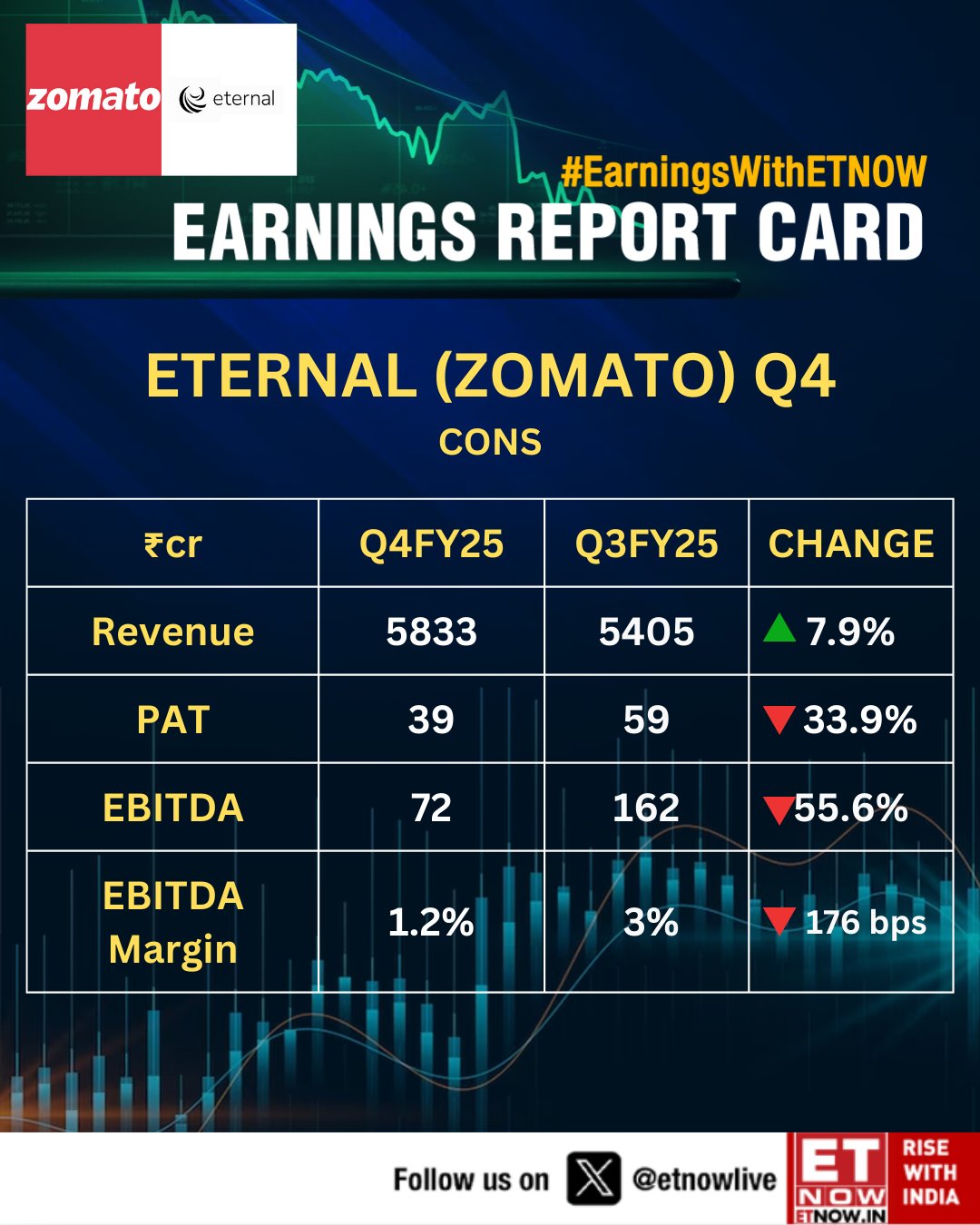

last quarter they did say that the next few quarters will be shaky due to the expansion costs of blinkit

2 Likes

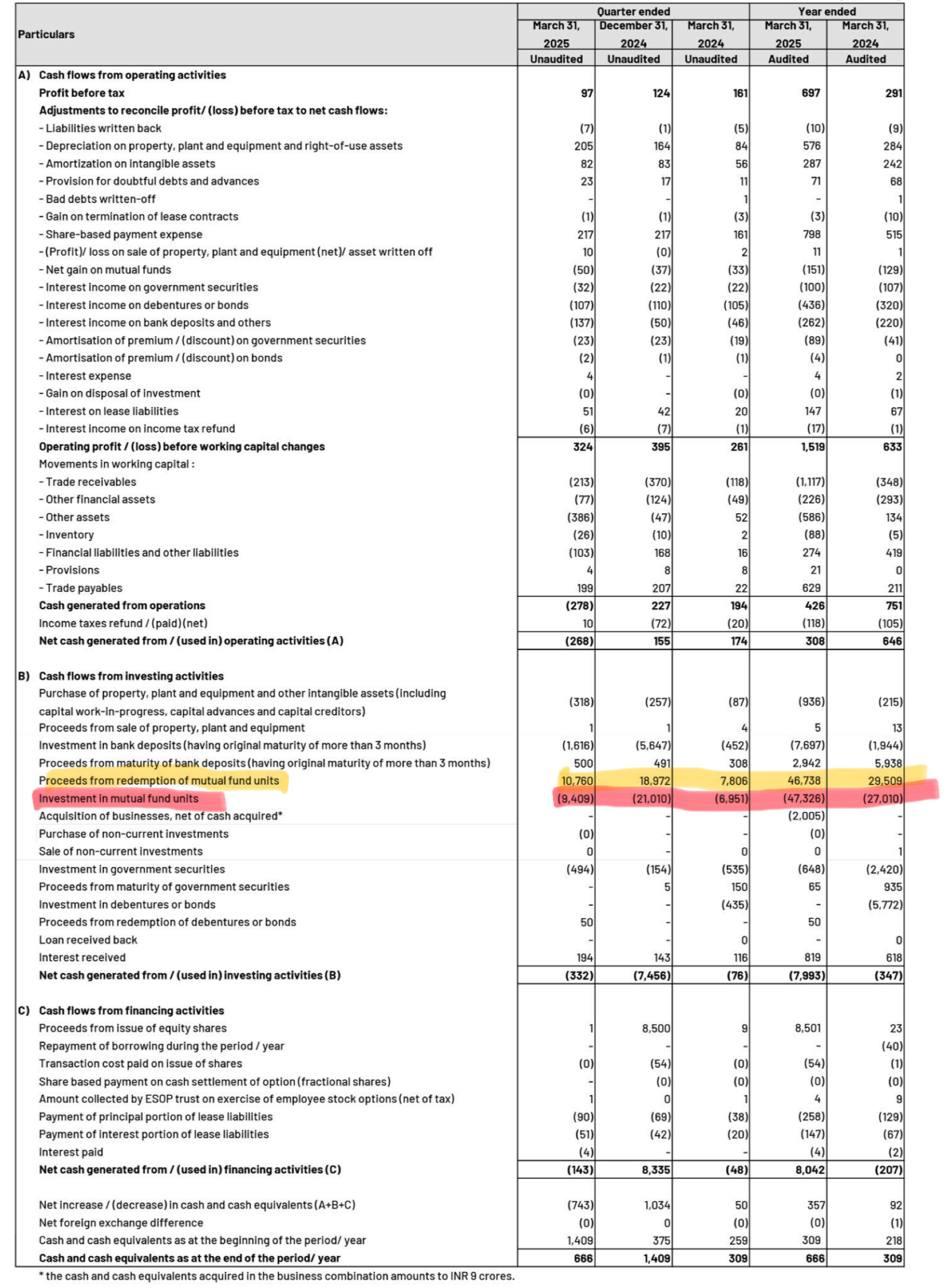

One Basic question out of curiosity:

While going through the Numbers in the Cash flow statement, found the below two statements with staggering numbers ( thousand of crores - Billions of dollars), of which I was blown away:

Are they trading in Mutual funds - Billion of dollars, From where they are getting this much of money ???

Question is Why are they doing this - is this their core Business??

3 Likes

These are most likely liquid funds churn. The company has a large amount of cash and investments on the book. Their core profitabilty comes from other income.

4 Likes