MARKET OVERVIEW

-

Here’s how India’s freight transport breaks down by mode:

Road: ~64% of goods movement by ton‑kilometres

Road: ~64% of goods movement by ton‑kilometres Rail: ~27%

Rail: ~27% Sea (coastal + inland waterways): ~5% coastal + ~2% inland = ~7% total

Sea (coastal + inland waterways): ~5% coastal + ~2% inland = ~7% total Air: ~ 1% or less

Air: ~ 1% or less

-

Double digit industry growth projected for next 5 years in all verticals

JOURNEY OF ZINKA LOGISTICS

2015 –  Incorporation & Platform Launch

Incorporation & Platform Launch

-

Company founded as Zinka Logistics Solutions Pvt Ltd and launched the BlackBuck marketplace for full-truck-load (FTL) freight

-

Raised initial seed funding led by Accel India.

2017/18–2019 –  Growth & Recognition

Growth & Recognition

- Continued expanding digital load-matching and introduced telematics solutions and FASTag/fuel card integration.

July 2021 –  Unicorn Milestone & Expansion

Unicorn Milestone & Expansion

-

Raised $67M in Series E led by Tribe Capital, reaching $1.02B valuation

-

Began exploring financial services and insurance, investing in product and data science

2019–2023 –  Fintech Integration

Fintech Integration

-

2019: Founded BlackBuck Finserve Pvt Ltd (BFPL) as NBFC arm

-

2023: BFPL received NBFC license and started lending by October 2023

-

By mid-2024, BFPL issued 5,109 loans worth ₹253 Cr

June – November 2024 –  IPO & Public Listing

IPO & Public Listing

-

November 13–18: IPO opened, raising ₹1,115 Cr (mix of fresh issue and OFS). INR 550 crore was primary issuance

-

Listed on NSE and BSE on November 22, 2024

-

TZF Logistics (BlackBuck’s subsidiary) got in-principle approval for a PPI license — helps own payment processes fully. PPI License (Prepaid Payment Instrument):

A license that lets a company manage digital payments end-to-end—like prepaid wallets. Gives better control of transactions and improves customer payment experience

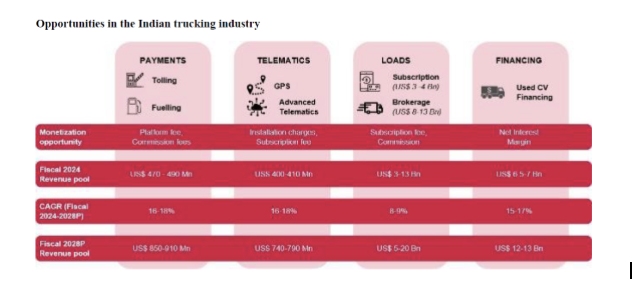

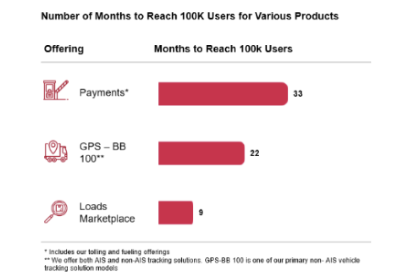

PRODUCTS/SERVICES:

Payments:

Tolling: The company provides tolling solutions (FASTags) in partnership with FASTag Partner Banks. They are the largest distributor and technology provider of FASTags for truck operators in Fiscal 2024 in terms of GTV with a market share of 33% in FY 2024 vs 26% in FY 2023

Revenue model:

- Commission margins from FASTag Bank Partners on the toll transaction flowthrough based on the monthly transaction value of the FASTags distributed

- Activation or convenience fee from truck operators in relation to FASTAgs

- Subscription fees to access specific services on the platform in relation to our tolling offering

Fueling: The company provides fueling payments solution through a cashless fuel payments platform, in partnership with multiple oil marketing companies (“OMCs”). It is the largest fuel loyalty management platform for truck operators in India, in terms of GTV in Fiscal 2024, with coverage enabling 72% of total fuel stations in India

Revenue model:

-

Commission margin from OMCs in fueling transaction flowthrough based on either the monthly consumption volume of fuel or monthly transaction value of fuel purchased

-

Service fees for providing services such as distribution and recharge of fuel cards, dedicated customer support, alerts and transaction history

Telematics:

GPS and Fuelsensoring:

- Provide real-time visibility into fleet movements, route optimization and enhanced fuel management, with the aim of increasing cost savings and improving efficiency

- Provide vehicle tracking and fuel monitoring solutions on the platform

- One of the largest players for vehicle tracking solutions in the trucking segment in India, with 356,050 average monthly active telematics devices in Fiscal 2024 and 390,088 average monthly active telematics devices in three months ended 30 June 2024

Revenue model:

- Monthly/Annual subscription fee from truck operators

Loads marketplace

Listing marketplace:

- Loads marketplace efficiently matches truck operators with shippers across commodities, load weights, truck types and distance ranges.

- This is India’s largest digital freight platform with 2.12 million digital loads posted in Fiscal 2024 via BlackBuck Transporter App.

Freight brokerage

- In January 2024, they started a freight brokerage business which is an extension of listing marketplace where they enable end-to-end logistics transactions for shippers. For the freight brokerage business model, they leverage the listing marketplace to discover trucks which meet the shipper’s requirements, negotiate the price and payment terms, and handle fulfillment responsibilities with the truck operator, on behalf of shippers

Revenue model:

- The loads marketplace offering is in the early stages of monetisation

- Subscription fees are charged to shippers for posting loads

- Subscription fees to truck operators for preferred matching services

- Commission on freight brokerage business

- Various other subscription plans to shippers and truck operators

Vehicle financing

Used Vehicle financing: Enable truck operators to buy used commercial vehicles or to avail financing on an existing vehicle by providing financing solutions. They facilitate disbursement of credit in partnership with our Financial Partners

Revenue model:

- Loan service fees. In addition, we are entitled to certain other fees charged to the borrowers in the process of loan disbursal and collections, either partially or in full.

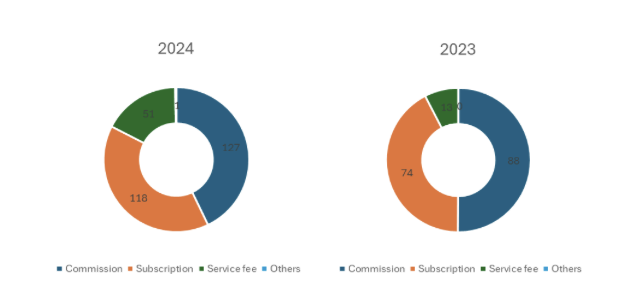

REVENUE MIX:

Commission fee and subscription fee makes up 83% of revenue in FY 2024 decreasing from 92% of the revenues. Service fees which is currently at a low base is growing faster and makes up 17% of total revenues

GO TO MARKET:

- Mix of digital marketing and targeted notifications through the BlackBuck App

- As of 30 June 2024, 9,374 Touchpoints on the ground, to acquire new customers, as well as cross-sell/upsell the products

- As of June 30, 2024, 843-member telesales unit that reaches out primarily to the existing customers for upselling and cross-selling

- 587 channel partners to reach out to truck operators for sales across multiple product offerings

- As of June 30, 2024, sold and serviced the products in 80% of India’s districts, including in all the major transportation hubs and across 76% of the toll plaza network in India

- Increased the base of annual transacting truck operators to 963,345 customers in FY 2024 from 761,871 in FY 2023 and 482,446 in FY 2022.

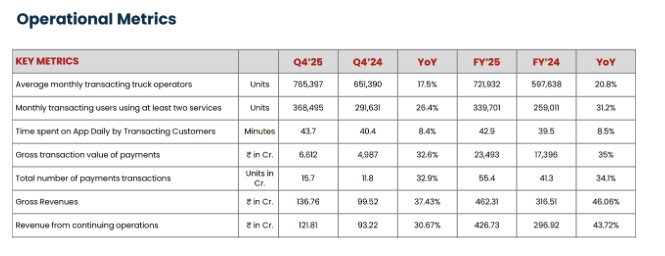

KEY PERFORMANCE INDICATORS:

- Significant growth in users, usage per day, GTV, no of payments on the platform and as a result, revenues increased. Amongst all the KPIs, in my view, 2 most important KPIs are no of truck operators, GTV of payments which increased 21% and 35% YoY respectively

FINANCIALS:

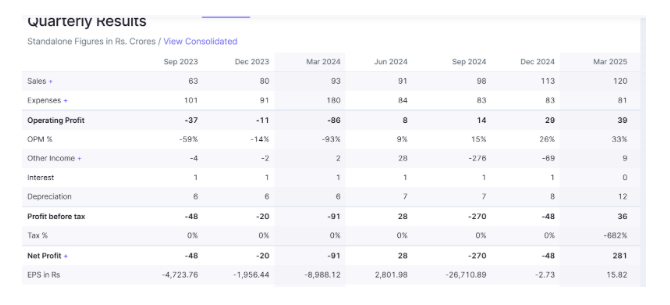

Quarterly P&L: Consistent growth in quarterly revenues and turned EBITDA profitable since September 2024 with growing EBITDA margins and solid 30% + margins

Yearly P&L: The company recorded high revenues in 2020 and 2021, during its private phase, when funding was readily available. Growth during this period was likely driven by easy access to capital—or possibly due to revenues being reported as Gross Transaction Value (GTV), although this is not disclosed elsewhere. Since then, revenues declined, which appears to reflect efforts toward cost optimization or adjustments in revenue recognition. However, over the past two years, revenue growth has resumed, culminating in a positive EBITDA margin of 22% in FY 2025.

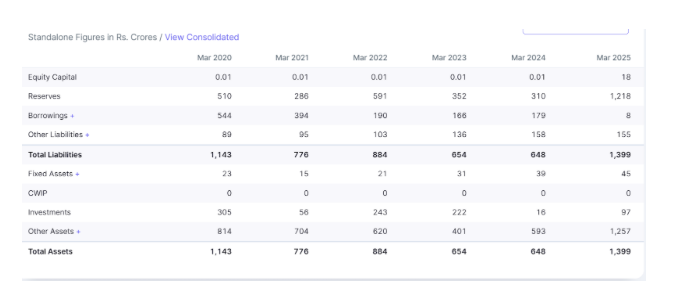

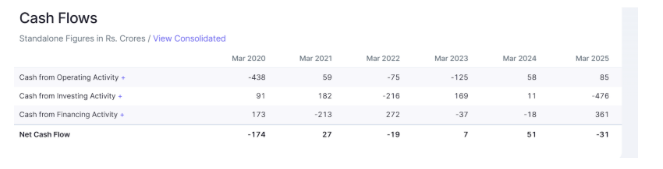

Balance sheet: Asset light business model. No borrowings - sitting on INR 600+ crore of cash

Cash flow: CFO positive since 2 years with good EBITDA conversion due to extremely low working capital requirement. The company raised INR 550 crore through IPO in November 2024

Working capital: Minimal debtor days and that has also improved recently post IPO

Shareholding pattern: Consistent shareholding pattern. No of shareholders decreased 20% indicating accumulation from institutions as can be seen from large bulk block deal that happened recently described later

RECENT TRANSACTIONS:

Large institutions such as ADIA, MIT, ICICI Mutual funds, MIT SBI Mutual funds entered at INR 420 price per share absorbing supply from VC/PE investors

NETWORK EFFECTS AT PLAY

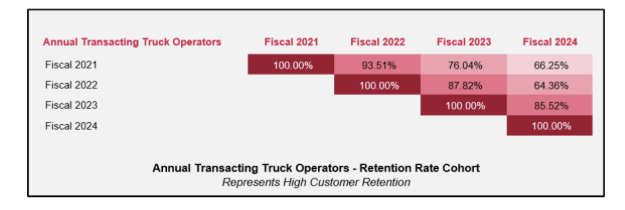

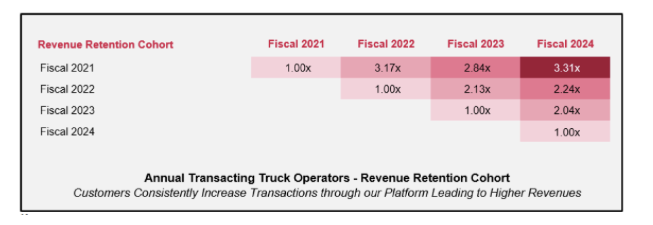

Cohort Analysis

- 2/3rd of the truckers continue using the platform after 4 years of onboarding indicating strong stickiness amongst users

- Trucking operators consistently increase their transactions. A trucker onboarded in a year provides 3 times more revenue after 4 years of its onboarding

- Time taken to scale new offerings is reducing which they were able to achieve this primarily due to the platform-led strong network effects playing out, valueadd of services for the customers and the strength of omnichannel sales and distribution strategy

As a result of the Network Effects and typical of platform tech, growth in revenues and cost optimisation is leading to exponential growth in EBITDA and CFO

COMPETITION:

Except for the vehicles financing segment which has traditional established players, BlackBuck is a clear category creator and leader in trucking digital marketplace. Even for these vehicle financing player, Blackbuck is just distributor and not competitor as it does not do much lending on its own but partners with the banks. Further, this is not a material part of the business.

MANAGEMENT STRATEGY (AS PER DRHP)

Expand distribution and truck operator base: Focus on attracting new truck operators in underrepresented markets like Gujarat, Karnataka, and Tamil Nadu.

Invest in core verticals:

- Enhance the fuel sensor product and improve customer experience in telematics.

- Leverage India’s trucking industry growth (8-9% CAGR from FY 2024-2028) to expand payment and telematics offerings.

- Vehicle tracking penetration expected to grow from 40-45% in FY 2024 to 65-70% by FY 2028.

Grow loads marketplace and vehicle finance:

- Invest in product and technology to grow the loads marketplace.

- Expand freight brokerage offering to more cities across India.

- Vehicle financing launched in FY 2024, facilitating over INR 253 crores in loans across 52 districts.

- Invest in new verticals and data science: Focus on expanding into new business areas and enhancing data science capabilities.

Q4 FY 2025 CONCALL SUMMARY:

1. Financial Performance & Growth

1. Financial Performance & Growth

-

FY25 revenue: ₹462 Cr (↑46% YoY); Contribution margin: ₹429 Cr (↑49%)

-

EBITDA: ₹139 Cr (↑10x YoY), driven by recurring, high-margin platform revenues

-

Growth expected to continue due to macro tailwinds and market share gains

2. Market Share & Segment Split

-

Tolling market share: 37% → 45.5% in FY25

-

Telematics share: 30–45%

-

Core biz (tolling + tracking) = 85% of revenue; rest from growth segments

3. Future Growth Drivers

-

Big runway in tolling, telematics, fuel sensors, load brokerage

-

Growth backed by infra push, rising fleet size, and tech stack

-

Confident in platform advantage and cost leadership

4. User Engagement & Platform Metrics

-

7.7 lakh monthly transacting truckers (↑18% YoY)

-

27% growth in multi-service users

-

App usage: 44 mins/day; tolling share also rose

5. Cost Efficiency & Strategic Investments

-

Costs stable; strong operating leverage

-

Telematics devices: designed in-house, manufactured externally

-

PPI license to enhance CX and margins over time—not immediate revenue

-

Confident vs OEMs due to price, tech control, and dealer reach

RISKS

- High dependence on business partners in payments offerings. One of the FASTag Partner Banks contributed to 33.51% of total revenue in Fiscal 2024

- Users and usage plateau: There are about approx. 12.5mn (expected to grow to 14-15mn truckers by 2028) truckers in India and currently only 1mn truckers are on its platform . There is still lot of headroom to grow

- Revenue is dependent on shippers continue to ship and continue to use their platform. Therefore, marco headwinds in the economy will lead to reduce logistics and thereby reduced usage in their platform and their revenue

- Although the current supply is being absorbed by Mutual funds and other FIIs. It appears that there is still some holding of early stage backers who most likely will sell at the next rise and if there are no takers at that price and there will be pressure on the share price

CATALYST:

- Limited adoption and growing profitably - There are still many truck operators that are not on digital platform. Today, a large part of India’s trucking is informal — unorganized and offline. BlackBuck can onboard more small truckers, digitizing payments, load-matching, tolls, and insurance. Management guidance is high double digit growth for next 3 to 5 years

- Not just market share capture but Blackbuck is also expanding its market size by introducing new products. As observed above, every new products launched is taking much less time to scale due to network effects

- Operating leverage - Growth in revenue will translate more growth in profits as can be seen in the current quarters which is the evidence of operating leverage. Further, most of the EBITDA is converted into cash flow operations due to limited working capital

- Network effects - 2/3rd of the truck operator are still active and transacting on the app after 4 years of onboarding and the revenue from such truckers are almost 2-3x after 4 years of onboarding

- Limited competition - This was built on the back of large private funding - unlikely that there will be another player like this in the near future. If they win, there will be few players or they will be the only player dominating this trucking digital marketplace (Marketplace philosophy - Winners take all)

- Lot of the supply/exit has been absorbed by large insitutional players such as ADIA/MIT/MFs etc.

Source: TheWrap, DRHP, Screener, Investor Presentation, Earnings Call Transcript

Disclaimer/Disclosure: Not a SEBI Registered Analyst. Hold position in Zinka Logistics