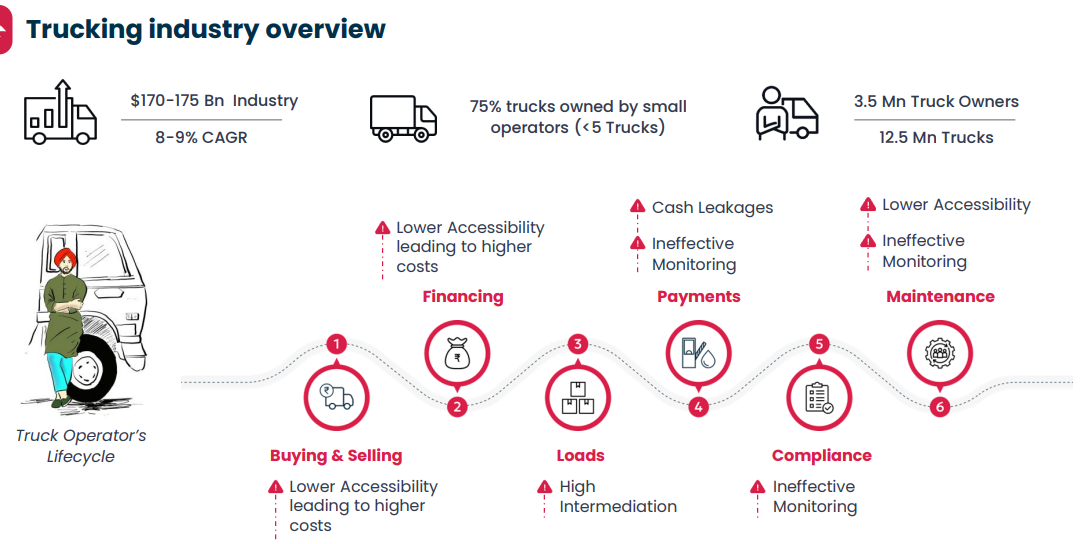

INDIAN TRUCKING LANDSCAPE

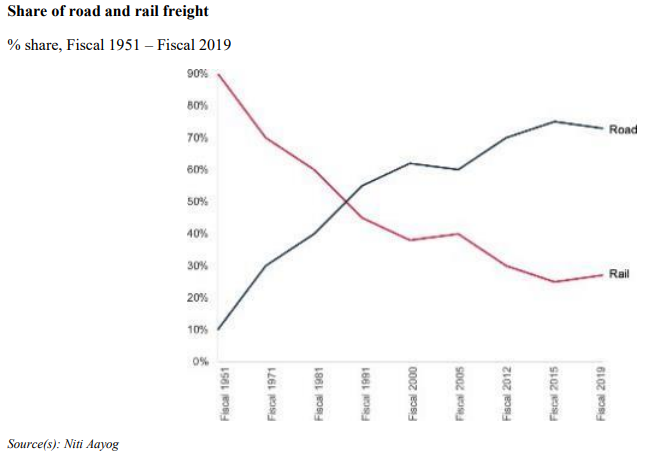

Road transport dominates logistics in India, forming the bulk of logistical expenses and emerging as the largest and most significant mode of transportation. Transportation accounts for the bulk of the expenses and accounts for nearly 66% of logistical expenses as of Fiscal 2024, with road transport being the preferred mode for various industries.

Hence, road transport stands as the backbone of the country’s logistics. Trucking is one of the fastest-growing sectors in logistics in India.

The Indian trucking industry stands as a vital component of the nation’s logistics sector. With approximately 12.5 million trucks and about 3.5 million truck operators as of Fiscal 2024 traversing Indian roads, the total freight value through trucks has witnessed a steady growth rate of 8-9% CAGR over the past four years. This growth trajectory is expected to persist over the next four years

Digital Toll and Fuel Payments

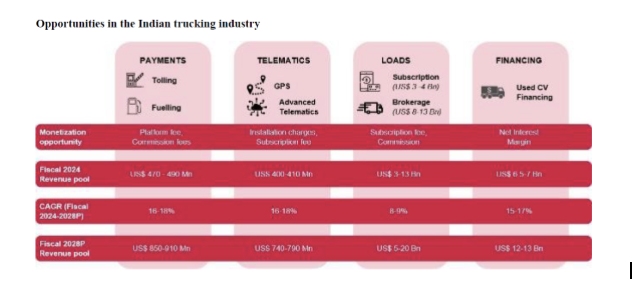

Toll and fuel payments represent almost 80% of a typical truck operator’s expense. The introduction of FASTags for toll payments and digital fuel cards is transforming how these transactions are managed. The total revenue pool for digital payments is projected to grow from $470-490 million in Fiscal 2024 to $850-910 million by Fiscal 2028, at a CAGR of 16-18%. Digital payment systems can help truck operators track and manage expenses more efficiently, reducing leakages and improving cost control.

Incorporated in 2015, Zinka Logistics Solutions Ltd provides a digital trucking platform for payments, telematics, loads marketplace, and vehicle financing services

As consumers, when we use mobile apps, apps on our mobile phone, we typically will have social media apps or browsers which typically will take largest mind share. For a truck operator, blackbuck is an app, and they are in the top 2-3 apps what he uses on a daily basis. And on an average, a truck operator on a daily basis is using Blackbuck’s app for like 41 minutes, which is continuously going up on an year-on-year basis.

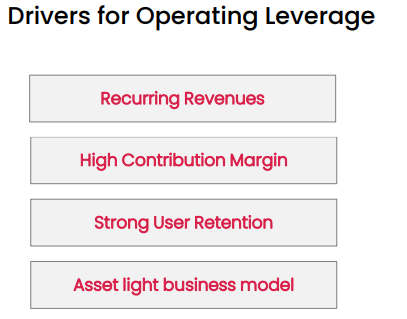

BlackBuck has an asset-light business model that primarily generates recurring revenue

through platform fees, subscription fees and commissions. There is neither any inventory risk nor ownership of trucks on the balance sheet, and distribution of loans is through financial partners.

Services Offered:

a) Payments:

Tolling, Fuelling

b) Telematics:

GPS, Fuel Sensor

c) Loads Marketplace:

Listing Marketplace, Freight Brokerage

d) Vehicle Financing:

Used Vehicle Financing

^ This seems right from text book - now some value adds around the whole thesis we should keep our eye on.

Tolling and telematics

- Tolling : 61% of rev : They have Pan India Service n/w + Guaranteed incorrect deduction refund + Protection from blacklisting through auto-recharge in case of low wallet balance

- They Earn via :- Commission fees, FASTag servicing fees, Subscription fees (Gold membership) - Partner are IDFC and Axis + more

- Fueling : Commision from OMCs, Subscription fees from truckers - Partner list : HPCL, Reliance, IOCL

- Telematic : 25% of Rev : Real-time visibility of the Fleet movements - Route optimization + Fuel management : Earn via : Device installation charges + Subscription fees + Own proprietary design of GPS device + GNSS can drive higher penetration as GPS becomes mandatory for precise toll deduction

Now, when it comes to tolling, if you look at a truck operator, a truck operator is like 100 times more powerful user than a car FASTag user. Car FASTag user annually probably spends INR5000-INR10,000 on a FASTag. A truck operator who has three trucks, average monthly is INR16,000 per truck, three trucks monthly is INR48,000-50,000, annually is INR6 lakh

Revenues in Tolling for Blackbuck is a function of 3 vectors:

First vector is basically how India macro grows.15% to 20% growth directly comes from how India macro grows because government is laying more roads, state highways get replaced by national highways. So more toll spend happens, more flow through to FASTag happen and the number of trucks keep growing

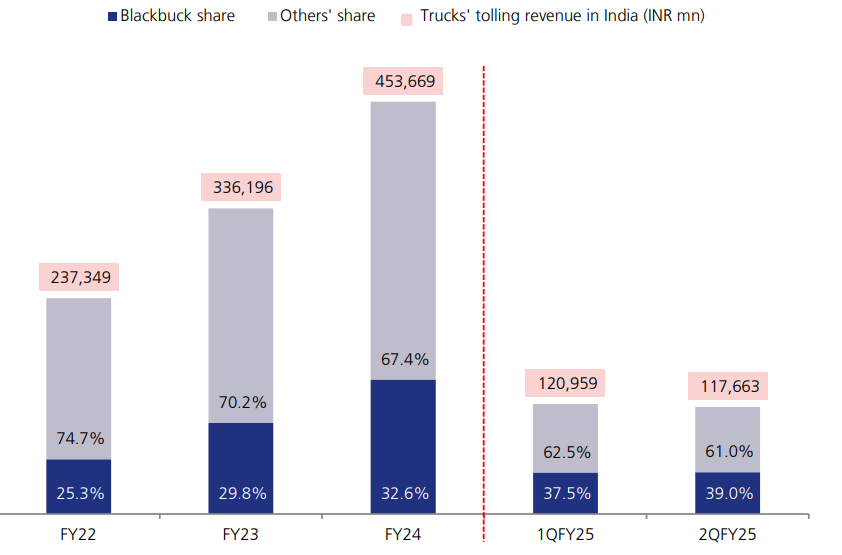

Second area is that we continue to gain market share.They have always gained higher percentage points of market share. That has happened continuously. they are the only ones who are doing and they continue to gain market share. Last FY24, they as a company gained like 7 percentage points market share over the previous year. This year again, probably they will be gaining similar or more.

Third lever of growth is their penetration of value added services. They provide much more better value to their customers than others. And they also charge customers for these value streams. That has helped them break out and add another alpha on top of that, which has helped them compound revenues at like 47 percentage kind of a level and in the core verticals.

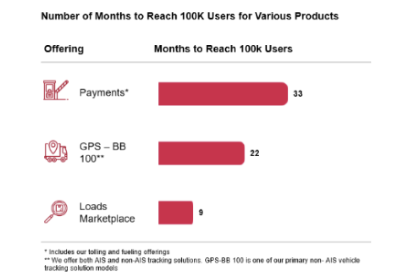

Cross-Sell oppurtunity

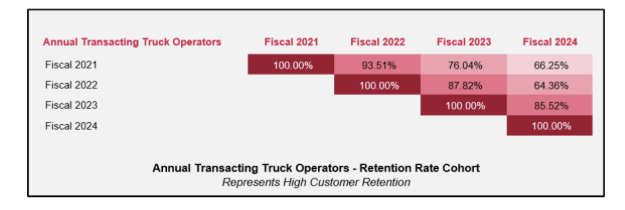

With the company having 1mn+ annual transacting truck operators who spend a substantial amount of time on its app, there remains a sizeable cross-sell opportunity. BlackBuck currently has only 20-25% overlap in its two largest offerings – tolling and telematics. Meanwhile, Fueling, Loads Marketplace and Vehicle Financing only have around 10-15k truck operators and hence can grow sharply driven by cross-sell on the existing consumer base itself. This results in the company incurring minimal acquisition costs to grow these businesses and delivering healthy LTV-CAC ratio.

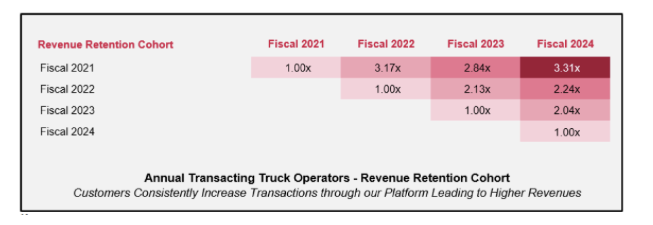

Operating Leverage enabled via contribution Margins

There is an instance in the concall where Management mentions that they have already increased the fees and it was in the range of 20-40% and that went smoothly with no churn at all. Shows a lot of strength in the model and the kind of service they are providing

BlackBuck’s platform led revenues driving a P&L with strong operating leverage

Transform truck operator → Transform Indian Trucking

BlackBuck continues to gain trucks’ tolling market share

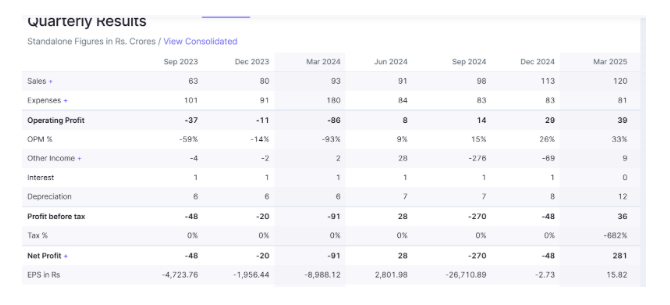

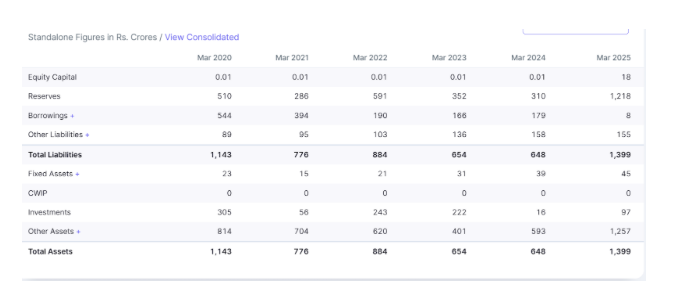

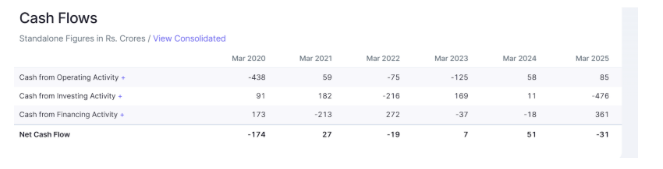

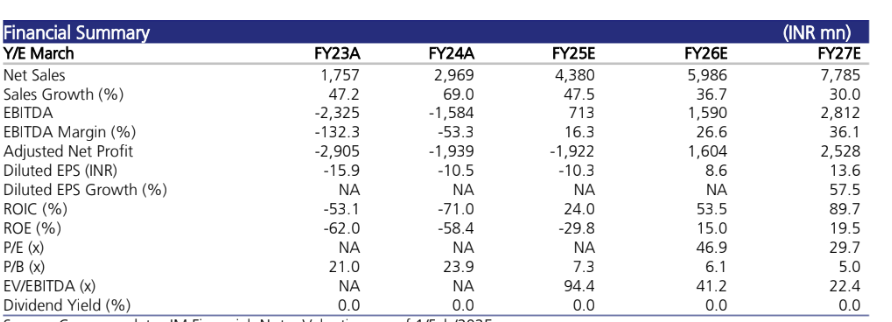

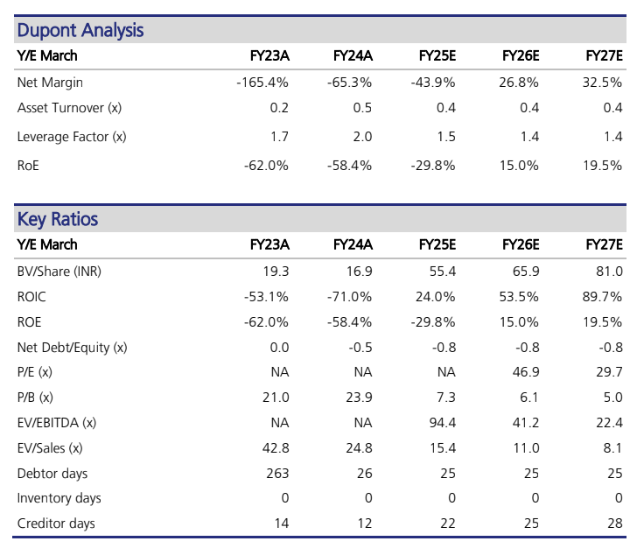

Financials

Risks should be kept closer vs the thesis

- Tolling and telematics business might see slowdowns which can lead to issues

- High dependence on cash-handling increases leakages at all these touchpoints, ultimately reducing profitability for the truck operators.

- Dependence on strategic partners - In the payments offering, one specific partner contributes to 45.26% of total revenue. High dependance poses risk too.

- Revenue concentration - High concentration 94% in payments and telematics offerings

- Dependence on suppliers - Some vehicle tracking solutions are imported and there are limited suppliers for the same.

- Seasonality business - Company’s payments and loads marketplace offerings might see seasonality especially demand during monsoon season due to logistical disruptions.

- Regulatory risks - Evolving laws and regulations. Dynamic nature of regulations, particularly in payments and telematics

- Vehicle financing risks - inherently risky due to the nature of borrowers.

- FASTag might make way to HNSS tolling ie a satellite bases sys that automatically collects tolls from vehicles and expressways vs FASTag which uses RFID tech

- https://www.business-standard.com/india-news/new-toll-rules-is-fastag-s-end-near-with-gnss-rollout-who-s-using-it-124091100595_1.html

Government initiatives

At a policy level, there is a clear realization regarding the value and prosperity that can be unlocked by digitizing transactions, introducing more efficiencies and fostering transparency in trucking operations in India. Below are some of the noteworthy initiatives towards this transformation:

-

Electronic tolling: The government’s implementation of FASTags has digitally transformed the tolling system, achieving 98% penetration by March 24 in toll collection. This move aims to modernize the cash-based industry, curbing leakages and enhancing efficiency by minimizing congestion and travel time on roads. Moreover, the transition to digital payments has spurred growth in toll payments through the NETC platform, with 3.5-4 billion transactions in Fiscal 2024.

-

Mandatory GPS requirement: In India, the implementation of the Automotive Industry Standard (“AIS”) 140 protocol has been pivotal in mandating the installation of GPS devices in trucks requiring fitness certificates and specific mining permissions to improve safety, security and compliance. This regulatory requirement has significantly increased the adoption of telematics devices within the trucking industry, enhancing monitoring capabilities and promoting operational efficiency.

-

E-way bills: E-way bills ensure faster movement of goods and optimal vehicle utilization at check posts. With preregistration required online for goods over ₹50,000 and a single e-way bill system, transportation processes are streamlined across the country. This eradicates the need for separate transit passes in each state, facilitating seamless road freight transportation.

-

National Logistics Policy: Government of India’s launch of the National Logistics Policy (“NLP”) aims to revolutionize India’s logistics sector, reducing costs from 11-13% of GDP to align with global standards. By enhancing efficiency and lowering expenses, the policy will boost the competitiveness of Indian products globally. Leveraging a holistic approach.

Rajesh Yabaji is very articulate and a must watch to understand a bit more about the man himself

Blackbuck Youtube Channel where you can follow them and look at some of the Ads they have worked upon https://www.youtube.com/@blackbuckzinkalogisticssol8238/videos

Disc : Invested