I agree with you that there was no clarification in the Notes for such a big drop in turnover in Q2. And no update about the investment made. Answer to these doubts is vital for assessing the quality of business and capital allocation. If any body has any clue on these and through some light, it will help a lot in understanding the company.

1 Like

There may be an explanation for that. some 35L was paid as medical expenses for the chairman. This is a business that seems to be completely run by the owners - the chairman and his family in this case. If he falls sick and needs medical attention then the business is likely to suffer i guess. They need some changes in the management structure to ensure that these things dont happen frequently in the future. Of course this is just a theory but its possible that that’s the reason for the fall in revenues

Hi,

In the latest sept half yearly statement, I noticed that around 10Cr has been moved from cash to non-current investments. I believe thats a good sign that they have started doing something with the cash in their balance sheet.

Hi,

i think we should wait for the next two qtrs results to get an idea where the company performance is heading. Its not growing as expected this year and need to keep an eye whether they are able to show some improvement in the performance in the next qtrs.

There is another thing - the capital employed in the business is 12.84cr ( equity + debt - cash) on which it earned a PAT of 8.49cr, which translates to a great ROCE of 66%. Even if you take the Sept Qtr PAT and multiply it by 4 assuming that thats the new normal it still translates to PAT of 4.32 cr or a ROCE of 34%. I wonder how competition is allowing it to have such high ROCE, i mean ideally all these returns should attract competition and be competed away. That or it has a moat, and my untested theory is that this industry has a lot of overcapacity and it most of it is owned by zenith being a big player in a very small pond. The thing that many seniors on the forum have repeatedly stated that players like zenith are “processors” they buy, process and sell. They dont have any intellectual heft to add anywhere unlike in industries like pharma, IT etc , so that is an area of concern.

2 Likes

This is at an interesting valuation. If we can get answer to why the revenue dropped significantly in the last qtr, we will know whether it is one off, or new normal.

This is a very simple but important point. Is there a way to find?

they have invested that much cash in mutual funds.

Heres what grabbed my attention

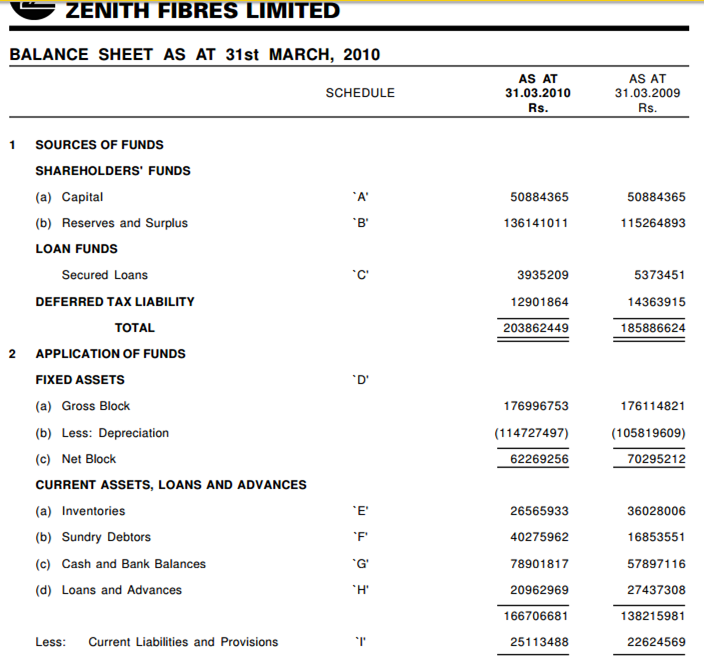

This a snapshot of balance sheet from the 2010 AR

The Capital Employed in the business in 2009 is

50884365 (Capital) + 115264893 (Reserves) + 5373451 (Debt) - 57897116 (Cash) = 11,36,25,593

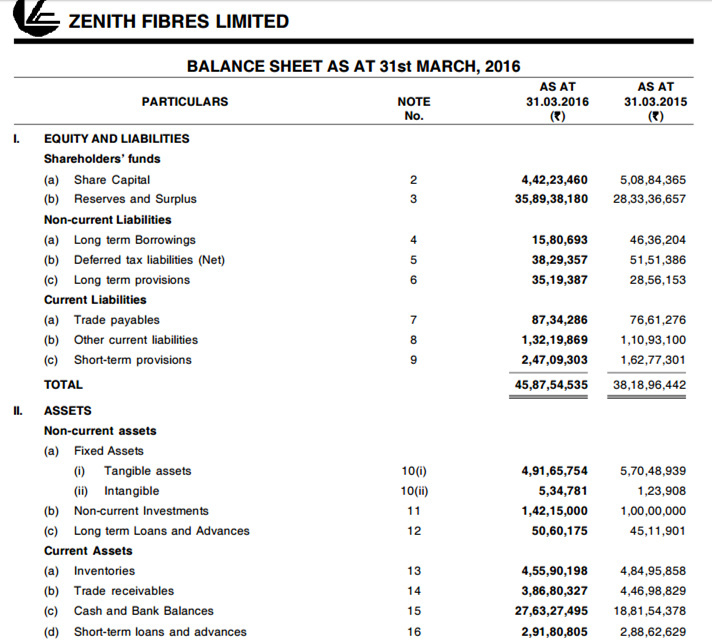

Fast forward to the last balance sheet

The Capital Employed in the business in 2016 is

44223460 (Capital) + 358938180 (Reserves) + 1580693 (Debt) - 276327495 (Cash) = 12,84,14,838

Capital Employed in 2016 = 12,84,14,838

Capital Employed in 2009 = 11,36,25,593

Incremental Capital Emply= 1,47,89,245

From 2009 to 2016 - the company has employed an incremental capital of only 1.47cr

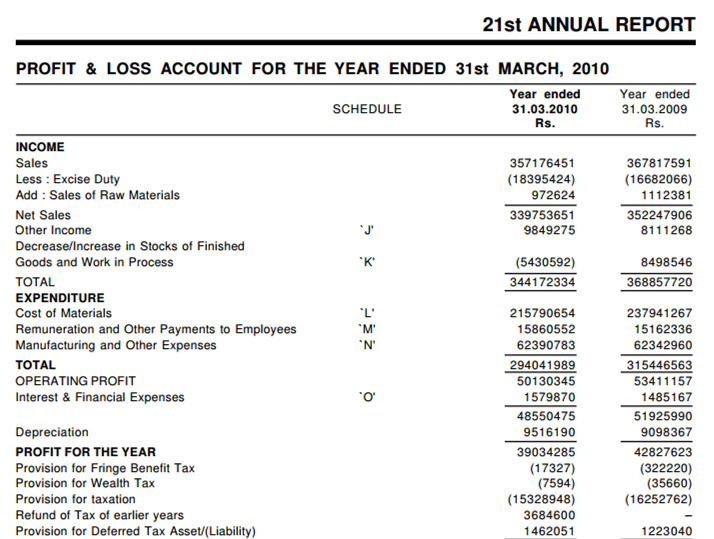

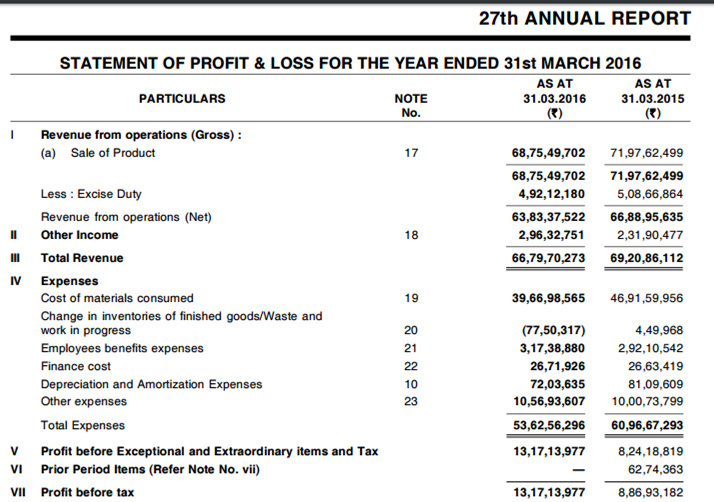

PBT in 2016 = 13,17,13,977

PBT in 2009 = 4,28,27,623

Incremental PBT = 8,88,86,354

The incremental profit over the same period is 8.88cr

The company employed an additional capital of only 1.47 cr but extracted an additional profit of 8.88 cr - a remarkable achievement in my opinion ( See’s candy anyone?)

Discl - invested

5 Likes

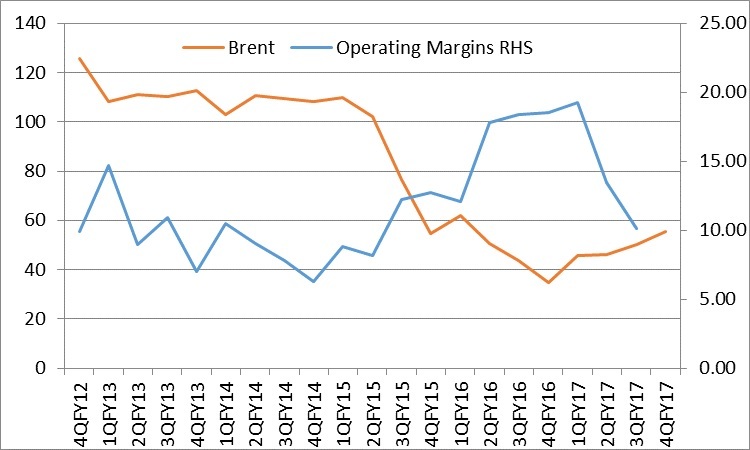

I think comparison could be misleading for FY10-16 as they majorly benefitted from lower crude/raw material prices…you could come out with similar numbers for sugar stocks over last two years…I think PBT growth majorly is because of cyclical upswing…posting chart of quarterly operating margins vs brent prices…now with higher Raw material they are now in lower operating margin environment…

1 Like

Hi @Pavas

Material costs as a % of sales have actually increased during the fall in brent prices for zenith. Have a look

Going as far as back as 2005

You will find the the capital employed back in 2005 was 11.19 cr and now its 13.14 cr - a measly addition of 1.95 cr

While earnings …

have grown by 13.17 - 2.20 = 10.97 Cr

10% drop in material cost in 2016 while Brent was lower by 44% in that year…it benefited from lower RM obviously…

Another thing that i wanted to highlight is that one of zeniths competitors ( Arora Fibres ) which manufactures virtually the same product (PPSF) has delisted following unsurmountable losses while Zenith being in the same industry and the same product has flourished ( although the last 2 quarters have been bad for zenith).

from the Arora Fibres 2015 AR

In the same period Zenith Fibre AR

The delisting document for Arora Fibres can be accessed here

http://corporates.bseindia.com/xml-data/corpfiling/AttachHis/CA834BCC_72C7_4621_A70E_01849A14A0A7_112055.pdf

3 Likes

This is an interesting find and amazing contribution by @bheeshma. Comparison with See’s candy seems apt  . The CFO needs to do better job with all the idle cash. Majority of the excess cash is in FD (approx. 26.5 cr) . The rates of FD’s have gone down significantly in recent past and this will impact other income. This can already be seen in last 2 quarterly results. OI has gone down to 65L and 48L for Q3 and Q4 of FY17 compared to average of more than 75L in previous 4 quarters. Not sure why they are not investing surplus funds in MF’s. If they could achieve approx. 11.5% return on this then that itself will increase EPS by approx. Rs.2.40 (7.5% FD rate - optimistic). CFO is being paid less than Rs.12L p.a. and that may explain his inability to deploy idle funds in more remunerative areas which are relatively risk-free.

. The CFO needs to do better job with all the idle cash. Majority of the excess cash is in FD (approx. 26.5 cr) . The rates of FD’s have gone down significantly in recent past and this will impact other income. This can already be seen in last 2 quarterly results. OI has gone down to 65L and 48L for Q3 and Q4 of FY17 compared to average of more than 75L in previous 4 quarters. Not sure why they are not investing surplus funds in MF’s. If they could achieve approx. 11.5% return on this then that itself will increase EPS by approx. Rs.2.40 (7.5% FD rate - optimistic). CFO is being paid less than Rs.12L p.a. and that may explain his inability to deploy idle funds in more remunerative areas which are relatively risk-free.

Also, they should spend their prescribed CSR amount on time. CSR amount for 14-15 was unspent upto March 2016. Overall, this amount is less than Rs.15L p.a. which is far less than what the company generates in cash.

1 Like

@bheeshma. Thanks for the great write up and detailed analysis on the company. I had a few basic questions regarding the business in general. They are detailed as follows: -

i. Who are the other major competitors in this space? eg. Nirmal Fibers. How does Zenith differentiate?

ii. What are the use cases for PPSF? Any clarity on industry size, its growth rate, future expectations etc would be great.

iii. Any possible scuttlebutt that could be initiated to gain a better understanding of the quality of the products?

Thanks,

Shaunak

As far as i can tell Zenith owns most of the PPSF ( Polypropylene staple fibre ) capacity in India. I have posted info on the industry size and growth rates in the earlier threads. The product itself is a commodity however PPSF is the lowest cost fibre amongst all man-made fibres. I have not done any scuttlebutt due to lack of time and resources!

Recently new use of synthetic fibers have been found in construction

sectors where Synthetic Fibers (Polypropylene) can be replaced in Reinforcing

Steel in the Concrete.

Similarly certain novel uses of PP fibre where replacement of glass with

polypropylene is identified in the industry. This augurs well for PP fibre

industry and it should definitely reflect in the growth of the company in the

future being a monopoly player.

ref: http://smallcapvaluefind.blogspot.in/2017/02/zenith-fibers-analysis-122.html

Hi, thanks for this. I too have understood that PPSF is a commodity. However, despite the cyclical nature of the commodity business, Zenith has never reported losses over FY05-FY16. Best best in a commodity play is to stick with the lowest cost producer because then you can be agnostic to the commodity cycle. Hence, Zenith at this valuation seems a good bet.

Disc: Invested

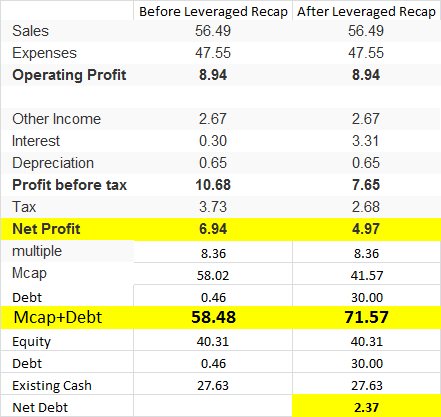

Zenith is also a leveraged recap bet. Due to its cash levels it can take on debt and still remain debt free. Because of all the free cash flows it generates it can easily service its interest costs. Lets do a small calculation.

In 2016, it generated a CFO ( before taxes and interest ) of Rs 13,23,57,179

Assuming a interest coverage ratio of 4 , it can service interest payments of 13,23,57,179/4 = Rs 3,30,89,294.75 or 3.31cr.

Because of its strong cash position lenders will be willing to give it a loan at 11% i.e it can take on debt of 3.31cr/11% = ~30cr without impacting its balance sheet adversely.

Hence its PE multiple is likely to remain at the same levels i.e 8.36 ( current ). The total embedded value of the firm is at least ~72cr - a margin of safety of at least 20% from the current levels. Even after taking 30cr of debt its net debt remains at 2.37cr.

Professor Bakshi lays down a case for leveraged recaps. I have learnt so much by just reading him. Here is the link - Value Investing – A presentation by Mr. Sanjay Bakshi – Capital Ideas Online

Something that i didnt mention was that the 30 cr debt can be used to pay a special dividend to the shareholders. The reserves of the company are in the range of 35.89 crs. So by paying a special dividend a large part of the reserves will get wiped out. Now the equity capital of the company will be 4.42 crs ( share capital ) + ( 35.89 - 30 crs ) = 4.42+5.89 = 10.31crs.

The following 5 awesome things will happen if you do that :-

-

The shareholders will receive a suerb special dividend of 30,00,00,000/44,22,346 = ~Rs 68 per share on a CMP of Rs 141

-

The RoCe will be PBT/(Equity Capital + Debt - Cash) = 4.97/(10.31+30 - 27.63)=4.97/12.68= ~40%

-

The ROE will be 4.97/10.31 = ~48%

-

The company will still having a net debt of 2.37 crs ( 30 cr debt and the 27 cr of cash on the books that is accumulated from previous years )

-

The share price of the company is likely to move up with the following scheme unlocking further value for the shareholders.

This is a win - win situation for everyone. A few years ago i think Brittania did the same thing. They issued bonus debentures. Look where its share price is now.

As always - happy investing!

13 Likes

As per Sanjay Bakshi’s method, deep value would have been created if Zenith was below 30Cr in Market Cap as you’ve expected that debt could be 30 Cr.

no. thats a debt capacity bargain. This is a leveraged recap. Where the EV of a debt free company can be increased by issuing easily serviceable debt and paying that to the shareholders in the form of a dividend (which i have not mentioned in the post - but the calculations will more or less remain the same). A few years back Britannia did the same thing. They issue bonus debentures and did a leveraged recap.