How to screen debt paying down bargains in screener?

1)Debt capacity bargains Screen :-

(((EBIT last year - Other income last year) + (EBIT preceding year - Other income preceding year) )/(240.11)) > *Market Capitalization AND

Debt to equity < .1

2)Debt capacity bargains Explanation:-

- Last 2 years average Avg EBIT = ((EBIT last year - Other income last year) + (EBIT preceding year - Other income preceding year))/2

Other income as one time should be excluded.

2)Maximum Defensive Interest Payment Capacity = (Avg EBIT / 4)

So that Interest Coverage will remain 4

ie…maximum amount of Interest can be easily seved

3)Now calculate Maximum Debt Raising Capacity of Firm at 11% Interest Rate = (Interest Payment Capacity)/0.11

4)Debt Raising Capacity must be more than CURRENT MARKET CAP

5)Assume existing debt should be negligible so D/E < 0.1

5 Likes

Thanks for explaining but my question is about how to find out debt paying down bargain using screener? If u go thru this http://capitalideasonline.com/wordpress/value-investing-a-presentation-by-mr-sanjay-bakshi/ link , prof explains 3 theme of value investing and i am asking about 3rd theme which deng paying down bargain

1 Like

1)Debt pay down.

When a leveraged company selling for a very low P/E ratio starts paying down debt from its cash flow and/or asset sales, then the value of the equity in that company rises automatically and quite dramatically.

**2)**Screening this type of companies is little bit difficult . According to Prof Bakshi only option is

In this theme what you need to do is to glance at the newspapers once in a while and look for transactions where highly leveraged companies are selling off assets and you know that once having learned the mistake of not having gone in that business in the first case and now getting out of it, may be for lots of money, and they are not likely to make the mistake out of diversifying, because that takes up more time. They will make that mistake maybe two years from now when they are becoming more profitable but right now debt is at their door.

**3)**With some mistakes we can screen such companies using below screen :-

Interest < Interest last year AND

Interest latest quarter < Interest preceding year quarter AND

Interest Coverage > 2 AND

Debt < Debt 3Years back AND

Net block < Net block preceding year

4)Explanation:-

a)Interest < Interest last year:::Reduction in trailing 4 quarters interest payment wrt last year Interest(Use this when First 3 /4 quarters results are available)

or we can use

Interest <Interest preceding year (when1/2 quarters result are available)

b)Interest latest quarter < Interest preceding year quarter

Interest payment in latest quarter is less than interest payment in previous year same quarter

c)Interest Coverage > 2/3/4

To have some Margin of Safety .To avoid bankrupt companies popping up in screen

d)Debt < Debt 3Years back (Optional: Avoid this screen to find out companies in initial phases of Debt Reduction drive)

Debt burden is reducing

But companies in initial phases of Debt Reduction drive can be missed out if we use this screen

e)Net block < Net block preceding year (Optional: Avoid this screen to find out companies in initial phases of Debt Reduction drive)

Companies selling off assets.

or

Net block < Net block 3Years back

6 Likes

Hi @bheeshma,

Very good work!

I was working on Zenith about an year back as everything was improving for the company and the valuations were very attractive. I continue to hold some shares. I attended the AGM of the company and I think the above post of yours in the right direction. From what I could understand - the market is limited for this product and the company has its niche and leadership. As they are already the leading player, it hasn’t been easy to grow. The product finds application in automobile sector and it takes time to get approval etc. The co seemed very very conservative and the management was very simple. For near term it didn’t seemed that they have much of growth plans…however for next year they did mention that they have lot of space at current factory and they have just started some civil work to be able to expand, if needed. Another thing they mentioned is that they have benefited by judicially buying second hand machinery at very cheap prices and the replacement cost is pretty high for similar capacity and probably this is the reason why competition hasn’t come into this area (or that its not very remunerative for a new player).

I’m still unsure about the reasons for substantial operating profit margin improvement over recent times. I worry the same may be have been due to fall in crude prices.

Regards,

Ayush

3 Likes

Good experiment. However, I believe that the same must be applied only to companies where the product and earning in future years is going to be very stable.

1 Like

Thanks @ayushmit for updating me on the AGM proceedings. Info on the company is scarce and hard to come by as it is!

Thanks for sharing this. Learned a lot by just reading that article.

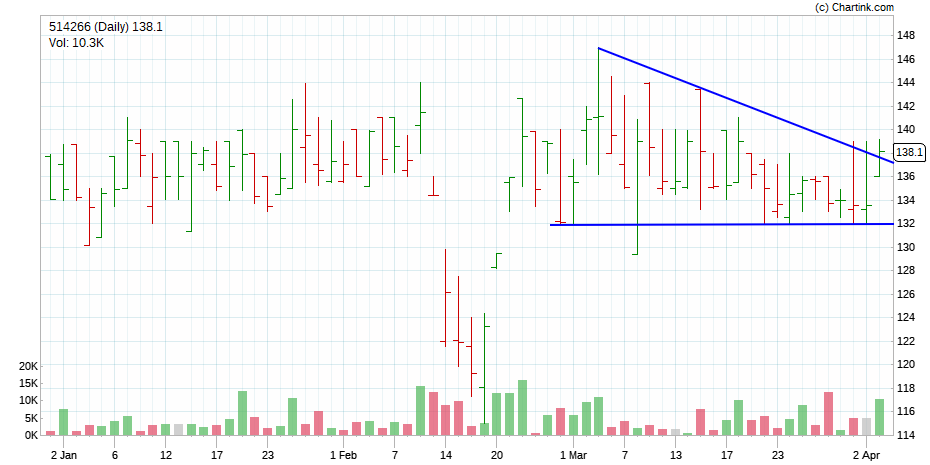

Zenith has broken out of a descending triangle formation. After an anemic past few weeks, finally Interesting times ahead for this stock!

1 Like

Great analysis ,Bheeshma. Do you have insight into sudden drop in Sales and also OPM in the last 2 quarters. Is the company feeling the heat from competition?

Information on this company is hard to come by. The AR is also not very insightful. The only way i guess is to attend the agm and get info. Till such time i am as clueless as you are! It seems prudent to assume that the psf staple fiber demand is waning maybe other synthetic fibers are gaining traction. Lets hope that it has a strong quarter. Lekin i have no substantial evidence in support

2 Likes

Looks like CFO is also following this thread ![]() . Non-current Investments are up by 15.75 Cr as on March 2017. Hope these are not diverted to some associated companies. We will have to wait till AR is out.

. Non-current Investments are up by 15.75 Cr as on March 2017. Hope these are not diverted to some associated companies. We will have to wait till AR is out.

Falling sales and profits are a concern and hope it was one-off due to ill health of the Chairman.

Discl.: Invested

Ill health of Chairman has been cited by the management as reason for falling profits?

Nope. That’s @bheeshma’s theory and I would want to believe that. We may be completely wrong in assuming this.

Yes its a theory and if recent results are taken into consideration its a pretty flimsy one!

The zenith business seems to be piling up liquid assets but there seems to be no visibility on growth prospects. It is a typical value buy with a lot of free cash flows but limited areas into which to deploy them.

3 Likes

http://www.makeinindia.com/article/-/v/technical-textiles-a-bright-future - Geo-textiles expected to grow at 30% CAGR.

hi,

what is the formula to calculate EPA ?

Is this same as EVA ?

thanks

Hi Bheesma , have always been an admirer of your detailed work,

I accidentally (which I find lucky though) got into this thread while exploring the major listed players in the Polypropylene (PP) space, from what I have understood in going through the entire thread is Zenith Fibre is a consumer of PP and coverts that into a technical textile product, what I am looking for is a listed player in the PP space to play the EV Plastic demand , in your research on the Zenith Fibres do you have pointers on the PP manufactures who supply to Zenith fibres. This is in the context of the following article that I was reading http://gcpa.themachinist.in/digital_assets/553/Whitepaper.pdf

(source of the article is also from value forum - thread - Electric vehicle disruption)

Thanks,

Pandi

1 Like