5 Likes

Press Release - Zen Technologies Introduces AI-powered Robots, Unveils Four Products for the Global Defense Market.

The products look quite state of the art.

4 Likes

https://x.com/alpha_defense/status/1812743001279742201?s=46

Video of the products in the above thread. Gives a sneak peek into them.

Regards,

Raj

8 Likes

It would be hard to believe it is indigenous. They must be importing parts. Is there any detailed information available?

Isn’t getting into new products in adjacencies good for the company even if rather than being indegenious they are system integrators??

2 Likes

I completely agree with these online articles that predict future wars will be dominated by drones rather than ground troops or expensive fighter planes. The cost difference is staggering: an F-35 fighter jet costs around $100 million, while drones range from $25,000 to $50,000. For the price of one F-35, you could purchase 2,000 drones. In a dogfight between a single fighter plane and a swarm of 2,000 drones, the drones would undoubtedly prevail.

Therefore, I believe companies like Zen Technologies, which specialize in anti-drone technology and simulators, are poised for significant success in the coming years.

8 Likes

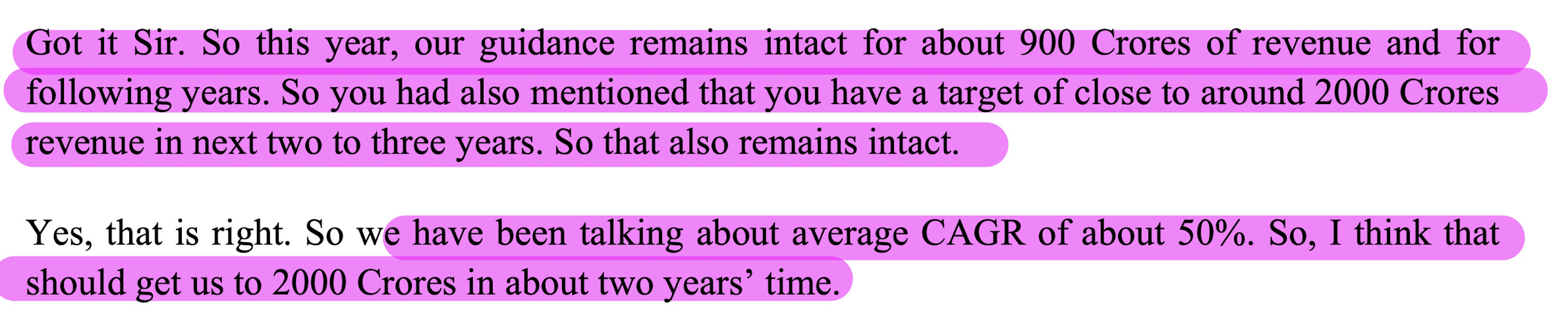

The issue is there are literally zero orders booked in Q1. The company takes anywhere between 9 to 12 months to execute orders. They have guided for 50% CAGR growth till FY28 with a target of 1500CR for FY26, currently they only have approx 3-400cr orders for FY26 assuming the 900CR for FY25. Unless almost 1000CR of orders are booked in the next 3 months I do not see how they could possibly achieve this…

5 Likes

Lok Sabha Election might be the reason for such small order Book in Q1, if not then upcoming 3 qtr decides the medium term sentiment.

2 Likes

Similarily new orders are lumpy. I think in this sector at least June is not the month rather December and March are the months for new orders.

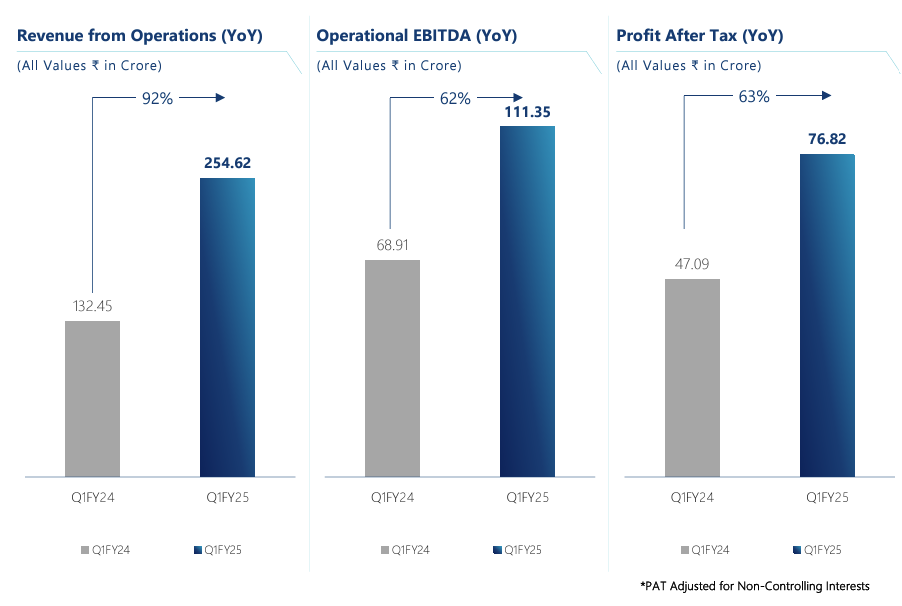

Notes from the Q1 FY 25 call

-

On track to achieve guidance of 900 cr revenue for full FY. EBITDA margin to be around 35% and PAT 25%

-

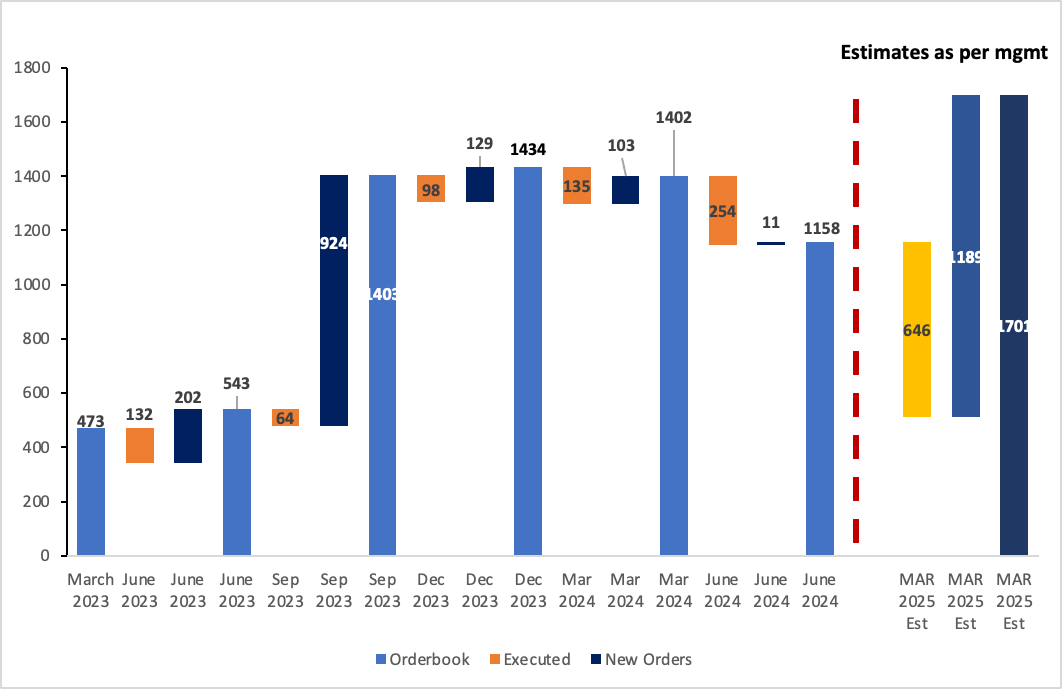

Order book – 1200 to 1300 crore by Q2 / Q3 end is what was earlier guided by management – emphasized that they are on target to achieve that order book. And expecting strong order inflow in later part of the year. Were expecting Q1 to be a little soft on order book

-

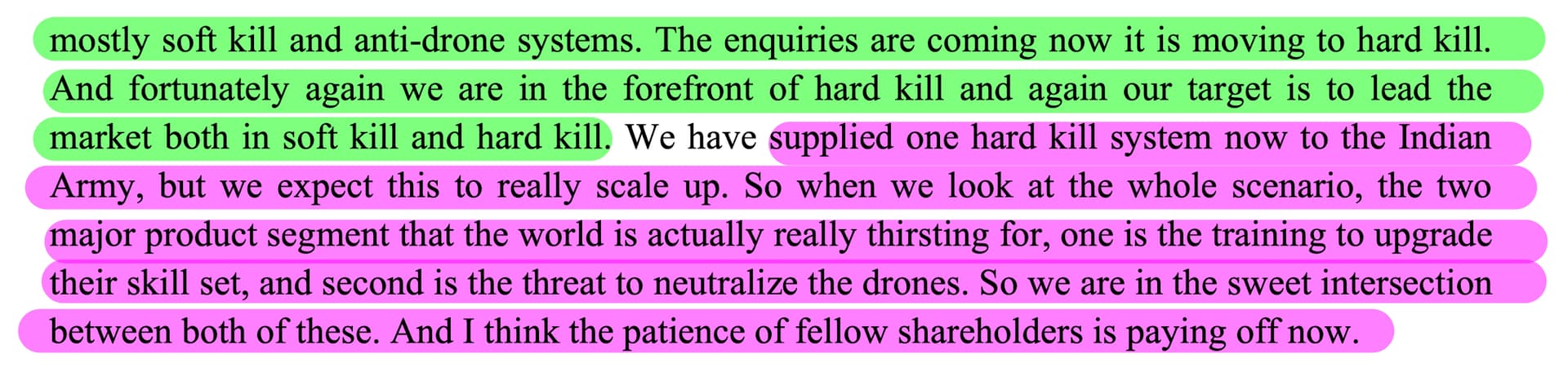

Launch of New products - (from the recent acquisition) – Witnessing Extremely healthy demand for these products. They actually showcased the new products during the call, a really commendable effort from the management

- Hawkeye - epitomizes a state-of-the-art anti-drone system camera

- Barbarik – URCWS is the world’s lightest remote-controlled weapon station (weighs less than 40 kg), offering precise targeting capabilities (5.56mm to 7.62mm calibers) for ground vehicles and naval vessels.

- Prahasta - a revolutionary automated quadruped that uses LIDAR and reinforcement learning to understand and create real-time 3D terrain mapping for unparalleled mission planning, navigation and threat assessment. Can be used as first line of defence in 26/11 kind of scenarios

- Sthir Stab 640 - a rugged stabilized sight designed mainly for armoured vehicles, ICVs, and boats

-

This will be an additional stream of revenue (from these products); in addition to the revenue guidance shared earlier. This is a more established field unlike simulators and anti-drones. There are established players in the segment.

-

Strong tailwinds - Indian defence mkt is on a different trajectory. Govt pursuing simulator procurement in a big manner. Orders received so far is just the beginning. Good demand for simulators in airforce and navy too

-

Indian army has one of the toughest screening criteria for procurement. While approaching overseas clients for exports, first question is ‘Have you sold it to the Indian Army’ post which they look at other points

-

Exports – much larger market than domestic.

- Margins depend on risk involved, export margins are usually higher than domestic margin

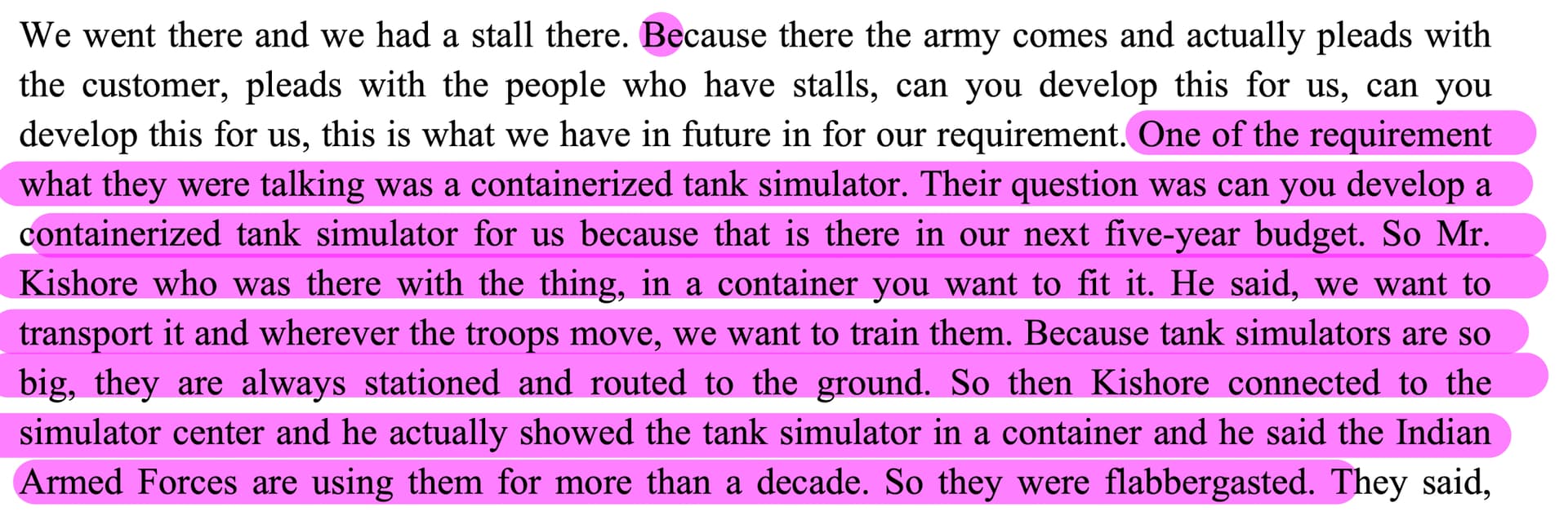

- Some of the companies overseas were highly appreciative and were stunned by the skill sets and capabilities of companies like Zen Tech. Gave the illustration of Containerized tank simulator to explain.

-

QIP – Only taken the enabling resolution . no funds raised yet

-

Exploring inorganic growth opportunities through acquisitions, will be able to give more guidance in upcoming quarters

10 Likes

Why would it be an antithesis pointer when management had already said that they anticipate new orders only in H2?

2 Likes

Maybe wrong choice of words at my part.

What I wanted to articulate is that order book is the key indicator / monitorable.

As with the managements it’s always trust but verify. One can’t take statements at face value.

So if orderbook doesn’t get recouped it will be a damper on the growth.

I am optimistic and invested (6% position)

5 Likes

Company’s current o/s order book after Q1 is 901 Crores excluding AMCs.

Company needs to do 645 Crores topline out of current 901 Crores order book o/s to achieve 900 Crores FY25 target, hence even after that company is left with 256 Crores of order with they will deliver in Q1 of FY26.

Hence, in my opinion company has enough time to replenish its order i.e., till June 2025, which is a long-time away.

Company in this time period needs to get orders of 1,094 Crores to do a 50% topline growth in FY26 over FY25 and in my opinion with new product launches, current tailwinds in current established products, company will be able to do that.

8 Likes

With this amount how many drones a country can buy!! Then they also need anti-drones too to counter the enemy UAV drones.

2 Likes

Concall Transcript is now out. Here are my notes.

In terms of business, the concall was very assuring and many of my concerns have been allayed.

Management Guidance

900 cr revenue for FY2025

~35% EBITDA Margin and ~25% PAT margin

Don’t look at Quarters but the whole year as product mix may change and execution could be lumpy

Have healthy enquiries for both their businesses i.e. Simulators and Anti Drone

Have launched new products. Market size for these products is in 1000s of crores however detailed study required to know the market size. There will be more announcements in this area.

New Orders will come predominately in Q4.

Simulators

15000 cr is the opportunity size

High margin segment with ~40% EBITDA

What drives this segment?? - Huge cost savings, reduces downtime etc.

Simulator induction is at nascent stage + new platforms will require simulators

Anti drone

Demand to be revised upwards from 10,000 cr

EBITDA margin in this segment ~30%

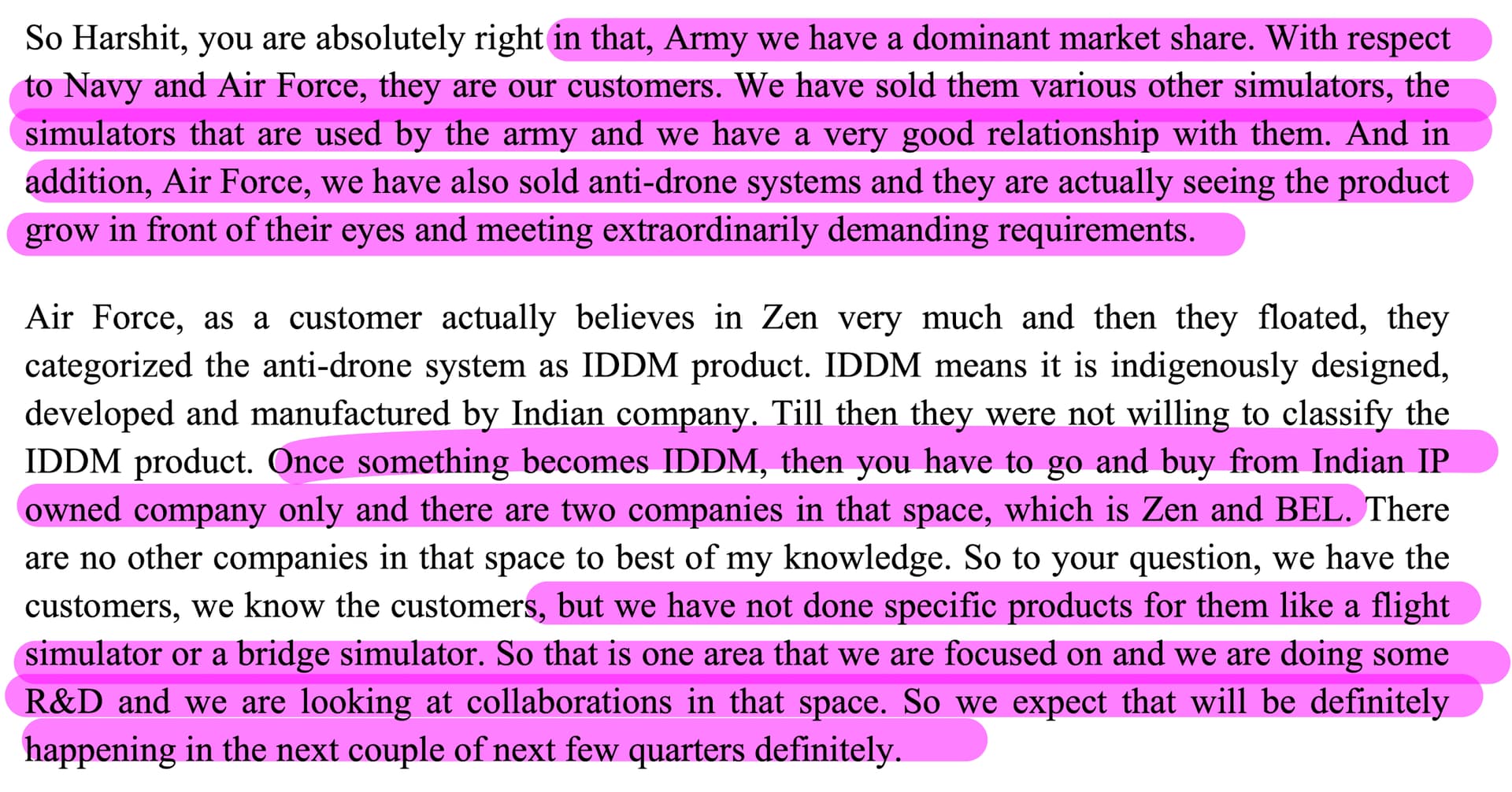

ADS are in IDDM list. Only other player is BEL

QIP

Enabling resolution - not raised funds yet

Looking for inorganic opportunity

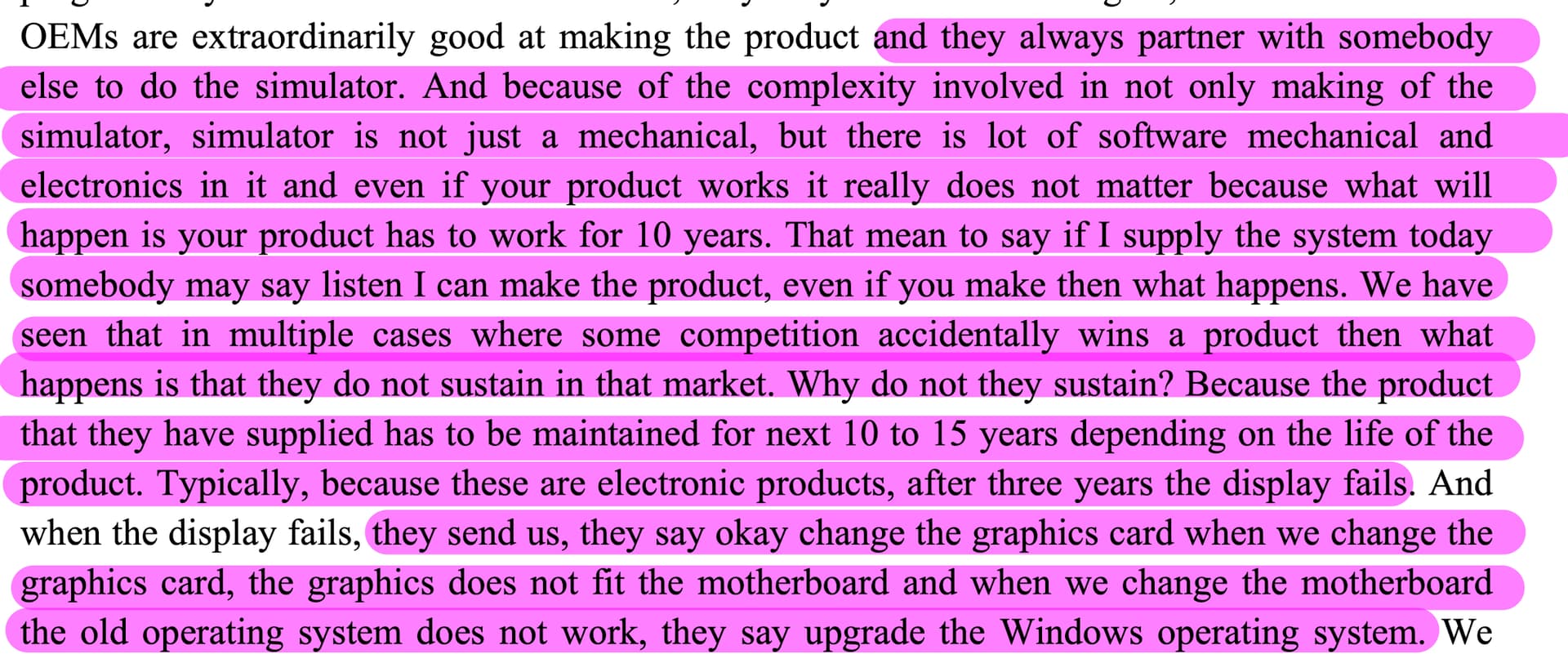

Why AMC matter and why simulators are not done by OEMs themselves

50% CAGR is this sustainable?

My take:

In the overall scheme of things the company is still a 15000 cr market cap company. They are growing rapidly and things like growth in simulators and ADS makes sense.

Simulators you need to train - it is an effective way to train and given the nature of modern-day warfare are crucial components.

Key Monitorable from Concall: Order wins by Q4, execution in between and new products

Disl - Invested and biased

18 Likes

4 Likes

Zen Technologies has launched a Qualified Institutions Placement (QIP) to raise ₹800 crore, with an option to scale up to ₹1,000 crore. The base issue will account for 5.95% of the company’s equity, which can increase to 7.43% if the full amount is raised. The shares are priced at ₹1,601 each, representing a 10.2% discount to the last closing price of ₹1,782.55 and a 5% discount to the SEBI floor price of ₹1,685.18.

Key Details:

- Issue Size: ₹800 crore, with an option to increase to ₹1,000 crore.

- Price per Share: ₹1,601 (10.2% discount to last closing price).

- Lock-in Period: 60 days.

- Shares Offered: Equity shares with a face value of ₹1 each.

- BRLMs: ICICI Securities, Motilal Oswal, Nuvama.

Use of Proceeds:

- Funding working capital requirements.

- Supporting inorganic growth through acquisitions and strategic initiatives.

- General corporate purposes.

Timeline:

- Launch Date: August 21, 2024, after market close.

- Closing of EOI: August 22, 2024, by 08:45 am IST.

6 Likes