why putting dcx news item in zen thread sir ? Kindly delete.

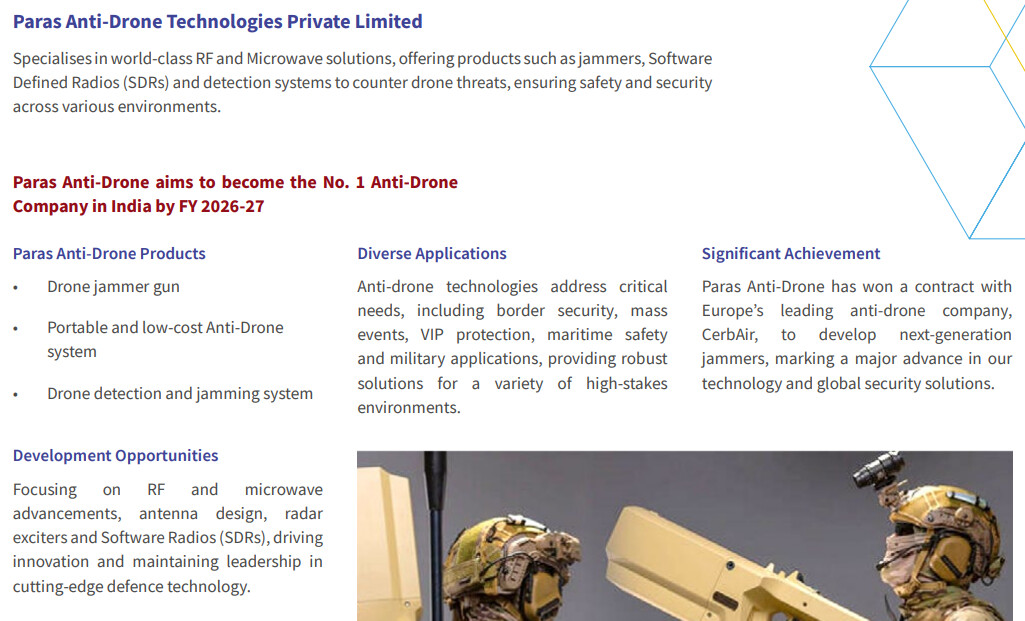

Was going through Paras defence and saw this in their AR:

Rattan India is also looking at anti-drone system:

https://idrw.org/rattanindia-trials-the-defender-an-indigenous-anti-drone-system/

Would be good to watch what is happening in anti-drone technologies and who is capturing the market share.

Disc: Invested in Zen Tech

Financial Results for H1 : https://www.bseindia.com/xml-data/corpfiling/AttachLive/020a71ed-3325-4965-bcb0-cda9f847bc90.pdf

Good set of results. YoY Q2 revenue is almost 4x (242 Cr v/s 66 Cr) and profit is ~4.5x (63 Cr v/s 14 Cr). Half year revenue has already surpassed the revenue for FY24. Looks like they are on track to more than double the revenue and profit in FY25. The MD has previously said that FY25 revenue will be about 900 Cr, which is about 2x of FY24 revenue of 441 Cr. So the management is walking the talk.

However the order book is a big worry. It stands at about 1000 Cr right now. Based on the management guidance, I am guessing that orders worth 500 Cr will be delivered in Q3 and Q4 FY25. So essentially for FY26 the company right now has an order book worth only 500 Cr. To justify the lofty valuations (TTM PE is ~80), the company needs to get additional orders worth at least 1300 Cr, which will help it double the revenue in FY26. We are already about 8 months into the financial year and it doesn’t look like this is going to happen. So it looks like the revenue growth will moderate a bit.

The MD has previously mentioned that the margins will moderate as well. I think we have seen a peak OPM of 41% in FY24. Expecting it to be around 35% in FY25 and 32% in FY26. A combination of lower revenue growth and lower margins will see the earnings growth moderate by much more than the revenue growth. So I don’t see a lot of upside from these price levels (~1880). A couple of big orders will change this, so need to keep an eye out for that.

Let’s discuss Zen Technologies’ financial performance and outlook based on the interview with Ashok Atluri, Chairman and Managing Director, on CNBC TV18.

- Zen Technologies is confident in achieving its revenue guidance of ₹900 crore for FY25. They believe they are on track after a good performance in the first two quarters.

- They expect EBITDA margins to be around 35%. While first-half margins are currently higher at 36.8%, they are maintaining a conservative outlook.

- Receivables have increased, impacting operational cash flow. However, the company expects to collect most outstanding payments within the next two months and bring down receivables. They anticipate average receivable days to stabilize around 150 days.

- Exports are also expected to remain strong, contributing approximately 30% to the total order book. They are on track to meet their export guidance of ₹300 crore, having already achieved 133% of the target in the first half of FY25.

- Order replenishment is anticipated towards the end of Q3 and in Q4 of FY25. The company expects significant order inflows during this period. Excluding approximately ₹35-40 crore from annual maintenance contracts (AMCs), the remaining ₹850+ crore of the ₹900 crore target will come from equipment orders.

- Zen Technologies is actively pursuing inorganic growth opportunities through acquisitions. They are looking at potential targets in the electronic warfare and simulator segments, with deal sizes ranging from ₹100 crore to ₹300 crore. They aim to close an acquisition in FY25, but significant contributions to growth are expected in FY27 after the integration process is complete.

Overall, Zen Technologies appears to be in a strong position to achieve its growth targets for FY25, driven by strong domestic demand, robust exports, and potential acquisitions.

Key takeaways from Q2FY25 Concall:

Expect 3500 cr orders expected in H2 FY25 (2000 cr is already bid and 1500 cr yet to be bid), Simulators and anti drones may have approx 60:40 ratio.

Guidance is for 900 cr In FY25 with gross ebitda margin of 35%. Guided for 50% CAGR for next 3 years.

Surveillance and remote control driven systems are in R& D stage and expect the revenues to flow in from FY26 onwards.

Capabilities in simulators meant for army planned to be extended for navy and airforce. Currently mostly in WIP/R&D and may yield revenues from FY27 onwards.

Has plans of USA and will adopt the similar strategy what is being done in India where in 85% of manufacturing job works through SMEs. With Trump’s administration, they expect good push on make in America and good supply chain availability in USA. 50% guided CAGR excludes any possible revenues from USA. Expected capex could be around $10 mn in FY26.

QIP money of Rs 1000 cr would be utilized for possible acquisitions in companies having technical capabilities in navy /airforce simulators. 400 cr is budgeted for acquisition and 100 cr for India capex.

Overall appears to be a consistent compounder story, but rightly valued currently. Triggers would be new large orders which promoter is quite confident about (they have walked the talk largely in past). Success in efforts in R&D and diversification of products would pave the way to beat 50% guided.

Disclaimer: Remain invested

One correction to Jitendra’s post , and few more points

1- Correction - the fresh orders expected in H2 FY 2025 (until 31st Mar 2025) are for 1200 crores (not 3500 crores). 3500 crores is their order pipeline.

Other points

1- Expect the receivables to come down significantly in this and next quarter. In the current Trade Receivables amount, major chunk is from recent times.

2- Company is confident of clocking at least 900 crores this year. Despite a lot of questions around 500 crores is already done in the first two quarters, so the H2 should be just 400 crores?', the management stuck with their guidance. They simply do not want to over commit and under deliver (like last year).

3- The management believes that they would be able to clock 50% CAGR post current year for the next three years. The EBITDA would be 35% and PAT margin 25%.

4- The management believes that their products in Simulators category is top notch, and even in the ADS (Anti Drone Systems) they are very competitive.

5- They are primarily an IP company. They get 85% of goods from suppliers and only 15% is manufactured by them. This asset light model helps them keep fixed costs in check, which helps them during dry order periods. They would have similar model in US.

6- The company is keen on acquisition but does not want to rush into it. Mr. Ashok emphasized that he would be extra careful putting any money and not do acquisition just for the sake of it.

Overall, my sense is that the company is on strong footing. They trust their skills and products. While the Ukraine-Russia war may end because of Trump, the need/market for the simulators, anti-drone systems, remote controlled weapons and surveillance is only going to go up. Key monitorable would be order book; they need to get wide & deep traction for their products and build many years’ worth unexecuted order pipeline.

Cheers,

Krishna

Thanks for correction. By mistake mentioned that way though in my mind H2 expected orders was 1200 cr.

Lots of innovation and demand on the anvil in drone and anti drone systems . Opportunities for drone companies and anti drone operators like Zen.

Zen signs MoU with a leading US company paving way to new export market.

The company has formalized its partnership with Applied Visual Technology Inc. D.B.A AVT Simulation, a premier provider of customized training systems, through a Memorandum of Understanding (MoU) inked today in Florida

zen-technologies-limited-targets-u.s.-expansion-with-strategic-partnership-with-avt-simulation.pdf (535.8 KB)

He is mentioning that there is delay in order placements from Indian government, I have a feeling they are unable to easily backfill the order book and that’s why stock is crashing.

In a positive he is saying exports growth should be strong.

Order book for Q3 is almost NIL , management guided for RS 900 cr Top line for 2025 & RS 2000 cr for 2026,

Other income is 50% of current quarter EBITDA

Really worried about the order book lag too. Historically, Zen’s financials have been all over the place with a 1-2 year peak followed by decreased revenues. Market will never favourably view that and will not give a premium valuation anymore. It’s good that they are doing acquisitions but that cannot save them. I would not even care about the lower financials… it is rather the absence of order intake which is the most scariest. With that matter, any guidance on orders in pipeline atleast would help their case.