Thanks @hitesh2710 Hitesh BHAI @Uservijay VIJAY JI for finding time to visit about the pointers in BRITANIA I had share my views in that thread .

Admid of the meltdown i want to analyse my portfolio and effect of the severe fall and found that THE CAPITAL ALLOCATION has protected me a big way .Thanks to thread one must pay sufficient time in studying the thread

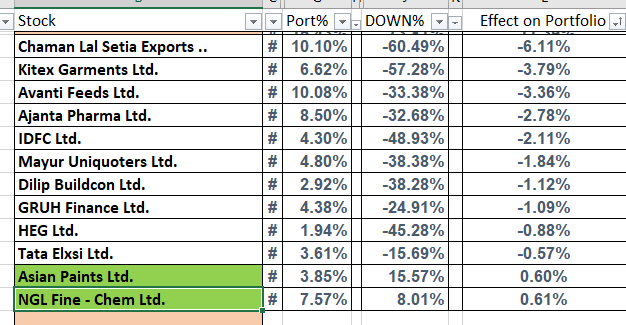

Everyday is a learning i want to share snippet from my portfolio

stocks are gone down from 15% to even 60% FROM MY PURCHASE VALUE …

WHAT I ascertain from this the MAGIC of WAITING and patience However the great learning

The stock may or may not come to low hanging bu the QUALITY AND @what price you pay MATTERS A LOT … i want to share a couplet recently heard from my friend

AGAR KAM KA AYE TARICA to SAMJHO india MIAn AMERICA–

each passing day i feel i know nothing

HOW TO CHECK THE effect one equity on one’s portfolio = %in Portfolio X DOWN or UP % in equity

Regards