Hi folks, I’ve written about the Yes Bank AT1 bonds saga here from start to now. Hopefully a good summary for those interested in learning about it:

Banks usually fund themselves by borrowing. They can “borrow” from a customer (that is, by taking in deposits) or they can issue bonds (that is, take loans from investors and pay an interest). But both of these have to be paid back! A customer can withdraw their money at any point. And bonds usually come with a “maturity date” when the bank has to return the principal back to the investor.

A nicer way for banks to fund themselves is by raising “capital” or money that it won’t have to return. A straightforward way to do this is by selling shares to investors. By law, banks need to always have some capital. If things go wrong, it’s this capital that comes to the rescue. All those borrowings have to be paid back somehow!

But selling shares to raise capital is expensive. Investors that buy shares expect double-digit returns, start owning a part of the company, and might get annoying and demanding. An alternative, a jugaad, for banks is to issue something called “Additional Tier-1 bonds” or “AT1 bonds” which are a cross of bonds with some useful features of equity (stock):

- Like bonds, AT1 bonds have a fixed face value (principal amount) and interest rate. If you buy an AT1 bond worth ₹100 with 10% interest, you’d get ₹10 every year

- Like equity, AT1 bonds don’t have a maturity date so you might never get back the principal. If you buy bank stock, the bank is under no obligation to pay you back for your stock, ever. Exactly the same with AT1 bonds

- Like equity, if the bank gets in extreme trouble, it can just say “sorry about this :(” and delete its AT1 bonds. Their value can go down to zero

- Oh and the initial interest? Banks can choose to skip interest payments if they’re having a rough day (they can’t do that with regular bonds)

Banks like AT1 bonds because they behave like equity and are a part of their capital because they don’t need to be paid back. Investors like AT1 bonds because, in their mind, they’re bonds with a higher-than-usual interest rate and a fixed principal. Unless things go really bad!

Of course things went really bad! In March 2020, Yes Bank was on the brink of death and was essentially taken over by the Reserve Bank of India (RBI), the banking regulator. The RBI did a bunch of things and turned Yes Bank into “Yes Bank 2.0” with new owners and a new management. The new management took the call to, well, delete all its AT1 bonds. Whoever held those bonds got nothing.

Bond investors obviously didn’t like it. The bonds were worth ₹8,400 crores ($1 billion) and they became zero. Tough luck, right? Someone who buys an AT1 takes the risk of losing their money for a bit more interest if the bank goes through trouble. Just like they do with equity! [1]

How it goes in finance is that an asset is sliced and diced into small pieces and those pieces then sold off to investors based on who wants to take how much risk. An investor buying a fixed deposit, for instance, wants 0 risk and is okay with less return. A bond investor takes a bit more risk and gets a bit more return. An equity investor takes the most risk for potentially even more return. On this spectrum, an AT1 bond lies somewhere between bond and equity, maybe closer to equity than to bonds.

When Yes Bank got into trouble and the RBI got involved, the first thing that it did was to ensure that customers with deposits were safe. Next came the bondholders. Standard stuff. But then Yes Bank 2.0 saved its equity investors [2] while asking its AT1 bond investors to go away with nothing. Of course they went to court. [3]

The Court’s cop-out

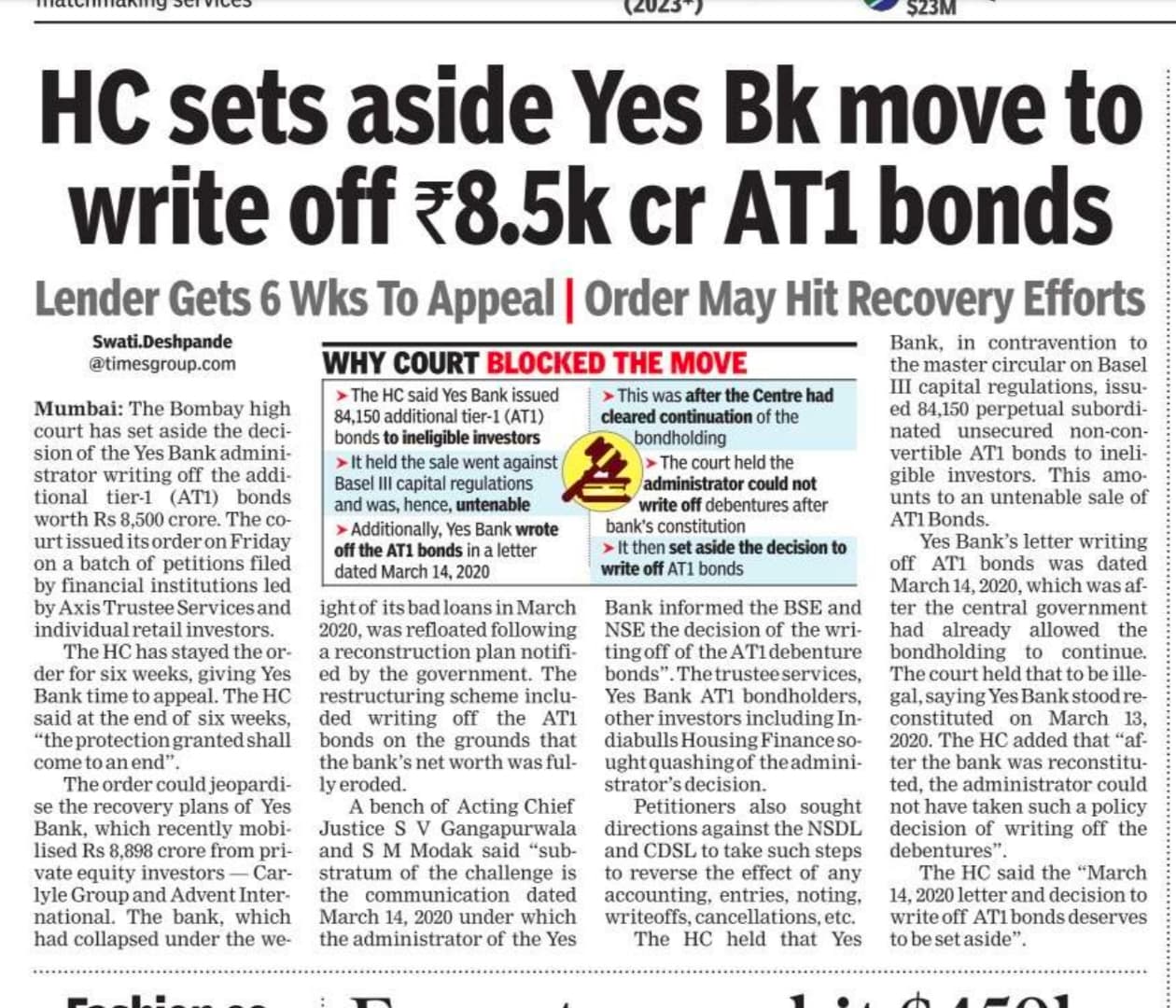

Last Friday evening, the Bombay High Court decided that maybe the AT1 bonds were not erased fairly and revoked Yes Bank’s decision to write them down:

The Court also observed that the final reconstruction scheme for the bank did not contain the clause for writing down of AT-1 bonds. “Upon consideration of the objections the Reserve Bank made modification in the draft scheme. It deleted the clause of writing down of AT-1 bonds. The final scheme sanctioned by the Central Government did not contain the clause or provision for writing down AT-1 bonds,” the Court observed.…The Court clarified that the matter being fiscal in nature, it would not dwell on whether writing off the AT-1 bonds was necessary but only deal with the decision making process.“We would not enter into a debate as to whether the AT-1 bonds could have been converted into the shares and or whether they could have been proportionately written down. The Court would not possess the necessary expertise of the same” the Court said.

The Court is saying that after the RBI swooped in to save Yes Bank and appointed a new management for Yes Bank 2.0, the RBI didn’t mention in their transition document that the AT1 bonds must be written off, so apparently Yes Bank 2.0 overstepped its authority by doing so. This is a major cop-out because it doesn’t answer the main point of contention: can AT1 bonds be erased before equity? Instead, the judge asks to bring back the AT1 bonds because of some minor lapse in documentation.

This obviously doesn’t end here. Yes Bank has already decided to appeal this decision in the Supreme Court and it’s likely going to be some more years before this ends.

Imaginary bonds

I like to think about what happens if the erased AT1 bonds from the original Yes Bank come back into Yes Bank 2.0. Here’s Prashant Kumar, CEO of Yes Bank v2, indulging the same thought experiment:

The Bombay High Court’s order on Yes Bank Ltd.'s additional tier-1 bonds issue will not have any impact on the lender’s capital structure, said the lender’s Managing Director and Chief Executive Officer Prashant Kumar.“There is no inflow or outflow of any money or liquidity. It will be on the change in CET (common equity tier-1) and AT-1. There would not be any impact on the tier-1 capital,” Kumar told reporters in a conference call after announcing Yes Bank’s December quarter results.

Also,

When asked whether the interest component on the AT1 bonds could impact the balance sheet, Kumar said that interest payments would be within the bank’s discretion.“On the perpetual bond, it is the discretion of the bank to pay interest or not,” Kumar said. “At this point in time, I would not like to add anything further.”

What Kumar is saying here is that even if the Bombay HC decision stands—it doesn’t matter. Yes Bank 2.0 is a bank that has decided it does not want to pay the old AT1 bondholders. If the bank’s forced to bring them back, it will bring them back on paper and that’s about it. The bank will point to a small component [4] of its capital and say “this is now AT1 bonds instead of equity,” and continue paying no interest. No money changes hands, nothing changes for anybody. The bonds would both exist and not exist at the same time, it would be a bit funny. [5]

If there were a lesson to be learnt it’s probably that you can’t force a bank to pay you if it really doesn’t want to.

Footnotes

[1] A problem here that’s probably very India-specific is that a non-insignificant number of individuals were mis-sold AT1 bonds by Yes Bank v1 with the promise that they were as safe as fixed deposits. Here’s a piece from December 2021 about a 61 year old widow who got duped out of her life’s savings by the bank’s relationship manager. I don’t even know how to deal with this problem.

[2] By “saved” I just mean that the equity wasn’t written down to zero like with the AT1 bonds. The RBI invited a few other banks to buy stock for cheap and in effect diluted the holdings of existing investors. So they did lose—a lot—but not everything.

[3] The fundamental issue here isn’t that the AT1 bonds were erased. The issue was that the bonds were erased even though the equity wasn’t. If both equity and the AT1 bonds were written off this whole saga wouldn’t have happened.

[4] What this small component could be would likely again be a big point of contention. It certainly wouldn’t be the original ₹8,400 crores but a much smaller chunk of the capital.

[5] In the future, if Yes Bank 2.0 recovers fully and comes back into good times, the bank might very well choose to start paying interest again. But until then, the bonds are imaginary.