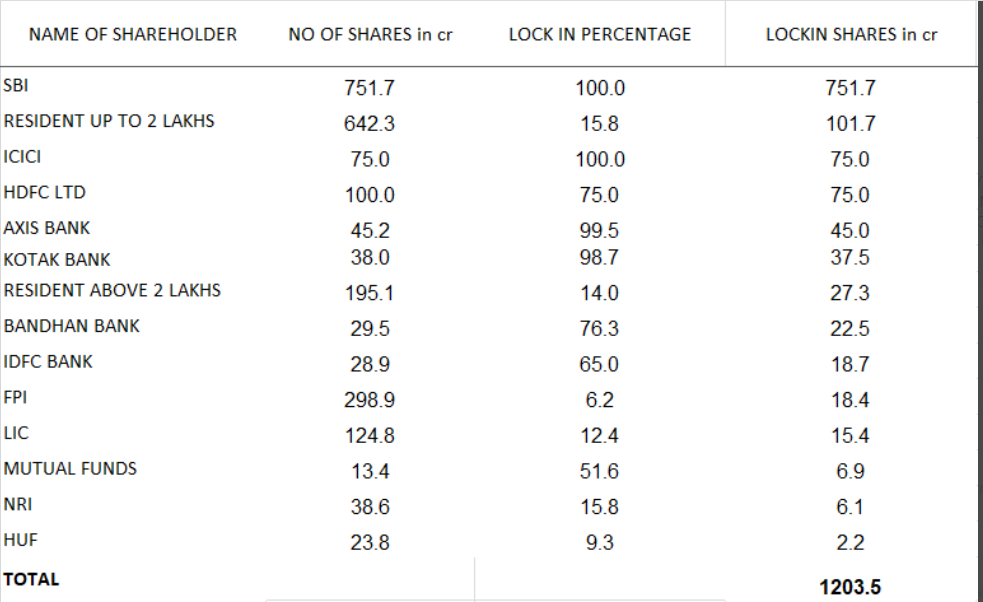

SBI and LIC will not sell. LIC has maintained its shareholding in Q1,Q2,Q3 so why sell now. SBI has saved yesb and yesb has indirect support from GOI so SBI selling does not make sense. PK has also given hint in concall that SBI wont sell

IDFC had an opportunity to sell 10cr shares 35% of it holding why it did not sell till now. I would assume max 30% selling from them on locked in shares. 6cr

Same applies with HDFC,BB . They did not sell 25% of unlocked shareholding

I fell BB can sell a good chunk let say 50%. 15cr and HDFC,AXIS,KOTAK,ICICI will hold. We have to compare invested amount to the investment portfolio of respective banks. In short they are peanuts for them.

can be wrong here as ICICI,KOTAK,AXIS have all their shares locked and how they would react is something which cannot be predicted but PK was confident and indicating that institutions wont sell

Total 134cr locked in. Let us assume 70% of them sell which is very high considering most of them would be at 50% loss. 94cr

The entire selling is going to be under 150cr(conservative). In my view max 2rs fall with these volumes

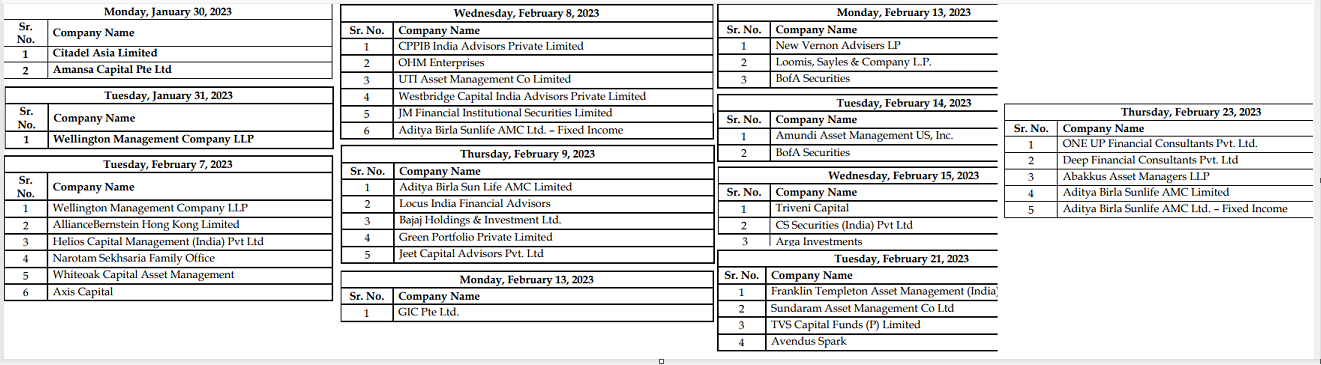

Between 30 jan and 23 feb. 19 working days they did 11 investor meet. Mid boggling

This is a very important point to look at. Both institutional buyer came at 14.2 avg price these levels are a no brainer to most of the instructions.

They have a book value of 14. This grows at a faster rate than profit because of 9000cr of Deferred Tax asset. For a Private bank with 1% NNPA PB of 1 is criminal

@Aarti maam you actually ended up being right but I am not a 100% wrong I started posting here when the price was 12 to 13 and it went up to 25. Yes but I believed it can go to 35 to 50 which as on date looks tough

I have recently developed the understanding that how important is cost to income and the provisioning for SR was also something new for me. I think next year is also going to be tough form them and they wont be able to generate high incremental revenue.

I would like to exit this stock now. Learnt a lot, Accepted my mistake and very important did not loose money.

I think even in IDFC case most of the people realized C&I is high and excited despite in the beginning expecting multi fold returns.

In SIB case Q3 was a result was a surprise for most of them as SR related provisioning was there.

So if this can happen with experienced investors then I am pretty new and fell for it.

My thesis was they can grow book value at a faster rate than earnings which is actually happening but what I could not see was there has to be some earnings to get that 1.7 or 2PB which as of now I don’t see

Atleast for next 3yrs I don’t see a turn around and as the get close to turning around they will have to dilute further. But as many say it is going to go bankrupt or is a fraud I don’t agree with that the price as per me should be in this range going forward as well

Market is a great place to learn… you have at least not lost money in the proces…

Yes bank can never make money as their cost of deposits are very high… and on that a huge employee cost… if you see banks which have given good returns have reduced cost through increasing CASA balances and lowering of deposit costs. and at same time use technology to keep employee costs low. Yes bank is not doing either of these… they will not be able to also… Deposit rates have to be higher so that people put money in yes bank. people will not make yes bank their primary account so CASA will never pick up and lasts employee costs are high which every one can see… and to top it all provisions for bad loans still high.

trust lost in a bank can never be recovered… it has happened many times in the past…

Disclosure - sold at huge losses… have written it off and moved on.

Congrats, all of your stocks were high growing ones. Yes bank eventually turned dud (which you eventually sold in 2014 itself anyway), but the rest were miltibaggers!!

Eventually, we did see yes bank and indusind had similar kind of problems. Run by family, giving aggresive loans (and to promoter friends).

What were your learnings in the banking sector?

Have a few questions for valuepickr community at large?

How do you view the current environment of aggresive unsecured loans to retail? Do we have some case studies of some countries where it succeeded or backfired?

How do you view the effort by yes bank to increase casa? Will it work?

Yes bank has one of the best brand recognition? But does this actually help considering its a bit in negative side.

If I may, here’s an alternative macro perspective with a bit of scuttlebutt:

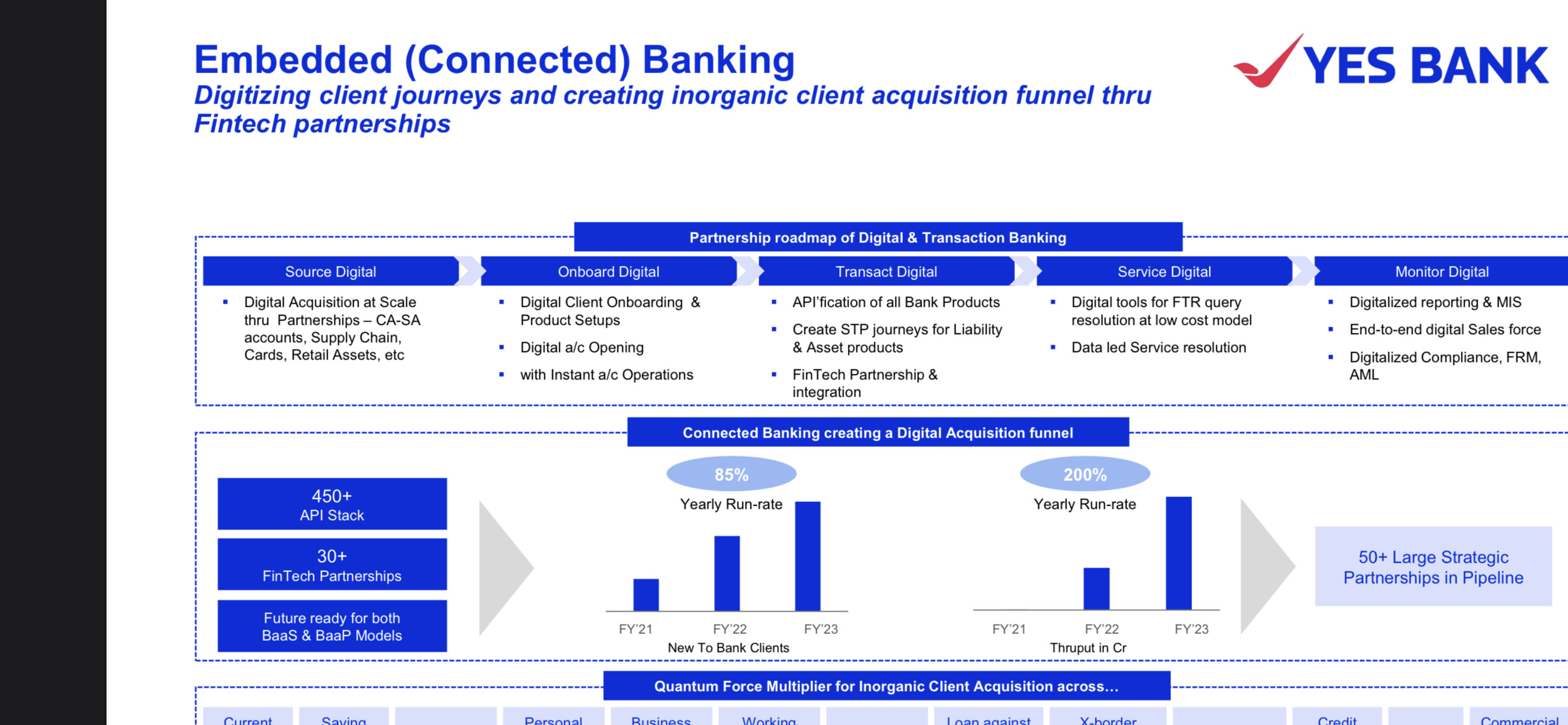

Yes bank has one of the best tech architecture across Indian banking system that I know of. They started to build APIs at least 5 years ago and they were working with multiple small fintechs at that time . Their investor presentation says that they process 40% of all digital payments in India !

The brand recall is good and even though the bank has gone through issues, there was never a run on the bank. I, eg , continue to run one of my primary account with them

I own one of their cards and have seen that their fraud management practices are better than any I have seen

Their CASA has not done well - don’t know the underlying reasons but I don’t think that over a period this is not a solvable issue . ( most of you may recall, yes bank was the first bank ever to give 7% interest on savings deposits)

SBI parentage is actually good because sbi itself has done a bit of transformation (someone one can’t say about any other psu bank including bank of Baroda )

Their Npa issue is behind them and with retail franchise now 40%+, the NIMs and ROA should improve

And I guess they have done well on SME banking as well

I would tend to think that over a 3-5 year period, there could be a significant growth possibility.

Ignoring asset quality and reverse calculating- just based on Earnings and multiple at 20x PE (HDFC bank is 20x) the PAT should be 2,500 cr. Is this even possible!!

if you go for lower multiple of 15 or 10x then it become even more impossible

everybody know asset quality is not great. Yes bank pricing is higher so riskier borrowers or those not getting loan elsewhere will borrow from yes bank

just fyi UPI payments and credit cards are loss making

After all of this if by some miracle goes to 24 again you are making 40% return. Analysts have given target of 2,200 to HDFC bank which is 30% from current prices.

Well P/B is 1.3 which was sitting at 2.5 3 years ago when the book had a lot more mess in it. And HDFC’s P/B is nearly 4. And if I’m not mistaken , it was HDFC whose CIO had to lose his job due to app issue…. So, I guess there’s some story here.

Again, it’s not a recommendation and everyone has their own risk appetite

Summary:

Profit: 10.26% YoY rise amounting to 342.5 crore (314.3 crore in Q1FY23)

GNPA: Significantly dropped from 13.4% a year ago to 2% (Because of bad loan transfer to JC Flower?)

NIM: 2.5% up by 10% YoY

Deposits: 13.5% increase YoY

CASA ratio: Dropped to 29.4 from 30.8 (only negative metric)

So they now have about 1400 CR in PAT on an annualised basis - that’s closer to 2500 Cr than it was last quarter. Point being everyone knows the bank is rising from the ashes. Which is why there is an opportunity for those with patience may end up being rewarded with asymmetrical returns. The market always rewards outlook into the future. And for reasons stated earlier, IT framework, user experience and even the shift into retail lending may all add up to a stronger outlook. The HDFC online user experience is far short of Yes platform. Disclosure - Invested for long.

Yes bank investors are the most optimistic lot in the market… hoping for something not achievable.

ICICI direct has given target of 14. After many more who have given targets of 14/13/11/10.

Do not listen to brokerages as they have their own axe to grind. Agreed that Yes Bank has huge equity of 2900 Cr shares. Remember that the bank has very big branch network PAN India … If bank manages to perform better, then it can be a good turnaround story. Only time will tell; and patience will be rewarded.

again terrible results !! its not going to improve… business model failure. once stress in retail portfolio happens - which will happen to many retail lenders- yes bank can go back into losses… high risk low return stock.

The media folks don’t think or analyse before ‘creating’ news from regulatory filings.

HDFC Bank now is the promoter of HDFC AMC and HDFC Life.

Whenever an institutional investor such as life insurance companies and mutual funds want to increase holding in a bank, they have to prematurely apply to the RBI for approval.

This is exactly that - when HDFC Life or AMC want to acquire more stake in Yes Bank or IndusInd Bank - essentially as the owner of these institutional investors HDFC Bank (parent) must apply for RBI permission.

Remember when there was hurrah around LIC approval to own upto 10% of HDFC Bank. LIC buying the dip, bla bla bla. LIC doubling stake in HDFC Bank…

Focus on what matters folks - lots of noise around everywhere.

I think this could be another reason for the recent rally

Clarification from Yes bank

“Yes Bank LeRemitt in pact to enable smooth cross border transactions for MSMEs”.

"In this regard, the Bank would like to clarify that the news regarding the Bank’s tie-up with

LeRemitt, a fintech start-up is in the normal course of business of the Bank to enable Digital

solutioning for the MSME customers of the Bank. This arrangement is currently at a nascent

stage and has absolutely no material impact on the business volumes or revenues of the Bank. "