Current P/B - 1.11

PEs gave 8900cr at P/B- 1.05

Now, with RoA only 0.5, the valuation looks expensive, considering many other bans with RoA more than 1 are available for P/B< 1.

In short, that “MARGIN OF SAFETY” is not there.

Current P/B - 1.11

PEs gave 8900cr at P/B- 1.05

Now, with RoA only 0.5, the valuation looks expensive, considering many other bans with RoA more than 1 are available for P/B< 1.

In short, that “MARGIN OF SAFETY” is not there.

Hi guys,

Extremely happy today!

MY target was 18 by jan to march 2023 and todays high was 17.95. They will be doing one of the largest capital raise and these 2 PE firms will be board members as well. I am confident of yes bank sustaining 18 to 20 my this financial year end and a long term view of 35 to 50(FY 25 end).

Now you will see DII entering into this and slowly slowly there will be research report on this giving buy targets all this is going to build up slowly here.

Why is it up today? there is a news in market that THE ADITYA PURI who has built 20 lakh cr bank HDFC bank is one of the senior advisor of Carlyle and there is a high chance of him coming into yes bank board. Yesbank is up by 15% when all of this is just speculative but if all of this comes out to be true then this stock is going to fly.

Adity puri being senior advisor of Carlyle is true. What my point is once speculation comes into a stock and there is a craze in market nothing works on valuation. Yesbank went from 5rs to 80rs in 4 days. Such move is not possible now but we neve know when thing trigger.

If you ask me I don’t want to price in all of this news as of now but certainly the future is bright here

According to valuations it is overpriced as of now but nobody knows to what extent it can be overprized and for how much time.

Prashanth kumar was asked weather aditya puri will join or not. Above article will give clarity

Hi guys,

The above article is extremely beautifully articulated and would recommend all of you to read it even if you don’t follow this bank. This article beautifully explains the hurdles for yes bank but it also shows the hurdles for small banks as well.

MY INTERPREATION OF THE ABOVE ARTICLE

They have emphasized on the importance of these rating agency. These rating upgrade have a huge impact on overall cost of the bank. Yesbank is almost 4 to 5 levels below the top private banks.

Secondly is CA. Now getting CA is extremely difficult. We need to understand that banks pay 0% interest on CA account. So the private CA space is extremely competitive and private banks have to offer lucrative deals to get CA. Yes bank being dominant in digital transaction space is one of the USP they have when they have to attract private CA.

Now apart from private CA there is government CA. This space is huge. One government CA has the capability to bring 10k to 30k cr. I was speaking to the regional wholesale manager of yes bank and I got to know that government CA have their own set of rules before opening a current account with a private bank. He mentioned one of them is bank being profitable for minimum 2yrs. Now different entitles have different rules. For HDFC bank government CASA is a walk in. Why I am mentioning all this is because once the books gets clean lot of window dressing is going to happen to their financial statement. So the improvement of all these ratios and assuming yes bank being profitable for 2 years places them in a good position in market to get CURRENT ACCOUNT.

Just think in this way before investing in a company you put a basic screener on 6000 companies and there after you go in detail on the 50 companies shortlisted. So after 2023 yesbank will at least qualify most of the basic screener.

Hi guys long time since I posted here.

@Sudhakar_Subramanian

Most of the lock in shares are with instructions which in my view will not be selling immediately after locking period. Individual investors above 2lakh and below 2lakh invested amount have 130cr shares in lock in. Even if 50% of them sell that day 65cr shares. If I quantify this the fall is not going to more than 1 or 1.5rs. On 17/09/2022 yesbank fell by 1rs with 58cr as volume and by lock if the share price is 21-22 then a fall of 1 or 2rs does not make any difference. The fall can be even larger but since most of the people are aware of lock in and there is no fundamental change in the company because of this activity the price will bounce back even stronger.

Was just reading the thread since 2012. The kind of bullishness at the beginning, then despair and now hope. Now that all the clouds have cleared and management focusing on the banking business, avoiding any extravagant risks, or making extraordinary promises is really commendable. The credit cycle in India will play a major role in the success or bust of this stock. Have invested a very little chunk of my money in this stock. Tracking it closely.

The member banks, except SBI I guess, of the banking consortium sold the sellable % of stake in yesbank when the stock price rallied after the rock bottom. They can do it again once the lock in period ends.

There is a slight liquidity crunch in the whole banking industry. Nothing to do with Yes Bank alone. I have never seen banks vying for FDs this much in the past 7 years. Its just that YB is giving a higher interest on SB to woo more depositors. However, if you are an equity investor and tracking the CASA ratio the figure put up by the company may be quite misleading due to the higher interest cost on saving account balances.

I was jist going to write on this

There is a big liquidity crunch. If you see most of the bank raises interest rates in last 10 to 15 days so that they can have a good q2 but this has costed them q3 and q4.

Last quater most of the banks lost deposits and i thought that was temporary but now it is a serious issue.

I was confidentn of yesbank giving 2200cr kind of profit but i doubt now. They were just standing on their legs their nim was very small on top of that they are forced to raise depsits. This quater might go good but next 2 quater is a serious issue to most of the banks.

It is quide ironicall that the credit growth is at all time high but there is no liquidity. You will also see most of the banks raising money now despite cost of debt is high. SBI just raised 4000cr at 7.57%. Tomorrow another 50bps hike comming. RBI needs to interven and do something about this. It is gettig serious.

I was not expecting them to rasie deposits rate that much. I am glad that they raised money otherwise this year would have been very difficult for them. I wont be surprised if they loose deposits this quater as well

Read this article it is very good

Below are main points of article. First point is scariest. Interbank rates are more than repo rate.

Liquidity in the system turned from surplus to deficit after 40 months

■ Inter-bank call money rate at 5.64 per cent, greater than policy repo rate at 5.40 per cent

■ Advanced tax collections, tepid government spending main reason for the system turning into deficit

■ Credit growth in the system is greater than deposit growth, another reason for the shortfall

■ Banks may now raise deposit rates to bring more liquidity in the system

I guess RBI did intervene with around 16000cr infusion if I am not wrong. But why is this liquidity issue so concerning? I don’t have enough knowledge to analyse the scenario, so if you could throw some light on the whole situation, it would be really helpful.

There are 2 major ratios one is CRR and second is SLR. To explain both of them in simple term banks have to maintain certain percentage of cash and liquid assets with rbi. Rbi recetly increased these two ratiois which means banks have to maintain more money with rbi.

Since inflation is hight cost of goods is high and rbi increaseing repo rates is sucking liquidity out. In simple terms people withdrawing money from their accounts. Banks dont have money to lend and if they dont lend they dont earn. Just read the above article it beautifully explains the problem.

Why the first point is extremely concerning is RBI is lending money at 5.4% but inter bank lending is happening at 5.64% that means banks desperately want money.

Explaing in short banks dont have money to lend and every body is raising deposit rates craizally that will put pressure on nim and resulting pressure on profits.

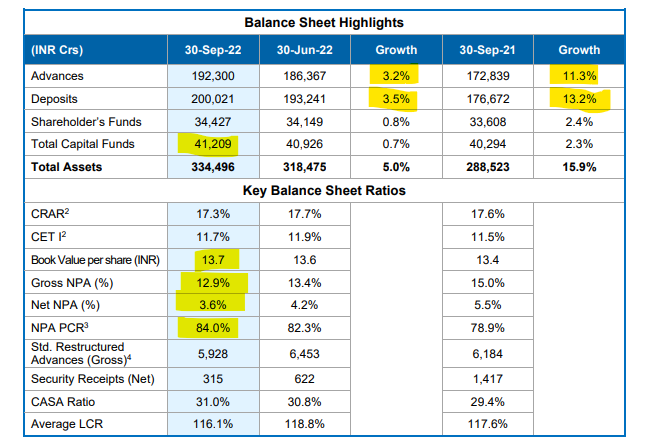

Numbers are very good was not expecting this from them. QoQ and YoY both of them are fantastic. This quarter for all bans will be good but next 2 quarter are in trouble.

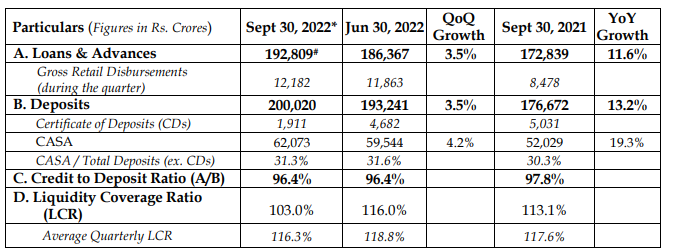

You can see their LCR coming down which is a concern. CASA is growing hand in hand with deposits. Actually yes bank has lot of attractive and creative products in FD so they get lot of money there that is one of the reason for CASA ratio being flat despite growth.

Went through this article yesterday and I feel Prashanth kumar is extremely underrated. He has done a phenomenal job and is continuing to do so.

I saw the recent interview of IDFC bank CEO and he says that the market is so huge and under catered that banks will not be competition with each other. The share of the PIE is getting bigger.

I also remember NIRMALA SITARAMAN saying that we will need 5 SBI to cater this growth.

My overall point and basic idea of investing here is that in next 2yrs this bank is going to be above 4 lakh cr and there is no way a profitable private bank with such huge balance sheet and heavy tail wind form the industry can trade at a Mcap of 40000 cr.

Thankyou

Finally, the much-awaited revision in rating.

https://www.careratings.com/upload/CompanyFiles/PR/12102022061605_Yes_Bank_Limited.pdf

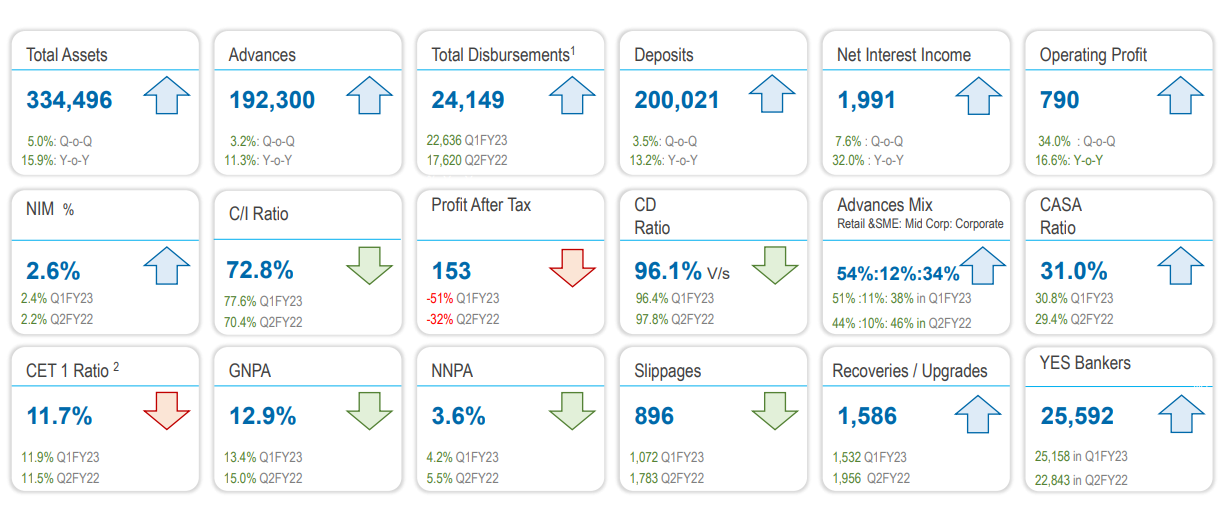

Results are out - https://www.bseindia.com/xml-data/corpfiling/AttachLive/5f2cae96-8150-4f2f-a6f2-1db7a8fdcea4.pdf

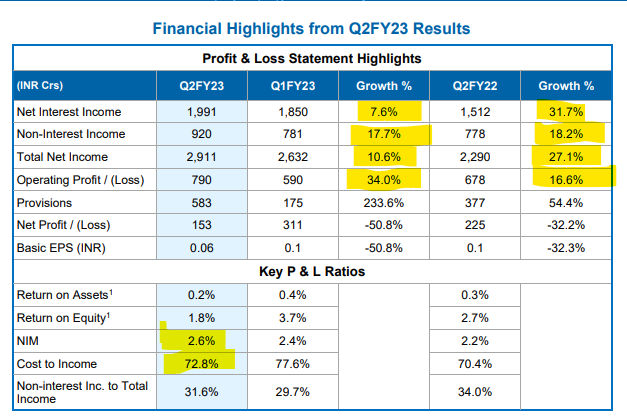

PAT is down both YOY and QOQ, need to wait for concall to understand the jump in provisions from 172cr to 582cr.

Much awaited results out.

I have been tracking this bank from last 8 quarters and I can say this is one of the best quarter I have ever witnessed as far as the business is concerned.

Yes bank is still in recovery phase and has not yet entered the growth phase. They enter growth phase after asset transfer and capital raising.

Profitability is low because of high provision and next quarter also it is likely to be high because they want to transfer asset with maximum provision. I don’t care much about provision because business is doing fantastic and also their provision coverage is at 84% so if recovery happens in future profitability is automatically going to be high because of reversal.

This year profitability will not meat management estimates but on all other parameter they are on track. The more provision they do now the more reversal comes in future

Slippage is lower QoQ and YoY and 61 to 91 days bucket is lowered by 3000cr

Business performance is extremally good but still below industry majorly because of they not completely focusing on growth.

Hi,

Did anyone download the audio recording for the earnings call. The links the bank has provided do not work.

Could anyone post that here please

Hi guys some more information on the results are as follows

1.Currently their MIX is 54:12:34(retail, SME and corporate). I have always been stressing that banks more towards retail will outperform banks more towards corporate.

Their Retail banking fees is at 586cr highest till date which is up 20% QoQ and 32% YoY. Their Credit card book has grown by 66% YoY and the spends have grown by 70% YOY. Their revenue per customer has grown by 54% YOY though cross selling.

They have added close to 500 employee this quarter but their Q0Q expense on salary is flat. Their IT related expense is up by 37% Q0Q and 68% YoY which single headedly takes their entire expense up by 4% Q0Q and 32%YOY.

This growth in expense is in line with 32% growth in NET INTREST INCOME. Now IT expense acts as an operating leverage in future where you just have to maintain the IT infrastructure and the benefit you get from it is extremely high.

Their operational efficiency is extremely high when I take a flat IT expense YoY and QOQ.

How does IT benefit?

Their Current account has grown by 14% QoQ and 21% YoY. This growth has not been on the back of 1 or 2 large accounts but has been on the back of sustainable growth. Their CASA is flat because of degrowth in savings account which is predominantly because of late deposit rate hike. Actually the ability of a bank to get CASA should always be seen by the ability to get current account as there you cannot offer any interest on deposit. They have opened 3.3 lakh CA account this quarter.

The spread between the advances has been shrinking in the recent times because of extremely aggressive rate hike. The bank is confident to take this spread back to the PRE WAR levels which is likely to improve their NIM further.

Their current yield on advances without the Gross NPA is at 9.5% compared to 8.5% with gross NPA. This shows how good their active loan book is and also shows the stress these legacy asset are putting on the books.

They have grown their deposits at 13% YOY where as their cost of deposits are down 10bps YoY. Despite liquidity issue in the next half of the year bank is confident to grow deposits with improving NIM.

Their borrowing has increased by 20% YoY now here comes the power of credit rating. In a liquidity crunch scenario this shows that they have access to liquidity. This quarter they have raised 3500cr kind of money from borrowing.

Their active advance have a PPOP(PRE PROVISION OPERATING PROFIT) to asset of 1.15% and this cost of provision excluding legacy provision is 15bps to 20bps. This means their current ROA on their active book is at 1%.

Their current credit cost is 50bps to 60bps and bank expects this kind of cost to continue in future. Their current ROA is at 0.4% on overall book but 1% on active book this clearly shows the stress these legacy advances put on the book and how good the bank is doing.

Close to 60% of their restructure book is out of moratorium now which is a big risk as of now. They will now need adequate provisioning for this part as per RBI guidelines. This quarter there was 350cr of slippage from this book and 170cr in previous quarter. I will have to further did deeper into this book and see the future possibility of slippage from here as now it is no longer under moratorium which was protecting it form provisioning.

Bank is in no hurry to match the industry growth in advances. They are building a good quality advance which can clearly be seen from their slippages which is extremely low and their provisioning requirement for these slippages which is close to 10% only. 95% of their provisioning is for legacy loan which shows what good quality loan book the bank is building. Their RWA is currently at 71% down from 79% a year ago which against shows the improving quality. They expect a 15% YoY growth in advances.

They expect at GNPA of 2% and a NET NPA of 1% after asset transfer. The bank is confident of achieving a 0.85% of PPOP to asset but says any delay in expected recovery may lower their FY23 ROA. I think they are referring to reliance infra here. Reliance infra has recently received close to 2000cr kind of money from Delhi metro and they are further going to receive money up to 5000cr. Reliance infra has already won this case against Delhi metro in supreme court. They have recently also filed a case against adani group. They roughly own yesbank 12 thousand cr.

Despite a NET profit of 150cr their equity is up by roughly 300cr this is because of 55cr tax and 90cr of recovery from a particular book which they are not allowed to route through profit.

Their average daily CA balance is up by 37% YOY and SA balance up by 30% YoY. This shows the quality of CASA and also helps bank manage their liquidity in such scenario.

QUALATATIVE ASPECT AND DIGITAL ASPECT OF BANK

They are turning out to be extremely innovative and aggressively doing more and more tie ups with fin tech and introducing new products in the market. All of this have increased in last 5 months. Since the bank has finalised capital raise and asset transfer now the management is able to focus more towards growth which can clearly be seen from their innovative products.

If I assume a flattish IT spend and provision only for their active book this quarter they would have shown a NET profit of 650cr to 700cr.I feel the bank is not concerned about profit and is building a sustainable business as of now. They are bound to give profits in future because of they showing such good performance in business and on top of this heavy tailwind from the industry.

Disclaimer: I do a lot of trading in this stock because it has a low beta and have an average price 13.64. Considering all the profits booked it comes out to be 12. Currently it is 60% of my portfolio and I expect a CAGR of 20% for the next 3 to 5yrs in the worst case scenario. I might be biased

Thank you ![]()

Hi @manhar,

Thanks for doing the hardwork for us by going through the earnings data.

Coming to the futuristic lookout in the price movement, I have some queries:-

Not considering any new positives apart from the ARC offload, the rest appears to be same struggle/growth story across the banking sector. Although, Yesbank is well positioned with some niche offerings and highest level of efficiency.

TIA

Few years back, every retail investor was upbeat on Yes Bank. I see the same exuberance… and justification of every bad result is similar to how low GNPA and NNPA numbers were justified 4 years back!!

no institutional investors have come in… its a party of retail investors and hedge funds… deadly combination…

depositors lured by higher rates and backing of SBI… quite contradictory… similar to ponzi schemes…

lets see how the story unfolds…

@Rax

Hi thankyou for your kind words.

So total 630cr share are going to be issued( it might not be precise as I am not referring the bank report). We will have immediate dilution of 330cr by next quarter and balance by next year. Both instructional investor will get 10% each.

The probability of SBI selling in FY23 is extremely low and as far as others investors are concerned I have given a post above where I have tried to quantify the fall.

I was expecting 2300cr this year so I turned out to be horribly wrong in my estimates. This year in a good case scenario they might hit 1500cr only. My estimates had a big assumption of ARC sale by June 2022 that is one of the major reason for such big deviation.

Seeing their current performance and industry tail wind I am extremely confident of they hitting 1.5% ROA by FY25 currently they are generating 1% on their active book and an asset size of 4lakh cr ( this means a 8% growth for the next 2.5yrs which I again feel is conservative). So I see this stock trading between 35 to 50.

If I had to give you advice I would say since your average price is 27 your probability of making money out of this is low. You should be selling a good amount of your holding at 20 or 18 and invest in a good company.

@Aarti maam

I think money can be made out of any stock. When yes bank was at 18 I was at 40% profit in 1 year on 80% of my portfolio(currently it is 60%). I am 90% confident that even in the worst case scenario I will make 20% CAGR form my avg price for next 3yrs.

If you could share why do you see yesbank not performing I would be glad. Just by assuming that it destroyed investor wealth earlier and will do the same in future is not the right way according to me.

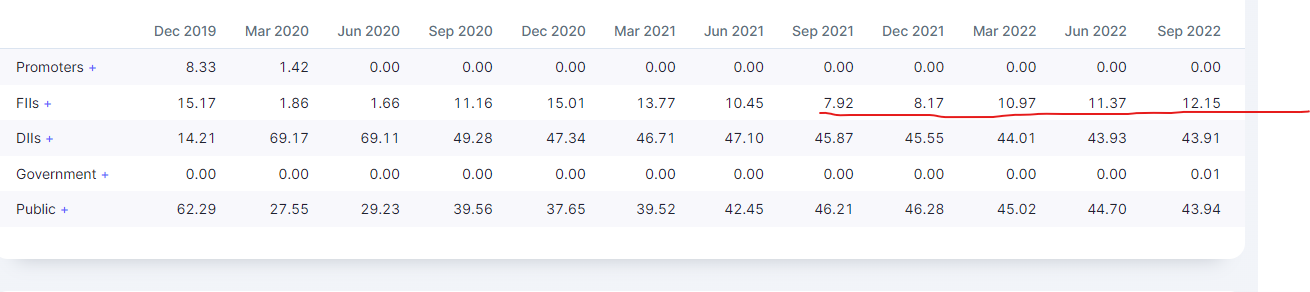

We can see 2 world class instructions buying stake here and FII stake increasing from last 5 quarter so you will have to elaborate your point on institution investor.

Thankyou