Did Yes Bank disclose name of the investor who is ready to invest $1.2B, which was the main reason for stock spiking up yesterday?

1 Like

They only hint its backed by US Fin. Instt.

In my opinion the announcement of Equity investor was mainly to pacify the depositors rather than Equity holders. The panic and hurry in which the management had announced yesterday was really very surprising and more particularly without making any specific disclosure in todays Concall. They could have anounced along with today’s result also.

I think there may be some panic withdrawal of deposits.

Logic : Had i been a depositor I would not have kept money in YES Bank savings account even at 10% interest rate. Why should i have a loyalty with a Bank for keeping my deposits when there are better Public Sector and Private Bank options.

Disclosure : Not invested; Tracking for learning

Investor is asking for 30% stake which anyways is not in line with RBU guidelines. So looks like a sham. Positive news with caveats are not reliable. We have seen many such in DHFL case.

1 Like

Stronger banks with better balance sheets are reporting losses upping the provisions where as RBL, IndusInd and Yes want to post profits. Really? Showing profits with PCR at 43%, I knew there is a sentiment side to it. Still, doesn’t make sense. The capital raised ($1bn if it happens) will go for new NPA and increased BB and below. Not sure what has changed since last quarter. From look of it, all metrics are down. Did any one hear mgmt commentary in concall Q&A and their plan forward

1 Like

They had to announce it and inform exchanges are it’s a price sensitive information

SEBI guidelines

3 Likes

All term sheets have confidentiality clauses. You need permission to share the investors name. Nothing is signed so I highly doubt they will officially name any investor they are in discussions with. Without speculating on the timing or credibility of their announcement yesterday, my own experience as a PE investor has been that the best way to convince your board to approve an investment is to show them a competing term sheet… there is a very powerful FOMO and herding effect amongst institutional investors. It’s really perverse but the thinking goes like “if X has done all the analysis and wants to invest then I don’t really need to apply my brains and this covers my *** if it’s a dud”. Perhaps this is just to raise the stakes for other suitors or people still waiting on the sidelines.

4 Likes

NPA’s increased, last qtr it was one time MTM losses due to exposure to DHFL bonds, this qtr it’s DTA. I am learning new one time losses that banks can report on their investments without catering much to NPA’s as PCR has not moved up by an inch(remains constant at 43.1% since last 3 qtrs). Next biggest NPA shocker could come from AA group companies-Rpower and Rinfra. Yes’s dream of increasing market share in retail will not be easy after the PMC’s faisco that happened recently, they might continue to lose deposit share. RG’s dream of achieving 1% ROA from -0.2% ROA reported in Q2 could be a distant dream for atleast few qtr’s(6,8,12…?) by then Yes seems a potential acquisition candidate by some big fish and pure short candidate for trading.

Only +ve I see in the Q2 presentation is the strengthening of digital leadership position, not sure how easy or difficult would be for other smaller banks to achieve that.

Disc: Invested.

3 Likes

Hi

I would consider this with a pinch of salt. I have started believing most of the tech partnership a bank is doing is a commodity business - a side act which any bank can take by cutting the fee by a few bps. Are these true needle movers? I doubt so when the core business of lending is questioned and borrowing is actually falling.

Leaving digital aside.

The problem in this case is finding what the true book value is. And I think if one can do that with some confidence he would already be in a trade be it long or short.

I was skimming through old annual reports just to see how the story was being written then. Would recommend doing that. I remember the whole focus earlier was to be ‘the world’s best quality bank in India by 2020’ and in today’s investor deck I see ‘to be India’s finest largest quality bank by 2025’. A cut in ambitions but rightly so.

On the brighter side I see the old management more or less gone (which is very important I feel). A good shift from corporate to retail business. Without DTA it would have posted profit. On a sequential basis GNPA and NNPA rose and the management claims that ‘recognition cycle is nearing an end’.

Retail is trying to catch the bottom because at the back of their minds it is the hope that bank will turn around or get acquired.

I hope Mr Gill can steer this ship.

Rgds

4 Likes

Key takeaways from the Management Call just concluded

Credit cost to increase to 250 from the erstwhile 125

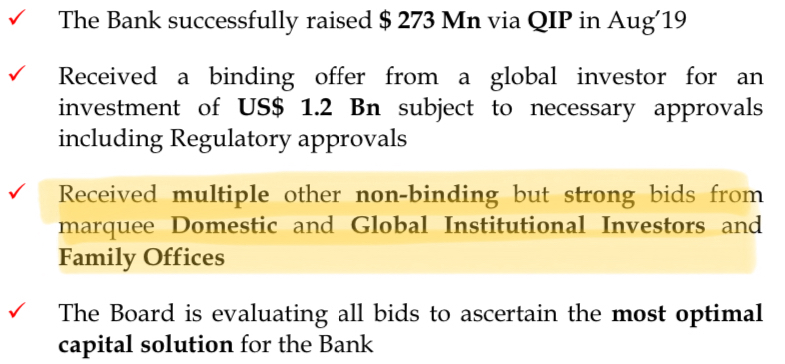

Binding offer of USD 1.2bn comes with an expiry date of 30-11-19

3% of total exposure to telecom with no delinquency

Fresh Slippages of 5,200 cr. Making total NPA to 9757 cr. As on 30th September - PCR of 43%

Management expects 25-35% of BBB and below book to go Bad

A brief of my key observations from the Q2 Investor Call

3 Likes

Absolutely, any fund manager with his skin in the game would have given you description of the game going on here. However, there was a mini bubble in the RK fan base who simply refused to trust any data or emerging cockroach in the kitchen theory. As an investor we all need to figure out if the perceived image of any business leader is “managed” or ‘deserved’. This is a difficult task to nail accurately but not impossible as such. Now that the need to ‘manage’ the image is over, we would see publishing of many ‘insights’ into the working of this bank and how the current management is doing great. I firmly believed that it made a fundamental bottom at 30s but I am still not comfortable with the current management setup. I need to dig deeper to understand what drives Mr. Gill because it all depends on him now.

Disc: No holding and not in watchlist

2 Likes

Yes Bank Q2FY20 Earnings Call Highlights:

Participants:

- Macquarie

- Bullero Capital

- Deutsche Bank

- Baroda Mutual Fund

- Franklin Templeton

- Birla Mutual Fund

Business Overview:

- NII at Rs 2,186 crore; NII impacted due to Rs 228 crore reversal and fresh slippages during the quarter

- NIM at 2.7%; though the reported NIM is 2.7% core NIM is above 3%

- Non-interest income at Rs 946 crore; bank witnessed 10% sequential growth in retail banking fees

- Treasury income at Rs 386 crore; last quarter bank had Rs 450 crore of non-core treasury gain while this quarter it was Rs 225 crore

- PPOP at Rs 1,458 crore; provisions at Rs 1,336 crore (most of it for credit quality)

- PBT at Rs 122 crores; Net Loss at Rs 600 crore

- One-time DTA adjustment of Rs 709 crore hit the bottom line during the quarter

- Yes Bank has 41% market share in UPI transaction

- Yes Bank’s assets based decline 7% on sequential basis to Rs 3.46 lakh crore; 12% contraction in investment book and 5% shrinkage in advances

- Operating expenses at Rs 1,711 crore

- CASA ratio improved to 30.8% from 30.2% QoQ

- CASA+Retail TDs at 60.3% vs 58.2% QoQ

- GNPA Rs 17,134 crore (7.4%); NNPA at Rs 9,757 crore (4.35%); PCR at 43.1%

ConCall highlights:

- Corporate banking fees will bounce bank post capital infusion into the bank

- Transaction banking fees continues to be robust; marginal sequential dip in this quarter on account of shrinkage of balance sheet

- Credit cost for the quarter at 69 bps and for H1FY20 at 100 bps

- Retail business continues to grow at healthy pace, grew 30% YoY. Share of retail advances increased to 20% from 14% last year

- CET1 improved to 8.7% from 8% on sequential basis on account of QIP issue and capital optimization

- Slippages during the quarter at Rs 5,945 crore; recovery and upgrades Rs 835 crore; ne slippages at Rs 5100 crore

- Overall increase in BB and below rated books has been around Rs 2,000 crore; which stand at 10.1%

- 60% of net slippages came from BB and below book; however there has been around Rs 2,000 crore from above BB rated book

- Yes Bank is reducing its exposure to NBFC, Housing Finance Company and real estate. Overall exposure reduced by Rs 1,750 crore in Q2FY20 and further reduction of Rs 1,500 crore happened post September quarter

- Exposure to telecom sector is 3%; nil delinquency as of now

- Management believe that increment credit cost will get reversed once the resolution start to kick in

- Received a binding offer from a global investor for an investment of USD1.2 billion (single investor and direct equity). Timeline for this offer is till 30th November

- As the voting right will be kept below 15% it will not trigger any open offer if any buyer acquire more that 25% stake in the bank

- Management feel that that around 25% of BB and below book can go bad

- Bank has been able to make material amount of recovery post September quarter from a large account which slipped from non BB book

- Incremental cost of fund around is around 6.5-6.7%

Guidance:

Bank has increased credit cost guidance to 225-250 from 125 bps given earlier

9 Likes

From the concall, looks like total exposure to DHFL is Rs 6000 crores (instead of Rs 4000 crores widely circulated) out of which 25% i.e Rs 1500 crores is provisioned as MTM in last quarter. The question was last but 1 in concall. Is my understanding correct?

1 Like

How is this a partnership? It sounds like a vendor-customer thing.

1 Like

I would still defend Rana, but he was getting too big for his shoes.

IBC has been successfully challenged in Supreme court and now referral to NCLT is left to the banks instead of by pure diktat/rules.

Flogging a horse does not necessarily make it perform. You do not kill a goose just because it missed laying an egg. Fascist tendencies are hard to control though. ![]()

RK made Yes bank, and it should grow even from here.

He petulantly challenged NPA recognition diktats, knowing fully well that RBI review would rap him on the knuckles.

I see nothing wrong in fee based lending. Show me a successful legal challenge to this and I will reimburse your costs. ![]()

2 Likes

Based on https://azure.microsoft.com/en-in/services/cognitive-services/language-understanding-intelligent-service/ looks like they have only 2 Customers (atleast ready to acknowledge they use it). Yes Bank will be added to it. When they use partnered it might be microsoft enhancing their product to suite Yes Bank needs or it may be co-development and testing etc. Also, Yes Bank might be moving to Azure to improve their systems performance. Just a hunch on why they might be using Azure Service.

It’s a pure vendor customer thing has nothing to do with investment.

I know since we are competing with Microsoft for one of the deal and I see nothing that indicates even sign of it