We should get to know about the name etc for at least this 1.2 billion term sheet by next week once the committee approves it which they will do ( why anyone would not want to do it in current situation ).

Lets hope for the best .

Invested - at 200 , 33 , 41 and 55.

Waiting to add more once get clarity on of Bank getting additional capital / how much etc.

DBS, Yesbank deny acquisition reports.

https://www.cnbctv18.com/finance/dbs-yes-bank-deny-acquisition-reports-4630611.htm

From standard PTI reporting:

" The bank, on Thursday, had disclosed that it is in touch with a family office in the US to raise $1.2 billion to shore up its capital. "

" Gill, who replaced promoter-chief executive Rana Kapoor, said the bank has received a binding bid from the North America-based family office that has never invested in India, and has a net worth of multi-billion. "

" Apart from that, the bank is in discussions to raise USD 1.6 billion from a clutch of six global private equity funds and two domestic mutual funds, he told reporters late this evening. "

" It is also in touch with two groups of domestic investors to raise USD 300 million, he said, adding that this includes two family offices and two financial investors. "

From Livemint reporting:

" Speaking to a small group of reporters late on Friday evening, Gill said that the bank has non-binding offers from two domestic mutual funds, six global private equity firms, two Indian financial investors and two Indian family offices. While the two domestic MFs and global PE firms have made an offer of $1.5 billion, the offer from four Indian investors is about $350 million. "

" “The new investor would own around 30-33% of Yes Bank for $1.2 billion," said Gill, adding that according to the term sheet, the offer price will be under Securities and Exchange Board of India’s (SEBI) two-week formula or any mutually-agreed price. The investor has also sought one board seat and will be a “pure financial investor” and has not sought promoter status. "

" The North American family office, Gill said, has invested in financial services companies as well as energy assets in other parts of the world but has not invested in India. It is a multi-billion entity. That apart, its term sheet also includes a letter from a “large US-based financial institution" saying that the investor has the ability to take the deal forward. "

Let the (more accurate) speculation games begin.

Reliance is indeed a good one, but just for $ ~100 million or so?

I believe it will be challenging for someone who has never invested in India before, to invest in Yes Bank, especially since it is a regulated entity. Even if it clears the board approval, RBI will take it’s own time to assess and approve. For some one who is coming as a non-promoter, might as well invest in Kotak or HDFCB. So, one should not be too enthused by the binding offer.

As per https://www.rbi.org.in/Scripts/Timlines.aspx time required is 90 days. So not sure if approval will come by Nov 30 which should have being given in filing with exchanges.

90 days can be a maximum time that RBI may take , I think since RBI representative is already on Yes bank board , and RBI must be better aware about the situation , it can also happen earlier else yes bank would not have proposed given timelines in Term sheet .

The language is used by bank in its regulatory filling and any objections can be sent to company secretary whose details can be gathered from bank’s website.

The stock movement today, opening at a price of ~Rs.60 (10% lower gap opening over friday’s closing price of ~Rs.66), the racing towards the days high of ~Rs.71 (up 20% from the opening price) and now the price settling in the Rs.65-67 range for the last 2 hours shows the confused state of market participants, post the Q2FY20 results.

A lot of messages and analysis have been circulated over the weekend and ownership bias was very evident in most of these messages (in my opinion).

Those who had long positions were of the opinion that the result was very strong and that the stock should open gap up today. The main reasons cited for that view was: (1) Capital infusion issue sorting out with strong interest reflected by institutional players, which will get finalised over the next 30 days or so (2) the results are perceived to be better, if one excludes the DTA impact (3) results being “much better-than-expected” as expected losses were in the range of Rs.1200-1900 crs!!!

While those who had short positions/ had sold off / were negative in their view earlier, saw a continuation of the trend of the bank reporting disappointing numbers and were expecting the stock to open gap down today. And well, this bunch had a lot of reasons to support their views (1) A ~40% yoy decline in operating profits and ~40% yoy growth in provisions (2) high slippages resulting in gross NPLs, now moving to 7% of loans (3) The ‘below investment grade’ book, despite high slippages, is still at ~10% of exposure (4) 10% yoy decline in NII (5) ~35% yoy decline in non-interest income (6) a decline in current, savings, retail and corporate term deposits on a sequential basis (7) doubts on growth, excess capital, path of RoE improvement given the changes in lending (8) doubts on the progress of building the bank’s liability franchise that is currently inferior to its peers and profitability. Etc Etc

Irrespective of where the stock moves in the near term, i personally believe that theres a long way for the stock to regain its past glory. Its only when the bank consistently demonstrates (a) no negative surprises on the asset quality front (b) growth in advances, without compromising too much on RoEs or margins © that the current management is walking its talk, will serious investors start taking a relook at this. Consistency, in its performance, is what is the key. Till such time, the stock could display volatility, giving enough chances to traders to benefit from. While newsflows such as capital raising would help keep the momentum alive, any murmurs of stress from non-discussed names could exert pressure on the stock going forward.

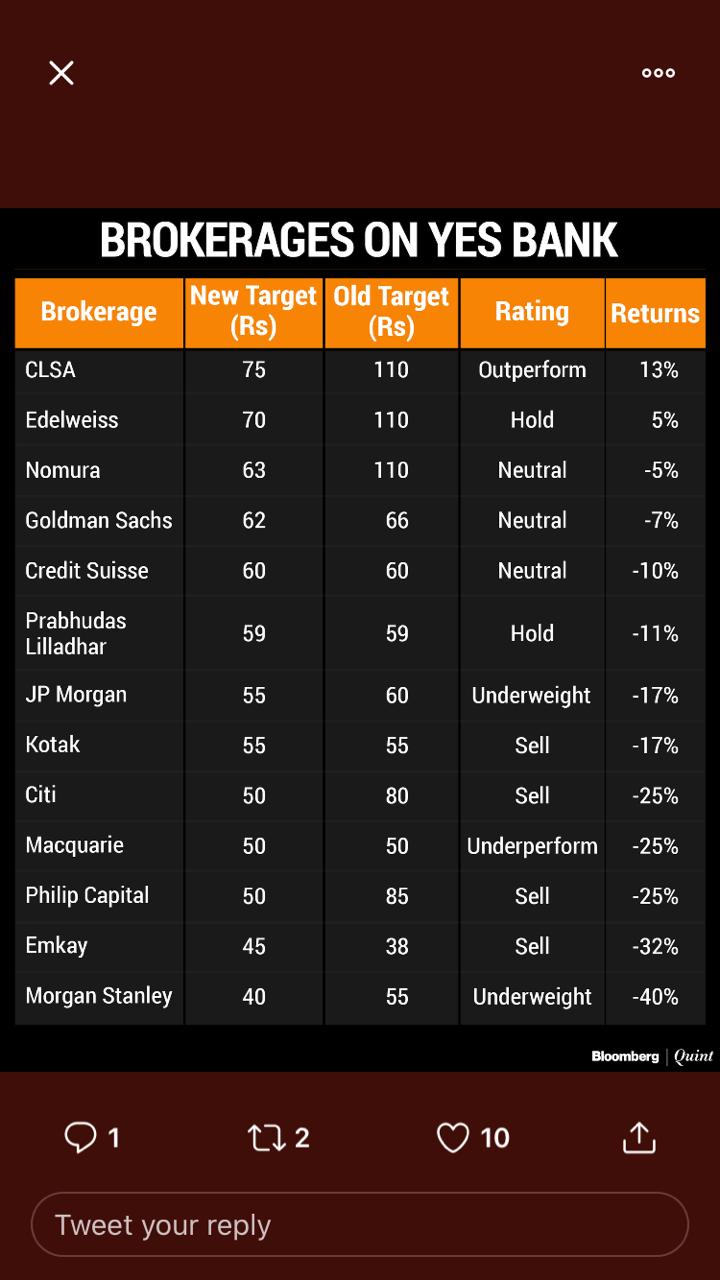

Of the 13 broking firms whose revised price targets on Yes Bank have been compiled, only 2 have their price targets above the current market price (Rs.66). That too, the price target, at best, implies a mere 13% gain from todays price ![]()

Not that one needs to take all these targets seriously (going by their historical targets and final outcomes), but this is just to keep everyone updated on what the ‘informed investors’ are opining.

Article feels really sorry for the “shorters”, complaining about bank talking too much, especially on expiry day (31/Oct), poor bears were hit badly.

Can we trust a sold out media circus?

I don’t see mention of ADAG exposure of Rs 13K other than reliance capital rating change. Did I miss anything?

Disc:Invested

Not sure why so much hype and discussion happening with what one investor has chosen to act upon? This is the kind of noise that deflects us from the core issues we should be focussed on, and more often than not tend to colour our thoughts.

Any investor for that matter has his own risk appetite and portfolio allocations, both of which are not known to the public at large and are open to interpretations. Then they have a trading book and an investment book and in which of these books they have made the purchase in, is also not clear. And even if it were clear, is our risk appetite and goals similar to those of the investors, who we discuss so very often? may be not.

Besides, have you ever seen any investor make any disclosure (block deal etc) while selling? i cant recollect. Announcements are made only during entries, isn’t it? Is it very difficult to assume why this case? ![]() So then why even bother discussing such things and wasting our time?

So then why even bother discussing such things and wasting our time?

Do your due diligence on the stock, stick to fundamentals and your read and then act upon it. Coat tailing is worthless.

ADAG Group loans R-power and R-Infra should be current and have not turned into NPA yet.

By that same reasoning, one leveraged investor forced to sell should not have had any impact on others but it does.

How? Bank books are not open to anyone so a retail investor should never be investing in any bank or financial institution.

Neither of any investors’ actions changes the fundamentals of any stock…their buying only makes it more pricier than where the stock was trading at, before their buying action…and selling (even if forced leveraged selling) makes it cheaper than where it was trading at before the leveraged sale. Isn’t it? and that wasn’t the point i was making. When you do NOT know why an investor has bought or what is his investible time horizon or what is his risk appetite or what the portfolio allocation is towards the stock he’s bought into, blindly coat tailing could prove to be dangerous. That’s all i was trying to imply.

That ways, no company opens its books to any investor, why only retail investor? Would you know if the clients of the software company has actually given a contract, if at all? Would you know the actual terms of an order awarded to an infrastructure company? Would you know the actual sales of a particular molecule, sold in a particular geography, by a pharma company? Chances are little that anyone would know specifically.

Doing due diligence implies keeping oneself updated with everything that a company has divulged in public, reading upon the industry and trying to read and dig into its clients publicly available information etc. I can go on and on. But i’m sure you have got the drift. Retail investors can be equally smart as an institutional investor (if not more), if they intend doing thorough research. And its been proved so in many cases where educated retail investors have held on to several multibaggers as well. No?

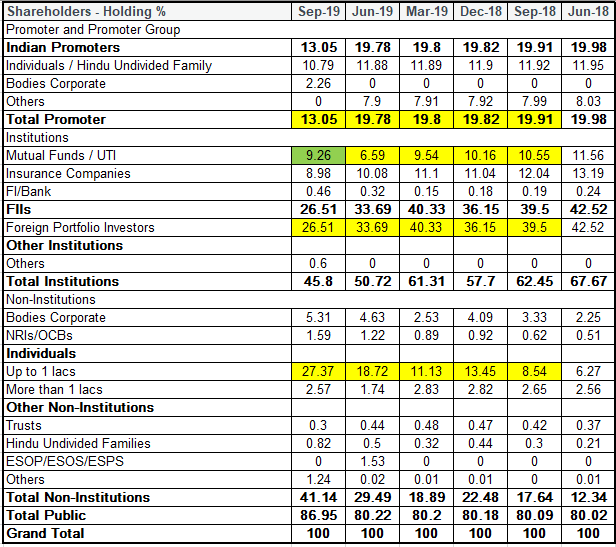

The shareholding pattern in Yes Bank shows interesting pattern. We have seen multiple examples in recent history, where retail investors get themselves dumped with stocks getting hammered down. As the price goes southward, retail investors feel its cheap and get attracted to them.

Below data shows that Retails investors have accumulated more than 20% of shares (more than one-fifth) in last 5 quarters. The supply comes from Promoters (7%) & remaining from FIIs . It makes more interesting when we see that Mutual Fund houses, who were sellers for 4 quarters till Jun’19 have turned buyers in recent quarter.

The million dollar question for VP community is that are retailers turning smart for the first time in history where they are able to smell a turnaround in YES Bank, which others (excluding MF houses to some extent) have failed to …

Interesting data point. Thanks for compiling and sharing. ![]()

That’s precisely what i have trying to contest. Insiders (promoters) and informed investors (Institutional players) are always assumed to know either everything or most of the developments within the company. Isnt it? Yet do they always benefit with the information arbitrage? In many cases, NO. In some cases, YES.

Lets analyse what it could have been in this case. Taking a look at the table, its evident that till June end reporting, the stakes of promoters was more or less intact and FIIs seem to have pared their holdings by ~6% over the last 3 quarters. Lets remember the stock price of Yes Bank as on June end was closer to Rs.150 (halved from the top, when positions were intact).

It was only in the September quarter and later that huge sales were reported by both these segment of investors. The stock made a 52 week low in Sep end! (Rs.30 types). Imagine.

So if these “informed” investors were as smart, why didn’t anyone sell at the top, or thereabouts? Why only after the stock has given way and take a hit on the exit price? At what price the management has sold of ![]() , is public data.

, is public data.

So i come from the school of thought that any trades executed by any informed investor NEED not play out right everytime.

FII’s have reduced, couple of MF’s have participated in the QIP at 83 odd levels, and MF’s shareholding shows an increase. Promoter holding is down due to voluntary and forced selling of pledged shared. Retail shareholders, primarily those upto 1 Lacs and predominantly, the uninformed have bought the most. Above 1 lacs segment of Individuals was at 2.65% in Sep 2018 and is at 2.57% in Sep 2019. Whether individual investors are turning smart or have averaged down from higher levels, or have caught a falling knife, would be known in the times to come ![]()