ADAG has given Delhi electricity as collateral, will not dare to default also AA has sufficient assets to clear off debts.

2 Likes

Looks like DHFL payment will not be coming immediately. As per this article below (needs subscription) the resolution proposed is the repayment will be for 15 years and interest being written off. So, another Rs 2500 crore possible NPA where everyone is expecting full recovery. I am assuming Rs1200 MTM reported in quarter 1 is for DHFL only. May be reason for QIP at such a low price and fall of stockprice on friday.

Disc:Invested

1 Like

Thanks for sharing. I am a little surprised at the market reaction to QIP. Before the QIP, reports were saying it would be a surprise if YB is able to raise any money at all. Now they are saying market is still not happy with the huge dilution. Seems like there is nothing YB can do at the moment to please the markets.

5 Likes

In my view QIP going through is a positive. This gives a definitive hope that slow and steadily the bank has decent chances of coming back to normal operations. Yes bank is the not so liked guy for the current market and for obvious reasons. But the current market mood will be mostly punishing , partly also cause lot of investors want to get rid of such beaten down names which have not been able to deliver as expected. But this is what we have to understand that a change of sentiment coupled with return to normalcy can atleast offer steady 10 to 15 % . One hindrance for sure will the noise which has accompanied the stock and second being the associative bias of it correcting from 400 levels to sub 100 levels in such a quick time. Let’s try and avoid such investing pitfalls.

Regards

Divyansh

Disc: not invested

Waiting for the initial green shoots to appear

4 Likes

3 Likes

5 Likes

What the bank will achieve by acquiring significant share in companies which are at edge of bankruptcy or under tremendous struggle.

In case if article is not opening, The article is about CG power struggle but at end it mentioned that Yes acquired 12.79% stake in CG power as a invoke of pledged shares.

3 Likes

Believe some can of worms will open up in every Industries as well. Cox and Kings is another such case.

It doesn’t look like a prudent strategy. They would have been better of selling in open market and encasing whatever possible.

May be yes bank has different strategy and know something that others dont.

But it looks like a bad decision as of now. Hope they dont end up acquiring junk companies along with the other liabilities on the books…

2 Likes

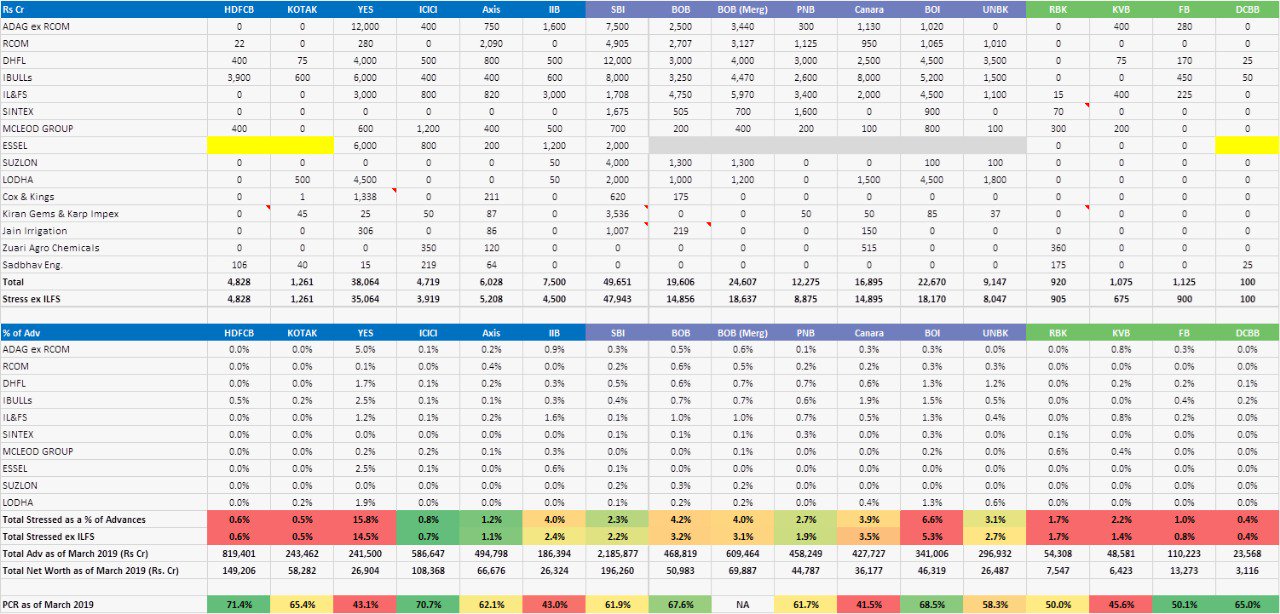

How much is the exposure for CG Power and CCD? I assume it is less than 500-CR.

Please share this info if you have it handy.

CG-POwer and CCD are a decent franchise… i will expect yes bank to nominate a good BoD and leadership team and may be in 2 -3 years, rerating will happen.

we look at it from the curent market valuation perspective and i am sure, Yes bank is looking at the real valuation.

disc. invested in Yes bank.

1 Like

Should Yes Bank manage bank ?

Or

all npa portfolio and their line management ?

3 Likes

In hindsight, seems that the RBI was bang on to remove Mr. Kapoor. Isn’t it? Can anyone guess and say approx. how much % of the loan book can be assumed to be good and what’s the book value in the worst case?

4 Likes

all news seem to be bad news for this stock. stinks of bad management. learnt an important (bitter) lesson : bad management is a more critical criteria than fancy numbers.

3 Likes

People who track this closely and have sound understanding of banking business , can you please tell me what could be the worst case scenario ? If suppose banks loose all the money in NPA’s and companies like Reliance capital , CG power , IFLS , DHFL etc. What would be they left with (BV) in end if we assume this money is not gonna come back ? As per last quarter results , Book value is 114 rs per share.

I am trying to search for a price which have enough margin of safety and than will enter again. Stock is daily going down like a falling knife , but I personally feels things should improve in long term. I have not seen a Indian bank getting closed in my life time. Hope Yes bank wont become the first example. Moderators please delete the post if you don’t find it relevant.

Disc : Invested since 2012 and still holding.

5 Likes

Please read about Global Trust Bank. If 10% of the book is not repaid and you are leveraged 10X your entire equity is gone. As outsiders I don’t know if we will ever be able to analyze the book the properly. At best this a gamble.

10 Likes

I don’t think we have customer wise loan distribution in the public domain and as Yes calls it “Can not Disclose as it’s Confidential”. Recently we saw reputed names including HDFC MF who have subscribed for QIP. I believe that they have done their due diligence including a worst case scenario.

The management has gone public stating that approx 20% of their exposure is BB and below". And approx 10% is under watchlist. Any further deterioration would severely impede the lender’s ability to raise capital to cover its losses (and even if that were to happen, it would be at a substantial dilution to existing shareholders). The suspicion of internal rot has kept investors on tenterhooks which is compounded by the rumor that there are many skeletons in the cupboard. Yes Bank also has the highest exposure to NBFCs and select real estate groups which have their own set of issues, not accounting for their severely stretched liquidity. Since the new management has no incentive to hide the mistakes of their predecessors (except perhaps try and save the jobs of the thousands of employees), any more hits to their capital would severely constrain their fund flows. While in the normal course we would expect the RBI to step in, the current government may allow the natural death of this institution wiping out of the equity of the promoters and facilitate a merger with Kotak (double wink) in the interest of depositors (who would otherwise run the bank to the ground).

Seems ominous and macabre situation for a “Yes” bank management which couldnt say a “No” to its promoter, but the price movements seem to hint everything towards this unfortunate end.

3 Likes