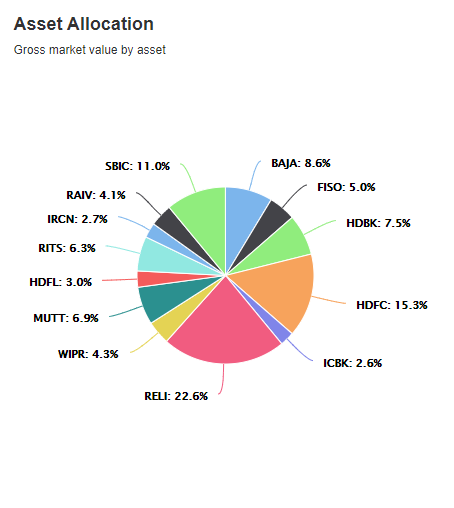

I’m new to investing (< 2 years) and am 21 years old. Have been building this portfolio for the last two years. Looking for some review/critique. Keep in mind though that I have almost equal amount invested in Large-cap MFs so some obvious stocks like HUL, INFY, Bajaj Finance have been ignored to avoid concentrated allocation.

Indian Portfolio:

Number

Stock

View

1

Reliance Industries

Long term, making good moves with Jio+retail.

2

HDFC

Long term, undisputed NBFC leader

3

SBI Cards

Long term, good growth expected

4

Bajaj Auto

Long term, three-wheeler market leader + good 2 wheeler exposure

5

HDFC Bank

Long term, biggest private bank

6

Muthoot Finance

Long term, diversification into gold + equity in NBFC

7

RITES

Medium term, Rail + Infra PSU, good order book, divestment

8

Firstsource Solutions

Medium term, small-cap IT firm with good growth

9

Wipro

Long term, most innovative IT company along with HCL

10

Rail Vikas Nigam Ltd

Medium term, Rail + Infra + Finance PSU

11

HDFC Life

Long term, market leader but expensive valuations

12

IRCON International

Medium term, Rail + Infra PSU, does international construction too

You have a very solid portfolio which can compound capital at a good rate especially with age on your side. If I was in your place I would allocate atleast 10% of capital to 2-3 well run small caps who have the potential to be 5-10x of their size in next 10 years.

Over the long term even 1 such investment can make meaningful impact to portfolio returns. For eg : A company like laurus - 10k Cr market cap can be a 20k Cr market cap company in next 3 years if they execute well and even beyond that they have enough opportunity to grow.

Whereas something like a HDFC and Wipro are well past their fast growth phase and would perhaps be able to grow at best at few % points higher than market rate due to their size.

I do agree with you that I need to invest some more in fundamentally strong small caps, that is exactly why I have around 22% of portfolio in cash (also because I’m expecting a drop soon after US elections).

Although I don’t exactly agree that companies cannot grow fast just because of their size. Amazon was $550 in 2015 and everybody said that’s it, the market leader has reached it’s peak. Today it is trading at $3260, that’s almost 6x money in just 5 years. Apple reached $1T valuation in 2018, and yesterday it reached $2T valuation, again a 2x in just 2 years. Although we don’t have companies such as Amazon and Apple, but just the size of a company cannot be responsible for slow growth.

Congratulations, you got an important lesson learnt pretty early which many, including me, take years! By when have you been investing and is this your first portfolio? I have myself been on lookout of strong tech focussed consumer firms (or those developing in that direction) in India like Amazon, microsoft, Google and Netflix but so far been unsuccessful.

HDFC, HDFC bank, RIL …these are also one of largest holdings of MF…so they are overlapping with your MF portfolio. You have railway heavy shares…can you give rationale about that…only IRCTC seems missing can you explain how each railway pick you have differs from other and why not consolidate the railway basket into the most worthy one…

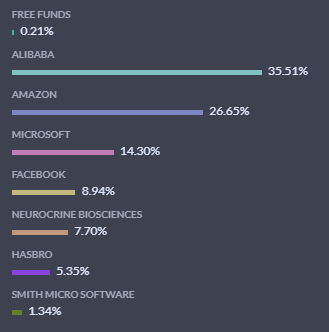

I envy your US stocks wish we had that opportunity in India…thanks

I agree with @Investor_No_1, although the options are now opening up, with Indian brokers tying up with US brokers, few have already started this service, although quite expensive

oh, yes I have been reading that many brokerages have opened up, specially after this crash and way the US markets have lead from front. Also, many PMS managers invest globally - this is one edge they have over retail investors. India has many good companies which may turn great but US has plenty of great companies in sectors I really like such as FMCG, consumer technology and branded pharma…

You mention that the service is very costly…can you elaborate on how to invest in US stocks for Indian retail investor and what are the price points/brokerages etc.? Thanks

HDFC, HDFC bank, RIL …these are also one of the largest holdings of MF…so they are overlapping with your MF portfolio. You have railway heavy shares…can you give rationale about that…only IRCTC seems missing can you explain how each railway pick you have differs from other and why not consolidate the railway basket into the most worthy one…

I envy your US stocks wish we had that opportunity in India…thanks

To answer your previous question, I have been investing since late 2018, so around 2 years. And yes, this is also my first portfolio. Yes, these three are some of the MF’s largest holdings but in April they were available at such beaten-down valuations that I could not resist. I wasn’t brave enough to have a complete small to mid-cap portfolio so it was nice to buy some security at cheap prices.

As far as looking out for strong tech-focused consumer firms in India, I have found some few but that too are trading at expensive valuations and hence haven’t invested yet. All big tech companies we have are all identical outsourcing machines with different names. 0 innovation or moat. Amongst those, I like HCL the best since it has a high R&D spending along with some production in hardware too. Info-Edge and Affle are also good in this space.

I do have railway heavy shares (only about 13% of the total portfolio and no more than 6 in anyone). RITES and IRCON International are pretty similar given that they do both rail and infra projects in India and abroad, but RITES has a slight edge in that it also does consultancy services for the government. Currently, railways are up for bidding in 3 stages to various private companies, and who is consulting the government to select the best one? RITES (they might also bid themselves in a later round). RVNL is kinda like the proxy company for railways to handle their projects. They themselves have a good order book, but they are also responsible for giving railway infra projects to further infra companies as they did recently in Dilip Buildcon.

About why I don’t hold IRCTC, there are two points. I don’t like the valuation, and I don’t like the business. IRCTC has a pretty high valuation for a PSU company (40). And although it has a monopoly on the railway internet ticketing and catering, there is a difference between such a monopoly of IRCTC and say Amazon. IRCTC is a government-controlled monopoly. It isn’t the best at what it does, in fact, it feels like it doesn’t even try to be the best. Their UI was terrible around a couple of years ago while websites like MMT and Yatra put in so much effort towards that. I don’t think anybody has been happy with IRCTC catering, it’s a necessity to say at most. If the government allowed competitors in this space, which at some point they might, I don’t think IRCTC would stand as the leader.

For me to even think of buying IRCTC, it’d have to be at a < 20 PE valuation which is about a 50% drop from current levels.

I agree with your take on IRCTC and indian IT. I would say the way you compared it with Amazon, same test must be done for above names like affle, info edge. Info edge is an investment company to me rather than consumer tech, and so far a good investment company. I do not track affle but without tracking I can say it would not be close to Amazon/Google/microsoft in even the line of business longevity and runway. I did a one line read of its business and at first glance it looks to me as a media company which uses technology and is B2B as it does not serve consumers with any product or services. It rather does mobile marketing so its customers are businesses who want to market. So it does not pass my filter of consumer tech in the very first line of their business. Can you share what consumer tech companies you like in India which are costly? Maybe IndiaMART is closest to a consumer tech I can think of right now, although it is B2B heavy. Jio is a perfect consumer tech in India, sadly not available in silo to retail investors…

Jio definitely is one of the fastest growing and most capital rich consumer tech we have. Not just that, it also has acquired various other consumer techs under it like embibe (Byjus) and most recently Netmeds. Jio IPO might take some time, Ambani might use it as a distraction from any negative news if at all (could be Aramco deal). He has Jio and Retail sectors to list anytime he might need capital.

Apart from Info Edge and yes, even IndiaMART is good too (esp their ROCE numbers), I like Dixon Tech too. It’s consumer hardware play but is unique and can be big in India, I just don’t like the premium valuations it has gotten right now. Many of India’s biggest consumer tech companies with a moat are mostly private as of now and I feel the main reason for that is not many of them are profitable. They are in their startup stage but have unicorn valuations. Paytm, ClearTax are some examples.

Well not wanting to hijack this post so I’ll be very brief

The best option for direct investment in stocks would be to look for a broker in India that provides investment in US stocks. Vested is one of the platform among discount brokers (not recommending as I have never used them) and then you have big players like ICICI Direct, HDFC Sec etc.

The brokerage charges are not particularly high and you can also buy fractional shares.However,the major pain point is transfer of money from India to US trading account which could eat in your capital by almost 10% before even you take a trade and then currency risk , redeeming profits and all sorts of things.

I would say it is better suited if you have good investment capital where remittances and brokerages will only make a small dent when compared to profits realised.

This is true regardless of your brokerage. Even with me, in my US portfolio, I’m down about 8-9% in my profits from where I should be JUST because of forex rates. I paid for my US stocks in Euros and the EUR/USD rate is about 10% from my average, hence the loss. Although if you are investing in INR, I’d say you’d be making even more than your actual return since rupee has been going down compared to USD for as long as I can remember.

Yes, The biggest hindrance is near 10% loss even before we can take a bet on these US stocks. I guess, investing in US focussed MFs is a better idea than trying to take direct exposure to US stocks.

As I mentioned again, if you are investing using INR, you should not be worried about loss. Dollar has been strong against INR since we have gained independence. In fact, it might give you more returns than your stock returns due to INR weakening. Though yes, investing in Hybrid funds like Parag Parikh Long Term Equity Fund or Motilal Oswal Nasdaq 100 FoF or Franklin India US Feeder are good options to invest in US stocks.

Rebalanced my portfolio a bit. Added a position in Deepak Nitrite a week ago and reduced HDFC Life completely. Although I think HDFC Life has a good future ahead, I’m uncomfortable paying 1.5x industry premium for it. It’s also lagging the market pretty much right now, especially with the LIC IPO news coming as well. I’m looking to add IOLCP as well as according to my DCF calculations (12% discount and 15% margin) it is still undervalued despite its recent rally.

Number

Stock

View

1

Reliance Industries

Long term, making good moves with Jio+retail.

2

HDFC

Long term, undisputed NBFC leader

3

SBI Cards

Long term, good growth expected

4

Bajaj Auto

Long term, three-wheeler market leader + good 2 wheeler exposure

5

HDFC Bank

Long term, biggest private bank

6

Muthoot Finance

Long term, diversification into gold + equity in NBFC

7

RITES

Medium term, Rail + Infra PSU, good order book, divestment

8

Firstsource Solutions

Medium term, small-cap IT firm with good growth

9

Wipro

Long term, most innovative IT company along with HCL

10

Rail Vikas Nigam Ltd

Medium term, Rail + Infra + Finance PSU

11

Deepak Nitrite

Long term, Cheap valuations + good free cash flow

12

IRCON International

Medium term, Rail + Infra PSU, does international construction too

That took a lot of research but just by looking at their business segments, you can notice how Wipro and HCL aren’t just outsourcing machines developing software for offshore companies. They try new things, spend a good % of sales on R&D, are more efficient per employee.