How about comparing Wipro/HCL with LTTS and Tata Elxsi in terms of innovations and future ready?

Tata Elxsi is trading at an expensive valuation of 68.61 and has exactly same revenue sources as TCS with different verticals. LTTS seems good at this valuation with a nice balance sheet. It might be heading towards being a large cap in the next few years.

2 Likes

The happiest minds IPO could be the answer for IT/Tech. Promoter quality is blue chip in Ashok soota and considering they run on themes of big data, iot, cloud computing I can see the market giving them valuations similar to infoedge/affle in the future. Been waiting eagerly for it. Getting allotments is another matter. CAMS could be a good fintech bet with the secularity of its 15 Mutual fund companies and the growth drivers in “alternate investments”. More fintech than tech but it looks a lot more stable than most tech companies as it has somewhat predictable revenue

What is your views on Oracle financial software services which perhaps is the only listed company which is in to cloud computing with its own Data center ??

My 2 cents on this

- Oracle (Parent company) is too late to get a market share in cloud.

- Oracle cloud computing solutions are B2B product Vs B2C products from amazon, google.

- OFSS growth rate is poor.

1 Like

Thanks…

I am not an expert on IT, but my understanding is that very recently they have opened two Data centers one in Mumbai and the other in Hyderabad…

if I want to invest in cloud computing / cloud service provider, I don’t think there is such a stock in India today… this is the only listed company as of today…even if B2B…

None of the existing IT pack such as TCS, Infosys , Wipro, tech Mahindra are expert in clouds…none of them have data centers…

They are moving their existing banking customer (those who are using flexCube for example HDFC Bank) to cloud. I guess they are afraid as they might loose customer as now a days cloud is a compulsory thing. So this may be a value proposition and might help them to get some more business.

Banking softwares are a very stick business. I don’t think this may help them a lot. Definitely this may save their existing clients.

Recently Vijay Kedia also entered in this stock as he don’t find a pure play for cloud theme.

Market is very smart, if they has a little sense of this cloud computing going in right direction, you would have seen a huge demand especially after us tech stock rallying.

4 Likes

Oracle finance is as far as I am aware an ERP product which are now as a segment extending them to cloud like say SAP Hana or Oracle fusion. So these are not exactly legacy technologies but neither cutting edge latest pure play digital. Pls correct me if wrong and if Oracle finance does have anything pure play digital?

Regarding data centers, I think Tata communications is the king here and RIL also had some interest here to grow? Thanks

1 Like

I thought they are now aggressive in pursuing what the market needs especially the banking industry and it is reflected in Q1 performance. I stand corrected… Performance better than Most of its peers.

Is Oracle cloud application part of listed Oracle financial services Ltd? I doubt as the listed entity by its name and functionality point to the ERP application for financial services and whatever digital offerings an ERP can provide these days…and not the actual full blown cloud/AI etc.

I am no expert on Oracle, but if I was someone who didn’t understand the cloud sector, but I saw growth in there, I’d simply buy the market leaders and Oracle is far from the leader. Amazon, Google, MSFT rule this space with some emerging players such as Salesforce. In terms of India, again I like IBM and Sify as they have a good presence in this space but sadly neither are listed in our market. The barrier to entry in this sector is also one of the highest. Financing a wide-spread network with low latencies as AWS and Azure with cheap enough prices that can beat them is almost unimaginable, hence many companies are focusing on niche cloud areas such as healthcare and finance.

1 Like

At such age you have good sense of Investing. I read the whole thread and can say you have matured very early in investing. I would only say to relook at SBI Cards. Not that stock is bad but valuation wise I am not comfortable. In Tech if you want a small cap try looking at Xelpmoc. Good work by the way !!

2 Likes

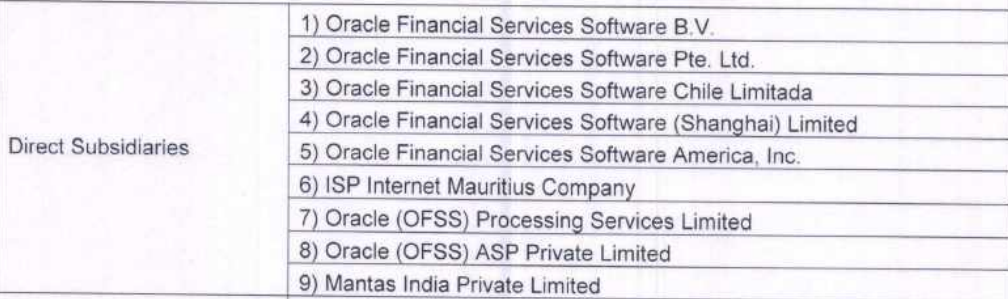

I doubt if this cloud business comes under listed subsidiary OFSS.

Can any one please confirm this?

Thank you so much. I’m comfortable paying a little premium for SBI cards as it has the largest market share in debit cards and the second-largest in credit. It surprised me with amazing Q1 results after a horrible Q4 result, which also indicates that going forward, Corona or no corona, people will use cards and apps more to pay than hard cash. Being the largest government bank, it holds a lot of government employee accounts which basically means it gets a new customer every time a new person joins government forces (they are all spread across various government banks but largest with SBI). If they had posted weak Q1 results, I might have revalued their position in my portfolio.

I looked into Xelpmoc and they do have some interesting products in their portfolio, especially trucking logistics and some other edtech ones, but I fail to see why this company deserves a P/E of 261. No matter the growth potential, I’m just not comfortable paying that high a multiple for any company, even Amazon. That just prices in for so many years of future growth. Either they’d have to drop considerably or just post really high growth earnings for me to reconsider them.

I don’t think so too. I went through their latest quarter results and they don’t have it listed under any of their segments. Although they could count cloud under product licenses, but any cloud company in 2020 would want to highlight the word cloud just for the additional hype, so I don’t think so it’s included. They only do ERP solutions.

I also got their subsidiaries and they don’t have any cloud business listed under here too.

Xelpmoc has recently turned profitable from last 2 quarters. Many times PE misguides. PE will automatically Come down in coming quarters.

Xelp has 5.13% stake in fortigo. Fortigo will do 300cr topline in fy21.It will be valued at 3x sales minimum. Nandan nilekani is invested in fortigo. Xelp assets and investment are close to its market cap.It has stake in mihup and other well known startups. I would suggest you to dig deep. You will get to know why PE makes no sense in Xelpmoc.

Their investments although good, are nowhere their market cap. But yeah, it does make PE a little redundant. This is more like an Info-edge case. Their investments are currently worth Rs 35cr according to their latest investor presentation. The sales multiple, I don’t think is of any use as it depends upon what the operating margin is. A 3x sales for 30-35% OPM is insanely cheap but the same 3x sales for a 5-10% OPM is expensive. Valuing small to micro-cap companies has always been hard for me, mainly because it neither has definite cash flows, nor reserves, nor dividends. I like the story so I’d research more about their investments and at what stage each of them is at, although since all of them are private I don’t think I’ll get exact revenue numbers. I’d personally also wait until they complete at least 4 quarters or 1 FY of being profitable. I might seem too defensive, but I’ve seen many friends go in chasing micro-cap or other penny stocks only to lose heavily and never to return again.

1 Like

I introduced you with this stock as your portfolio was very good but a bit defensive. Keep this stock in track. You will learn many things, how fundamentals and current numbers don’t tell the real picture and how most of the current fundamentals don’t do the justice to the company’s future potential. Multibaggers are created from microcaps. You can get rich by Investing in defensive stocks but real wealth is created from microcaps if held for long term. If investing in microcaps has been that simple everyone would have made a killing . I am not saying I will definitely be right in this stock but my long journey in market has been because of picking quality smallcaps.

Disc : I own this stock since 66.

1 Like

I understand and agree that real wealth is created with micro caps. I will keep it in my watch list and might invest as soon as I feel more confident about it. Although with my age, I can afford to be a little more aggresive as I have time to recover even if I lose some bets. I do own one micro cap in the US market but didn’t do so in the Indian market so far. Thank you for the recommendation, I’ll keep track of it.

2 Likes

Is this Oracle and OFSS the same. My understanding is OFSS and Oracle India are 2 separate entities. Correct me if i am wrong.

If not, does improving business landscape for Oracle India has any bearing on OFSS?