Environment clearance is still to be received. 24 months thereafter for expansion to come on line, right? Or have I got it wrong?

Yes, EC is still pending and after EC approval it will be 24 months or more. Till that time the sales will not move beyond 10-15 percent.

4 Likes

Yes, Operating leverage has been played out, now normal compounding will happen, stock will hold till it’s capex is ready for fire, gestation may be 2-3yrs , in the mean time competitor with ready capex will have edge,

The promoters were thinking for large capex as they said in latest concall that this capacity will be the highest in their history and what turnover they achieved since inception this capex will add more turnover than that. They must have waited for all visibility to think of this Capex. Meanwhile competitors like Camlin Fine, Clean Science will be there with their ready capex but the industry tailwinds will help accommodate multiple players imo.

The stock price may test patience of investors till the new capex gets functional.

3 Likes

Q1 FY23 Results-

Environmental clearance

Can someone share the EC itself, cant view the site from outside India?

In Q2 concall they said, post capacity they can do peak revenue of 1200 Cr. Even if i assume 18% margins, EBITDA would be 216 Cr.

For new capacity utilization would be 60% in FY25. May see optimum utilization by FY26. So EBITDA will double in next 3-4 years. Debt will also increase which will impact bottom line. So PAT may be double which looks priced in already

Please correct me if i am missing something.

Management commentary was hawkish for H2FY23 due to US and Europe slowdown. Apart from that there are other strong players like NOCIL, CAMLIN, Clean science.

Someone on the call asked the management about their edge against the competition, his answer was " see my result, it has been growing so i am more competitive".

I can’t find any competitive advantage for the company. If someone have read NOCI, clean science or any other peers. Please update us here.

5 Likes

I have few questions can anybody answer it.

-

rubber chemical segment - they are growing more than the industry average due to China+1 Because china hold 70% of the rubber chemical industry. And they are gaining market share from China.

So what is the price difference between the yasho rubber chemical and China’s rubber chemical?? -

lubricant additive segment - (a) can anybody know the geographical spilit of lubricant Additive that which country have how much market share?.

(b) it is true/false that lubricant will not use in EV ?

(c) why they are growing at more than industry average in lubricant additive segment.??

Thank you

I will wait for the answer.

Is anyone still tracking Yasho Industries?

2 Likes

I See No Detail Business Analysis, hence I’m Breaking down the Business of Yasho In This Thread The Views Are more than Welcomed

Yasho Industries

Yasho Industries Ltd is a manufacturer of specialty chemicals, food antioxidants, aroma chemicals, rubber accelerators and lubricant additives.

Yasho Derives of it’s Revenue from 2 Segments Namely –

- Consumer Chemicals

- Industrial Chemicals

- Consumer Chemicals – Consumer chemicals Include Aroma chemicals as well as Food Anti Oxidants.

A) Aroma Chemicals – Aroma chemicals portfolio includes Clove oil and it’s derivates. Clove oil and it’s derivates are used in basically formulations of Perfume reason being Eugenol, the main constituent of clove oil is responsible for fragrance of clove oil.

B) Food Anti-Oxidants – Assume you want to eat the apple you slice in a half and eat it and leave the other half in open and go on to your work, Coming from office you realise that the other half of apple if probably more or less brown. This happens due to oxidation of apple with air

Now food preservatives are used in commercial use such as Food preservation, Beverages (Juice), Processed Foods, Etc.

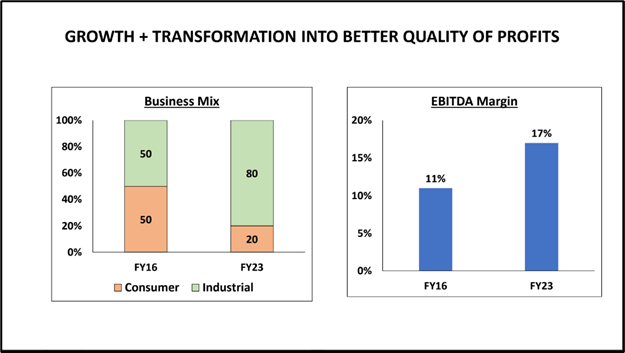

This puts the end to consumer business – Consumer Business is low margin Business – EBITDA margin ranges from 6%-8% (Source – Solidarity Investment Presentation) and hence revenue from this source is 20% (FY23) and 17% (Q2) - Industrial Chemicals –

A) Rubber Chemicals

B) Lubricant Additives

C) Other Speciality Chemicals

The Industrial chemicals is very high Margin Business – 20%+ (Source – Solidarity Investment Presentation) and hence the revenue from the segment is more than 80% in Q3 and for FY 23 it’s at 80%

The company has taken conscious decision to shift from Consumer chemicals to Industrial Chemicals

The same can be observed below –

Source – Solidarity Investment Presentation

Now since the major revenue is from the Industrial Segment and also the New Capex (Which we’ll talk about latter) is in Industrial Segment, Lets understand the business part in deep

A) Rubber Chemicals –

Manufacturing process for Rubber is something as below

-

Harvesting – Harvesting Rubber Either That can be natural rubber derived from latex sap of rubber tree or can be Artificial rubber derived from petroleum-based feedstocks

Some of the artificial rubber are - styrene-butadiene rubber (“SBR”), polybutadiene rubber (“BR”), ethylene-propylene-diene rubber (“EPDM”). -

Harvested rubber is then compounded (Compounding Process)-

Understanding why do we do Compounding – it’s one of the most essential process as it involves to tailor the characteristic of rubber to meet the specification required to meet the needs of End product. It improves the strength of the natural rubber and increases it’s durability, It allows the Rubber to be Flexible helping the manufacturer if the end product to give the rubber final shape, Improves vulcanization (Vulcanization is the process for transforming the raw rubber’s molecule chain into more sustainable and elastic chain of molecules), Stabilising against various environmental factors such as Heat (Conveyor belt faces the issue hence compounding is necessary during it’s production

Some of the Products used in compounding are – -

Vulcanizing agents – Vulcanization process which we learnt about earlier is initiated by the this products (Agents)

-

Fillers – Improves the strength of the properties (Co-agents is one of the Product chemicals of Yasho over here)

-

Softeners – This enhances flexibility

-

Accelerators – they speed up the compounding process

-

Anti-Oxidants – As we learnt earlier the oxidation process here antioxidants protect rubber from oxygen, Rubber is a polymer it’s chemistry with rubber can cause degradation in the Quality of rubber hence Anti-Oxidants are necessary

-

Mixing – the above compound is mixed to make sure even distribution of the ingrediants

-

Shaping – The rubber compound is given desired shape and Size

-

Finishing – Additional Treatment such as cutting

-

Quality control and Packing and distribution

Now Understanding the above process for rubber manufacturing let’s jump into the process of understanding where does Yasho’s Product Portfolio Falls

Yasho’s Chemicals comprises of

A) Accelerators

B) Antioxidants

C) Co-agents

for processing EPDM, SBR, NBR, ECO, Acrylic, NR (Basically for all types of rubber refer manufacturing process)

Source – Company Website

End user are typically – Tyres Manufacturers, Conveyor Belt Manufacturers, Condom Manufacturers, Latex based products (Glove) manufacturers, Etc.

B) Pre – Dispersed Rubber Chemicals –

pre-dispersed rubber chemicals are an alternative form of rubber chemicals that offer certain advantages in the rubber compounding process.

Consider this you want to make panner ka Sabji at home – you have 2 options either you make it from scratch Cutting vegetables, making gravy, adding panner, etc.

Or you can buy Suhana ka Ready made pack and make the Sabji with less efforts

So now back to technical terms

In traditional rubber compounding, rubber chemicals such as vulcanizing agents, accelerators antioxidants, and other additives are added individually during the mixing process. In contrast, pre-dispersed rubber chemicals are formulated in advance, with the active ingredients uniformly dispersed in a carrier polymer.

Certain Advantage is that this are easy to handle rather than Traditional Chemicals as they are in powder for rather than Chemicals form

Some of the products are

i) SULFUR AND METAL OXIDES

ii) DITHIOCARBAMATE

iii) THIURAM & SULPUR DONORS, (Pre-dispersed Rubber Chemicals - Yasho Industries - GLOBAL MANUFACTURER & SUPPLIER OF SPECIALTY & FINE CHEMICALS based in Vapi - India) Website for More Names

C) Lubricant Additives - Lubricant additives are special Objects added to the lubricant (Oil) to enhance the performance of the Lubricant some of the major Products in Portfolio are

- Antioxidants – Same as above but for machinery

- Molybdenum-based Friction Modifiers / Antiwear Agents: Think of it this way machinery has lot of friction inside it to cause the smooth functioning and not to cause the brake down Molybdenum-based Friction Modifiers / Antiwear Agents are used

- Di thiocarbamates: this protects your machinery from any scratches

- Thiadiazoles – This protects the machinery from rusting and protects from any damage from water

End Users are Turbine and Engine oils, metal working glass Cutting (Source – Solidarity Investment Report)

D) The company also has API Business Division but couldn’t get any figures around it nor the business

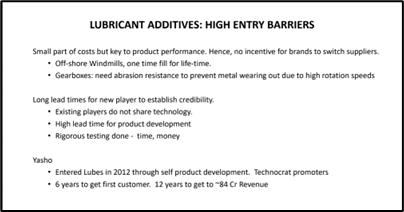

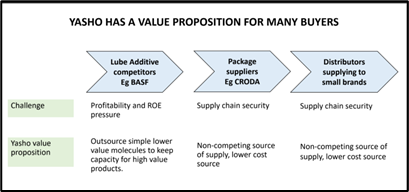

Entry Barrier – Source (Solidarity Investment Report)

Business and Financial Statement analysis

The company has generated more than 25% of CAGR Growth in revenue in past 6-7 Years, increased the margins from 11% to 17% Now aiming for 20% and Upwards (Q1-Q2 Concall)

Improvement in ROCE is also Backed by Change in the product mix one can See ROCE Shoot up from single or Low teens to now Mid twenty

The company undertook the Capex in 2020 and continued for minority Capex improvements, Causing the business to be more or less Stagnent in terms of Volume where as value per molecule kept on changing

Q1 company took on inventory loss due to this however this was majorly a Anomaly (Q1 Concall)

Management is very prudent and Seems to Walk the talk.

The company has the History of performing at the Optimum capacity

The company has undertaken a Huge capex for Industrial products which will go Live in start of FY 25 However the trial production was started Post Diwali (Q2 Concall)

Management has the Quite a good confidence that the Capacity will utilise in 2 Years Or will be performing at atleast 75% of the capacity (Q2 Concall post which in completion of FY26 they will announce the Phase 2 of Capex in Pakhajan (there is still land available after Phase 1 completion

Hence the prudent management not Giving up the cashflow all at once

The management is Very Confident on Back of pending inquires of the clients – Q1 Concall They are Waiting for the Capacity to go live to start ordering from Yasho

One thing to note is that this story will take Loooong time to Play Out, this isn’t one or two Years story

Even management has stated that most probably this year revenue will be flat Q2 Concall and hence In My opinion Following Year FY25 Thoda bhot growth hone start Ho sakta hee

Disclaimer – Not invested Might Look it up to do so in few Days through SIP Since this story will take time to even Start

EDIT - I have taken the Starting tracking Position will add more on the basis of performance Thanks

23 Likes

Hey Saurabh

I’ll Consider Bull, Bear and Base case in margins Rather than PE multiples

PE Is likely the outcome of Growth and market sentiment

Imo considering 18-19% margins at nase case Scenario

15-17% in bear case and 20%+ in Bull case

If co. Delivers good on earnings PEG Will be more than 2

Imo one should set the earnings forecast and not the PE Multiples forecast i might be wrong

Other Key points nobody in the right mind would comprehend the company to do turnover of 1000 crores in this Financial year

- The company doesnt even have the capability to do so

- Capex going live in Q1 of next FY

- 1000 Crore will take atleast 1.5 year FY 25 May be

And hence the whole model goes for toss

I Might be wrong but wrong that co. Can do such big turnover even after 1.5 year may take 2 too

Disclaimer - Invested and Biased

1 Like

Bud the FY 2024 Assumptions are wrong

For a co. That did 300 crores in H1 can do 700 crores in H2?

Great Joke

Please take the physcial capability in account

Like others, i am also learning brother and as i mentioned in the beginning of that post that correct me where i am wrong.I am thankful to you for correcting me.

We both are in the same boat of learning and figuring the things out inthis lumpyness😀

Yes we all are here to learn. Thank you for correcting my mistake.Look forward to learn from you as well as from others.

1 Like

I deleted the post beacuse of my mistakes in estimating the earnings and at the same time i also don’t want anyone to get the wrong post.Will correct my mistake soon.

1 Like

Continuing on this post- my estimates say they reach about 900 crs in FY25 and 1200 odd crs in FY26. Question only remains can they find optimal capacity utilization becasue the costs of capitalisation are going to skyrocket starting FY25.

Additionally, I would really appreciate if someone shared the macro outlook on rubber and lubricant chemicals if they have access or sector knowledge. Macro info is a little hard to track

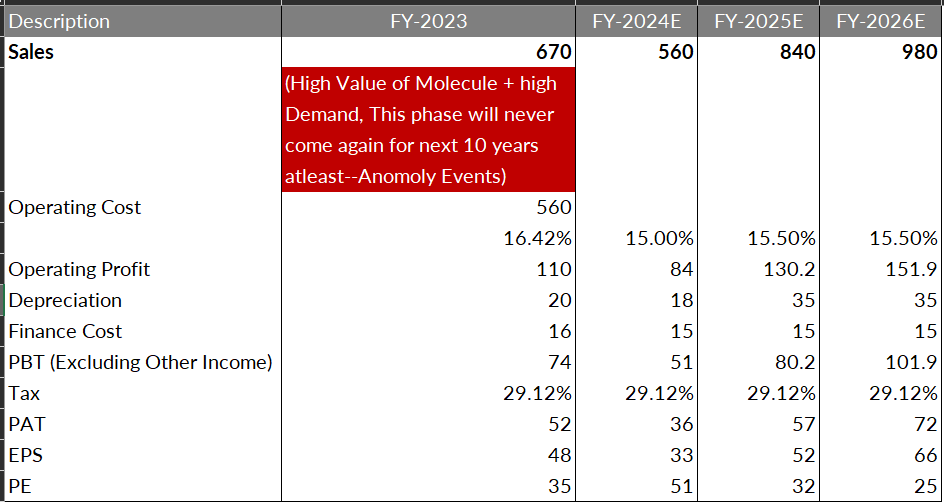

Above is the Rough Sketch of how the things after incorporating MOS Pans Out

Note the company Ain’t cheap at 25x 1.5 Year Forward PE

This is After incorporating MOS

So One thing that once needs to ask management is how much value they add in chemistry this imo is just one or 2 step Process amd hence lots and lots of Unorganized Sector is in the competition

EDIT - After Putting Certain Assumptions such as → Since the margins of new products is 20% → the PF level margins will be in range of 20% the company Trades at around 15x PE → no level of Margin of safety Incorporated expecting smooth Journey

Disclaimer - Invested → Pf Size here Mann's Portfolio - #19 by Ashar_Mann

3 Likes