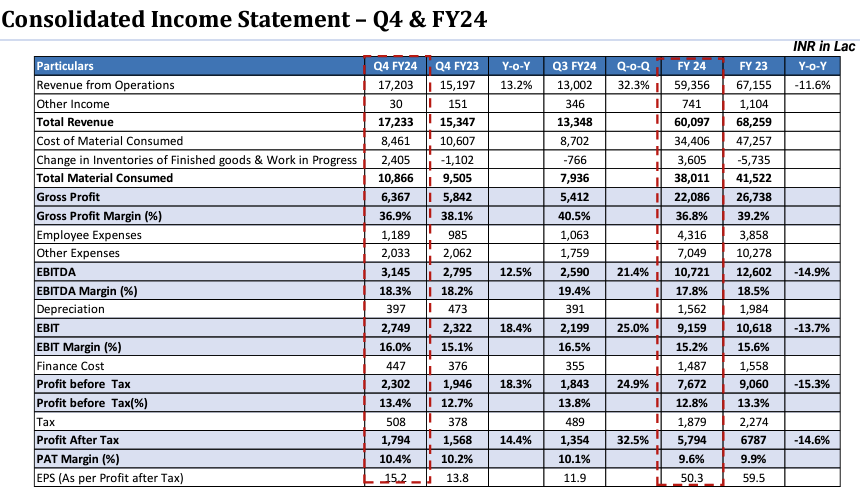

EBITDA Margins stood at 19.5% and PAT margins at 10%

Increase in volume @ 21% YoY and 5% for Nine months (Signaling Demand recovery)

Dahej Plant’s Trail run has began and since the EBITDA margins of the products from new plant is 20%+ new leg of margin expansion will come from here

Industrial segment accounted for more than 87% of the revenue out of which export accounted for 62% total revenue

Incorporated subsidiary in US making it area for future growth

Downward revision in the guidence of total plant capacity → Pakhajan can do 550 to 600 crores of revenue and Vapi can do 650 Crores (earlier guided for 700 to 750) at optimum utilisation (90%)

this downward revision is just on account of correction in RM prices

The prices of RM are correcting i.e. Inching Upward, but not at the speed it dropped

The company is seeing spark already but too early to comment weather this will be fire or fizzle down

current capacity is utilization 85%

Will complete trial, will take govt approvals and then only can start taking orders as client will need everything before placing orders. Will get govt certification within 4 - 8 Weeks

Peak EBITDA will be 120 crores from Vapi facility

Depreciation is on lower side as some asset have got fully depreciated

Peak debt will be 500 crores including WC

Markets will rebound overall within next 2 quarters as the demand comes back in European as well as Asian country

Vapi is completely saturated @18% EBITDA margins any new improvement will come from pakhajan only

Hi @Ashar_Mann

From whatever I understood abt Yasho, is that the pricing of the items would be generally a pass through. if that is the case and the RM costs is inching upwards, then why would the revenue from the new plants decline, shouldn’t it increase? Did the mgmt say anything about why the downward revision to the revenue potential

Hey @divygupta

So Yes you are correct that any kind of RM Increase will result in the increase in the revenue as the it’s a pass Through

The Downward Revision is on the basis of Current Prices of RM if you see management has said that they are not committing to the statement that Price will go back to mean of RM and hence the statement that → weather the price inching up is likely to be a fire or Fizzle out

Hence in short downward revision is Excluding the increasing RM Prices

→ my bad should have framed sentence better

Disclaimer as Above

Now let us look at the guidance for FY25. Revenues of Rs 900-950 crs in FY25 and Rs1250-1300cr in FY26 (up from 596crs in FY24) implying 60% growth in FY25 and 37% growth in FY26 and margins expected too move upto 19-20% (up from 17% margins). People can do that math

It looks like management is giving agressive guidance just for mcap appreciation.

Q1FY25 sales is 172cr so they need to do sales of 240cr in each remaining quarter.

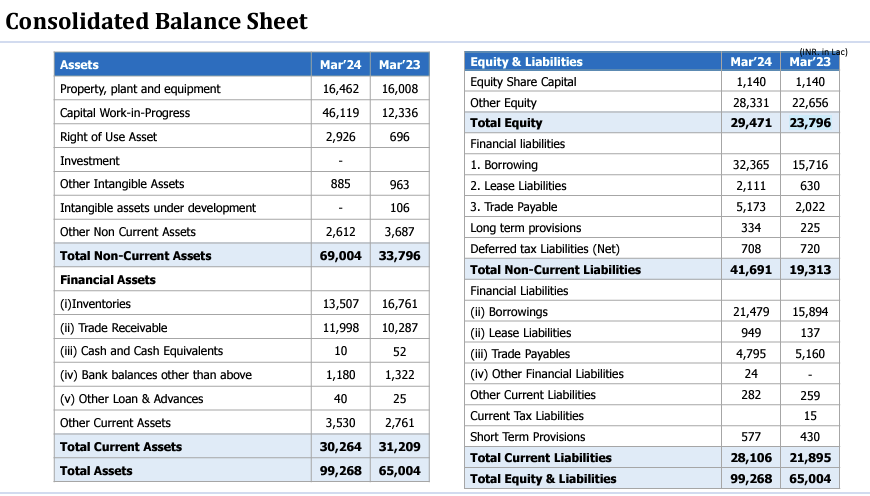

Also borrowing has been increased to 579cr.

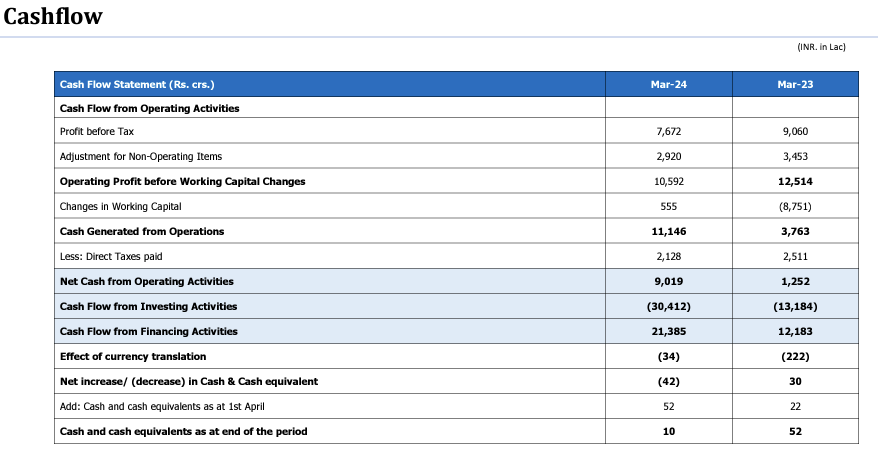

In Q1 they have reported loss and interest cost has been increased from 4cr to 14cr.

Now the whole game is depend on execution by management.

I am tracking this business & saw today’s results. Would wait for tomorrow’s earnings call to get more clarity on the below points. However, if any of the member has any visibility of the below points - would love to hear about it

Their results looks decent with volumes increasing 18% YoY. Encouraging sign is GMs expanding to 47% from 35% same quarter last year. My earlier understanding was that their Industrial portion would have increased substantially as that was the higher margin business. However, the product mix seems to be 82:18 (Industrial to Consumer). Hence, factor contributing to such high GMs is important to understand & their sustainability.

Their inventories have increased alot. This has also deteriorated their working capital days to now at ~200 compared to ~100 in FY24. Need to understand if there was any price increase in RMs that the promoter were certain of? Or what is the reason of such high increase in inventories as it is increasing working capital by a wide margin.

~50% of EBITDA is going into debt payments. Debt / EBITDA being as high as 5x is a strong monitorable for anyone tracking this business.

Management had highlighted that they are seeing some downward trend in prices & that should continue for the next 6-9 months. Has the downward trend in prices effected Q2FY25? I don’t think so - as both volumes growth & revenue growth are almost in line. 2% different give or take.

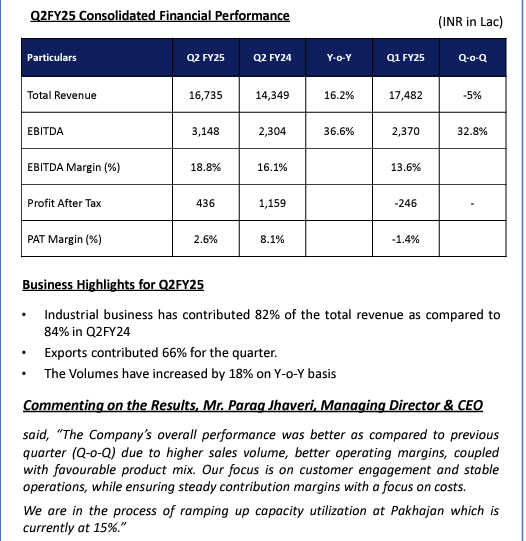

Q2 FY25 revenue: INR 167.35 crores (+17% YoY), driven by a 16% increase in sales volumes.

EBITDA margin for Q2: 18.8%, with expectations to remain between 17%-19% in the coming quarters.

Export contribution: 66% of total sales.

Industrial business: Contributed 82% of revenue.

New US subsidiary to become operational in January 2025 to expand market reach.

Gross margin improved significantly to 45% in Q2 (from 35% YoY) due to favorable product mix (Industrial segment) and contributions from the Pakhajan facility.

The chemical sector remains under price pressure, but the bottom level of pricing is expected to stabilize.

Pakhajan facility utilization: 15% in Q2; expected to reach 35%-40% in Q3 and 60% by Q4 FY25.

Long-term guidance: Pakhajan facility to achieve 90% utilization by FY26.

Industrial chemicals remain the primary revenue driver, with expected volume growth of 30%-40%.

*Continues to gain market share, leveraging a strong product portfolio and approvals pipeline.

The lubricant additives market estimated at $10-$12 billion, growing at 3%-4% annually.

Export markets, particularly the US and Europe, account for over 70% of industrial segment revenue.

Inventory levels increased due to customer trials and future production planning.

Working capital cycle currently at 200 days, expected to normalize to 110-115 days by March 2025.

Long-term debt repayment starts from FY26, with plans to reduce debt-to-EBITDA to 3x by FY26.

Gross margin improvement attributed to product mix optimization within the industrial segment.

Pricing pressures impacted revenue despite volume growth, with chemical prices expected to stabilize.

New customer approvals for Pakhajan products are progressing, with significant ramp-up expected by Q4 FY25.

Cautious due to global chemical sector volatility but confident in maintaining EBITDA margins.

Operationalization of the US subsidiary in January 2025 to cater to smaller customers with shorter lead times.

Focus on long-term contracts to mitigate pricing volatility.

Infrastructure investments (e.g., Pakhajan facility) provide room for future capacity expansions at lower incremental costs. Double the capacity with 200cr investment.

Long-term focus on sustainability and competitive positioning in mature markets.

Stabilizing raw material and freight costs.

Increased demand in industrial chemicals.

Global pricing pressures in the chemical sector.

Delays in customer approvals impacting capacity ramp-up.

Pakhajan facility expansion allows for incremental capacity additions with minimal infrastructure costs (~INR 200-250 crores).

Long-term plan to expand capacity post-70% utilization.

Export to the US and Europe remains a significant contributor to revenue.

Tariff changes in the US may present opportunities, though uncertainty remains.

Growth focus on Central and Latin America for diversification.

FY25 revenue target unlikely to reach INR 900 crores due to pricing pressures, but volume growth remains strong.

FY26 revenue target of INR 1250 crores maintained, with expectations of better price stability and margin improvement.

Long-term debt repayment begins in FY26 (~INR 25-30 crores per annum).

Future capex will leverage existing infrastructure at Pakhajan to minimize costs and enhance ROCE.

Yasho Industries Limited is a leading Indian manufacturer and supplier of specialty and performance chemicals, including food antioxidants, aroma chemicals, rubber chemicals, and lubricant additives. It also manufactures BHA (butylated hydroxy anisole), AP (ascorbyl palmitate) and various complementary antioxidants which are used in edible oils, fried foods, poultry feed, confectionery, and vitamin blends.

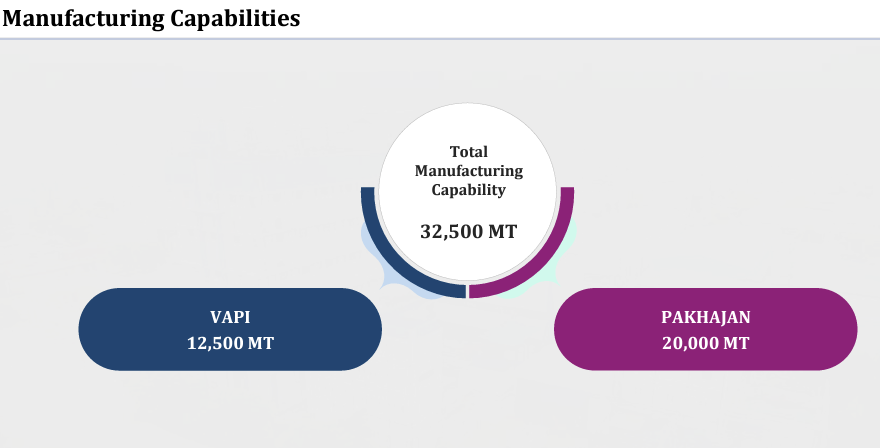

Established in 1985, the company has significantly expanded its operations and product offerings over the years. It has 3 manufacturing facilities in Vapi Gujarat with a combined capacity of 12500 MTPA. They acquired a 42 acres land in Dahej for further greenfield expansion which is the new plant at Pakhajan.

Products

Two major verticals - Consumer and Industrial with total 142 products (according to latest ppt)

Accelerators / Antioxidants / Co-agents for processing EPDM, SBR, NBR, ECO, Acrylic, NR and more.

Pre-dispersed Rubber Chemicals

For dust-free handling and to achieve better Dispersion.

Aroma Chemicals

Is a market leader in a supply of Clove oil & its derivatives.

Food Antioxidants

Form the company’s core business and Yasho is amongst the leading manufactures of Food Antioxidants in India.

Lubricant Additives

Manufactures a range of Additives for Industrial / Automotive Lube & Greases like Antioxidants (Phenolic / Aminic), Molybdenum based Friction Modifiers / Antiwear agents, Dithiocarbamates, Thiadiazoles Corrosion Inhibitor & Extreme pressure additives, Triazole Metal Deactivators

Specialty Chemicals

Manufactures various Specialty Chemicals used in different segment of industry such as Electroplating chemicals, Intermediates for API / Bulk Drugs, UPR Resins / Fibre Composites Resins, Thermoplastics Urethanes (Polyurethanes), Printing Inks & Agrochemicals.

The Industrial division is the key revenue driver contributing 84% of the revenue while consumer contributes the rest.

4 new products in the pipeline with an addressable market of 5500 crores in Pakhajan.

The company is more focused on industrial segment which is a higher margin segment and according to the management, the consumer segment isn’t growing.

There products can be further divided into commodity and Value added products (VAP)

Commodity: Includes chemical for tire manufacturing. The new plant at Pakhajan focuses on producing high volume commodity type specialty chemicals with average selling price of around 350.

VAP: Out of the specialty chemicals for rubber and lubricants which are split in 60-40 ration, about 25-30% are VAP. YALUB and YANTQ are the brands in lubricants and food preservation respectively.

Geography

They have customers in over 50 countries with over 2000 customers. They have offices in India, US, Europe and are expanding in Latin America.

Geography

Revenue % share

India

36

US

17

Europe

29

R.O.W.

18

Within the Industrial segment, US and Europe account for 70% of the revenue and US is 40% of the revenue in the overall export segments.

Central and Latin America are potential markets for future expansion, while the company has already expanded in Asia and middle east.

Over 2000 clients with the top 10 customers contributing approx. 30-35% of the total revenue with all of them being with them for over 5-7 years.

Works on long-team contracts with price and volume commitments for a quarter/ 6 months to mitigate price fluctuations and customer cautions.

Raw Material

Sources 40% of its RM from sustainable sources

Few of the key raw materials include:

Hydrophenol is sourced from Europe, the USA, and Japan.

Diphenamide is procured from suppliers in the USA, Europe, and China.

Amines are obtained both locally in India and through imports from Europe and China.

Raw materials for aroma chemicals are imported primarily from Indonesia and Madagascar.

Competition

China is a big competitor and due to dumping from China, there is a pricing pressure. Even with China + 1, the customers want chinese prices for non-chinese chemicals

Lubrizol in lubricants is a big player and they get competition from established players in Europe

Industry Insights

Global Chemical and petrochemical market is expected to reach $300 billion by 2025 with the Indian specialty chemicals industry positioned as a prime catalyst for India’s economic growth and development. It is designated as a sunrise sector by the Ministry of Chemicals and Fertilisers.

The lubricant market size is about $10 to $12 billion and the market growth is between 3% to 4%.

The Indian specialty chemical market is growing at almost 2x the global.

There has been a slowdown in the industry due to destocking and economic weakness in Europe & China.

Subsidiary

Two wholly owned subsidiary, both engage in specialty chemicals.

Yasho Industries Europe B.V.:

Acquired in 2021, located in Netherlands, provides stocking location in Rotterdam.

Yasho Inc.:

Acquired in 2023, US, it will serve as a stock point for the company’s US retail customers, it will help increase profit margins by 3-5% by holding stock locally by reducing lead time (Eliminates wait time for 90-120 days)

Growth triggers

Rising demand for specialty and performance chemicals, growth in the Indian chemical space.

Shifting global supply chain from China due to geopolitical issues (China+1)

India’s emergence as a prominent manufacturing hub, PLI schemes and anti dumping duty by the government.

Capex

Greenfield capex at Pakhajan, Dahej, Gujarat with capacity of 20k MTPA with cost of 470 crore and is expected to add 550 crores topline at peak utilization and manufacture ~15 products. They have invested in automation, efficiency enhancement at its new facilities which along with inflation and other variables have increased the cost from initial 400 crores.

50% utilization by FY25 and 100% by FY26 and no further expansion until plant reaches 70% utilization.

TAM of the products manufactured at the new plant is around 5500 crores.

Cost of fund is 8.75% and the management does not plan to reduce borrowings but use the cash flows from the plant to finance future expansion. ln FY25 there is no repayment for the term loan and it will be 45-50 crore in FY26.

Notes

Vapi is totally saturated and there is no room left for expansion

Topline guidance of 900-950 in FY25 and 1250-1300 in FY26, they expect 30-40% volume growth to achieve it.

Guidance of EBITDA margin of 19-20% in FY25 and to maintain debt/EBIDTA of 2-2.5 times. Target working capital cycle within 105 days.

There is a volume growth however there is a decline in topline due to pricing pressure which has reduced gross margins.

Disclaimer: Studying, not invested. Any and every feedback is appreciated.

One has to track how the volume growth comes in the coming quarters and how quickly price pressure cools down.

Results for Q3 were not that good and it didn’t achieved their initial guidance of capacity utilization. Further promoters raised some money for paying long term debt and future expansion (now being utilised in working capital maybe kind of signal of some stress in liquidity and balance sheet).

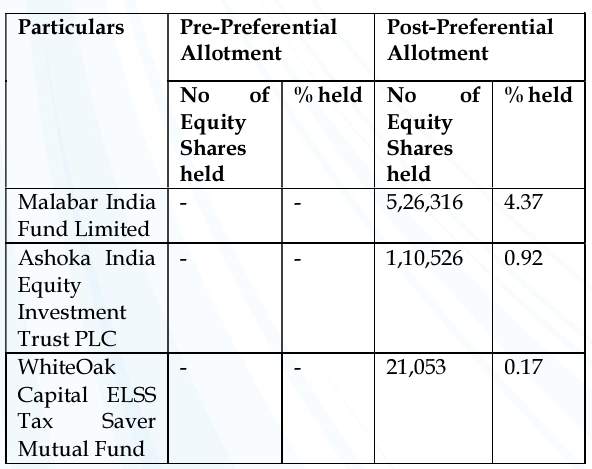

Malabar (Sumeet Nagar) entered must have been one of guys from whom money was raised.

Gross Margin: Sustainable range of 40–42%, with favorable product mix.

Focus on volume growth as prices remain subdued in global chemical markets.

Long-term contracts preferred to manage price volatility.

FY26 Capex: ₹75–100 crores

60–70% toward Pakhajan expansion

30–40% toward R&D setup

Targeting ** debt reduction to ₹450 crores** by FY26.

Long-term goal: Debt-to-EBITDA of 3.5x by FY26.

Additional capacity post-70% utilization planned, with minimal incremental infrastructure cost.

*** All targets delayed by 2qtrs/ except WC days (delayed by one year)** My take 0.4mn revenue/MT with 70% capacity utilisation converts to 910cr revenue

Last year, the company had guided for ₹900 crore in revenue (about 50% growth), but actual revenue came in around ₹670 crore, which is just 12–13% growth. The miss was mainly due to delays in order flow and slower ramp-up of new capacity.

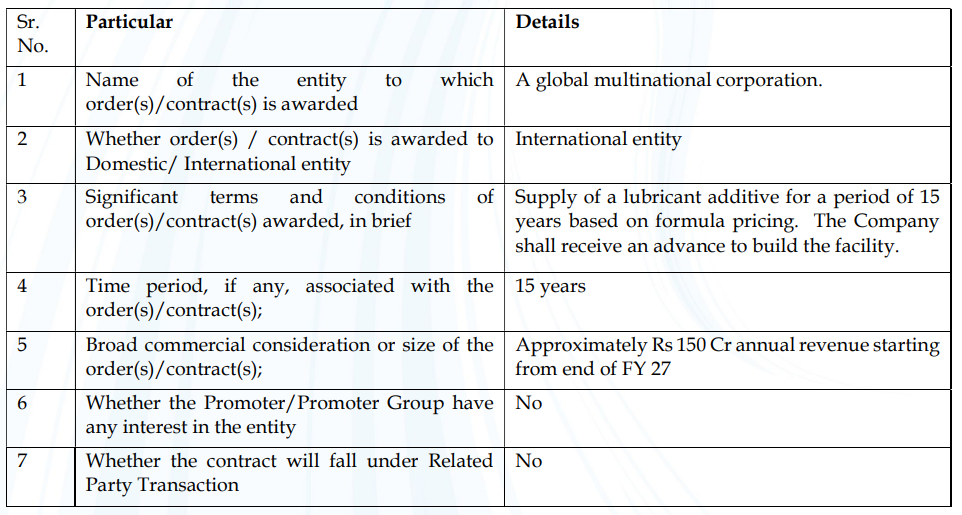

For the current year, management has again given a strong guidance of 40–50% growth. With the recent long-term order win (₹150 crore annual revenue from FY27) and expanded capacity, let’s see how execution pans out this time.

Date: September 04, 2025

Intimation for entering into a long-term agreement with a leading multinational corporation (MNC)

It gets about 25 per of revenue from US as far as I can remember.i think it will be a hit on margins in short term due to tariffs.one thing I did not like was in recent call when an analyst asked about debt the management gave a wrong figure later they corrected it via disclosure.thoughts are welcome.