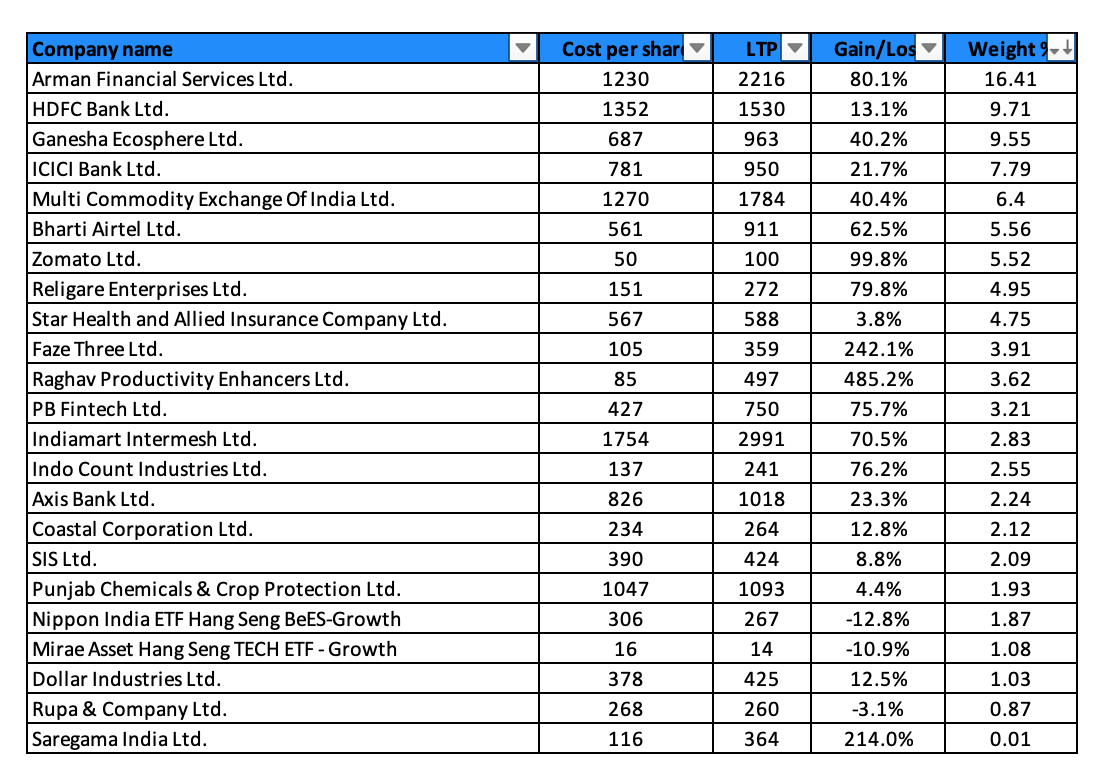

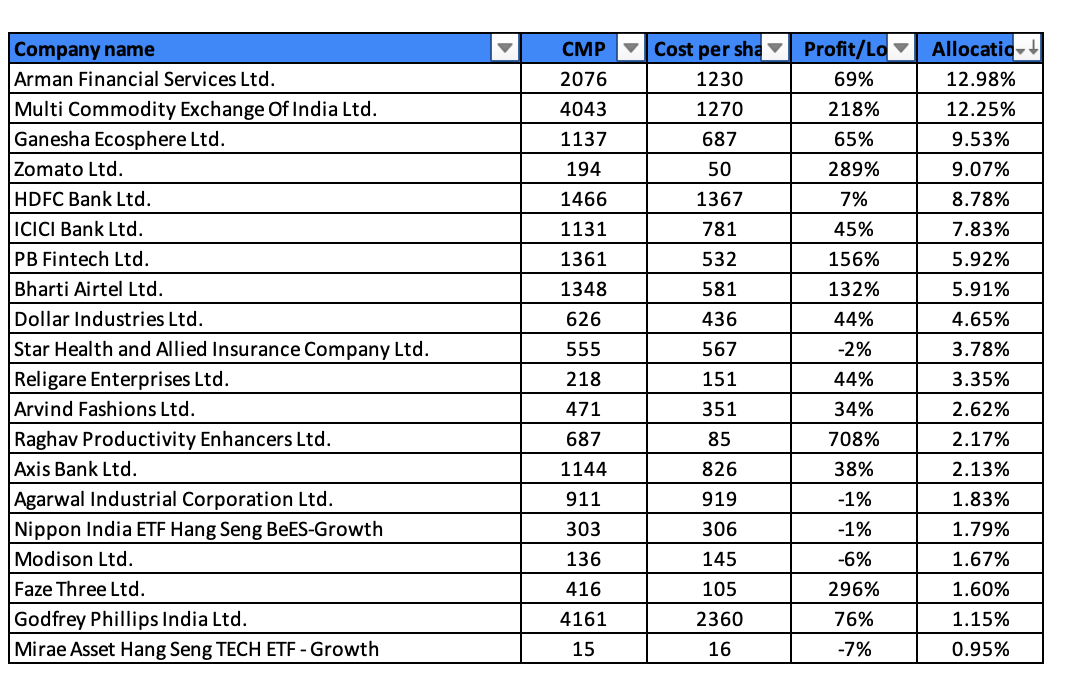

Added Policybazaar (PB Fintech) in the last couple of weeks. The core insurance platform is superb, and has dominant share of the industry’s digital premiums (more than all the insurers own website channel combined). The website attracts 3x-5x more traffic than most insurers own websites and as much traffic as LICs. I believe it has become a strong brand in the insurance space, and is now top of mind in the consumer insurance buying journey. This brand strength should continue to grow over time as the company continues to spend increasing amounts on brand and customer acquisition.

PB-Fintech has the potential to be a structural long term compounder with the following growth triggers:

- Increased penetration of insurance in the country leading to double digit industry premiums growth

- Incrementally more of these premiums coming from digital channels (~60% of Policybazaar traffic comes from consumers below the age of 34 who will coming into their prime income earnings years over the next decade) taking share away from agency channel which is prone to mis-selling, poor experience and fraud.

- Potential for Policybazaar take rates to improve as they become a larger part of industry premiums

At the moment, the platform originates about 1% of total industry premiums. For health, by my calculations, Policybazaar is already accounting for >5% of industry premiums. The superiority of this channel over the agency channel is evident by the premium/salesperson number which is 10x of the agency channel.

Economics:

The core platform generates a 45% contribution margin (including all acquisition costs and variable employee related costs). Below contribution are mainly corporate salaries, brand spend and ESOPs. ESOPs should come down next year and continue at a ~200-300 cr run rate over the long term. Other fixed costs are growing at ~10% per year.

Over long periods of time, as renewal revenue starts to become a bigger part of the premiums, the company’s contributions will expand. Renewal revenues have 85% contribution margin (no acquisition expense).

This is what I think numbers for the core platform can look like by FY28:

Growth of insurance premium from 7000 cr to 35000 cr

Growth of Credit Disbursement from 6500 cr to 35000 cr

Revenue from core platforms: 1200 cr to 6100 cr

Contribution: 470cr to 2750 cr (assumed no change in margins at 45%)

Fixed cost (including ESOP): 1200 cr to 1550 cr

Leading to PAT from core business of ~950-1000 cr in FY28

This is not very far from the guidance given by Yashish Dahiya of 1000 cr PAT by FY27

At 1000 cr PAT, and with 100+% ROE, company can easily be valued at 50x PE. Including Cash accrual, we could be looking at 55-60k MCap by FY28. Effectively a 3x opportunity in 5 years (25% CAGR). Plus all the optionality with the experiments the management keeps doing.

There are 3 things I am concerned about here:

- Market share moving to mobile app players such as Paytm, PhonePe, GooglePay over time. All in all, the biggest value that Policybazaar is providing is comparison between different insurance plans. While there is some challenge of technical integration with various insurers, this can easily move to other more convenient app based channels over time. Will only be evident over the long term given the low digital penetration.

- Change in commissions structure by the regulator: this is not a short term risk anymore given the IRDAI white paper last week. In any case, even if the regulator mandates lower premiums, PB should be able to mantain take rates by charging in other cost items.

- Bima Sugam: regulator is planning to come with its own insurance exchange. Contours of this are still to be detailed out but this could lead to a “UPI” moment for insurance.

The thinking is if any of these 3 come true, I can easily exit at a small loss; whereas if the core platform grows and becomes a dominant insurance distribution channel, the potential for long term compounding is immense.