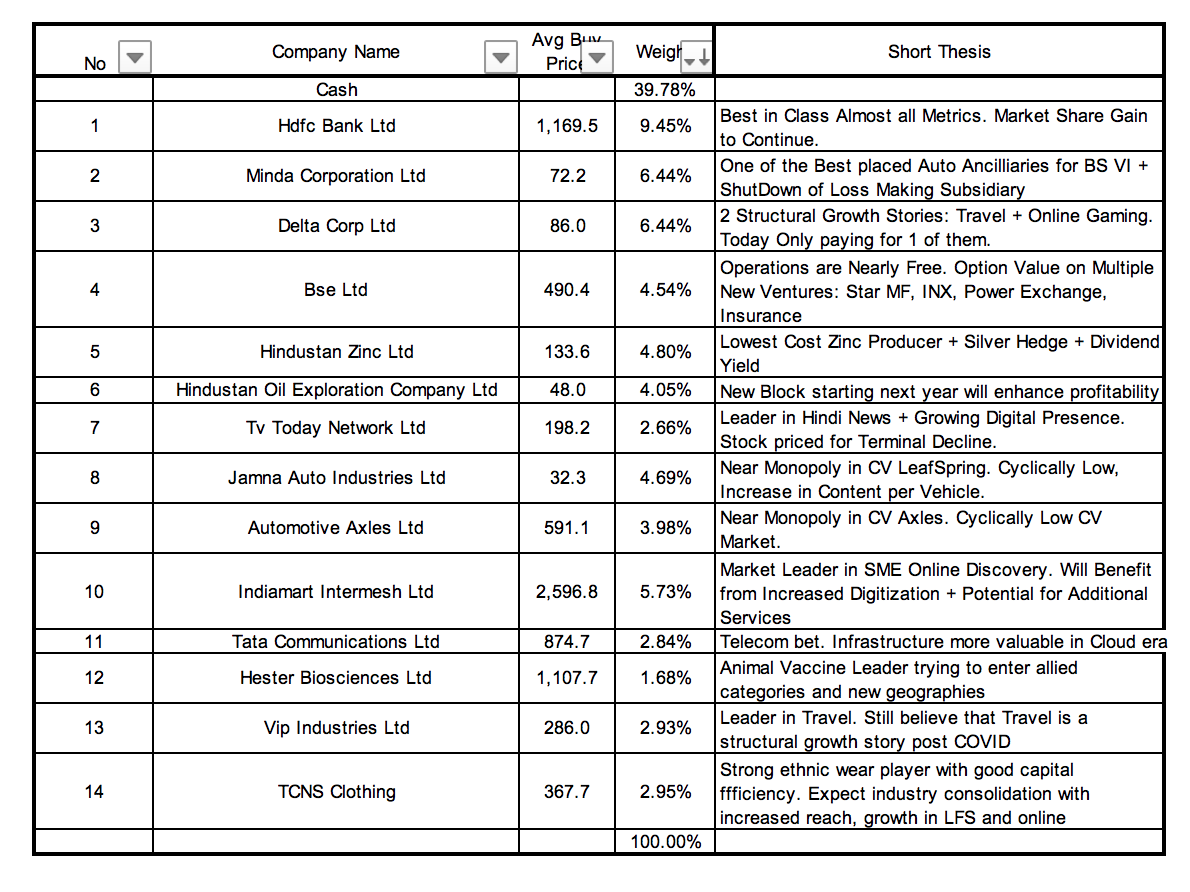

Hi, Started this portfolio in January 2020. Looking for some feedback. I prefer to play large cap through mutual funds, consequently, most of this portfolio is focussed on small/mid caps with selective large cap bets for diversification, balance and where I felt there were not many adequate small cap names (eg banking). Have also booked losses worth about 6% of the PF in March.

Current Watchlist:

Kotak Mahindra Bank

HDFC Ltd

TCNS

Alembic Pharma

Looking to mantain cash portion at about 35-40% given market valuations. Any new bets will have to be made by replacing existing bets. Looking to reduce BSE if any new bets fructify.

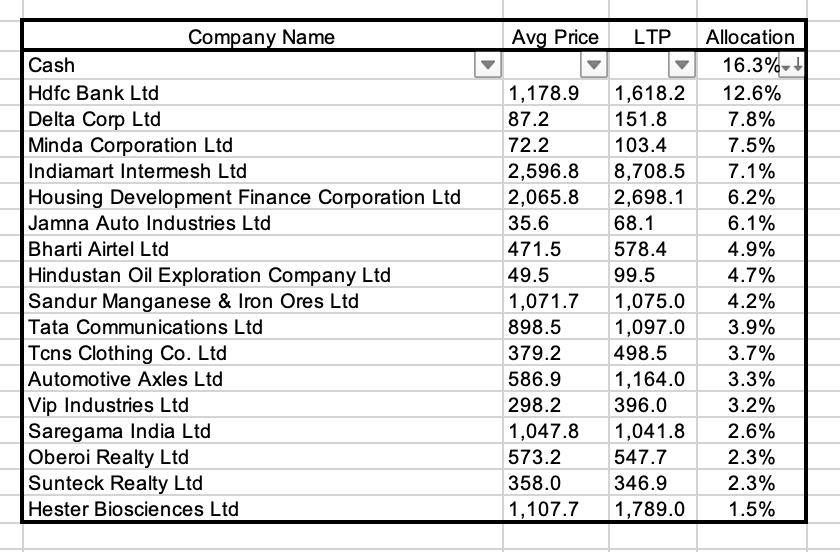

Have added TCNS, increased stakes in VIP and Tata Comm and reduced some TVToday. Got scared of them losing their market leadership to Republic Bharat post the Sushant Singh coverage. Feel the portfolio is unbalanced and looking for some advice.

My 2 cents :

All pharma are near 52 week high - it would be great if you could add them example CIPLA (during this covid - CIPLA stands tallest in respiratory business)

Not sure on others - Auto sector there are headwinds due to liquidity wherein people have stopped buying cars for now due to covid. There might a win win case against if there be might be case of contract however no one knows.

Minda Inustries is better than corp. PS : Exited waiting till end of this year to check on strength

There are no FMCG/ big players such as asian paints, marico to your portfolio consider to add these briges when in event market corrects these bridges will help you.

Thanks for the feedback. Pharma is a theme that I would like to play. Unfortunately, I have limited knowledge of this space so currently working to understand the pharma industry before I initiate a position.

Regarding autos, recent data has been surprisingly positive. In hindsight, a better quality auto ancillary name would have been a better bet, but chose Minda Corporation because they have significant tailwinds with the BSVI transition, so can possibly grow even without the market growing much. I will wait for a few quarters to see if BSVI related gains actually play out for them.

I have purposely kept large FMCG and ‘quality’ names such as Asian Paints, HUL, Nestle etc out of the PF since I am finding it hard to justify their valuations. Always on the lookout for a significant fall in any of these names for an entry. Rather than pay over the odds for them, my strategy is to keep a healthy cash balance to hedge against any market declines when these companies are likely to outperform.

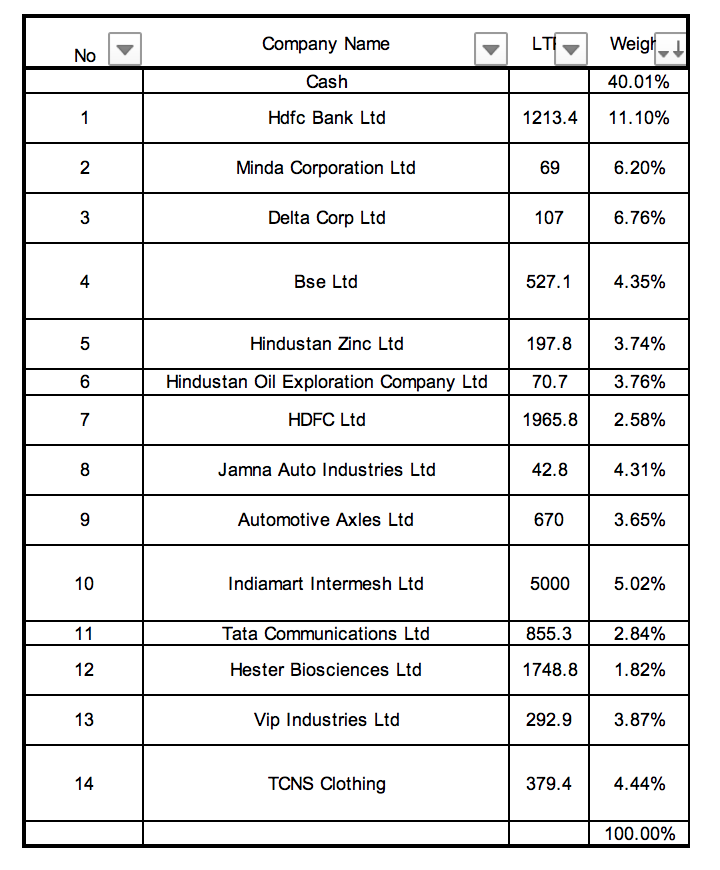

I have made a few changes to the PF in the last month:

Sold all of TVToday. There seems to be a decisive shift in market leadership toward Republic Bharat (at least on paper, lets see how the TRP scam plays out) which is a thesis killer for me. In hindsight, a larger Media house may have been a better bet where one also could play subscription revenues to gain from the increased TV viewership.

Reduced holdings in BSE and Hind Zinc: this was mainly to make space for increased weightages elsewhere.

Increased weight in TCNS & VIP Industries. Feel COVID impact is being extrapolated for a long time and there is still signficant margin of safety in these names.

Added HDFC Ltd. Market Leader available at historically low valuations when most other housing finance companies are struggling/going out of business. Feel real estate cycle has bottomed out and company has made adequate Covid provisioning. See limited risk of book being eaten into in the current year. While I dont think housing finance is a 20% ROE business anymore, I still feel 15-16% ROEs are possible once growth comes back.

Updated Watchlist/To Do List:

Currently studying the pharma sector to widen scope of competence.

NESCO, Godrej, Sunteck, Sobha, Oberoi Realty. Looking to understand real estate in more detail. Think it could be a good play in the current low interest rate environment.

Airtel

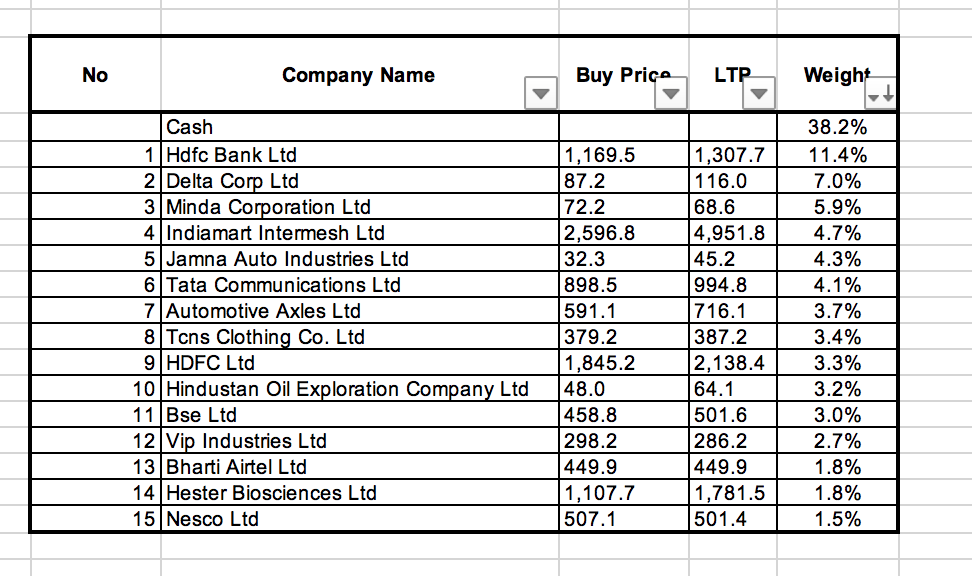

Exited Hind Zinc completely post the dividend and reduced allocation in BSE. This was primarily to make space for new entrants and increased weights elsewhere.

Increased weight in Tata Comm to 4% after the stellar Q2 results.

Added Airtel. Think the risk-reward is really favourable at this price for Airtel. See high probability within a 3 year time horizon of either 1) Improved industry performance with substantial tariff hikes or 2) Improved performance for Airtel with Vi either becoming insolvent or continuing market share loss due to poor network performance. None of these seem to be priced in adequately.

Added Nesco. Strong commercial real estate developer with no debt and stable occupancy. At current price, Company is available at better yields than any listed REIT despite having a much stronger balance sheet.

Some General Thoughts

Getting more and more scared seeing the market rally day after day. However, I can take some solace from the fact that high frequency data is now in positive territory and Covid cases also seem to be receding. There still seem to be quite a few attractive opportunities available, especially in the small and midcap space and in sectors which are not in market fancy. As of now, the near 40% cash allocation in the PF is providing some comfort.

Watchlist:

Continuing on the real estate theme. Some really encouraging sales being reported recently. Sunteck, Godrej, Oberoi

Still trying to understand pharma better. So far uncomfortable with the valuations which is why I have not taken the plunge. However, the industry does seem to be coming out with strong numbers. Currently looking at: Alkem, Eris Lifesciences, Marksans, Ipca, Natco.

Also looking at some quality auto names like Bosch and Endurance.

Now struggling with asset allocation. While I would like to mantain cash allocation at current levels, will have to think really hard about where to reduce allocation. Minda Corp and BSE seem to be places where I can lighten up a little. Minda Corp , while Q2 performance was along expected lines, I was disappointed with the 5% stake dilution at these levels, especially when there are already excess funds on the balance sheet.

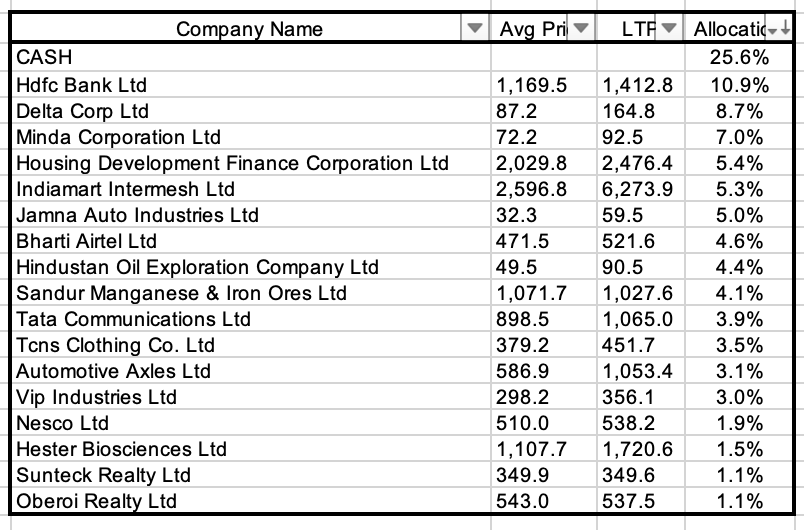

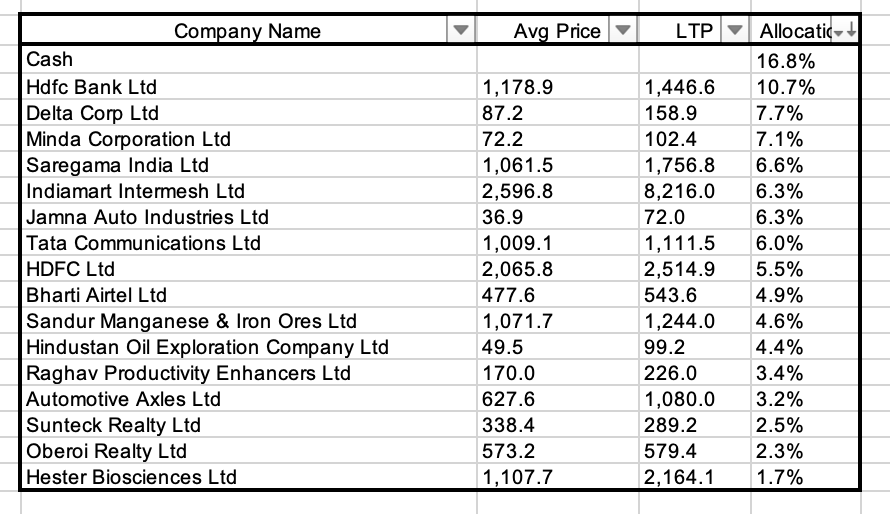

Added Sandur Manganese. The company has many things currently going for it in the current scenario: a) Rising Iron Ore Prices, b) Commissioning of new capex which is likely to lead to a >50% increase in EBITDA & c) Company is also a beneficiary of mines being renewed at higher premiums since it holds its license till 2033. Even if one ignores the iron ore pricing tailwind, company could do an EBITDA of ~320-330 cr once the capex has been commissioned and fully utilized which implies it is trading at ~3.5x forward EV/EBITDA. On top of this, if we add the rising ore realisations (current realizations should be 2x that of FY20) as well as free option of approvals to double mining capacity make this a no-brainer today.

Added realty players Sunteck Realty, Oberoi and increased weight in HDFC Ltd. Real estate cycle seems to have bottomed out and companies with a clean history as well as strong balance sheet are likely to disproportionately gain in the next cycle. Furthermore, IRRs of new projects being done now are likely to be extremely high since at least in the case of Sunteck, most of them are being done through the JDA route. Initial hesitation at adding real estate developers was because it was unclear if sales trajectory was coming due to temporary govt policy initiatives and discounts being given by various developers or a sustainable cyclical upturn in demand. I was wary of a large price fall post March once the policy initiatives ended which would really affect IRRs. However, from various news reports and channel checks, it seems likely that premium reduction may take place in the Mumbai market. This can lead to falling real estate prices while mantaining EBITDA margins for developers; a dream scenario for Mumbai based developers. In terms of valuations, by my calculations, both Sunteck and Oberoi ar trading at slight premiums to NAV. The NAV assumptions I have made are also conservative with an elevated sales cycle and no price hikes for the duration of the projects. This implies that the market is currently saying that these businesses have no terminal value/development potential post the current projects. If anything, for developers with strong balance sheets, potential to acquire new projects today is far better than at any time over the last 5-6 years. Chose Sunteck and Oberoi because they have the strongest balance sheets in the industry and reasonable valuations.

Increased weight in Airtel. Did not expect the customer additions over the past 2 months. If anything, this makes the risk-reward even more compelling for the company.

Exited BSE completely and reduced weight in automotive axles, primarily to make room for the bets made above and to mantain some cash holding which has now come dangerously low to 25% given the current valuations.

Hi

My thought on looking your portfolio.

I like this quality company Like HDFC,Hdfcbank,Nesco your PF.

Indiamart: I don’t track.

Why we have many auto ancillary like Minda corp,Jamna Auto,Automotive axles. Why not direct player like Maruti,eicher ,M&M or any one .

Real-estate play since we have nesco(very good company )but then we have more on Sunteck /oberai. Real estate is highly competition and last decade real estate didn’t create return. I see coming decade too situation wont change. Some pocket in india may show grow but overall will be -ve. Until earning and job growth happen real estate sector wont boom.

Hester bio science: constantly promoter disappoint in number and they struggling to grow number. They involve in animal pharma side, Any moat do they have on this specialization?

Also if we see many company last decade , (delta corp,sandhur manganest…etc)even last 5 years-decade they haven’t able to show /generate return sharevalue wise vs sales-profit growth wise. Any specific reason why we have selected ? . TCNS posting very bad result (-ve profit)and borrowing incraesed too recently . How they can pay back ? if they post -ve profit.

Why Airtel and Tata communication? why two in similar business that too they facing brutal competition.

PSU oil company itself trade at single PE. How Hindustan Oil exploration,oil business is boom?.Do they have any moat or advantage

P.S i see some business may not able to turn around due to this covid and many small cap may value eroded due to interest/debtissue/competition/other factors. if we dont know the business in & out and we may eventually lose the value.

There were a few reasons why I picked auto ancs over auto OEMs:

Auto Ancilliary valuations were even more attractive than OEMs

In the case of Minda Corp, there was a huge tailwind with BSVI 2-Ws which would lead to nearly doubling of wire-harness content per vehicle overnight as soon as BSVI norms kicked in. This alongside the closure of the loss making unit made this a very attractive proposition at the time (and I believe it still is today).

Wanted to play CV cycle but not through Ashok Leyland as was a bit concerned about ICDs and merger of Hindustan Leyland Finance in the company.

However in hindsight, it seems like the risk-return in OEMs would be much better. I was already betting on a cyclical turnaround. To add more risk by picking small cap names was maybe unwarranted. Will evaluate once the dust settles and take away some learnings for the next cycle.

I respectfully disagree. On the ground, it seems that the time has scarcely been better for high quality real estate players. Today there is limited competition in each major market, availability of funding for smaller players is a big challenge which means they have to do JDAs with established developers for access to funding, affordability of housing has never been better due to low interest rates, govt policy incentives and time-correction in rates which is leading to explosion in sales velocity for strong developers. If one can back the right horse, real estate could potentially become the largest wealth generator of this decade.

This is a small weight for me and to be honest I need to do deeper work on this company. My understanding is that there are 2 moats here:

Technology Moat: Vaccine generation (even for animals) is a highly technical process requiring expertise and R&D spend. This acts somewhat as an entry barrier to the business.

Distribution Moat: It seems that animal vaccines are distributed through more retail routes rather than B2G. So an established distribution network, especially in rural areas would be difficult for a new entrant to replicate.

But I take your point on the promoter, he has a tendency to overpromise and underdeliver. A lot now rides on the Africa expansion and its success.

This is exactly the reason why most of these have been selected. Even though they havent delivered value for shareholders, business performance for most of these companies have been good. Sandur has grown EBITDA 2.5x since 2017 and likely to see a big jump again once the new capex cycle comes onstream. Delta Corp is faced with temporary Covid headwinds but in the meanwhile they have incubated a high quality online gaming company: Adda52 which is being significantly undervalued by the market in my opinion. VIP, TCNS as well in my opinion are facing temporary headwinds due to Covid but the long term story seems intact. All have strong balance sheets, so in my view there is no bankruptcy risk. It is just a case of being patient and letting the Covid headwinds recede.

To be honest, a few years ago, I would never have touched telecom with a 10 foot pole. However, it does seem now that most of the competitive headwinds have receded. Industry has consolidated from 11 players to 2.5 and the price war is definitively over. We are likely to now enter a cycle of price hikes over the next 3-4 years. It is an inflection point of sorts. Tata Comm is a different story. It is mainly in the enterprise connectivity space where products are sticky. With corporates technology needs changing: more proactive risk management, work from home architecture, cloud computing; Tata Comm should be one of the biggest beneficiaries.

HOEC is a short-term bet. I bought when Oil price was <$20. The thesis was 3 fold:

Oil at $20 is unsustainable. Many macro factors exist which will force oil back to a 50-60$ equillibrium over the medium term.

The commissioning of the new B-80 Block would lead to a 3x increase in the company’s profitability. Market was not pricing this in at all.

HIgh quality management with demonstrated good execution capabilities.

This company should look different starting Q1 of next year once the new block is commissioned.

Few changes made to the PF in the last month. Surprisingly, opportunities have still been reasonably easy to find even though the market is at all time highs, albeit not as easy as it was a few months back:

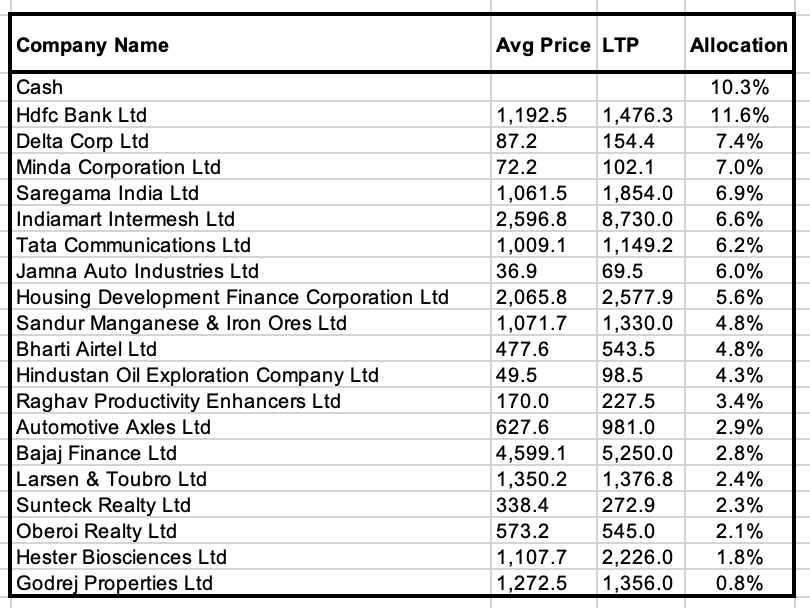

Some shifting of PF weights. Sold out of Nesco and reallocated to Sunteck and Oberoi. Also added little bit in HDFC Ltd and HDFC Bank when the markets corrected. Think the potential of gains is more in aggressive real estate developers who are looking to expand their project portfolio today as opposed to passive players like Nesco. I am also unsure of the trajectory of commercial real estate.

Added Saregama Ltd. Really like the B2B music licensing story. Company has managed to grow B2B music business from ~60 cr in FY16 (excluding telecom revenue) to ~240 cr in FY20 on the back of: 1) Rapid digitisation of music listening in the form of audio streaming apps such as Gaana/Saavn, etc which are helping expand the size of the market & 2) Finding new use cases for the music library: Social Media, Video Streaming, Short-Format Video Apps, etc. Furthermore, the company has managed to do this while not investing much in new content and riding the old retro music library. I feel music streaming is a structural growth story in India which can grow for possibly a decade more given that the paid music subscription penetration is hardly ~1%. Company will also be using cash flows from its back catalogue to acquire fresh content, thereby continuing to gain market share going forward. At the same time, as smartphone penetration increases and more users come online and download music streaming apps, piracy will go down and the latent value of Saregama’s back catalogue, which is completely written off from the books, will get unlocked even more. I expect this business to compound earnings at 20%+ rate for the next 10 years at the least (from next year’s base). As long as fresh content is acquired at an incremental ROIC of 20+% (biggest risk to thesis), the stock should compound handsomely from here. In terms of valuations; if I value Carvaan and the movie business at 0; the B2B business is trading at a FY21 EV/EBITDA of ~14x, which is a large discount to global peers who are at 20-25x; seems reasonable given the opportunity ahead. Eventually, this business should get acquired by one of the global biggies. Big risk is capital misallocation; it is an RPG group company.

Other Thoughts and Watchlist:

As the markets rally and the equity portfolio grows in size, the cash allocation has automatically come down even more. Still trying to formulate how to think about the cash. Two things give me comfort to deploy more as of today:

If i look at the overall portfolio; except for Indiamart, I still think most of the other names are not overpriced. In fact I would be happy to deploy more capital incrementally to all the other names in the portfolio even today.

I continue to find (what I think are) mispriced opportunities such as Saregama, Oberoi, Sunteck, etc even today.

I have changed my thinking a bit on the cash as compared to before. Instead of holding on to cash, I am happy to deploy so long as these opportunities are available.

Watchlist:

Will probably take portfolio weight in Saregama upto 5-6%. It seems to be a rare asset that has a long runway of growth available at reasonable valuations.

Post the correction in some of the pharma names, also plan to do more work on Marksans, Ipca & Abbott.

Also plan to study logistics companies: Blue Dart, TCI Express. THey will likely be big beneficiaries of a cyclical growth recovery.

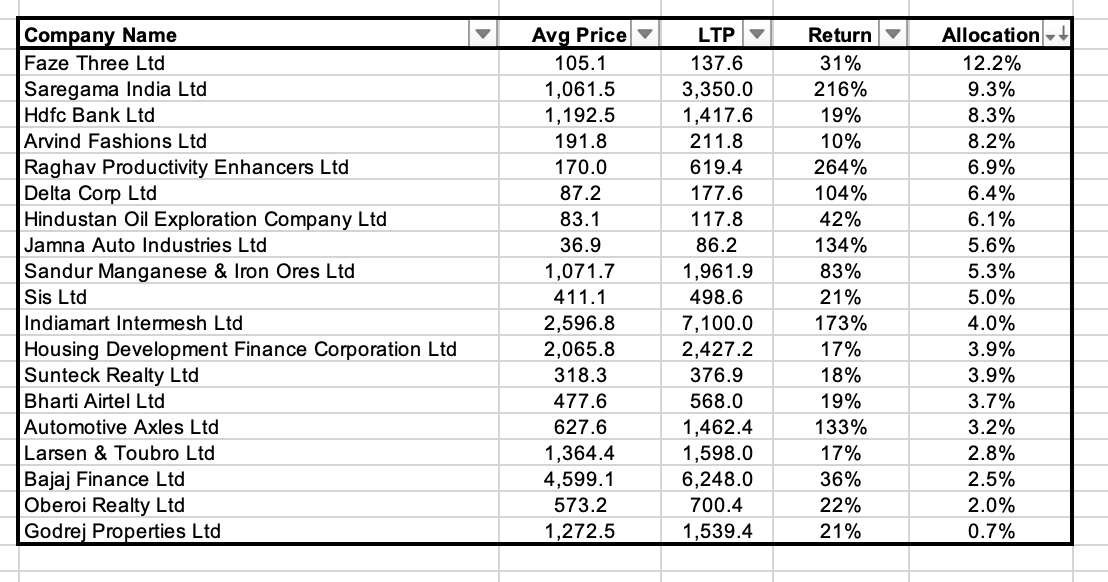

Few more changes made in the last month and a half and 1 new name added. Portfolio is chugging along, and some new bets such as Sandur and Saregama are starting to pay off:

Added Raghav Productivity Enhancers. This is a 200 cr micro-cap company involved in the manufacture of Silica Ramming Mass which largely goes into the induction furnace for the steel industry. While the product is quite commoditized in nature, the company is a leader having a 15-20% market share in the domestic market. The company has 3 moats:

a) Access to the highest quality RM in the world with plant near Rajasthan quartz mines

b) Cost of production advantage due to scale

c) Organized and High Quality Management: a big advantage in such an unorganized industry. This has allowed them to invest in talent especially in the Sales & Marketing, and technical and R&D side. Thereby the company is continually gaining share; and doing so selling its ramming mass at a premium to the market.

The company has recently done a QIP to double its manufacturing capacity. Large marquee investors such as Utpal Sheth and Ramesh Damani participated; Utpal Sheth also sits on the board. Expect the company to continue gaining market share in the ramming mass market from its unorganized peers. In addition, expect export share to increase which will be margin enhancing. Going forward, we also have optionality of company getting into allied lines such as ramming mass for the foundary market or ceramics market; where realizations are even better. EBITDA has been growing at ~25%/year till FY20 for the last 3 years at a ROCE of 30+%. Expect this to continue going forward led by the new capacity enhancement. At a PE of ~20x, the company still looks reasonably valued.

Increased weight in Saregama as expected. Also picked up some Tata Communications in the govt OFS. Took advantage of market drops to add small weight in Jamna Auto, Auto Axles , Sunteck and Airtel.

Exited both VIP Industries and TCNS. The second Covid wave is a big hit to the growth prospects. Too many risks at these valuations to justify holding both these names. At the same time, was willing to hold Delta Corp for 2 reasons: 1) According to recent concalls, it has shown that it can get back to its old revenue run-rate at even just 50% capacity by changing its customer mix. 2) Any second wave will bring fresh tailwinds to online gaming.

Watchlist:

Too many companies in the watchlist now where work needs to be done. Aside from Pharma, have been spending some time trying to understand the IT sector. Also plan to look at CGD companies and 3-4 other smaller companies such as Jash Engineering, Praj, Cesc Ventures, SIS.

The sales in TCNS and VIP have again brought cash levels up to decent levels whereby if there is any panic due to second wave, I can deploy fresh capital.

Decent amount of activity done over the past few weeks. Was able to deploy some capital in the market fall. 3 new entrants into the PF!

Added Bajaj Finance: Best in class retail franchise NBFC; the company has a massive customer acquisition advantage over peers due to retail and now digital touchpoints as well as 0 EMI product. It is very smartly able to pick credit-worthy individuals from that basket and cross-sell them multiple products. The last 12 months was a huge vindication of its business model and under-writing quality as Gross NPAs were maintained at very reasonable levels. With a customer franchise approaching just 50 million, the potential for growth here is still massive. Picked it up at 7.4x P/B which while expensive isnt unreasonably so for a company expected to grow at 25% YoY with a ROE of 20%+ over the next decade. The only regret is that I wasnt able to stick a higher weight to the name; would have liked to allocate 5% of the PF at 4500 but the pullback was too sharp and thus got stuck at 2.5%. Will probably have to wait for another shock to get another good buying opportunity here.

Added Larsen and Toubro Ltd: Another contrarian pick. The company hasnt delivered much shareholder value over the last 10 years; but in the meanwhile has incubated/invested in 3 quality IT businesses (LTI, LTTS, Mindtree) which together with L&TF account for about half the current market cap. It has made some poor investments in asset heavy projects - Hyderabad Metro, PDL and IDPL which are pulling company ROCEs down. Management has stated their intent to now only focus on the asset-light business and stop acquiring heavy investment infra projects The core EPC business has actually done decently over the last decade growing revenues at 10% and profits at 8%. In addition, it is asset light; and turns the large WC investment 3x per year at 8-10% margins, so 25-30% ROCEs should be possible . Furthermore, the govts infra push as well as L&Ts order pipeline offer good visibility on growth; the order book has grown 10% in the 9 months FY21 and will probably end the year 15% up. Receivables tend to be a concern, but if you look at this business from 5 year periods, it is able to convert all its earnings into cash. In some ways, the best time to buy this business is times like today when the receivables cycle is elevated; so that normalization of that cycle can give a cash boost. Today this business is available at ~13x FY 22 Earning; ludicrously cheap given its leadership position, resilience in this segment and strong growth visibility. In addition, we also get to play the IT cycle which has some tailwinds over the next 3-4 years. Happy to take weight in this to 5% over next week or 2.

Added Godrej Properties: making a basket of real estate developers. Dont know enough about the segment to take a concentrated bet on one name. Godrej is the largest and the most diversified in terms of geographies and is rapidly expanding its area under development. Bound to do well if the cycle turns in a couple years. Happy to bet as much as on the other 2 names on this one.

Hiked stake in HDFC Bank at 1380 levels. Dont see any risks to asset quality.

Lots of more churn and additions over the past couple of months. In general, the churn level has been far higher than I would like; and I will analyze the sell decisions made over the last 10 months in the next post.

Fair amount of weight shifting, 2 new additions and 2 sales from the PF:

Sold Minda Corp: Sold despite the fact that the story largely is playing out. Content increase in BSVI wire harness clearly being seen in revenue growth numbers which were among the best in industry. As the margins catch up to BSIV, company should be on track to do ~250 cr of PAT on 2019 volumes. I am comfortable to give a 15x PE multiple; which implies a 3750-4000 cr valuation in FY23 which is when i expect the industry to get back to FY19 volumes. I sold at 135-140/share which is when the market cap was already ~3300 cr implying very little upside left.

Sold Tata Communications: was disappointed with management commentary in the analyst day. They were guiding for double digit data revenue growth with margins remaining in the same ballpark for the medium term. This is despite their addrressable market going up multifold with Internet WAN opportunity opening up globally. That basically implies a <10% EBITDA growth in the medium term once you take voice decline into account. Not good enough in my opinion and the price had also run up to 1300 levels. Will keep monitoring this for a growth uptick.

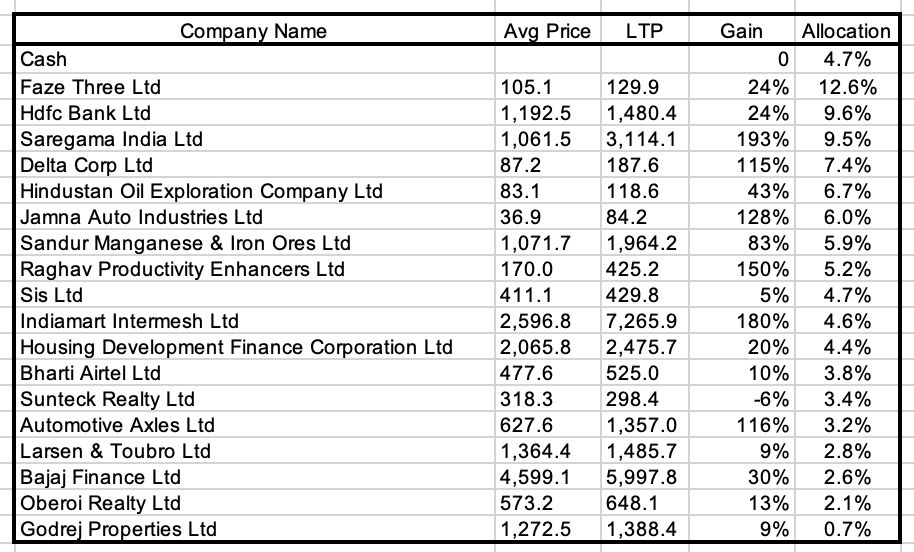

Added Faze Three Ltd: Came in with the highest PF weight here. Company is right in the middle of my circle of competence with mouth-watering growth potential at high incremental ROCEs. They are a manufacturer of home textiles (primarily bath rugs and area rugs). I feel there is potential for an aggressive market share shift to India here from China with a) 25% incremental duties levied by Trump administration on Chinese imports making Indian products competitive & 2) Buyers looking to diversify sourcing from China (China + 1). The growth from Q2-Q4 FY21 is there for all to see and mgmt in Q4 commentary is guiding for 20% PAT growth from that base with a potential for positive surprise. This can be a multi-year growth story which was picked up at ~10x FY21 PAT. If this story plays out, this can be a potential multi-bagger with high earnings growth as well as potential re-rating to 15-20x.

Added SIS with a 5% weight. This is a traditional security staffing and facility management business with operations in India and Australia. The domestic industry itself pre-Covid has been growing at 13-14%. SIS being the second largest player only had 4% market share showing the growth potential here. I am very comfortably able to underwrite 20% organic earnings growth here (in the domestic market) from FY23 onwards till FY30. The business only requires Working capital really to grow. It moves the WC 6 times a year at ~6% margins implying a 35% core incremental ROCE. Large organised players such as SIS have a massive competitive advantage with regard to HR compliance and use tech/software to manage their business and receivables. There is also some degree of operating leverage that is gained with scale; the leader in the security business makes 7% margins whereas 5.5-6% for SIS. Furthermore, we also have optionality with the cash with regard to acqusitions. Company has a good track record of buying smaller players, enabling them with SIS’s tech processes, and accelerating growth and margins as seen in the case of DTSS. Company looks highly undervalued. The current M.Cap in my opinion doesnt even discount the domestic business fully let alone the international business. Large margin of safety here. Valuation of other staffing companies: Quess, Teamlease is also a sanity check. They trade at 50x earnings whereas SIS is at 20x despite having a better growth profile as well as better ROCEs.

Also added weights to Sunteck at ~285/share and HOEC at ~115/share. Sunteck is a long term play on the RE cycle; while HOEC is currently a mouth watering play on the potential of the B-80 block and current oil prices.

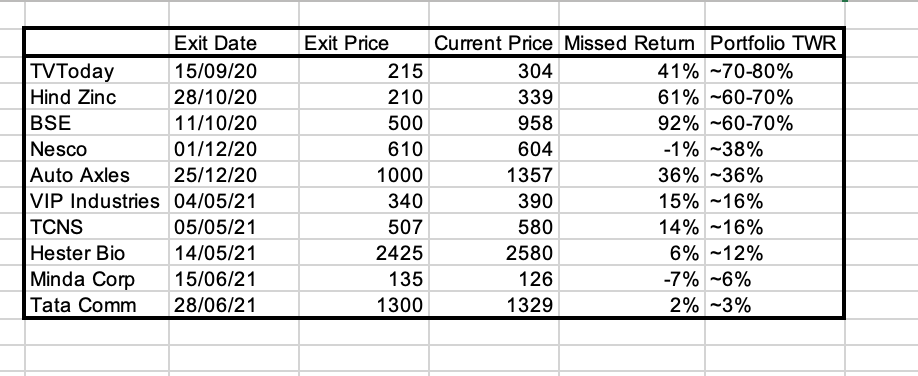

Methodology Used:

Compared the missed return from the stock sale to the Time weighted PF return from the sale date. Essentially trying to analyze if the stocks would have underperformed or overperformed the PF had I kept them. Obviously this isnt the best way to analyze and I would have much rather analyzed what I allocated capital to with the proceeds and how those stocks did in comparison to the stocks I sold. However, that is hard to do given that there was also cash in the portfolio that got wound down. The online portfolio tracker I use already gives me Time weighted returns for 1 week, 1 month, 3 months, 6 months and 1 year so I just used that data with some approximations to estimate returns from the sell dates.

Most of the time I sold, there was still value on the table. Most of the stocks had postive returns after I sold them.

My sell decisions were average. Most of the time, the stocks I sold did as well as the PF at large. In some cases such as BSE the stock did much better. The only sell call which was actually undoubtedly correct was Nesco.

It does seem that I was able to redeploy the money from the sales however at a similar rate of return. However, cannot rely on doing this forever; there is definitely a need to be more patient with the initial stock selection.

Give the magnitude of the returns made over the past 12 months, by far the biggest mistake made in the portfolio was holding cash. With the initial sales, there was still cash left to be deployed. Rather than selling, I could have kept them and added incremental money subsequently.

This realization partially reflects in subsequent cash allocation which has been wound down significantly. Intead of ‘timing’ the market, I now am happy to allocate money wherever I can see 20%+ returns while mantaining quality, growth and ROCE filters. The Sell decisions will now have to satisfy one of the following criteria:

As long as cash is available to deploy; expected returns from the stock need to be <10% over a 3 year time horizon

If there is no cash left to deploy, happy to sell where i can with reasonable confidence see better returns in a new pick. However, I will not pre-emptively go to cash like last year when there are opportunities available.

Thesis breaking information/development or sustained poor performance for an extended duration

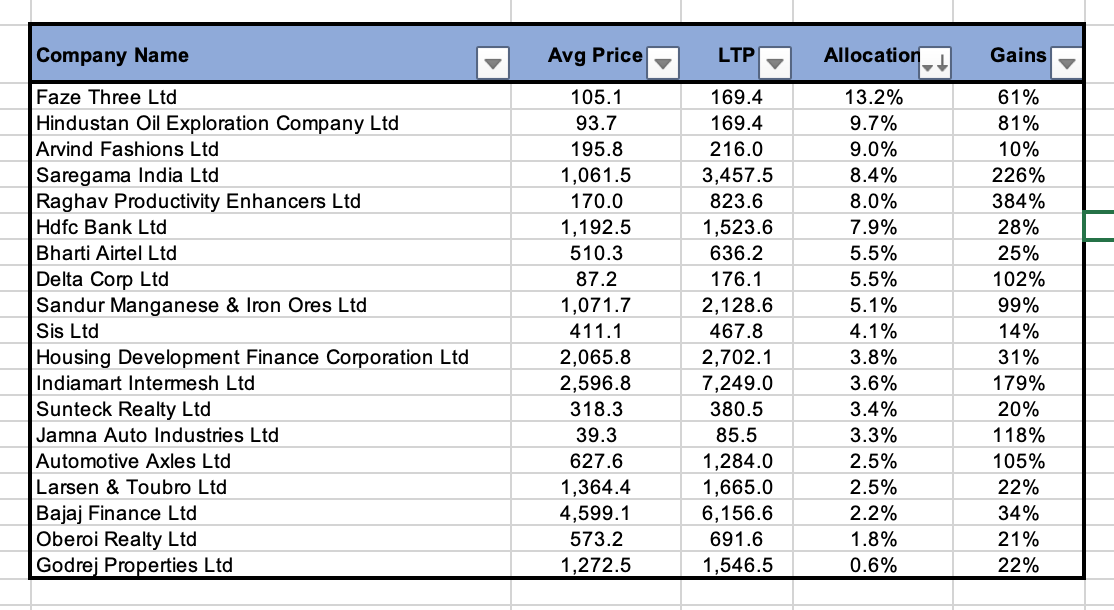

Its been a good month for the portfolio overall with the newer bets like SIS and Faze Three doing well. Raghav Productivity has re-rated significantly and now up >50% in the last month. Valuations are frothy here. Real-estate bets have also done well with the overall developer basket up ~20% over the last month. Rest of the pf has largely remained where it was last month. All stocks in the green now; such performance is unlikely to be repeated going forward. 1 new entrant in the PF:

Added Arvind Fashions Ltd. I have been following this group for a while. I have noticed that Management here is really bipolar: completely inept and wild when times are good. We have seen this in the early part of the last decade and again from 2016-19. This inevitably leads to periods of high stress such as 2008-10 and today. In these times, management has been amazing; made all the right decisions and made the organization leaner and focussed. I see this playing out again in Arvind Fashions. A lot of the tail brands have been discontinued/in the process of being discontinued and management is focussing now on just 6 brands. I was very pleasantly surprised to see Unlimited also being sold to VMart last week which made me initiate the position. The valuations are reflecting 2 years of intense pain; most investors have written off the management and the company. If we take just US-Polo; that is a 1000 cr revenue brand. Given that management sold a stake in Flying Machine (a much smaller/weaker brand) last year at a 1000 cr valuation; it would not be unreasonable to posit that the fair market value of US-Polo brand is greater than the market cap of the entire company today. The fact that promoters are also regularly putting money into the company in rights issues also provides comfort that the risk of bankruptcy is low. Initiated an 8% position here; and there is no reason why it couldnt be higher.

Q1 Results for all PF companies have now been released. All-in-all I would say they were much better than expected given the Covid issues. Going to give quick feedback and thoughts:

Faze Three: Stunning results. 8 cr PAT ex of one-off exceptional gain. This was without any govt incentives which should be announced any day now. Even with 2% RODTEP rates, company is tracking a run rate of 10 cr PAT per quarter. Mgmt Guidance has been increased and company is hoping to double revenues by FY24. Company still looks very cheap.

Saregama: growth trajectory for B2B licensing continues. EBITDA increasing QoQ and doubled YoY. However, this is not the right base for EBITDA since company is not incurring any expenses for new content. Will be interesting to see how dilutive new music acquisition will be to earnings.

HDFC Bank: Rolls Royce bank; best in class earnings quality continues. 2.8% slippages (annualised) which was the best of any private bank. Retail growth has slowed down but expect this to pick up as economy starts reopening.

Arvind Fashions: Painful quarter, large loss delivered as expected due to Covid. Once Gap is closed down we will be back to 6 core brands. These brands delivered 300+ cr of EBITDA (post rental expense) in FY19 with 20% ROCE. The hope is that we get back to those kind of numbers as the Covid threat recedes. Expect next couple of quarters to still be loss at EBITDA level (post rental) as GAP shutdown costs start coming in.

Raghav Productivity: result as per expectations; 4 cr quarterly PAT run rate maintained in a tough environment. RJ coming in was a surprise and while I think the stock is very expensive; feel fair value is somewhere close to RJ buy price. However, company has a long growth run way so will wait it out and see how they progress. Expect a 30-40% stock price decline from here.

Delta Corp: Disappointing results. Casino performance was expected due to Covid but surprised to see online performance being so bad. Online now at FY20 revenue levels. Waiting for some more mgmt commentary to explain this.

7)HOEC: results dont matter for the next couple quarters. Only thing that matters is oil price and how quickly they can get B-80 online. Even at $60 oil price; company could do ~500 cr CFO once B-80 comes online. Stock could still be a doubler from here.

Jamna & Automotive Axles: Slow quarter as expected. MHCV sales were down 50% this quarter compared to Q4. However heartening to see the EBITDA margin performance of both companies. Jamna especially delivered a stunning 12% margin which was not far off last peak cycle margins. Shows the work done in cost control and in the upcycle expect margins to hit 17-18% this time.

Sandur Manganese: 260 cr Q1Fy22 EBITDA, 2000 cr Enterprise Value: Just wow. 85% QoQ growth in EBITDA. Everything has come together: commodity price inflation + earnings from new capex coming online. This is likely the peak earnings of the company for the next many years so a decision needs to be made here.

SIS: Resilience of the company on show. QoQ revenue and EBITDA decline was mantained to low single digit rates, very impressive. Expect this company to be a big beneficiary of economy reopening and people going back to work. The I-T dept enquiry on Quess Corp for Section JJAA tax benefit is a key monitorable. This is likely to become a industry issue and could have big ramifications for intrinsic value if goes against the company (20% impact to intrinsic value as per my calculations).

Indiamart: Again a much better showing as compared to lockdown quarter last year. Absolute Subscriber churn was mantained at low single digit. But we need to start seeing rapid subscriber additions going forward to justify valuations.

HDFC Ltd: Impressive performance compared to other HFCs. Asset quality outperformance continues. Think the company is overprovisioned as it stands and we should start seeing some unwinding of provisions in the second half of the year. Further have high growth visibility; July disbursements were third highest ever. We may be at the start of a structural upcycle in residential real estate which would mean high growth for 5-6 years from here.

Real Estate Devlopers: Oberoi, Sunteck & Godrej: Slow quarter as expected. Pre-Sales were down >50%. THis was expected as the stamp duty benefits receded and Covid second wave. However, commentary from all 3 companies was good with regard to demand in Q2. There was even some talk of price increases. If we are in a structural upcycle, still believe developers will be the greatest beneficiaries.

Bharti: 5% QoQ increase in EBITDA mainly due to Airtel Africa. Good to see that India mobile business absolute subscriber numbers were mantained despite Covid second wave (though company is losing market share to Jio). Company has started to take selective price increases in certain plans. Story is playing out here perfectly. Company is a big beneficiary of Vi situation and faced with a win-win situation. Either they gain more subscribers as Vi’s financial distress continues or tariffs go up substantially. 5G capex and spectrum auction is a big monitorable here.

L&T: disappointing quarter. execution as well as order wins impacted by second wave.

Bajaj Finance: while numbers in terms of customer acquisitions look good, loan growth has slowed down considerably and asset quality also seeing some stress. Market doesnt seem to care and stock continues to get re-rated.

Managed to keep my cool during the small meltdown in small caps this week; however, wasnt able to add to positions. Portfolio has fully recovered from the short correction. Had added weight in Bharti Airtel leading to Q1 results @ about 570/share and Arvind Fashions @ 213/share. On the flipside, reduced some weight in Jamna Auto @86 levels. This was just because the risk-reward in other names looked better.

If you see the tax rate of the company (the Indian entity), except for the last couple of years, it has been very low (single digit tax rate). This is because the Indian entity gets tax breaks from Section 80JJAA of the income tax code. Section 80JJAA states that the company will get a 30% tax deduction for 3 years on any additional employees hired by the company; as long as their monthly salary is <Rs 25000.

See link below to understand more:

There were certain news articles recently that the IT-Dept is going after Quess Corp for concealment of income of 880 cr relating to Sec 80JJAA. As per my understanding, there were 3 issues:

I-T department claims the benefit can’t be claimed if the employee leaves after 1 year and has to stay at the company for 3 years in order to receive the Sec 80JJAA tax benefit. This is very rare in staffing companies due to high attrition. I don’t think this issue is much of a problem as there is legal precedent with the company (Page Industries case in Bengaluru earlier) stating that the employees don’t need to stay 3 years

I-T department is saying that if ANY month compensation exceeds Rs 25,000, then the company is not eligible to claim benefit for that employee. Now this is a problem since every employee gets a Diwali bonus in the month of OCt/Nov that takes that month salary above Rs 25k. Standard practice is that the companies claim benefit if the employees annual salary is <3lakh. We have to see how this plays out but common sense says that this shouldn’t be a problem.

The third issue is in the form of reimbursements. The I-T dept is claiming that reimbursements should form a part of the income; whereas Quess is saying that since reimbursement is not taxable; they shouldn’t form part of the income.

Common sense says that the I-T dept claim is quite frivolous but you never know what will happen. The same practices are followed by other companies including SIS and it stands to reason if Quess is found guilty, so will competitors.

Regarding impact on intrinsic value: in a worst case scenario; you have to assume that the Indian entity has to pay full tax rate for previous year’s income as well as for income going forward if the ruling goes against. I had foolishly assumed that tax rate will stay low for the foreseeable which seems to anyway be an aggressive assumption. After adjusting my estimates; the hit on intrinsic value is ~20% for the Indian entity. For the consol entity the hit will be lower since they are anyways paying full tax on international earnings. The good news is that even in this worst case scenario there is a margin of safety from the CMP