Another Portfolio update,

Took the market rally as an opportunity to trim down some small holdings/companies where thesis was going wrong:

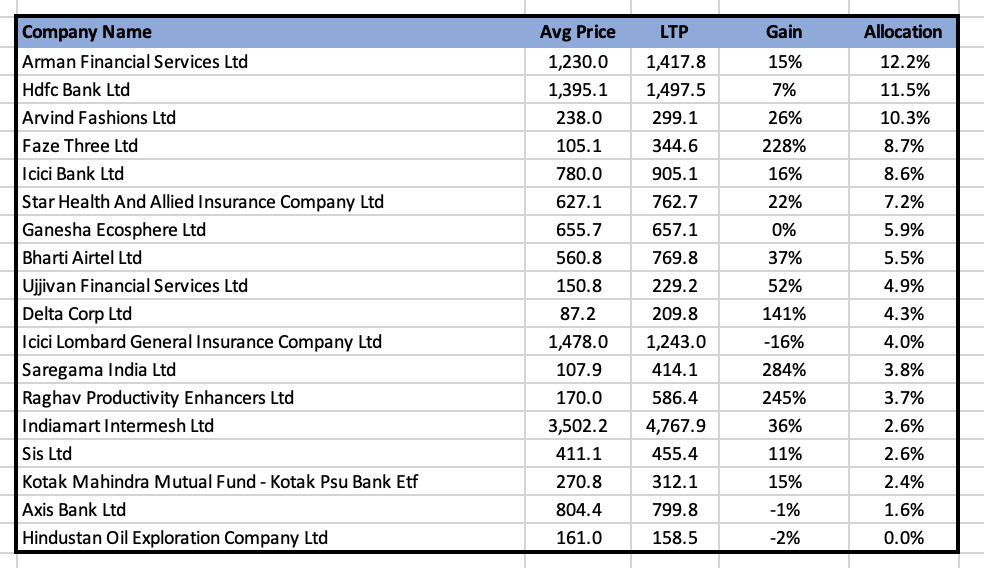

- Exited Hindustan Oil Exploration Company: Thesis gone bad. Post repeated delays, have lost faith in management’s ability to execute on the B-80 block. Poor communication with investors doesnt help. This was one of the stocks bought in the peak of Covid, and as such delivered multi-bagger returns

- Exited Manappuram Finance: Thesis gone wrong. It really hurts to sell this one at book value. I suspect returns might be decent here, however it starts looking like a value trap. High ticket size gold loan business is permanently impaired which will challenge the company’s ability to grow in the long run. I still think the company can do 16-18% ROEs, however growth is question mark. Booked a ~15% loss here. Probably will look to reallocate to Ujjivan Financial Services. Will keep tracking and re-look if there are signs of growth or reducing competitive intensity.

- Exited Bajaj Finance: rich valuations. At 10x P/B, there is limited scope to make a good return. In addition, it was a small weight. Made sense to reallocate to other names.

- Exited Sunteck Realty: thesis going wrong: In a couple of years where residential real estate sales are going through the roof, company has struggled to sell its ready inventory in BKC and meaningfully accelerate sales trajectory elsewhere. I further expect the Mumbai market to be in oversupply starting this year as mentioned above based on the advance premium collections.

- Exited Century Textiles: This one might be a bit harsh. Paper business is in an upcycle and real estate business is just being setup. Valuations too are fair. I primairly bought for real estate. However, chosing to exit and make room for other opportunities given that I dont expect Mumbai real estate to do great from here. This marks the exit from all real estate stocks. I held for much lower time than I envisaged, however nevertheless, the returns from the overall basket were pretty healthy at somewhere around 50%.

- Trimmed Faze Three: the expected returns had just started dipping post the monster rally. Took the opportunity to reduce allocation and reallocate elsewhere.

- Trimmed Saregama: valuations are steep. Expect to exit this one completely when better opportunities become avaialble. I actually think cash might even be a better opportunity. Valuation rationale is explained here: Saregama India Ltd: India’s premier music publishing label - #414 by yrm91

- Expect to add Ujjivan Financial soon. Have also taken a short-term trading bet (not discussed here). Rest is going to cash in wait for better opportunities.