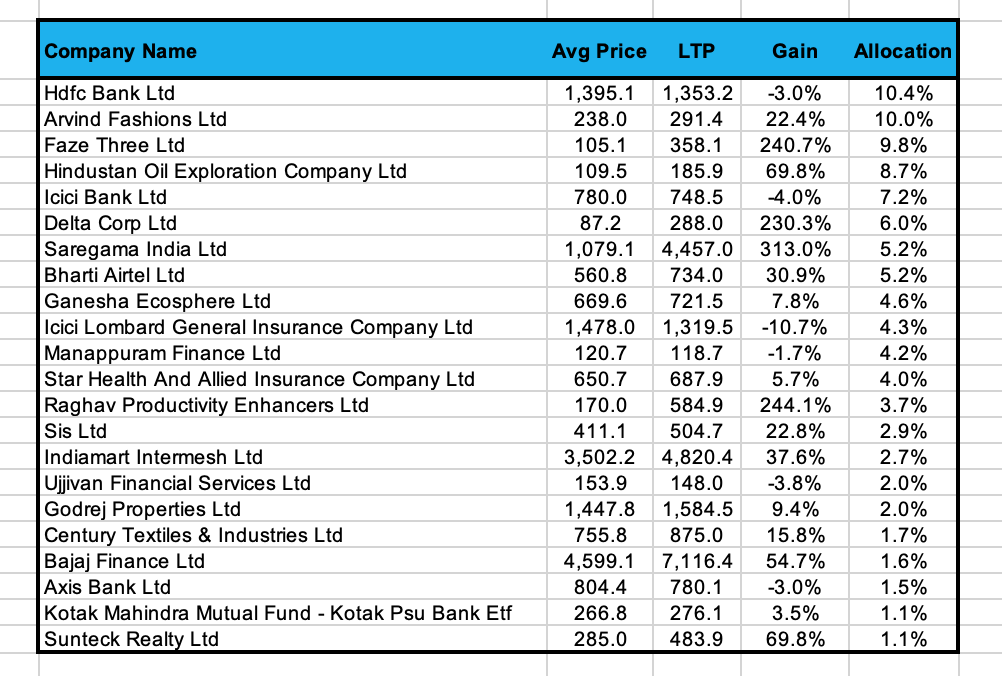

Another portfolio update. Not too much change, 1 new entrant and a couple of sells.

- Added Ujjivan Financial Services: I view this as a cyclical + special situation pick which provides decent margin of safety. UFSL is the holding company of Ujjivan SFB; one of the larger micro finance lenders in the country. In fact I would say Ujjivan is one of the worse microfinance organizations in the country going by their credit loss track record in the last 2 crisis. However, this is a deeply cyclical sector. Good times see next to no credit losses and healthy ROEs of 20%+ vs bad times see erosions of networth and even some blowups. My thesis is that we are past the worst of the Covid credit crisis and leadership crisis and good times should start next year with normalization of credit costs. Recent company and peer updates relating to collections in Q3 and Q4 backup my view. Company is now adequately provisioned with maybe a bit more provisions to be taken in Q4 related to the second restructuring done in Q1-Q2 FY22. From H2FY23, we should start seeing the full benefit of a) Book growth, b) Normalization of GNPAs and credit costs, c) recovery of NIMs as the GNPAs decline & 4) Normalization of cost to income ratio as the extra temporary collection staff are let go. Here are my (conservative) expected numbers for FY24 for Ujjivan SFB:

Book Value: FY24: ~4000 cr (2600 cr in FY22 + 600 cr QIP + 800 cr PAT FY22-24)

P/B Multiple in FY24: 2 (In FY24, company should deliver 18-20% ROE)

FY24 M.Cap: ~8000 cr

Ujjivan Financial Stake in USFB: 70% (Assuming 600 cr QIP at Rs18/share)

UFSL MCap in FY24 post reverse merger: ~5600 cr (0 holdco discount)

CMP Market Cap: 1800 cr

Potential to make 3x returns in 24 months. If we even take no rerating and P/B at 1x for USFB in FY24, IRR for UFSL comes to 25% provided the reverse merger is successful.

-

Exited Oberoi Realty: while the thesis of increase in RE demand was playing out well, came upon some data that showed the extent of premiums filed in the last 12 months when the state govt gave premiums discount. I do think most of these will come to market and thus we are likely to see supply outstripping demand in Mumbai starting next financial year.

-

Reduced Saregama: hard to justify valuations