YASH PAKKA Q3 Concall Notes: Very Ambitious - CHUK de…….Let’s C……

Q3 Investor Presentation

- Refer Investor presentation for Team/New Business Heads and Quarter Nos. - Will end up with highest numbers Next quarter and FY22.

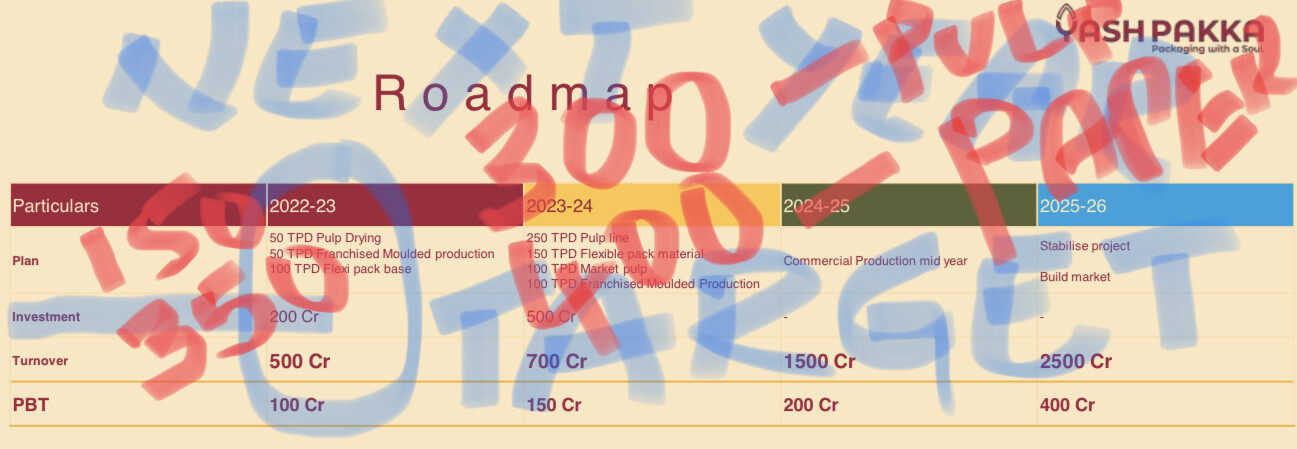

- FY 23 Sales break up Targets :

Pulp + moulded Products - 150Cr, Paper - 350 cr - FY 24 Sales break up Targets :

Pulp + moulded Products - 300Cr, Paper - 400 cr - Present Capacity Utilisation : Moulded - 58%, (Break even point is 65% for profits), Pulp+Paper-100%

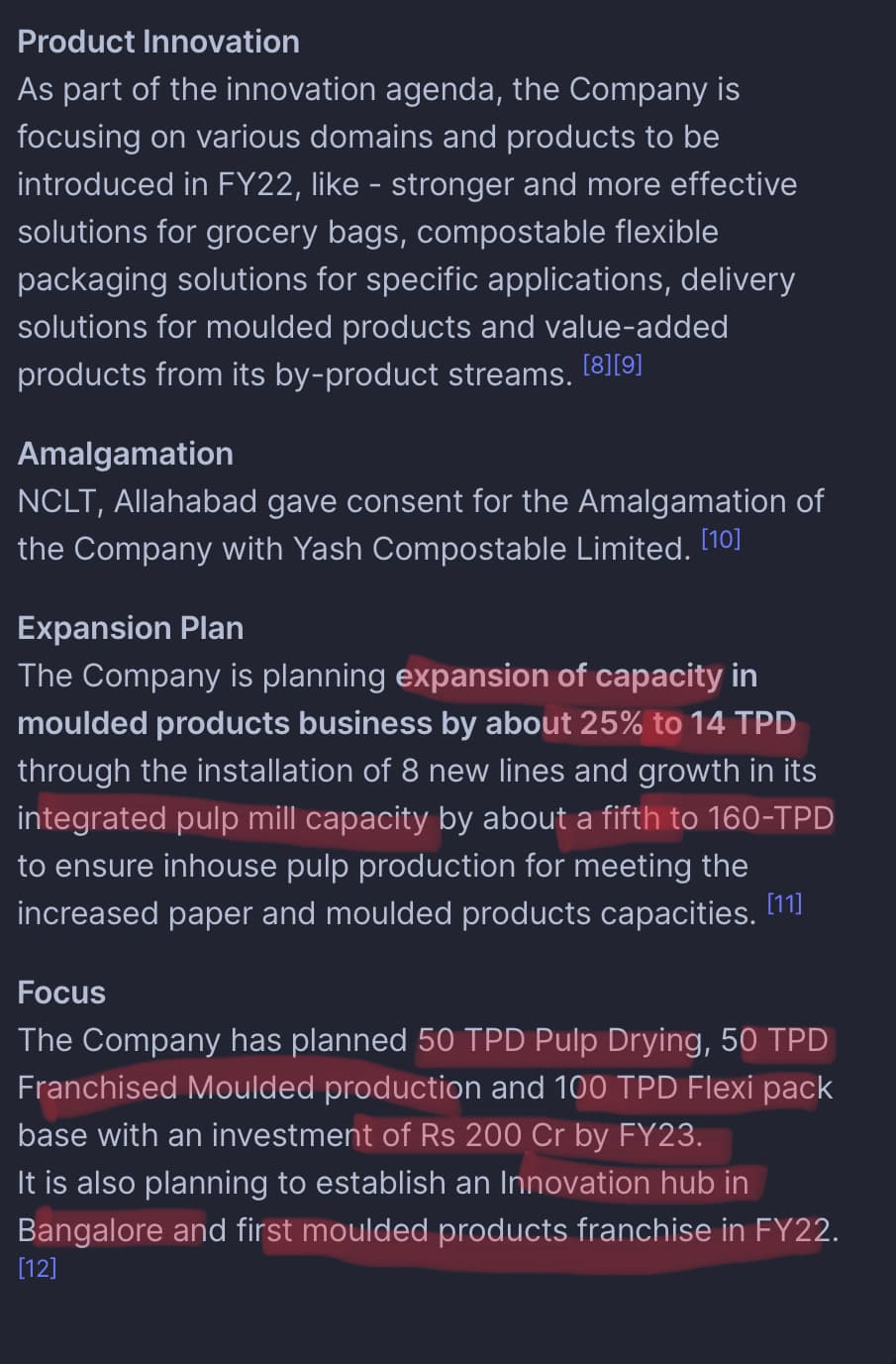

- Strategy for Moulded Products - Franchisee route: For faster growth, Supply Pulp & Moulds, and buy back finished Moulded products, Started with first Franchisee-stabilising it, In this year to go with 3 Franchisee. Design with IP registration and Tool/mould will be owned by Company, No one can/should copy Design.

- Flexible Package - Different mix of products, looking at certain specific applications, MVP’s (minimum viable product ???) under trail, to go with minimum 100MTon/month and grow month on month, partnerships done, some technical success and outsourcing manufacturing with formulations, create the base paper(others paper now, later will be done with own paper), both food and non-food usage, done successfully sachets kind of products. Now doing food contact packaging. Very buoyant about this. Doing this with Global Companies, will share after success/confirmation.

- US Market -

- Moulded Products next year, set up franchise route, exploring Mexico with partners.

- Innovation partnership with US/EURO players, Flexible package (bio mimicry???) research/exploration with US base organisations

- Set up first Pulp Mill outside India with finance options, partnerships to set 200/250 TPD baggasse Pulp unit, 3 countries in exploration.

- Technological Platform for compostable package Industry with collaboration for investors/partners with revenue generating option.

- In Study stage for Revenues - High complex market, by March will decide/finalise Strategy.

- Appointed AFRY consultant for Market study

- Funding -

- 200cr - Debt + Equity with minimum dilution,

- Next cycle Capital (500cr/700Cr) raise explore with all options but won’t dilute at these valuations, will wait for market to recognise us and see.

-

Inventory : Very High - 1.5 years, RawMaterial Bagasse - seasonal procurement - Sep to Mar, so End of March always shows High Inventory. This is used for the next whole year. March 21 have some COVID impact. But Generally will have Baggase one year (10-12 months) inventory by March end to operate for the next year. Another Raw material Husk - Around 6months inventory - This is the nature of Business.

-

CHUK - From Investor - In Calcutta Seen Everywhere, Airports, QSR’s, In all Local Markets - why? Quality and Safety, Multiple key Accounts heads setup, regional heads, Larger institutions/QSR heads setup, Distribution/sales setup. Working this setup very well.

-

CHUK Competition : Zume, Ecoware. Price vs Utility - Zume is Higher and foreign brand, CHUK is Local brand, Premiumness, value, safety and affordable. Zume is premium product with Higher price point. Ecoware is great looking products, cheaper but CHUK beat handsomely in performance in Market. CHUK is priced between ZUME & Ecoware. Newer capacities are strategically placed to go wider and deeper. Next quarter planning - meals trays rolled out for delivery. Innovative products in lineup with customer feedback, safety, thinner and strong products in lineup based market wants/needs.

-

Future funding how?? - can see Sustainability/ESG funding is real and Huge Change happening. Company future plans/funding are still low in comparison with - Smaller US company - Footprint??? - Half of our size raised 1.6Billion USD. Funding should not be problem once we start delivering our promises. Once present 200cr expansion done, results/rewards are seen then lot of options to raise capital. Observation : Tone is confident this time.

-

Startup setup Culture is been followed in the organisation.

-

Current Debt including working capital - 80Cr, majority of this taken for Tableware Project from 2018, will be repaid in future, on the path to streamline our debt portfolio.

-

CHUK capacities- Present 14TPD, Planning to go 50TPD to 100TDP by Franchise root.

-

CHUK - Key is Scale and Size ( Decided to go by Franchise root), Our focus is investing/growing in Pulping.

-

Will Produce only very very High grade Paper above 150Rs/kg for Packaging.

-

Going with Apple Business Model, OEM model also being exploring. Idea to do at scale and size not small boutique route.

-

CHUK Challenges - Only around 8Cr per Quarter after 3 years ?? Machine Setup/Capacity Utilisation/Market Challenges with COVID. Over come all. Capacity utilisation to be 80% next 2 quarters.

-

CHUK partnered with Blinket in this Quarter, and in Talks with Zomota for potential Partnerships with Restaurants. Very buoyant in this space.

Yash Pakka’s CHUK brand enters partnership with Blinkit | PrintWeekIndia -

CHUK - From Investor - Seen everywhere, not only in QSR, even in Dhabas.

-

Sponsoring a conference in LONDON - For Rethinking Materials, to build Global think tank. Biology and Technology/ Global Compostable Packaging ………….

-

ESOPs/Equity - new Scheme is TeamSOPs in planning for the Team.

-

Raw Material Availability/Pricing for Bagasse- Power companies in plan to produce Ethonal/Power ??? - Have strong Longterm Relationship with near by Sugar Mills and exploring new partnerships. Bagasse won’t be converted into Ethonal, is only used as fuel to produce Ethonal, presently not big challenge. Stay competitive for procurement.

-

IRCTC - Not much supply now, complex structure, but open/exploring for major supply once IRCTC in full running.

-

Might have missed some points - So Take with some sugar and Salt.

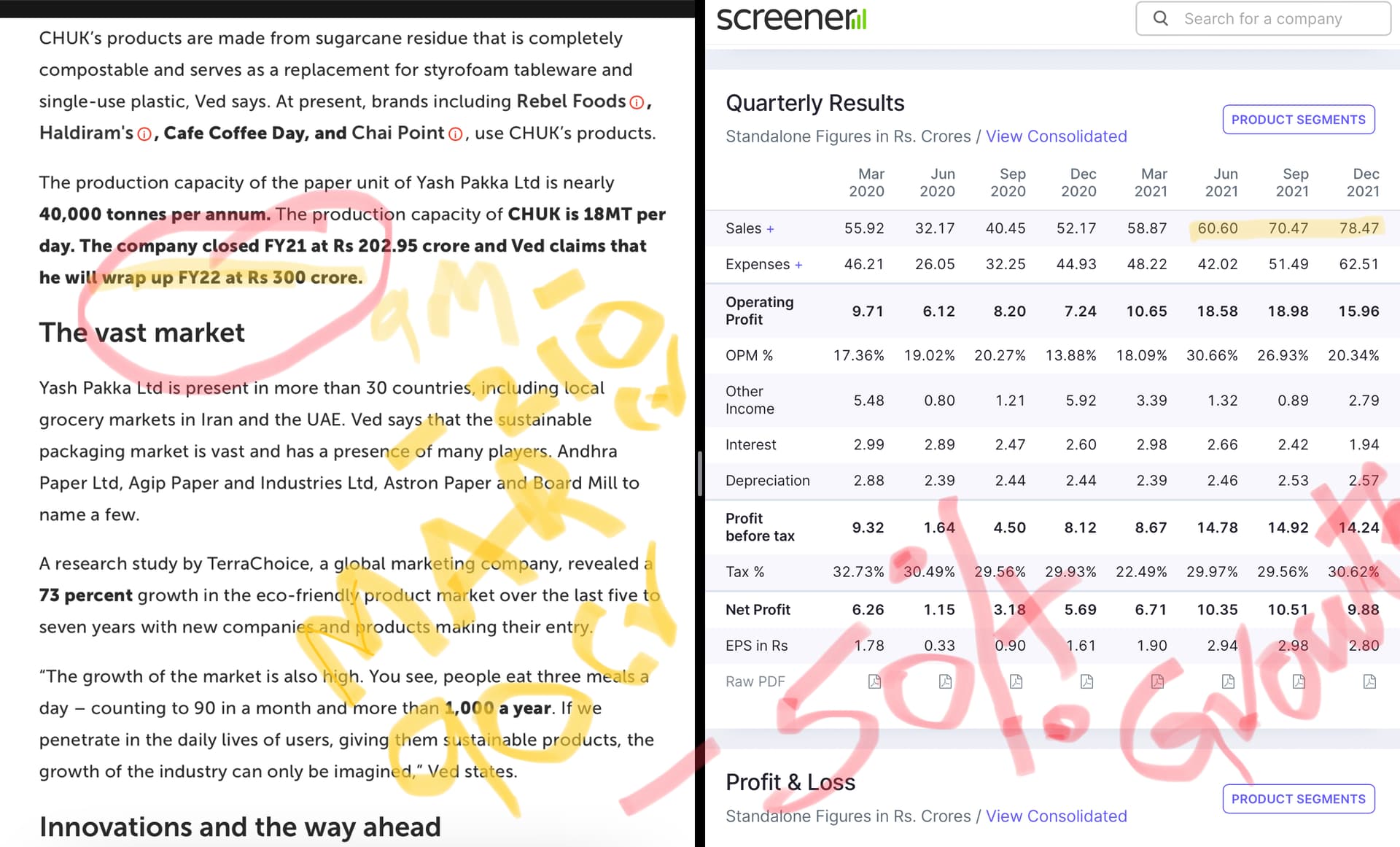

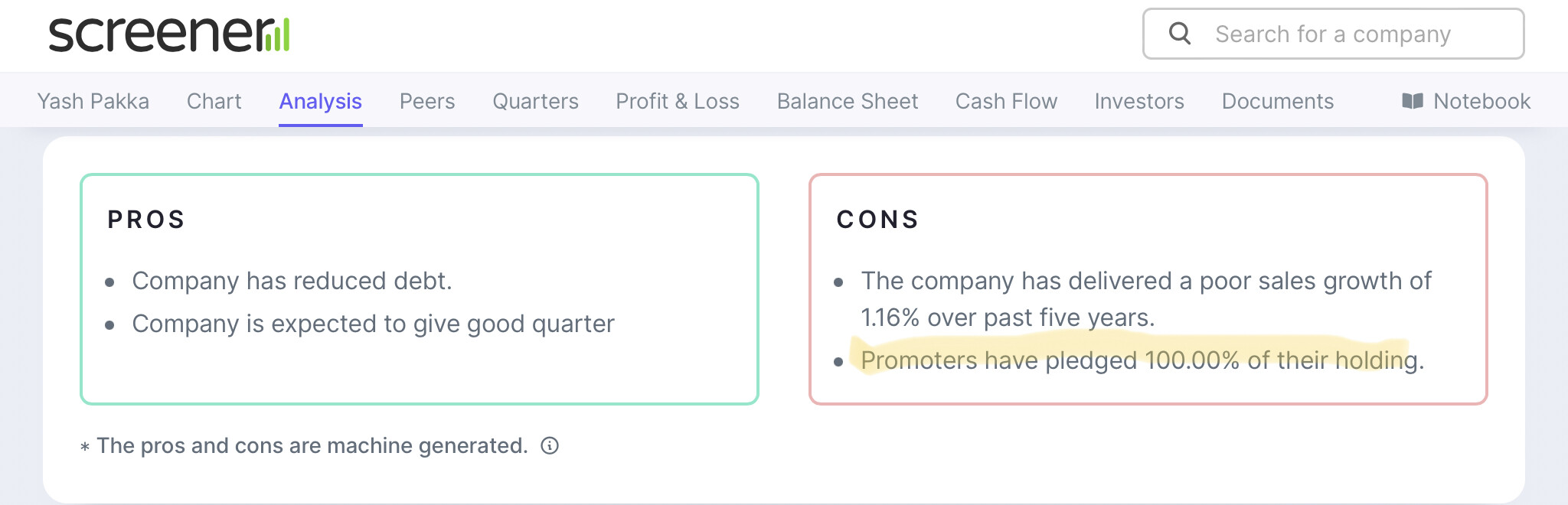

From Screener.in

From Q3 Investor Presntation:

From above Interview:

How CHUK was created:

Refer Satia Industries thread for Paper Industry and Tailwinds:

Risks:

Disclosure - Invested, Transactions in Last 15 days.

Not SEBI Registered. Read/Understand/Invest at your own Risk.