This is my first post reviewing a company so please be gentle in your criticism. Having said that, all feedback is welcome to make this post better.

1/ Yash Optics & Lens: Company Overview

-

Established in the year 2010, it provides wide array o-f vision correction solutions. Primarily engaged in the business of manufacturing, trading, distribution and supplying of comprehensive range of spectacle/optical lenses.

-

Offers from single vision lenses to advanced progressive lenses, customized progressive lenses to personalized progressives for professionals along with wide range of coatings.

-

Products are available across the entire range of price points enabling us to serve the entire gamut of customers from economy to the luxury segment.

-

Company manufactures the lenses based on order and prescription received from the customers. Under the trading space, the company sources the spectacle/optical lenses and market the same under its own brands for further sale through distributors and its own retail channels.

-

Yash has been appointed by HOYA Lens India Private Limited, as an exclusive distributor to sell, market and distribute the “Pentax” brand of Ophthalmic lenses in India pursuant to agreement dated October 01, 2022 as per the terms and condition laid down in the said agreement.

-

The principal raw materials required for the manufacturing process includes semi -finished ophthalmic (CR-39) lenses, plastic plain/ blank lenses etc. The company maintains a base of reliable material suppliers who consistently provide materials of appropriate dimensions as per our requirements. Raw materials are majorly procured in the international market from China, Germany, Japan, South Korea, USA etc and in the domestic market from Maharashtra, Telangana Rajasthan, Karnataka and Delhi.

-

Raw material Purchase Bifurcations – almost 70% raw material is imported and the rest domestically sourced (see table below; source DRHP)

-

Promoters are Mr. Tarun Manharlal Doshi, Mr. Dharmendra M Doshi and Mr. Chirag Manharlal Doshi who are related to each other.

-

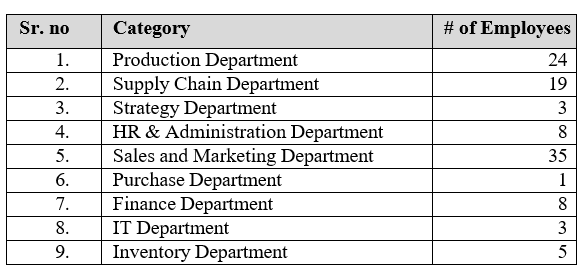

106 employees as of Dec’2023

-

Company follows B2B and B2C models. Whereas in B2B model, they sell products to distributor for further sale and under B2C, they products directly to opticians, directly through their branch offices or sale depot.

-

Customer concentration:

-

Revenue bifurcations from manufacturing and trading activities are as follows – almost a 70:30 split between manufacturing and trading

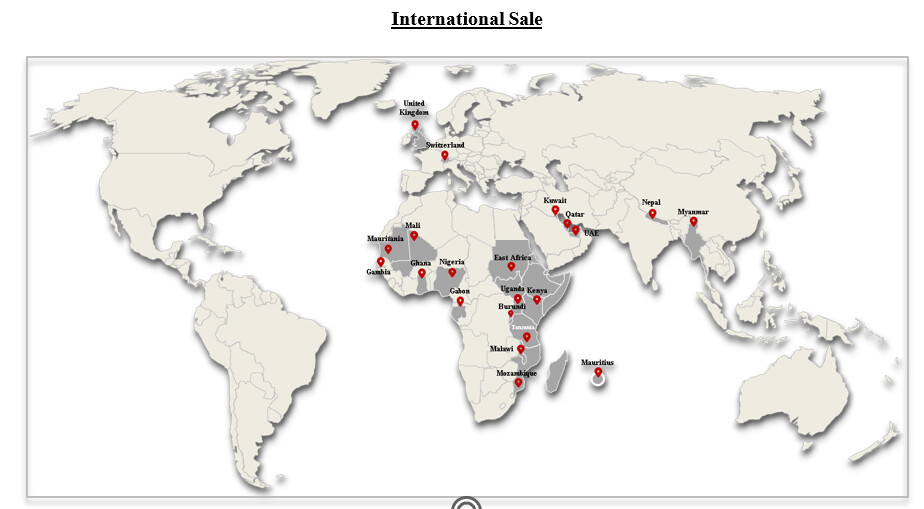

- Export vs Import: about 8-to-9% of revenue is generated from exports, with exports primarily being to countries in Africa

2/ Product Portfolio

Single Vision Lenses:

- Single vision lenses have only one optical power and are primarily used to correct deficiencies in either near or distant vision. As they are essentially simple magnifying glasses when used to treat near-sightedness, single vision lenses tend to be cheaper than other types of lenses and are readily available in the market.

- These lenses offer solution for myopia or hypermetropia and presbyopia, and these lenses are for the people from the age group of 0 to 35. It helps to correct near sightedness or farsightedness.

Bifocal Lenses:

-

Bifocal lenses have two optical powers and are used to correct deficiencies in both near and distant vision. The surface of the bifocal lens is typically divided into two parts, the upper portion for distant vision and part of the lower portion for near vision. The division between the two parts of the lens is clearly visible and forces the eyes to make an abrupt transition.

-

These lenses offer solution for myopia or hypermetropia and presbyopia, and these lenses are for the people from the age group of 35 onwards. These lenses offer solution for farsightedness and near sightedness together, not good cosmetically and are also cheaper then progressive lenses. Also, these are the traditional solution and the only solution for such patients where both far and near correction was needed until progressives were discovered using new technologies.

Progressive Lenses:

-

Progressive lenses utilize complex designs to combine several optical powers for different viewing distances, with the optical power gradually increasing from the upper portion of the lens to the lower portion of the lens. The transition between powers is gradual and seamless, thereby eliminating distracting lines between the different vision areas and allowing the user to see at various distances without an image jump, restrictive focal lengths or demarcation lines, although some users have difficulty adapting to the distortion areas of progressive lenses. Progressive lenses are generally the most expensive type of lenses and are less frequently covered by insurance than single vision or bifocal lenses.

-

Progressive lenses are used to treat Myopia or Hypermetropia and Presbyopia, a vision condition where the crystalline lens of the eye loses its flexibility and the eye muscles become less powerful causing the eye to lose its ability to focus on close objects. Presbyopia is part of the normal aging process and develops gradually over an extended period of time and affects almost everyone over the age of 45, regardless of whether they have previously had normal vision or have suffered from myopia, astigmatism or other vision conditions. Presbyopia is a degenerative condition that worsens and often requires progressively stronger lenses over time. Presbyopia cannot currently be cured but is treated with lenses that generate optical power assisting the eye to focus on both close and distant objects.

Special Category:

- These lenses offer solution for myopia or hypermetropia and presbyopia, and these lenses are for the people for any and every age group as it consists of mirror lenses, polarized lenses and any and every lifestyle lenses. These lenses can be offered in the form of single vision lenses and progressive lenses also hence the price range varies and being a lifestyle category and a special category, the prices depend on the combination of categories as per the need and demand.

Revenue split by lens-type:

- About 60% revenue comes from Progressive Lenses

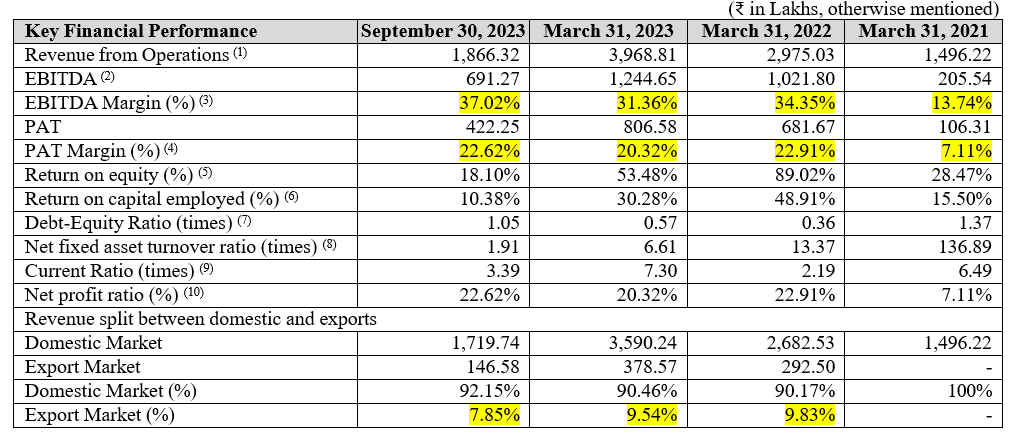

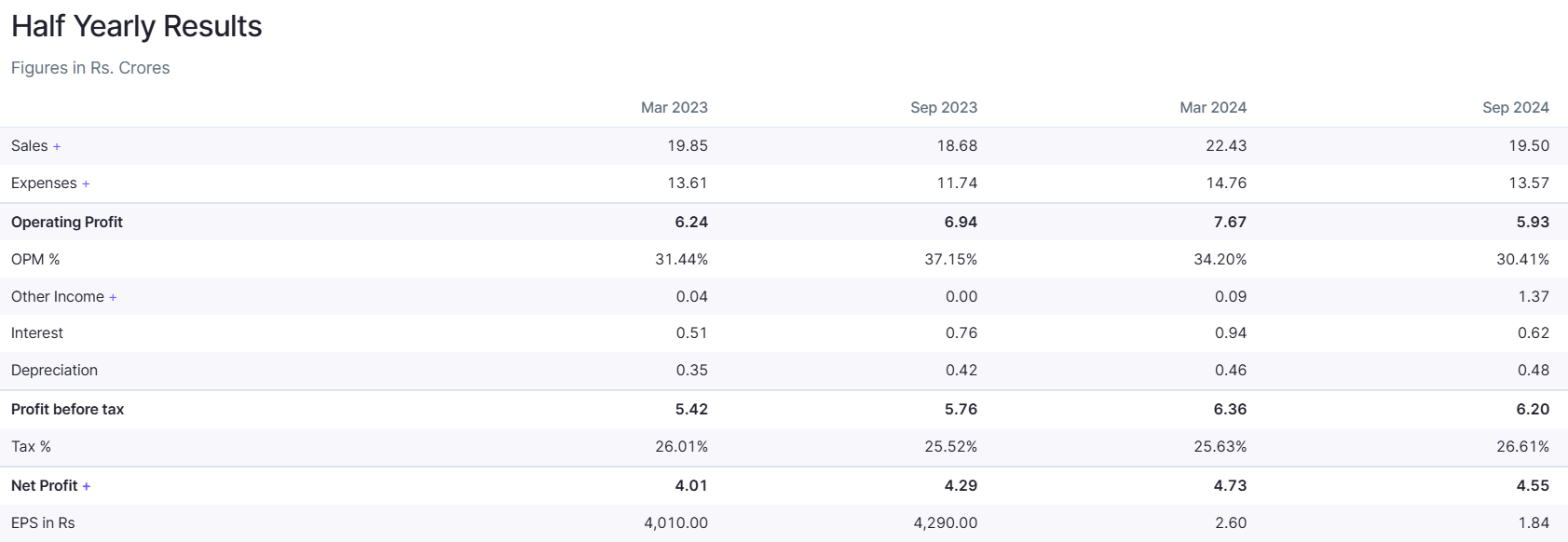

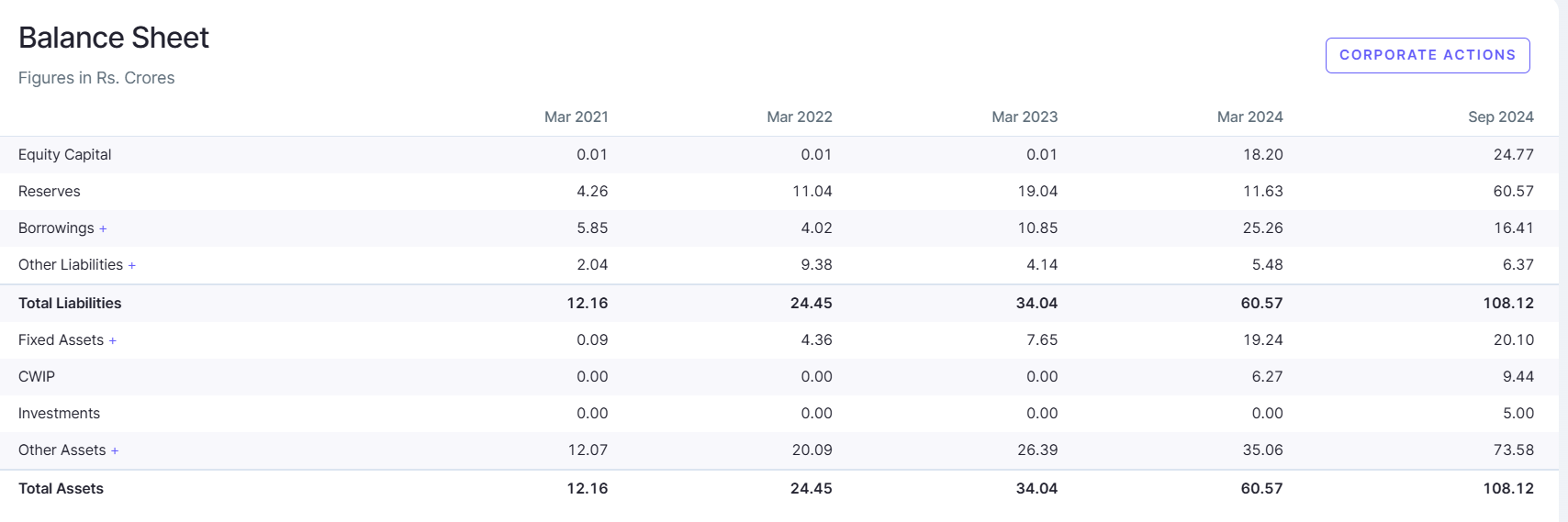

3/ Numbers and valuation

-

The EBIDTA and PAT margins have been both consistent and healthy in the last 3 years

-

Even the recent results (Sep’24 half-yearly) are on the same lines

-

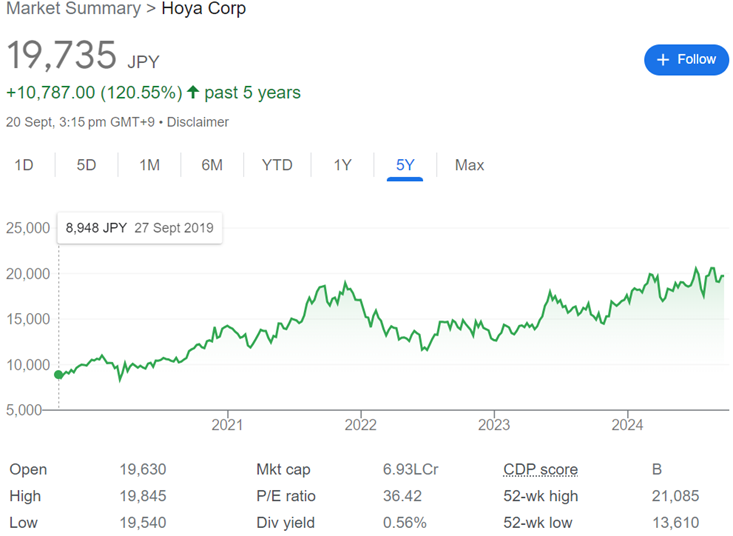

From a valuation comparison standpoint: as far as I could find there is only one other listed company that makes prescription glasses in India – GKB Opthalmics. But I think the comparison will not be fair because GKB also operates retail outlets.

-

EssilorLuxottica and Hoya Corp trade at a PE multiple of ~35; although in my view it’s not fair to compare Yash with either of these companies given the scale of operations.

4/ Industry Overview

Global Eye Wear Industry:

-

The global eyewear industry is a rapidly growing market, with the value of the sector estimated to reach USD 197.05 billion by 2027.

-

The prescription eyewear segment accounts for 63% of this market share and is expected to grow at a CAGR of 6.08% between 2021 and 2025.

-

Luxottica and Essilor completed their $52 billion merger in 2018, further consolidating their position as major players in the industry.

-

Blue light blocking technology has been gaining traction lately due 90 % adults using digital devices more than two hours each day contributing significantly on rising demand for these type spectacles worldwide

-

Asia-Pacific holds the largest market share due to a large middle-class population and increasing consumer awareness.

-

North America follows closely behind, driven by a high prevalence of vision problems and strong demand for designer glasses.

-

The sports eyewear segment is expected to grow at a rate of 4% between 2020 and 2025.

-

The sunwear segment is anticipated to grow by 4.3% from 2021 to 2028 globally.

-

The online eyewear market was valued at USD 31.87 billion in 2019 and is expected to reach USD 41.61 billion by 2027, growing at a 4.1% CAGR.

-

The luxury eyewear market will grow at a CAGR of 11.4% between 2021 and 2026.

Indian Eye Care Industry:

-

It is reaching an inflection point where organized businesses wanting to establish a national footprint will attempt to disrupt a market that has historically been controlled by mom-and-pop stores, India’s eye care sector is poised to experience a surge in Merger and Acquisition (M&A) activity.

-

In the next five years, the M&A boom might see the rise of four or more significant firms, which together could own more than 2,000 eye hospitals across the country. According to industry observers, acquisitions may account for up to 50% of their growth.

-

Currently, patients who require surgical procedures for cataract removal or vision correction are taken care of by ophthalmologists that operate tiny clinics around the nation. The larger firms with access to money are attempting to buy out the smaller ones and merge them under a single brand.

5/ Manufacturing Process & Facilities & Utilization

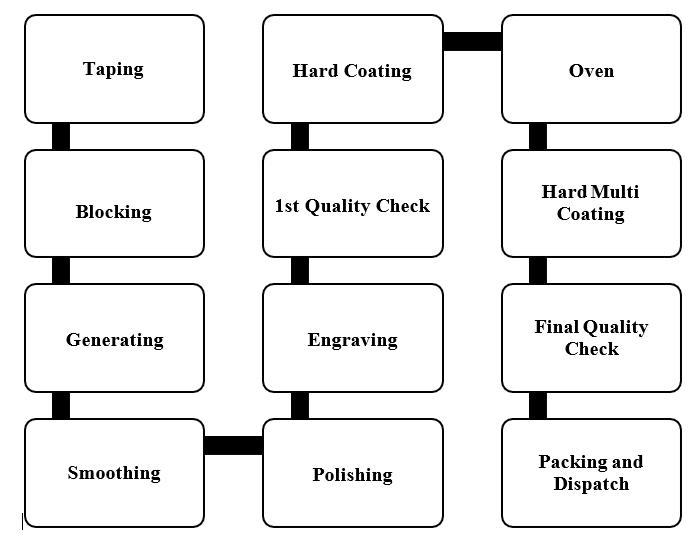

Manufacturing process

- Followings are the steps in the manufacturing process:

Taping – Taping the raw lense from front side to protect the front side from any damage as all the generating, smoothing and polishing process needs to be done only on the backside by using the new advanced technologies.

Blocking – Once the raw lense is tapped on the front curvature then that lense needs to be blocked using alloy and giving it a handler so that it can be attached to every machine for generating, smoothening and polishing purpose.

Generating – Here the lense is first cut to the required diameter size from the outer border using milling tool and then on the backside of the lens polycrystalline diamond (PCD) diamond tool is used to generate power through generating prims required as per the prescription.

Smoothing – Once the prescribed power is generated and the required diameter and thickness is received the lens which is still rough on the back surface so it is smoothened to get the surface fine.

Polishing – Once the back surface is smooth it needs to be polished to get the transparency of the back side of the lens just like the front side.

Engraving – Here we engrave the details of the lens in order to distinguish it from the other products in the market and this is done using carbon dioxide (CO2) laser so the engraving is not visible to the naked eye.

1st Quality Check – After all these processes are done, we do a quality check of the lens where each lense is checked for the correct prescription, the lens is transparent as it should be and if there are any external scratches or dust or any other issues with the lens.

Hard Coating – Here the lens gets layered for strengthening the quality and life and gets the property of scratch resistance through dipping it in multiple chemicals.

Oven – After applying the hard coating and its chemical layers to strengthen these layers the lens is kept in oven at 120 degrees for 2 hours so as to strengthen the quality and life of lenses.

Hard Multi Coating – This is a vacuum process in a machine where lenses are treated on both sides by applying chemicals on both sides so as to get the properties like smudge resistant, oil resistant, water resistant, UV protection and such other properties depending on the orders and the recipe selected.

Final Quality Check – Once all these processes are done the lenses needs to be checked for each and every aspect in terms of the coating quality, prescription, transparency, scratches and such other variables.

Packing and Dispatch – The lens is then wrapped with a soft sheet and packed in an envelope and then in a box and then dispatched to the particular customer.

Facilities

Machines installed currently:

-

Antireflective Coatings (ARC) department : OAC 120D Coating System, OAC 120 Coating system, OAC-75-D, coating system etc.

-

Hard coating department: Hard coating machine CD1000, Hard coating machine Procoat 140, CD500 Hard coat, Velocity coater 220V/50HZ etc.

-

Digital Surfacing department: FLASH-A NG, Digital Surfacing-Turning Machine, Chiller 1.8 KW, Coolant System KB 100, ASP 80 Twin-A, Digital-Surfacing-Polisher, PB 30 Polishing Slurry Tank - Ophthalmic, Pressure Calibrator, Schneider HSC Modulo Generator Schneider HSC Modulo Generator, Schneider CCP 103 Polisher, Schneider CCL C*Mark Laser, Schneider Poliermittelanlage, Flash-Generating-turning machine, Flash-Generating-turning machine, Easy twin CNC Polisher Manual, GE-33-0033, 3M Applicator, Opto Tech Plano Blocker OTB 60, ASM 80 CNC-TC-M

Capacity Utilization

- Note: capacity in the table below is in pairs per day

6/ Risks

-

Company has signed a distributor agreement with HOYA Lens India Private Limited for exclusive right to sell, market and distribute the “Pentax” brand of ophthalmic lenses. Their inability to renew or maintain said agreement may have an adverse effect on our business operations. The contract has a validity of 1 year from date of signing and the same is automictically renewed for 12 months period with a maximum of four times.

-

Company does not have long-term agreements with suppliers for the raw materials and an increase in the cost of, or a shortfall in the availability or quality of such raw materials could have an adverse effect on the business

-

Potential conflict of interests between the Company and other enterprises promoted by our promoters or directors. The main business object/activities of our group company, Yash Optical Trading LLC and promoter group entity, Yash Optics, permit it to undertake similar business to that of our business, which may create a potential conflict of interest and which in turn, may have an implication on our operations and profits. Conflicts of interests may arise in allocating business opportunities between our Company and our Group Company and promoter group entity in circumstances where our respective interests diverge. Further, our Group Company is allowed to carry on activities as per its MOA, which are similar to the activities carried by our Company. This may be a potential source of conflict of interest in addressing business opportunities, strategies, implementing new plans and affixing priorities. In cases of conflict, our Promoters may favour other companies in which our Promoters have interest.

-

Being an SME stock is a huge risk by itself

-

Something that doesn’t add up for me: while the asset base grew from FY23 to FY24 but there was no commensurate increase in the top-line

7/ Miscellaneous Observations

-

I was going through the company updates posted on NSE, and there seems to be considerable interesting amongst institutional investors and FIIs…but no one seems to have invested in it so far

-

This China-based website (I am guess it’s China based) lists Yash as one of the top 5 prescription glass manufacturers in India

https://www.lenstechopticals.com/about/ -

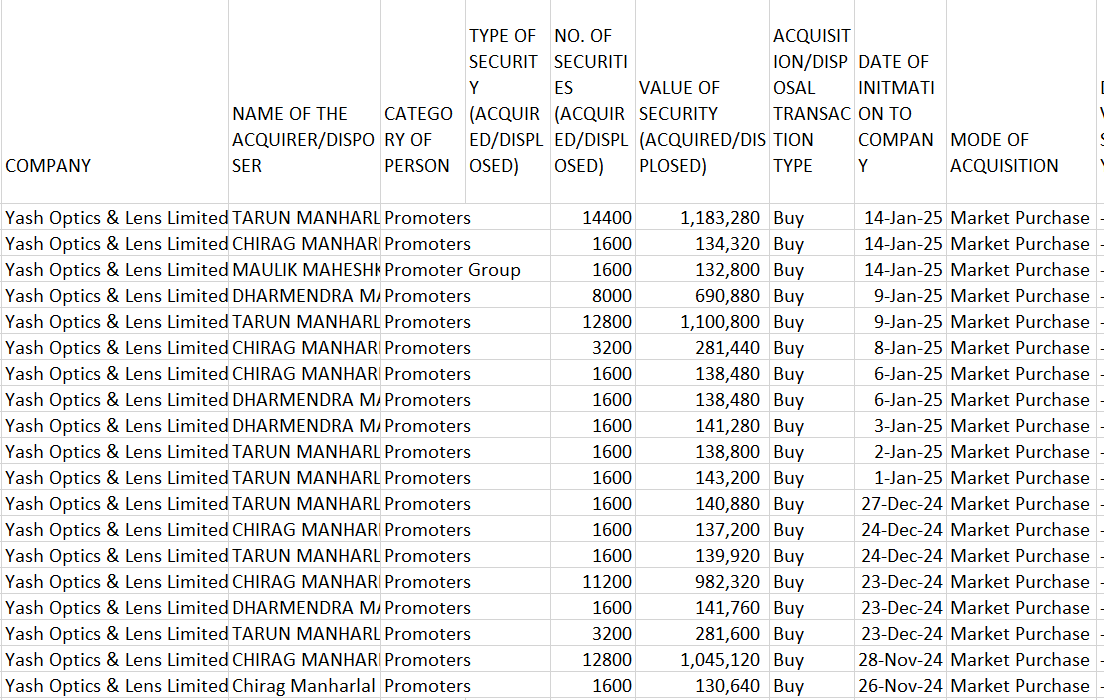

In the last week of Nov ('24) the promoter is buying shares from the open market (very small quantities though)

Disc.: Invested. This post is not a recommendation, please do your own due diligence before making an investing decision in this stock.