Good H2 numbers

1 Like

Would like your view on how these are considered good numbers. What am I missing?

`

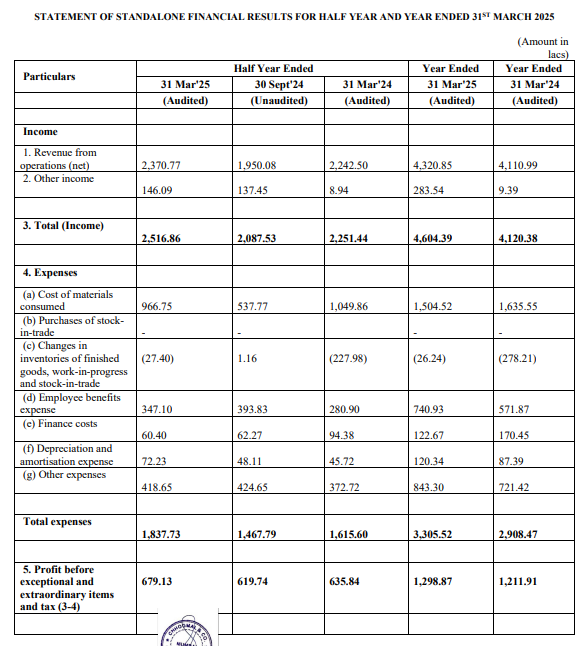

Marginal growth both at top line and bottom line.

1/ I track a bunch of nano/micro caps – and what I am seeing is for a lot of them the post SME IPO results haven’t been great.

2/ With that backdrop, I like the fact that Yash has shown both sequential and YoY growth in half-yearly numbers.

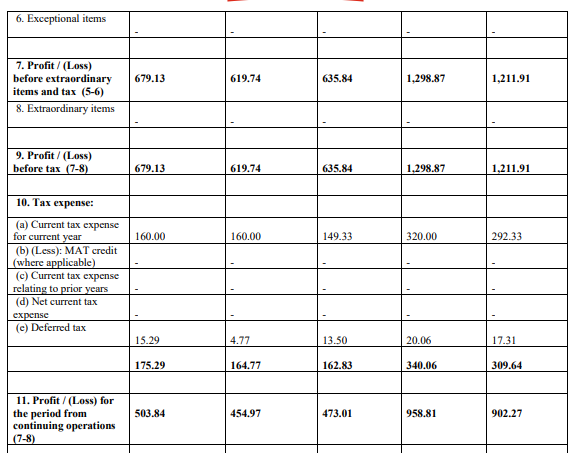

3/ Also, for the full year there is a 12% growth in topline and about 7% growth PAT

4/ In their note they did mention that there were additional expenses this year else numbers would have looked even better

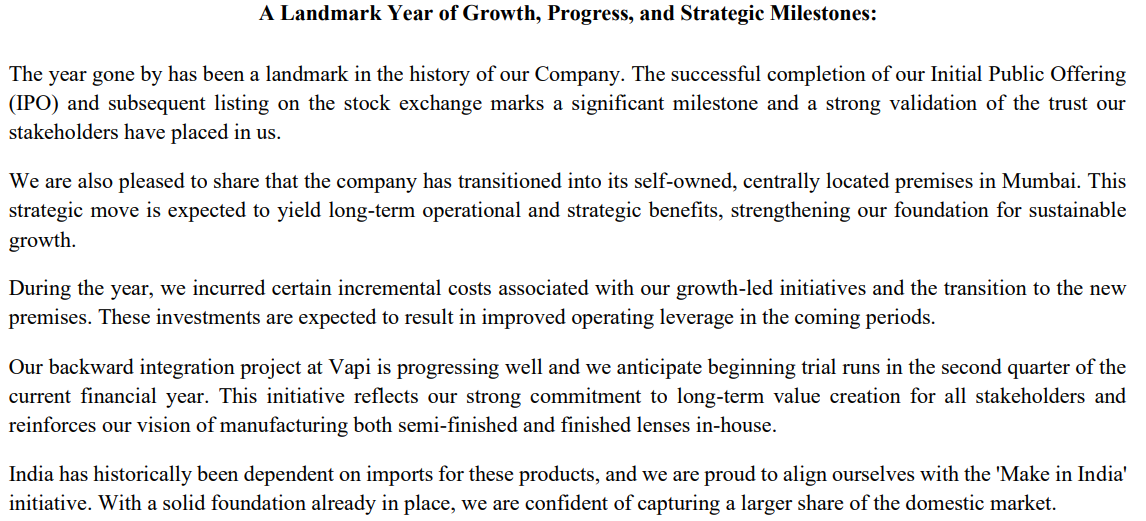

5/ Lastly, they are doing capacity expansion, backward integration and streamlining their operations

Overall, I like how the story is developing…and in my opinion the numbers are good (def not stellar)

2 Likes

I am sorry, but operational revenue is up 5% and profits are up similarly for the year. Again I ask what did you see in numbers to tell its good.

FYI though Indian optical lens market is expanding at 7% a year. India Optical Lens Market | Forecast & Outlook 2031

GKB Ophthalmics Ltd share price | About GKB Ophthalmics | Key Insights - Screener…One of the worst product companies in the market with zero marketing skills and they grow at 10% YOY.

Zeiss India is doing double digit revenue growth. Carl Zeiss India (Bangalore): Zeiss Group expects to maintain double-digit growth in India this fiscal, ET Government.

1 Like

Hi All, adding my few takeaways from past management meetings -

-

The flatline in base business growth we see in FY25 is due to fully used up capacity. With the new machines (were due to be placed in April/may-25 as per their press release) - they will add 60% more capacity. They guide for 15-20% growth and full utilisation in 2-3 years.

-

On the backward integration, that should be looked as a new business line itself. While some of it may be used up for internal consumption, the opportunity here is of import substituting the base lens which is largely imported from China today. Margins will be lower than base business but asset turnover will be better. As per press release this will be visible from H2 onwards.

-

Yash has descent presence in Maha and Gujarat, they will be stepping up in newer regions (Kerala, Chennai, Blr, etc). Hence despite competition, market growth should help.

-

Having met them, Quality and integrity of management is exceptionally good.

Key risks here is growth opportunity amidst competition, I am betting they are not too large a base so if they execute well 40cr top line has good room to grow.

Brand building at consumer level is difficult for mid level ones like Yash, but some basic branding and good service and retailer relationship helps.

Hope this helps.

Disclosure- Invested

5 Likes

Having worked for more than 20 years with a MNC lens company, I can tell you, Yash will find it the going very tough. Yash is a lens manufacturer who sells directly to retailers (Opticians) or through distributors. It operates in budget category of lenses where margins will always be under pressure as retailers & distributors will squeeze you as much as they want. The leading players in lens manufacturing are Essilor, Zeiss, Hoya, Nikon ( Essilor), Vision Rx ( Essilor), Prime lenses ( Essilor) & small players like Yash. The manufacturing process is very complicated and consistency is a huge challenge. MNCs have been the go to players for most leading retailers which includes National chains like Lenskart , Titan , Himalaya etc , Eye Hospital chains like Dr Agarwal, Arvind Eye, CFS , Vasan etc & leading independent retailers across the country. As of today ,Yash can make inroads into budget range category across independent retailers which is not a very lucrative category. The only talking point for Yash is price and that’s not a great position to be. The industry is highly fragmented, there is no moat in lens industry, retailers can change the supplier anytime they want and there are no long term contracts for supplies. One more concern for Yash would be , Lenskart is gaining market share big time at the cost of independent retailers & this is the segment which Yash is targeting. Even leading lens players are finding it difficult to grow in the market as the category does not sell on brand power and retailers will always have upper hand in price negotiations. There are hardly any lens brands other than Crizal from Essilor which has a decent pull in the market. Even consumers are not concerned about lens brands as they go by wgat retailer recommends & also its not something that can be flaunted. The consumers focus more Frame brands like Rayban, Oakley, Vogue, Prada etc.

9 Likes

I agree with you, with the caveat that Essilor and Zeiss have brand pull at the premium level, at least for progressives.

Rest I have been clear in earlier posts in this thread that Yash would find it extremely difficult to grow in this market.

1 Like

I feel making a comparison with Essilor or Zeiss, we should also consider that we are NOT paying a 40x pe to Yash (unlike brands like Zeiss or chains like Lenskart).

Progressives Lens is a difficult thing to master (as you also said), and Yash is a brand in mid tier/low tier progressive lens segment since last 20 years. I feel the need for low/mid priced progressive lens will keep increasing, as Essilor/Zeiss pricing is 4-6x of Yash.

Also, with listing of brands like Lenskart, the pricing environment for sector will improve post listing. That benefit will flow through to all, specifically mid tier ones like Prime, Vision Rx, Yash, etc.

At 20x trailing PE, I feel growth expectations are not super high. With them adding capacity to do 60-70 cr revenue, it’s about them expanding in adjacent cities to Mumbai (Pune, Surat, Ahd, etc) where they have some presence but can be expanded.

How they execute is what we will need to track, and their scale is too small vs larger brands - so growth for them should be more dependent on their sales strategy and positioning than how the overall market share shift happens.

5 Likes

PE is low for a reason. Scaling in this business at this juncture is very difficult. Even big boys in the industry are not able to grow beyond 10% even after price hikes of 5-6%. The traditional optical trade which Yash depends for growth is shrinking, the new age retailers are gaining market share at a furious pace. The only way to grow for Yash is somehow get a foothold in the national chains like LK , Titan or Hospital chains like Dr A , Arvind etc. At this juncture it looks very difficult. As I said in the previous message the best play in this industry in my opinion is Dr Agarwal Healthcare.

3 Likes