Based on my discussion with a major pump manufacturer based out of Ahmedabad, I understand that the RM prices had increased from April till end of September and are significantly down now. The prices have more or less been stagnant since early October and majority manufacturers have not changed the pricing yet. I believe products division should perform well in Q-3 and the co. should be back on track on gross level.

8 Likes

2 Likes

The Promoters of WPIL have bought 6518 shares from the open market in the last couple of days.

At the AGM the CMD had also talked about NSE listing. The Co. has, I believe, initiated the process of NSE listing. I also understand that the Co. is in the process of engaging the services of an Investor relations firm to help investors be better informed about the developments in the Co.

8 Likes

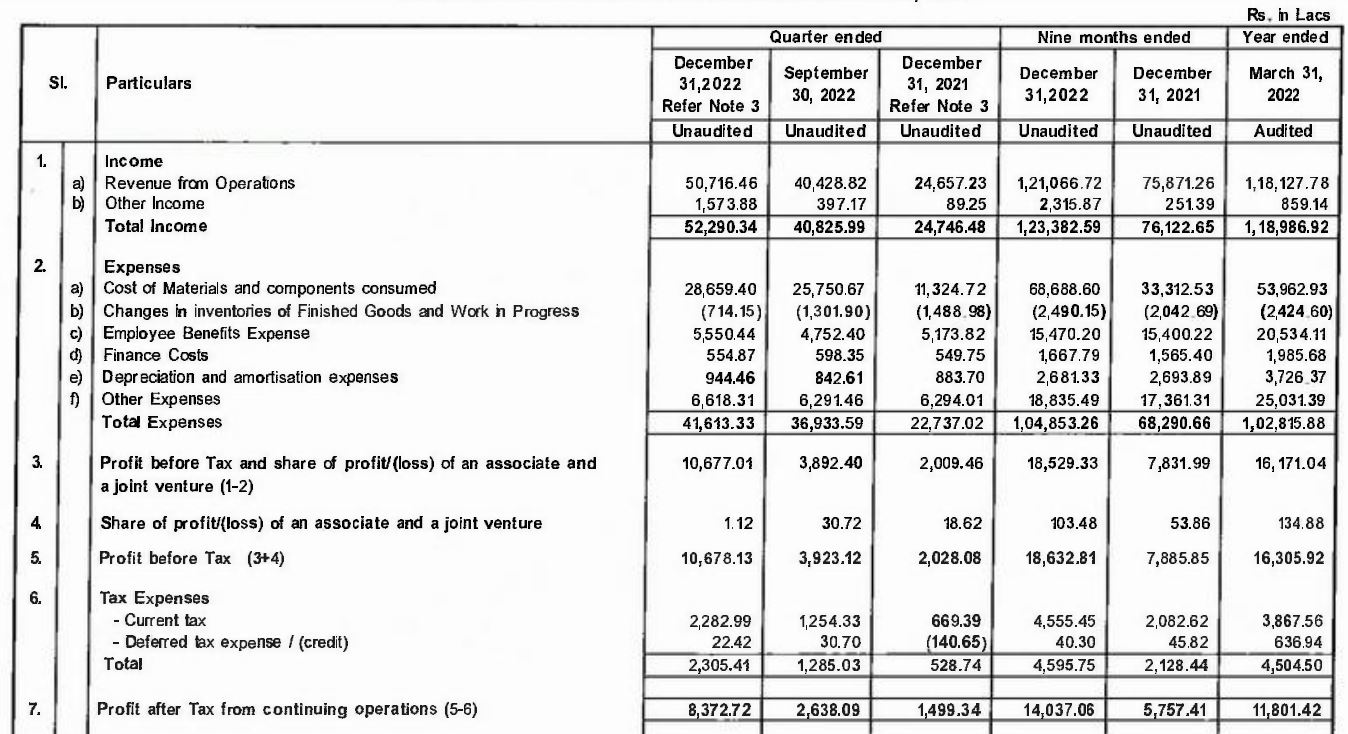

WPIL 's Q3 numbers were nothing short of spectacular & the stock is up 35% in two days! Not without reason! Sales have more than doubled & have crossed 500 crs, with operating margins coming in at about 21%.

The Media release attached below, that came along with the results made for very interesting reading as it gave some insights into the nature / scope of work of its subsidiaries across the globe. With the Co. now opening up & engaging with its investors / shareholders by giving a quarterly media release & appointing Valorem Advisors, for its Investor relations, it will not be long before the investing community appreciates how under valued it is, despite the recent run up. Even if the market cap were to double from here (currently 1,580 crs), given its high operating margins, given that it is an Indian multi national with its various subsidiaries across the globe, being as profitable if not more than its domestic operations, the Co would still be comparable to its domestic peers in terms of its valuation.

The table below (taken from Screener.in) would throw more light on the valuation vis a vis its peers.

Peer comparison

Sector: Capital Goods-Non Electrical Equipment Industry: Pumps

| S.No. | Name | CMP Rs. | P/E | Mar Cap Rs.Cr. | Div Yld % | NP Qtr Rs.Cr. | Qtr Profit Var % | Sales Qtr Rs.Cr. | Qtr Sales Var % | ROCE % |

|---|---|---|---|---|---|---|---|---|---|---|

| 1. | KSB | 1852.55 | 38.80 | 6448.73 | 0.67 | 39.00 | 0.26 | 431.30 | 17.17 | 21.00 |

| 2. | Kirl. Brothers | 393.40 | 16.23 | 3123.95 | 0.76 | 88.90 | 323.19 | 957.50 | 32.01 | 11.02 |

| 3. | WPIL | 1618.10 | 9.46 | 1580.41 | 0.62 | 83.71 | 431.02 | 507.16 | 105.69 | 20.28 |

| 4. | Roto Pumps | 570.55 | 30.96 | 895.98 | 0.50 | 9.25 | 12.70 | 57.21 | 21.57 | 30.03 |

| 5. | Shakti Pumps | 412.50 | 17.29 | 758.18 | 0.48 | 11.25 | -23.94 | 314.22 | 16.97 | 21.33 |

| 6. | Adarsh Plant | 16.65 | 16.50 | 0.00 | 0.06 | -57.14 | 5.11 | 44.35 | 4.32 | |

| Median: 5 Co. | 570.55 | 17.29 | 1580.41 | 0.62 | 39.0 | 12.7 | 431.3 | 21.57 | 21.0 |

11 Likes

Thanks to @rcinvestor999 and @RajeevJ for regular insights on recent developments.

A quick recap of past Order Book and following year revenue pattern (note it is only approximation to see trend and sourced from rating report etc)

- Dec 20 2021 order book was 1900 cr and CY 21 revenue was 1200 cr at 17% revenue

- Dec 21 orderbook was 2500 cr, CY 22 revenue is 1650 cr at 18%,

- Dec 22 order book is 3350 cr, CY 23 revenue likely to be …2400-2500 cr around 20% margins. (margins can be higher as well with operating leverage and RM stability)

Potential - current mkt cap is below 1800 cr. 10+ year median EV/EBDITA is 7, potential mkt cap of 3500 cr+ if above pattern pays out as base case, much stronger balance sheet than earlier as well.

Some points that stand out are

- as @RajeevJ pointed out this being a case of Indian MNC pedigree organization

- Strong balance sheet, return ratio and good Cash flow,

- Promoter increased stake over last many qtrs + MF holdings leaves less float in mkt

- Have taken out ATH on charts and looking in strong momentum

- Part of global infra spend story (India + strong global footprint enabling broader participation e.g. Nuclear energy spends in France)

- Investor communication - Valorem Advisors has been appointed as IR and they do have a good track record, quite important aspect in mkt perception

- Sector tailwinds - Water EPC - Many peers in India have also reported strong order win/book - KEC, kalpataru etc. Reassuring of collective sector demand visibility.

Stock has run up post Q3 results, however story might be just getting started and has potential of growth + some re-rating.

Invested

12 Likes

Thank you @Dev_S.

Just brining in a technical chart perspective:

Quarterly chart of Wpil, strong Momemtum and breakout seen. It’s respected a multi year channel as well. I think we may be looking at a channel top touch sometime in the next few years.

5 Likes

Company received 4 Letter of Acceptance (LOA) from Madhya Pradesh Jal Nigam Maryadit for a total value of ₹1225 Crores to be completed in 24 month period.

4 Likes

Isn’t it a high time that WPIL gets re-rated since it’s P/B is at 2.5 times and no stock bonuses/splits/right issues in these many years. All ratios seem to point towards an under-valued company raring to get correctly valued.They also have MIT as an institutional investor ,which makes it a privileged investee company.

they had MIT as a privileged investor in last two years. Markets are supreme they award those who wait patiently

disclosure no investment and not tracking except technically

1 Like

The Key Risk is Retention Money of 10-15%. Sometimes getting the release of these is painful and affects the cash flows.

Disc : No Exposure

1 Like

Almost no data available about the management vision, Capex, revenue mix and also their employee cost plays a crucial role into OPM , seems directly affecting

1 Like

First time investor presentation :).

9 Likes

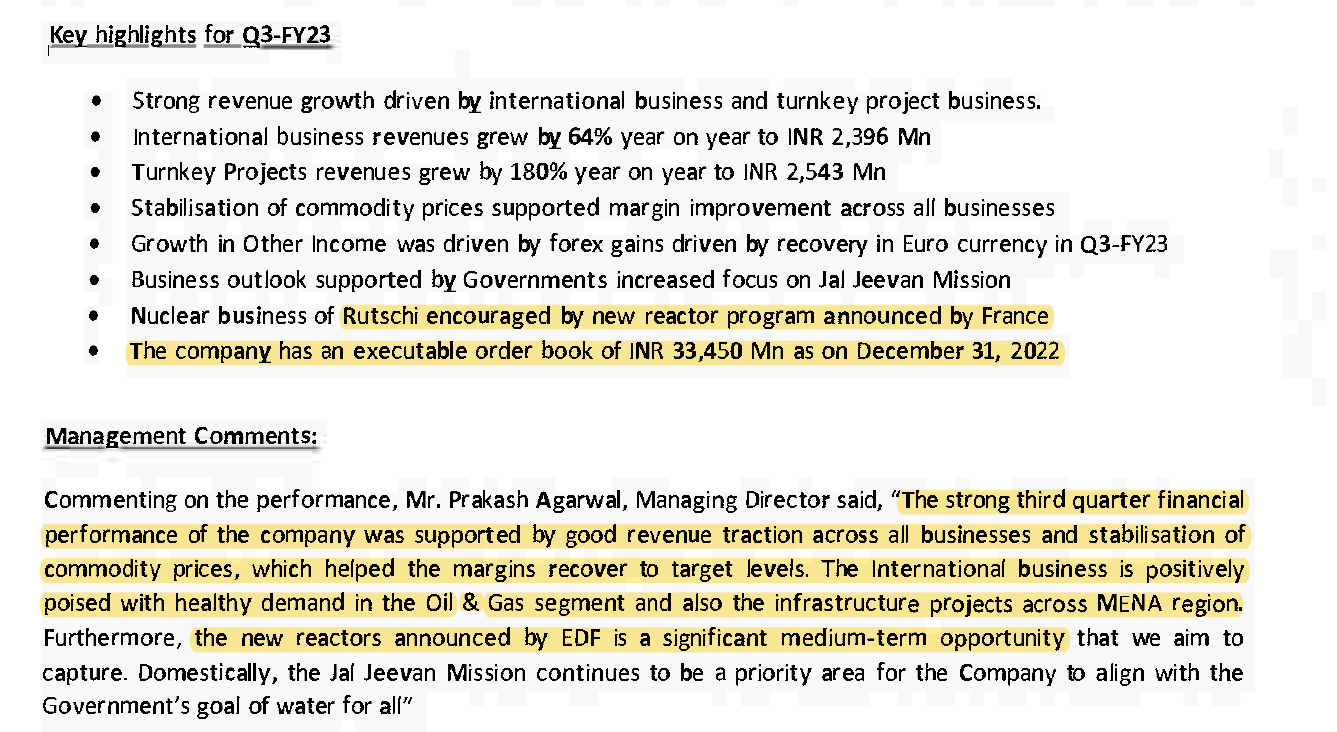

Presentation - Gruppe Rütschi specializes in water pumps for nuclear reactors.

Govt. of India currently announced approval for 10 new reactors

Q3 press release Mgmt. highlighted the opportunity for Rutschi by new reactor program announced by France (EDF) as ‘significant opportunity’.

https://india.edf.com/en/our-activities/nuclear

EDF India is involved in Jaitapur site, State of Maharashtra and possibility will have a role in future reactors of India as well. They are a global major.

If we get a chance to interact with mgmt. then we can surely ask questions related to this. Seems like a significant development keeping future in mind.

Disc: Invested, buy in last month.

11 Likes

thanks @rajpanda , some additional pointers to substantiate mgmt claims to be able to leverage EDF opportunity (attempt to validate its not just a wish list ![]() )

)

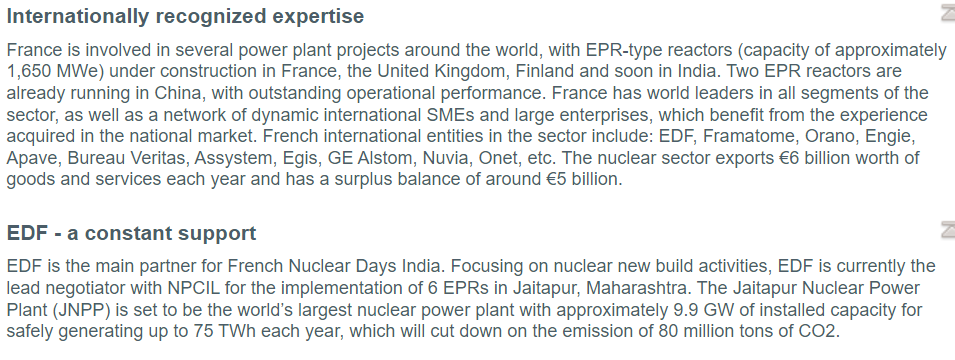

1. Why France and EDF? French Nuclear Days India 2020 - La France en Inde / France in India

France is apparently a key country with high concentration on Nuclear power skills (across value chain) , EDF is front running organization working with NPCIL (indian authority) - has signed binding commercial agreement - details on link in previous post

2. Where does WPIL/Rutschi fits in EDF equation

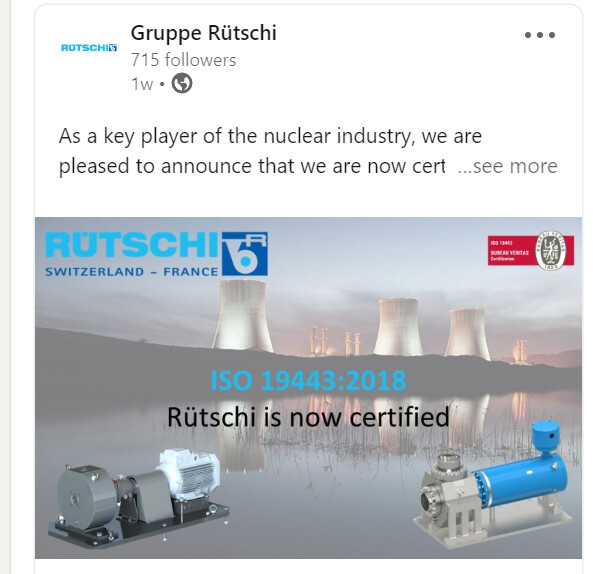

EDF has clearly laid out supplier requirement( in a ring fenced manner where this certification came into existence in recent times), where significant part of supplies/capabilities are planned from local sourcing - who can be a supplier/qualifications - a key certification reqmt is ISO 19443 - specific to Nuclear power industry

here is Rustchi (read WPIL) status

-

To validate certification critical aspect further - L&T claims to have received as first indian company to get this certification just last month

https://corpwebstorage.blob.core.windows.net/media/47952/2023-02-28-lt-heavy-engineering-becomes-indias-first-to-earn-iso-194432018-certification.pdf

Appears L&T doesn’t have a direct play in pumps though - Nuclear Power Plant | Heavy Engineering | L&T India -

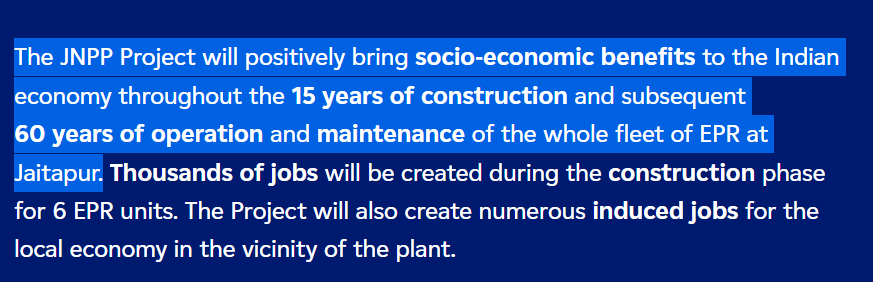

How big is EDF - India - JNPP project scale -

These are mega projects and have their own pace and in a different league, may not be near term triggers but something worth understanding mgmt game plans on Nuclear play in India, global credential are more established with Rutschi.

15 Likes

Investor concall by WPIL tomorrow, the first by the Co.

7 Likes

Annual report - WPIL FY2023

Rev growth - 90%

PAT 14,302 lacs Vs 6,387 Lacs

Dividend - 20 Rs/Share

Domestically

Jal Jeevan Mission has gained traction

Extended to AMRUT 2

ATO (Assembled to order pumps) - Strong demand by MC major thrust on swage and drainage pumps. Industry like Oil and Gas are also another growth area.

Internationally

Rev 794Cr Vs 664Cr

Investments in Finder and United Pumps Australia and the oil & gas sector did well with growing order books and good aftermarket business. Another growth driver were infrastructure projects in the Middle East and North Africa region for

water and irrigation. The nuclear business of Rutschi was positively impacted by the restart of new nuclear reactors in Europe with France taking

the lead and the European Commission declaring nuclear as a Green Energy. A large number of reactors are proposed

over the medium term and this creates good potential for the business. The company is reviewing this new opportunity

and planning for the future as large investments in infrastructure and manpower will be needed to cater to this expected

demand.

5 Likes

@RajeevJ Hi sir. Since you are tracking the company, whether you have researched Roto Pumps which is also from Pump sector and has good operating matrix plus done some capex also.

Also whether WPIL caters to Solar pumps also since that sector is also growing very well under the Kusum scheme and Shakti pumps has got good orders in that.

WPIL Ltd. European subsidiary Gruppo Aturia has entered into a binding Share Purchase

Agreement with newcleo France on 6/08/2023 for sale of its subsidiary Rutschi (consisting of

Pompes Rutschi France and Rutschi Fluid AG Switzerland) for a consideration of 68.7million

Euros subject to terms and conditions of the SPA.

1 Like

The buyer did a fund raise last year:

another this year:

This knocks off 10% of consol revs for WPIL.I was a bit surprised that WPIL decided to do away with the subsidiary just as it seemed to be entering a period of good growth/order intake.And it’s not as if WPIL needs the money even if one assumes higher WC needs as they execute the large order book since their WC cycle and balance sheet were already solid.But 3x sales is a decent multiple given how cheap European assets usually go for.

Will be interesting to hear the management’s views on the same.Q1 call and results are also yet to take place.

7 Likes