Hi Mukul, just curious to know - momentum-based approch to protect gains

Can you please explain?

I have been invested with my first buying at around 205 levels, at that time I anticipated 750-800 would be an ideal price. Although fundamentally it performed way better I don’t want to give up gains in case the market turns bad and this company falls more.

So, I am riding the momentum currently, and if the price reverses or breaks the support zone. I would exit and protect my gains. This is how I am looking at it, although there can be many perspectives from different investors.

Regards,

2 Likes

Mukul Ji, Very honest opinion.

What is the support zone

Currently, have kept it at Rs. 770/- made during mid-oct.

1 Like

Brian Feroldi assigns a moat score of 20 out of 100. However, it is evident that Wonderla possesses a substantial moat.

1 Like

Wonderla is entering the high ROCE capital light phase now. Their competitive advantage keeps increasing in size. They manufacture their parks much cheaper than anyone else. At the moment is fairly priced for 12 % growth in price but undervalued for 20 % plus growth. Multiple are reasonable. It is played on a consumption theme. They can maintain single-digit footfall plus a 5 % (inflation) price increase that gives an easy 12 to 15 % cashflow increase. Plus growth will come from Bhuvaneshwar and Chennai. We are also underestimating the pricing power that Wonderla has (even management is underestimating ). The ability for people to spend is way higher.

I was buying at 200 and had no competition last year. Of course, at this price, you need to get growth assumptions right but in my view is still not expensive.

Disc: Invested from 2017 at 250 Rs, so my views can be biased.

6 Likes

Amit Ji, Are you talking about profit growth or sales growth?

If you are talking about 12% profit growth, May I request to please explain in detail how it is fairly valued ( I am not from finance background)

This is based on the assumption every park going forward will be on leased land. Might not be the case for every park (As acknowledged by the management. They would prefer the asset light model, but are prepared to buy the land outright if necessary)

Fairly priced is based on an estimate that profit will grow at 12 % then multiple can be 24 times earnings ( 2 times growth rate ). So now if your profits grow 15 % for 5 years and multiple (price to earning or better price to cash per share ) stays the same in 5 years market cap will double and your stock price is expected to follow it. However, this is maths but in reality, your return can be higher or lower based on the mood of the people who are buying and what they think will happen in the future.

2 Likes

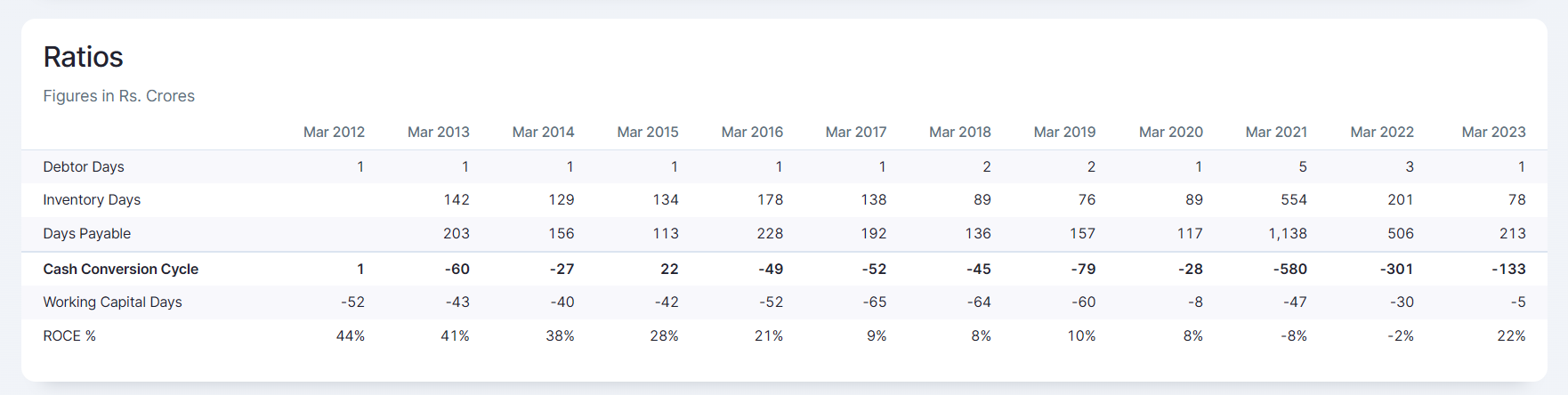

Wonderla was always a high ROCE business you should look at the unit economics of a park. ROCE was 40 % when parks were out of the investment phase and were buying expensive lands in Kochi, Bangalore, and HYD. now it will get even better if land which is 50% of capex is given free.

3 Likes

How exactly are you calculating the ROCE? Return ratios for the business have always been meh because of the asset heavy nature of the business. Even the management says they don’t look at return ratios because of that. IIRC, they said they would be happy with 12-14%.

(Presumably, the work on new parks will begin immediately after Orissa & Chennai parks open. So, they will still be in investment phase for a long time. Chennai & Orissa parks will take time for operations to stabilize. Even the mature parks are getting new rides at significant cost. So, ROCE to be considered should be 3 or 5 year average)

1 Like

Accounting does not show real profits, you will need to build your own unit economics and cashflows per park normalized. I did the same in Narayana Hrudalaya and found out it was so cheap in 2018.

You also know that they assemble most of park rides and then buy cheap rides from abroad to save cost. No one in India can do this.

They are also one of the biggest restaurants/fast food businesses with 2 to 3 M customers eating every year.

2 Likes

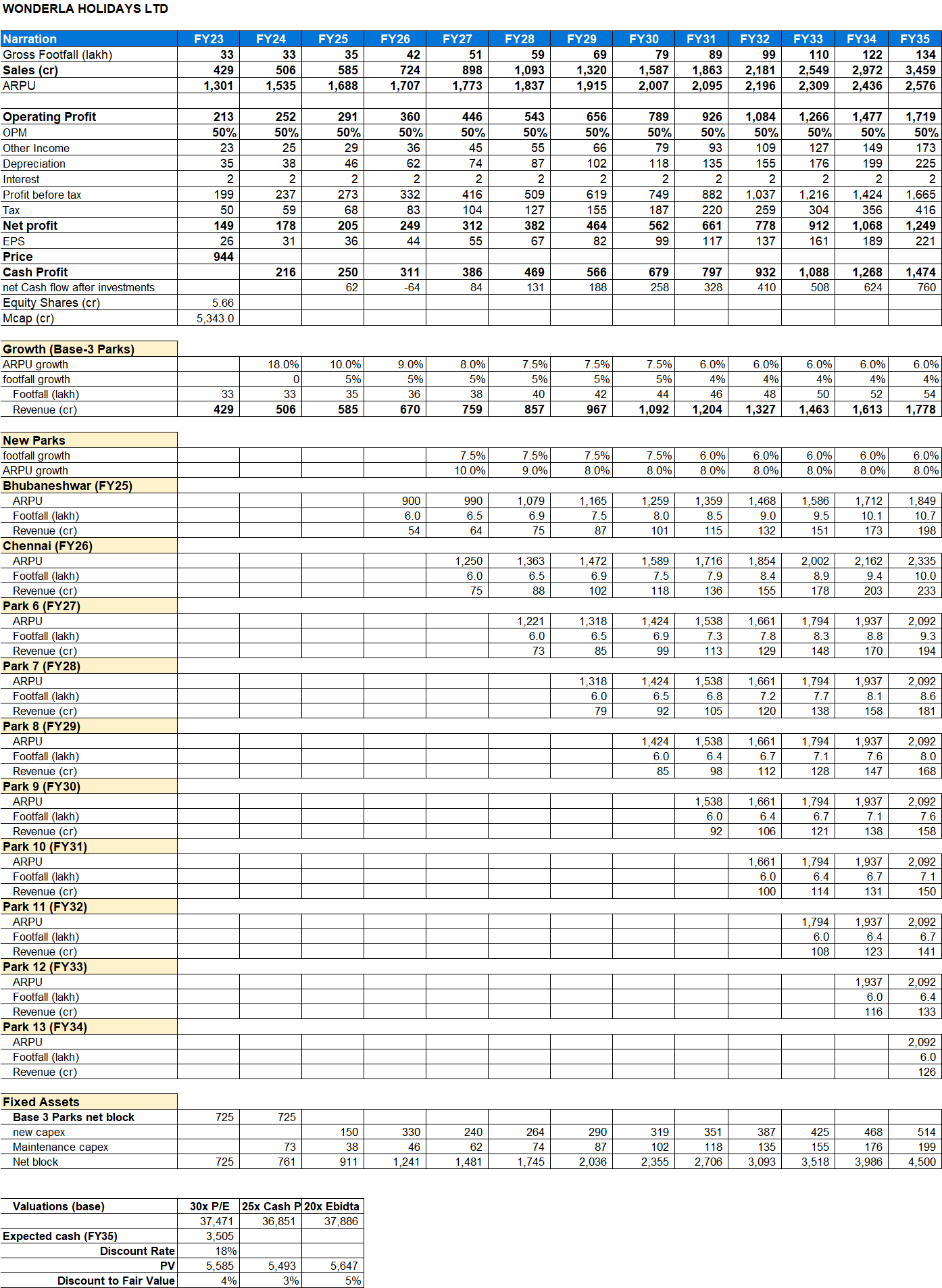

Hello all,

I did this valuation exercise for wonderla couple of months ago. This could be referred to assess potential returns over long term.

8 Likes

Wonderful, Kindly share the excel sheet also (If you are comfortable)

1 Like

Wonderla.xlsx (25.8 KB)

Excel sheet with workings on valuation attached herein.

7 Likes

Good work Saurabh. Just on ramup of footfalls it takes time to go 6 lakhs so you can prune inital year down a bit. Footfalls also degrow but anyways it can be managed by growth in non ticket spending

2 Likes

I agree. These are fair points.

1 Like

Do you think Imagicaa can be a threat to Wonderla? I believe currently it is fairly priced(Wonderla). And 2 more parks are in pipeline. I am holding the stock and planning to increase my exposure.

Thanks

i have studied Imagica early but not done much research after they went bankrupt. But i avoided that company purely as it looked debt was way higher for them to manage. Just avoiding high levraged companies helped me avoid a disaster. But recenlty some one asked me it was cheap and on pure mathematics it was way expensive then Wonderla. You can check on Imgica thread. Adding new parks is not very simple so we need to see if new management has some exp in executing such projects. Wonderla has unique strenghts which makes it win. Please see parks business is not new there were so many water parks in each city so it how to execute.

short term stock can go anywhere so do your own research.

3 Likes

hello, I have not done deep dive on imagica but on like to like basis I found their past in terms of financial performance as sub-par.