Thank you very much for the information.

What is ATP?

Thank you very much for the information.

What is ATP?

I would look at this strategy with skepticism. This business is a volume game - more the footfall better the revenues. Given the current economic scenario and the Indian demographics with low per capita income, prices cannot be increased beyond a limit else one risks losing footfalls.

On the existing 3 parks - the footfalls would remain stagnant, the focus would be to improve ARPU by price increase & more contribution by F&B. The ticket prices are still fair and affordable. So there is room for a price uptick. The parks seem to be heavily crowded during peak season and waiting in long queues and losing time is very irritating. So I would be a little skeptical about the comment that more rides would consume more capacity.

Volume growth will be triggered with the commissioning of the two new parks in Odisha & Chennai in the next few years. Visited Kochi & Bangalore parks in 2023, and was happy with the experience.

Disc: Had invested and booked profits in recent retrace. Prowling to re-enter again.

What is the market size for three parks (Bengaluru, Hyderabad, Kochi).

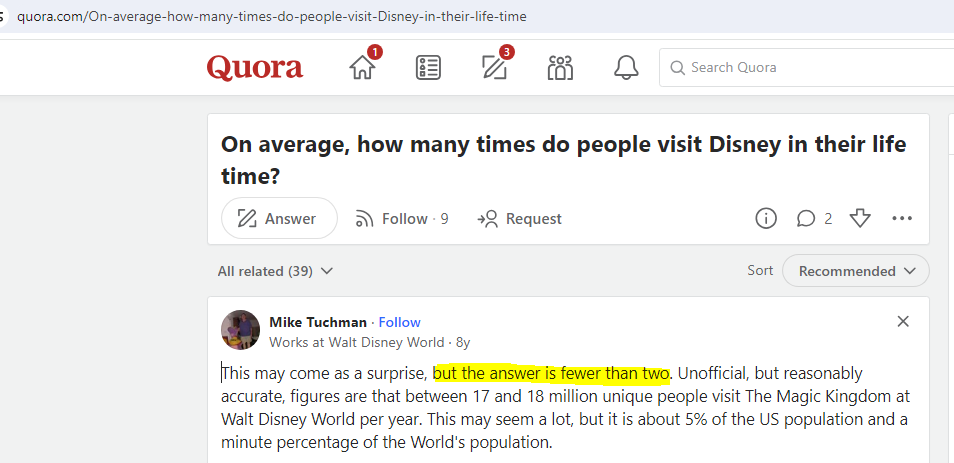

A person visits any amusement park less than 2 times in his/her lifetime (See the image below)

Although anecdotal, the conversations I engage in suggest that individuals (young professionals) tend to visit Wonderla multiple times. Consequently, gaining insights into the demographic distinctions between Disney parks and Wonderla parks holds significant importance.

In contrast to the substantial financial commitment required for a family trip to Disney, a visit to Wonderla does not exert a comparable impact on the overall budget, even at prevailing prices.

I think the demographic profile of Wonderla extends beyond family visitors to encompass other repeat customers, many of whom are employed professionals with disposable income.

Regrettably, I lack specific company statistics to prove these thoughts.

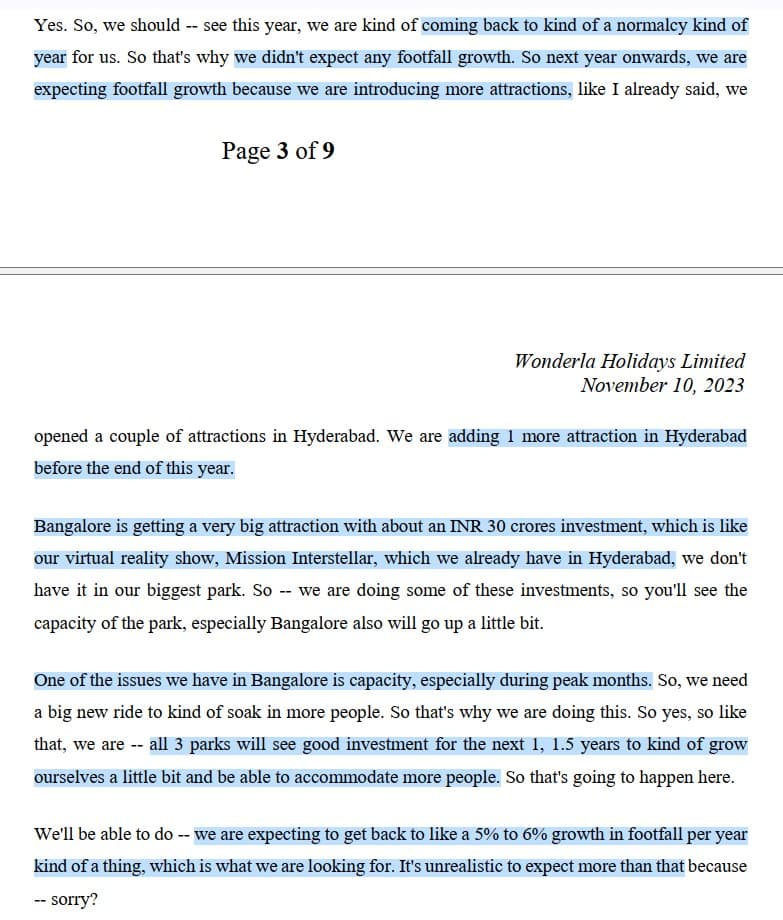

Madhya Pradesh and Punjab are expected to adopt an asset-light model. There is also interest from Ahmedabad, and a clearer picture of these projects will emerge after the elections.

New initiatives such as the Sunburn event and others are being introduced for post-evening activities. This marks a strategic move to extend the hours of operation beyond the standard shutdown time of 6 pm.

Hopefully, they will grow sensibly so they can maintain the quality and scale gracefully.

Similar experience at Bangalore park where I visited last week. That was my 3rd visit to the park and I find it great option to rejuvenate after busy workload, especially kids just love it. Amazing experience, very good footfalls and very well maintained rides. Food options have improved too. May be there are too many rides and difficult to cover in a day, they may start charging for either dry or wet rides or both, similar to water kingdom. Worth a visit and am sure their growth strategy to now penetrate towards T2 cities will work well.

https://twitter.com/shome_rajarshi/status/1740006575656587703

What you think?

Repeating what I tweeted.

Wonderla is fairly valued now-- Assuming 20% YoY Sales Growth & 36% PAT margin, 30x FY24 PAT= 30 x 185Cr = 5560Cr.

There won’t be a big jump in footfalls going forward.

Red Queen Effect in action! ![]()

Technically, the stock has dropped back into the channel.

Disc: Invested

To the best of my understanding the advantages of Wonderla includes:

The independent directors of the company including Mr. M. Ramachandran, Mr. R. Lakshminarayanan, Mr. Madan Padaki, Mr. K Ullas Kamath and Mrs. Anjali Nair are stalwarts in their own fields of expertise and the promotor family has done an amazing job in attracting the best of talent to the companies board.

Further we get comfort from books being audited by Deloitte and internal audit run by Varma & Varma.

Book keeping: The financial statements of this company clean and lean -the asset side of balance sheet has hardly anything other than fixed assets, investments and cash while equity including reserves form more than 90% of liability side.

The parks keep adding attractions year after year - be it additional rides, food/ beverage options, events including Sunburn or the facilities added to the resort - this keeps the parks fresh and help create new experience to returning as well as new visitors.

Ability to revise the price upward while sustaining footfalls: this is evident from the last two quarters and will act as a huge lever for the company.

Low cost operating model: The ability to build and maintain rides house is unique for Wonderla and this helps them keep the cost lower and meet the quality standards at the same time.

Land bank: All the three parks that the company is running currently has significant amount of land that is available for future development.

Adopting technology: The investment that the company has made in analytics to understand the customers better, online booking facility to help customers plan the visit in advance and automating business processes to run business smoothly has helped them immensely in recent times.

Ability to grow organically: It is impressive to note that many of the large Indian states are calling Wonderla management to set up parks and the company has hardly relied on debts for building new parks.

For me Wonderla is a low risk consistent compounder, they generate real cash and have plenty of opportunity to redeploy that cash for profitable growth - this business has significant longevity and as India grows the disposable income of its middle class will grow and outdoor entertainment facilities have very less probability of going out of vogue.

AJ

Disclosure: Invested in Wonderla. Opinion above is biased. Not a registered investment advisor.

As I am from South Kerela, let me add to the above: Many of the group, being school, college or family , planning for one day trip will eventually comes to Wonderla. Whatever options they have, eventually most of them will land in wonderla. This from my personal experience from School, College and Office. The probability increases if the group consist of different age group.

Even if they had gone once, they will come back to enjoy the moment with different people.

Disclosure: Not invested

Thanks for your note. What’s your rationale of giving 30xPE, if a company is sustainably growing revenues at ~20% and EPS ~30% (operating leverage)? First of all, why 30x to FY24 and not FY25. Assuming 30x multiple on FY25 earnings would imply market cap of ~7000 cr. To me 30x is minimum for a company with strong moat, high pricing power, sustainable earnings growth, ROE above 20%, zero debt and good corporate governance. With more parks to come, stock can easily give 30% CAGR if management executes well on its guidance.

Here’s my general view on the business.

The market had previously awarded a high multiple (45x iirc) to the business assuming the same secular growth characterstics, & the expected footfall growth didn’t come through for various macroeconomic reasons.

By management’s own admission, Hyd park hasn’t performed as well as they had hoped. So, how can we be sure the new parks will meet the growth expectations, especially since they are coming up in cities with less spending power than Hyd?

We are also assuming the new parks won’t face any cost overruns or delays like it happened with the Chennai park.

Also, 30x is me being conservative, assuming I have to exit the business during an overall market downturn.

That’s fine, but why would you give multiple to backward earnings and not forward looking earnings. One should always value business on 1-yr fwd earnings, 30x to FY24 would imply market cap of 7000cr or 40% upside.

Advanced booking on BMTC Volvo bus to Wonderla

Read more at: Advanced booking on BMTC Volvo bus to Wonderla

Not the opinion I hold. (I’m just looking 2 quarters ahead rather than 6 quarters as you sugguest)

If I’m looking forward, I prefer to do a 3 or 5-year exit multiple based reverse dcf on OCF/ FCF rather than just looking at 1 year forward PAT.

Ok, that’s your view, but general principal for market valuation and any multiple (PE, PB, EV/EBITDA) is always on forward looking basis - be it 1 yr or more, else why would someone worry about Earnings growth in future?

I agree with you on DCF, but my experience is that DCF is highly dependent on near-term growth and terminal value (say 10 years). DCF is therefore a good metric to value a company in cyclical industry or in matured phase but not high growth/underpenetrated industry like Amusement parks. May be 2-3 year forward earnings multiple is a better valuation metric for Wonderla, definitely not FY24!

Appreciate others comments as well.

It looks good but what about the future parks which are likely to be add one in a every financial year.?

In FY24 Orissa park,

In FY25 Chennai park,

Further in gujarat and other states??

When company is going with such huge capex in asset light model how you are giving the valuations based on only net profit?

Management is good, without rasing any significant debt they are completing the new parks surely tells about the quality of management.

If they are able to achieve the same 30% margins in the new parks also then defiantly it’s a 2-3 bagger from the current market price.

It’s a decent but even at the CMP.

Thank you

I would like to add a few points which could be useful to readers here:

An increase in ATP will mostly flow to the bottom line. As costs are somewhat semi-fixed. Now, with inflation both ticket prices and costs will increase but just imagine who could afford to spend 2k-3k/day on a full-day adventure? Especially when other adventure costs are growing crazy and there is a rise in per capita income.

F&B offerings will experience higher income along with a higher proportion. As footfalls increase, the increase in number of restaurants will be at a lesser pace. Also, if space is given for rent then the company can easily charge higher rent.

There are optionalities in terms of how many agreements they do in the asset-light model. Goa, Gujarat, MP, etc. all are ready to give out leased land. Imagine, Odisha took 100cr. to build a park with potential footfall of 5-6lkh i.e. on 800/ticket it goes to 40-48cr. Now tweak the assumption and add F&B offerings. Give comfortable margins as well here. Even if 30% OPM is achieved in Odisha it can generate decent ROI.

Chennai Park has very high CAPEX and I think this could only be a concern as ROI will be lower for years. So, temporarily (maybe 2 years) we have to face the pain of worsening return rations.

For years, the company had only 3 parks. Now it will soon have 5. If at all the pace of park addition continues this itself will be a trigger for sustaining valuation either at current levels or slightly higher valuations from here. (I have no comment on valuation as it is always subjective).

Hope it helps.

Invested at lower levels and hence following momentum-based approach to protect gains, so might not remain invested if price falls!

Regards,

Mukul Jain