The company has changed its business model to asset light strategy and collaborating with state governments for long term leases(90 years) for land which bodes well in opening up new parks and thus faster growth which was muted in last seven years.

8 Likes

Company is moving in the right direction .The recent coo hire Dheeran is ex zomatao , redbull and should be able to drive nps , cross sell and scaling up the business.

8 Likes

https://www.apnnews.com/wonderla-holidays-registers-several-firsts-in-this-blockbuster-quarter/

Bengaluru: Wonderla Holidays Limited, India’s largest amusement park chain, has announced its financial results for the first quarter of the financial year ended June 30, 2023.

Highlights:

• Highest ever quarterly Revenue, EBITDA, PBT and PAT since inception.

• Bangalore Park recorded 4.69 lakhs footfalls, Kochi Park recorded 3.19 lakhs footfalls and Hyderabad Park recorded 3.14 lakhs footfalls.

• Double digit revenue growth across units, driven by robust footfall numbers.

• Park revenue was up by 23% compared to Q1 FY23 and recorded ARPU of Rs.1,626.

• Resort Revenue was up by 10% compared to Q1 FY23

Quarter Update:

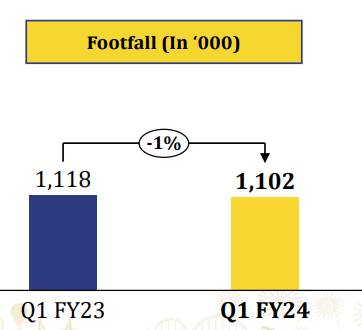

Footfalls for the first quarter ended June 30, 2023, were 11.02 lakhs, as against 11.18 lakhs during the corresponding period of the last financial year.

Gross revenue for the first quarter ended on June 30, 2023, was Rs. 190.27 crore, marking a 25% growth compared to Rs. 152.30 crore achieved in the corresponding period of the last financial year.

EBITDA for the first quarter ended June 30, 2023, was Rs. 122.50 crore, marking a 30% growth compared to Rs. 94.20 crore achieved in the corresponding period of the last financial year.

Profit after tax for the first quarter ended June 30, 2023, was Rs. 84.47 crore, marking a 31% growth compared to Rs. 64.38 crore achieved in the corresponding period of the last financial year.

Business Outlook:

Commenting on the performance during the quarter, Mr. Arun K Chittilappilly, Managing Director said “With an accumulated footfall of 11.02 lakhs in the first quarter of FY 2023 and gross revenue amounting to Rs. 190.27 crores, Wonderla’s performance speaks volumes about its resilience and commitment to delivering unparalleled entertainment experiences. Since our parks were already operating at capacity during Q1 FY 23, our efforts focused on enhancing ticket prices, boosting non-ticket revenue, and attracting a larger share of retail footfall. Our primary focus was on cultivating higher-spending retail customers as opposed to groups. The consistent growth, along with record-breaking financial achievements, positions us for a promising business outlook. The company’s relentless dedication to innovation, quality, and customer satisfaction sets the stage for further expansion and success in the quarters to come. Our solid financials and the ability to adapt to changing market dynamics make us a formidable contender in the amusement and entertainment sector.”

2 Likes

In the most recent presentation, we find that both Kochi and Hyderabad have had lower footfalls (though with higher profits). Overall there is a marginal drop in footfall.

Combined

Kochi

Hyderabad

I am surprised to see this. Can others weigh in on this? Hopefully this will be discussed in the upcoming concall.

Based on the management commentary there are 2 reasons

a) The June quarter has the peak footfalls during the year, the baseline of Q1 last year did not leave a lot of room for expansion.

b) They are changing the mix in terms of individual customers vs group bookings ( reflected in ticket ARPU also, since the price increase was to the tune of 10% while ticket ARPU increase is to the tune of 20%) So assume the discounting has gone down.

Going forward- this year they have planned CAPEX of ~90 Cr for existing parks alone and I see that with time they will add rides and increase effective capacity of the parks

5 Likes

To repeat (for my understanding):

They are trying to optimize the customer mix for greater profitablity.

Going by this, even with just the current space they have, there is room for future growth and profit.

Thank you @baniyainvestor

This kind of sales model improvement is great to see.

1 Like

Agree Sunray!

Moreover Q2,Q3, Q4 would be a good test to check if there is a room for footfall growth- if it comes due to the operating leverage full year profits could be a lot better this year

I wonder if increased footfall would mean more wait times, more overcrowded experience and thus increased footfall might be ok up to a point but revenue growth per ticket should go up for future growth and profitability. More parks would be a better way to improve revenue than increasing footfalls for ever. Maybe they will have differential pricing for peak and non peak timing to smoothen the visitor flow through the parks/rides.

They do have differential pricing for peak/non-peak hours. Also like most parks they have a Fast track ticket more like all global parks - Not sure though what % of tickets are sold in the fast track category since the price is 2x… What I am not sure is if charging a 40-50% premium is better vs 100% premium

Disney’s saving grace lately has been their parks. Also their highest growing segment is personalised service for park where family of 4 would normally spend $1000 and wait time for popular rides will be 1-3 hours. Whereas this personalised service - price tag of $5000-$6000 - they can zip thro rides with 2-3 minutes wait. It also comes with dedicated guide and special cart to roam around in the park

All premium segments - travel, shopping, automobiles - is seeing crazy traction

2 Likes

Wonderla Holidays Q1 concall highlights-

Current Portfolio-

03 theme parks-Bangaluru, Kochi, Chennai

01 Resort

Portfolio wise performance in Q1 -

Bengaluru park -

Sale-80 vs 60 cr, up 34 pc

Footfalls-4.7 vs 4.2 lakh, up 11 pc

Avg Ticket Price-Rs 1323 vs 1075 cr, up 23 pc

Non ticket revenue-Rs 396 vs 350, up 13 pc

APRU-Rs 1720 vs 1420, up 21 pc

This park has 40 land slides and 21 wet slides

Bangaluru Resort-

3 Star property, 84 rooms, suitable for wedding receptions, parties etc

Revenues-5.3 vs 4.8 cr

Occupancy-69 vs 80 pc

ARR-Rs 5888 vs 4891

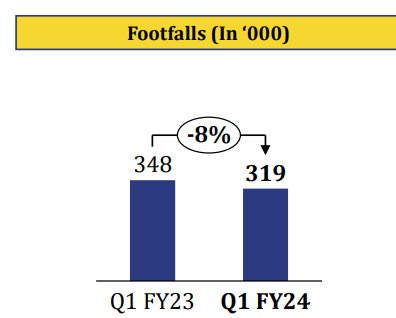

Kochi park -

Revenue - 47 vs 39 cr, up 20 pc

Footfalls - 3.2 vs 3.5 cr, down 8 pc

Avg Ticket price - Rs 1145 vs 882, up 30 pc

Avg non ticket price - Rs 326 vs 244, up 34 pc

ARPU - Rs 1471 vs 1126, up 31 pc

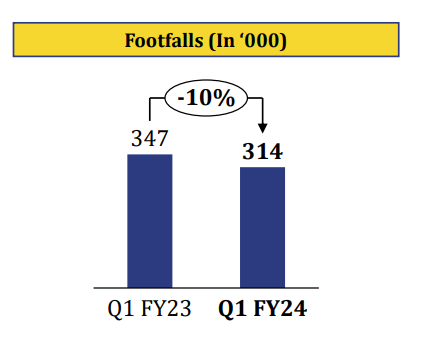

Hyderabad park -

Revenue - 51 vs 46 cr

Footfalls - 3.1 vs 3.4 lakh

Avg ticket price- Rs 1224 vs 986, up 24 pc

Avg non ticket price-Rs 418 vs 338 , up 24 pc

ARPU- Rs 1642 vs 1324, up 24 pc

Consol results-

Sales- 190 vs 152 cr, up 25 pc

EBITDA- 122 vs 94 cr, up 30 pc

PAT- 84 vs 64 cr, up 31 pc

Company running 15 restraunts across 3 parks

4th park to come up next FY in Orrisa

Recieved regulatory clearance for Chennai theme park. Construction to commence soon

Have signed MoUs with UP, Punjab Govts for construction of new theme parks. Expect some announcement wrt expansion this FY

Company remains debt free

Fall in footfalls (YoY) in Kochi, Hyd- due pent up demand post COVID in Q1 LY. Bengaluru remains far more bouyant because of greater per capita income and population density in the region

Hence, not worried about footfall de-growth in Hyd, Kochi

Refurbishment/Expansion to take place at the resort in Bengaluru. Adding 2 new Bars, 40 rooms, 01 convention centre

Looking to build new resort in Hyd-work may start sometime next FY

Growth in Non-ticketing revenues due various initiatives taken by company wrt its F&B offerings

Confident of achieving 5 pc footfall growth this FY at the company level

Aim to go for lease models for further expansion into newer states. Size of the park to be commensurate to the size of opportunity - eg - a smaller park in Indore vs larger in Ahmedabad

Spending 70 cr on maint capex and adding 5-6 new attractions to all three parks this yr

Should be able to complete Chennai park construction by June 25

Chennai park to have at least 30-40 pc different slides / experiences vs the Bengaluru / Kochi park

Aim to achieve 15-20 pc revenue growth for full FY

Company’s equipment is either European or made in India. No equipment is Chinese

About half of the land is un-utilised in the existing 3 parks - have huge headroom for expansion if demand dictates so

Disc: holding, biased

15 Likes

Should be able to complete by June 2025?

Here is the latest company filing

Hope this helps.

They are going to start the construction. But have not mentioned any deadline for opening of the park.

2 Likes

Results out for last quarter.

Investor presentation attached:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b7ef3123-bd7a-4867-af57-1937d6d8ae86.pdf

2 Likes

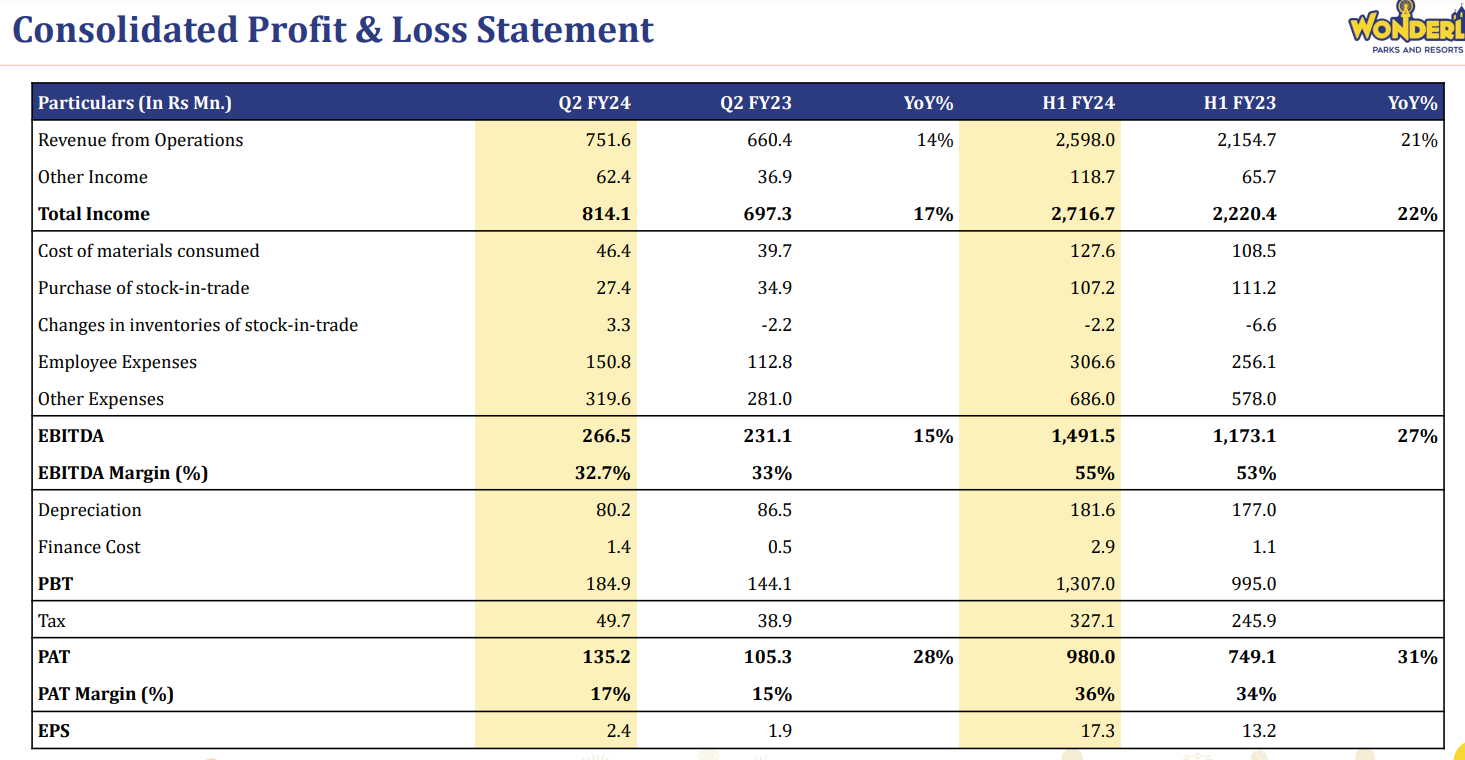

My takeaways from Q2FY24 earnings call:

Revenue growth

Immediate growth is expected to be flattish. In long term, the mgmt expects to double the visitors in 8 years, which would be about 8-9% growth YoY. On top of this, ARPU growth is around 10%, which would give a sustainable revenue growth of about 15-20%.

Hyderabad had a slight degrowth. The mgmt mentioned that they will be focussing on being more aggressive for Hyderabad.

Expansion across regions should add more to topline.

Margins

Margins seem to have recovered back. EBITDA margin is at 55% and PAT margin is at 36%. There might be a slight dip going forward as the company implements more aggressive marketing and customer acquisition activities.

Capacity expansion

There are continuous capacity additions planned for existing parks, including new rides & attractions. Bangalore capacity is expected to go up in the next 1.5 years.

On new projects, 48 and 113 Cr is spent in Odisha and Chennai respectively. Odisha is expected to come live by June 24 and Chennai by Aug 25.

Just signed an MOU with Gujarat govt.

Talks are also going on for MP, UP and Punjab.

At current rate, one park will be added every 18 months going forward.

Key risks

- Natural disasters / pandemics etc.

- Accidents that would negatively impact the image (risk increases with increase in capacity)

- Economic slowdown (seems unlikely as of now)

Investment hyopothesis

- Trust worthy and investor friendly management

- Sustainable revenue growth of 20-30% can be expected as baseline

- Secular growth story as middle income group grows

- Margins would keep improving as more parks are added

- IMO, the scope of marketing is not yet tapped. So, need to watch their marketing activities and spend (google trend is slightly inching upwards). If it is unlocked, then they will be able to deal with lean periods more effectively.

Disc: Invested

11 Likes

In the risks category, what about scalability of management and quality of service. In contrast, Disney has huge parks and they can concentrate their management bandwidth on these few parks. However, if Wonderla has 6-7 parks in the future compared to the three now, then how would they ensure that the management of these parks and quality of service in these parks are maintained. Probably this risk is not as high but i hope the top management can execute these parks well with good incentives for the management as well as the employees to ensure good quality.

1 Like

Thank you for the crisp summary @shyamdsundar. I have a couple of doubts:

- Do you think the increasing capacity in existing parks can increase the footfall in the park?

- I am not sure how margins would improve if new parks are added as they are totally independent of each other. Each park will have its own staff, equipment, maintenance, etc.

There are typically two problems to address since this is a very seasonal business: (1) handling lean periods through marketing efforts (2) handling peak load with capacity expansion.

The guidance is about 5-6% annual growth in traffic. However, there is some scope to improve footfall in Bangalore during peak season. Should be a delta over the normal growth rate.

They are also trying to improve marketing spend on hydrebad. This should also help improve the footfall there.

Relevant section from earnings call below:

Wonderla manufactures its own rides and equipments, which would be better utilised with more parks added. Furthermore, with scale, I expect more efficiencies in the marketing spend, branding, overheads, process implementation etc. Having 3 parks vs 6 parks will be markedly different in the way they operate and scale out. But, I do agree that margins are largely independent between parks.

This is a good problem to solve. So far, the management seems to be adept in maintaining the growth. They also are constantly hiring which should help with the expansion.

9 Likes

Few observations from my visit to hyderabad park last weekend…

- F&B offerings have increased with new stalls everywhere around the park.

- Focus is on increasing ATP rather than footfalls which shows the co is moving towards premiumization.

- Introduced evening park entry from 4 to 8.30 PM in this holiday season where DJ, live band and other entertainment is being served.

- 2 New water rides introduced - Rainbow loop and drop loop, both are fab experience.

- Huge crowd - Its a blessing in disguise for people who want to go for vacation but could not make it due to expensive holiday season all over india.

20 Likes