Disney did want to do some business in India, and I think it was about parks, but this was almost 20 years ago. They may have found it loss making so this plan got dropped. As India has changed much in the past 20 years, they may try again.

And Disney being Disney, quality with a price tag, so not many may not afford to visit Disney and look for other options, with Wonderla a first choice.

Even if everyone flock to Disney to have a Disney experience, the delays for each ride may not be acceptable to all, even with special bands, and people may have to book weeks in advance, and if they don’t want to visit on that date, there may be a refund or may be not. So they may choose Wonderla or others if they are readily available. I guess there are many moving parts.

Folks, to put things into perspective Wonderla did a PAT of about 150 Cr last year and is likely to maybe grow to 400-500 cr in the next 5 years. Not sure if this is something that would make large companies jump off their chairs ( <$100M).

Also, Wonderla has been built on a very astute understanding of the Indian customers in terms of offering and pricing - not sure if it is so easy for lets say a Disney to replicate and disrupt.

Disc: Invested in own, family and friends accounts - highly biased

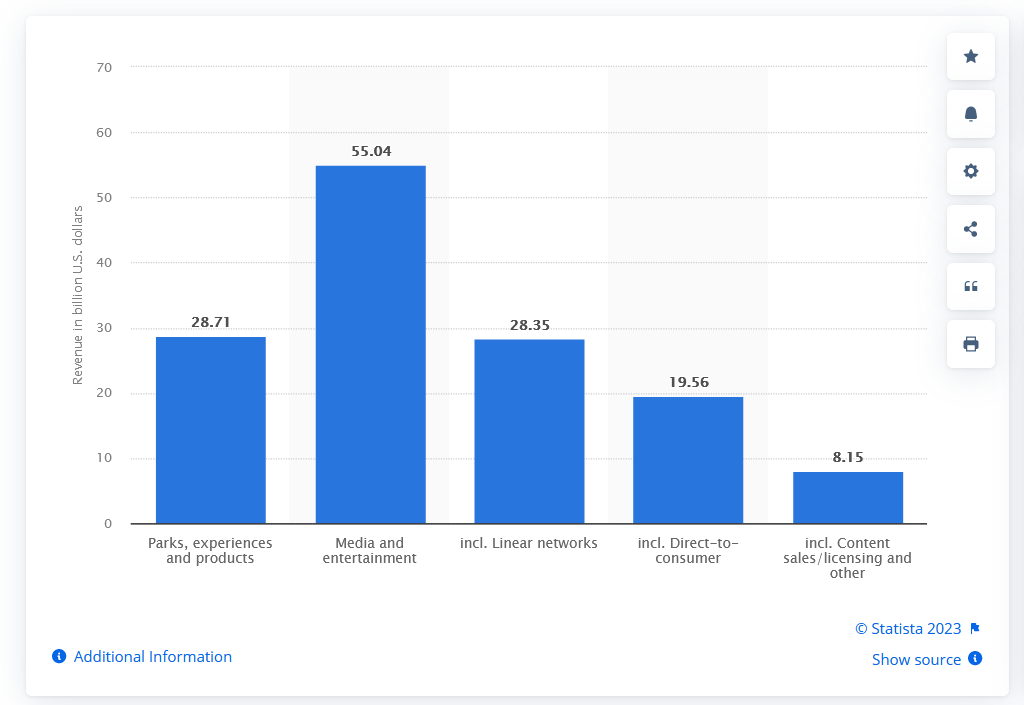

Super to hear people talk about Wonderla and comparing it to Disney. I thought it would be helpful to look at the Disney numbers, please do verify and research Disney a bit more if neccessary.

The numbers are a bit dated so some mental extapolation will be neccessary:

The Magic Kingdom Park in Bay Lake, Florida, ranked first in 2015 with 20.49 million visitors.

Parks and resorts were the second-largest revenue source, generating a total of 16.97 billion U.S. dollars. It is a very successful segment – Disney’s parks take places 1 to 9 in the ranking of the most visited amusement and theme parks worldwide. The Magic Kingdom Park in Bay Lake, Florida, ranked first in 2015 with 20.49 million visitors.

Tickets:

A one-day ticket to Disneyland in China costs 499 yuan, or about $76. For comparison, a one-day ticket to Disneyland in California costs $110.

Food: You can expect to spend around 200 yuan, or $30, on food per day at Disneyland in China.

Not just Disney, I was thinking of Indian conglomerates. Just like Grasim is trying to shake up the Indian paints industry, what if another company decides to get into the theme park business. However, as of now there isn’t a Wonderla equivalent. Also, Disney has one theme park in all of China if I am not mistaken. Please correct me if I am wrong. I am not sure one park will dent the appeal of the current customer base of Wonderla who might be visiting from the same state. Perhaps, it will be insightful to see what percentage of walk-ins are in state vs out of state.

The question of risk from larger parks is not going to emerge in the near term unless some one is ready to burn significant amount of cash like the way Adlabs(Currently called Imagicaa) experimented in Pune. The price point of larger parks is just not affordable for the common folks currently.

Even recently i have come across comments on social media criticizing Wonderla’s pricing! - i honestly dont think we have anything better available at this price point in India at this time - land rides, water rides, wave pool, fun for kids and good food - that’s a whole day of fun and excitement at less than Rs. 1500 per head. Imagicaa charges roughly double this for a day and still struggling to turn profitable.

I don’t believe any of the international players including Disney/ Universal Studio or the likes will be happy to plunge until our countries per capita GDP moves >$5K – India still struggles at <$2.5K(see the list here.). Wonderla should continue to implement its tried and tested model in new parks and grow its business slow and steady the way they have done over the years. Big players will eventually come in at some point in time in future - i believe by the time the global biggies move in, the best choice they would have would be to associate with or buy out Wonderla.

All these points are FINE. But what about the valuations?

Though a small cap, at P/S of 7, this looks very costly.

Can someone compare it with Disney on this P/S metric? As per my search, Disney trades at a P/S of less than 2. But not sure about Disney’s P/S only for the theme parks. Can someone share it here?

Regards,

dr.vikas

In terms of valuations I find it to be extremely cheap even after the current run up. Wonderla trades at a trailing P/E ratio of 20 times and has a visibility of earnings compounding of 20-25% over the next 3-4 years.

All well governed consumer facing companies typically trade at a valuation that is much higher than 20 given the typical justifications i.e. Low penetration in India, very long runway for growth , high terminal value, High ROCE etc.

Wonderla has all the above attributes and has a potential to command significantly better valuations going forward.

Disc: Invested in own, family and friends accounts - highly biased

While studying Wonderla, I had the same same concerns on the competion aspect - why not a global player like Disney cannot setup a park in India. Have read that it is not viable for Disney to setup a park in India in near future due to the premium it demands. So cannot expect this competition coming in this decade.

Had visited Wonderla, Kochi in Jan, 2023. Their services are good and there is the impact of revenge tourism accelerating the revenue this year. Recently one of my colleagues visited Bangalore wonderla and he told me that the prices have further increased and there is still crowd. I would anticipate the Q1 results should also be great, considering summer holidays and school vacation.

Disclaimer:

Invested, biased. Momemtum pick. Will hold until the narrative is rosy. Im a novice in equity investing. Do not do deep financial analysis. Got convinced with the improving metrics like footfalls and avg revenue per footfall and capex on new parks. Management also seemed to be good (sources: Interview videos, concall transcripts, Qtryly reports). Tries to follow peter lynch’s principles.

IMO such businesses see India in 2 parts. Top 5% of population (7 cr) and balance 95% (133 cr)

The top 5% population earns 80-90% of GDP (don’t recollect where I read this). Cred also targets the top layer.

With further growth the clusters of top 5% might attract bigger players. Many Indians spend thousands of rupees to visit Disney/Universal studios across the world. If similar experience is available India people will pay.

The expansion plans of Wonderla foraying into other cities excluding Mumbai, Pune, Delhi, and Kolkatta showcase the stiff competition from local unorganized companies where price sustainability is poor and eventually being defunct over the years with poor attendance.

The entry fees of competitors(Rs.500-Rs.1000) in Maharashtra, Delhi, Pune, and Kolkatta to WonderLa (Rs.1500 and above) in Hyderabad, Bangalore, etc. show the competitiveness of this space.

Coming to Disney’s point of view to invest in India

It requires consumers to spend Rs.8000 and above per head and a head count of above 15 million per year. The company does not see India as a potential market for its growth for the specifications cited above.

Lowering the entry fee to suit the country with the investments and the experiences remain the same as the other parks in the world which make the profitability a far cry.

Joint venture or tie-up with Indian players, thereby reducing the investments for a park maintaining the same experience by setting up Disney park making it a win-win for all ( Disney, WonderLa/ Imagica (say) and consumers).

In a joint venture, the average ticket price could be Rs1500+ Disney park Rs.1500 which would be less than Rs. 8000.

Top/ High branded MNCs have had their share of India by adapting to Indian conditions.

Examples of successful MNCs are

Mc. Donald’s ( Franchise model and adapting to Indian local tastes to grow)

Tata Starbuck’s ( JV) expansion beyond the top 6 cities (Tier 1) shows the new avenues for growth to suit the Indian markets.

The question that remains is not whether Disney would come to India but whether India can afford Rs. 2500 to Rs.3000 ( assume to be the least) per head per park.

Conclusion:-

Disney foraying into India is far exaggerating the future as there are very few companies that are profitable in this space. In such a scenario the amusement parks need more maturity on

price sustainability:- the demand to override the price,

profitability, and longevity of the parks.

Can you please guide me on how to check the website traffic? It would be really helpful to sort of track this thing monthly and especially on event days.

You can use similarweb for website stats- Y-o-Y increase I accessed using a premium subscription. The free/open version will give you website hits over the last 3 months.

Even if Disney does come to India, which it doesn’t seem like it will in the near future, Wonderla will still be the best option among the regional competition as Disney is not going to have too many locations in India. It might have one or two huge parks for all of India, whereas Wonderla can have one per every state it wants to venture in. So, this seems like a win for the Wonderla brand. However, can they scale well?