I think third-party, anecdotal, personal (and somewhat outdated) experiences maybe avoided in judging the company’s fundamentals/ investment value. No personal offence intended. I’d personally visited the park in 2019. The hygiene & cleanliness standards even then were very high, one could have roamed throughout the park bare-feet comfortably (very few people did). Food was excellent in taste, high quality and quantity at a very economical price. If I remember right, the company operates all in-park restaurants since 2018, which led to increased margins & non-ticket revenues since then. There are no outside third-party restaurants like Papa Jones anymore. I’d also stayed at the resort, the hospitality, comfort & facilities there were at par with what I’ve experienced at some of the Mariott hotels, albeit at a lower price.

If people are crazy and it continues to attract crowds, regardless of the hype deserved, it will accrue value to investors

Wonderla Holidays has announced reopening of the theme park in Kochi starting December 24, 2020. Visitors can enjoy a special reopening offer of Rs. 699 inclusive of GST, with access to all rides, unlimited times. The park will be open everyday during festive period from 24th December 2020 to 3rd January 2021 from 11 am onwards. As per the guidelines issued by the Government of Kerala and the Ministry of Health, Wonderla in Kochi will operate at a reduced daily capacity

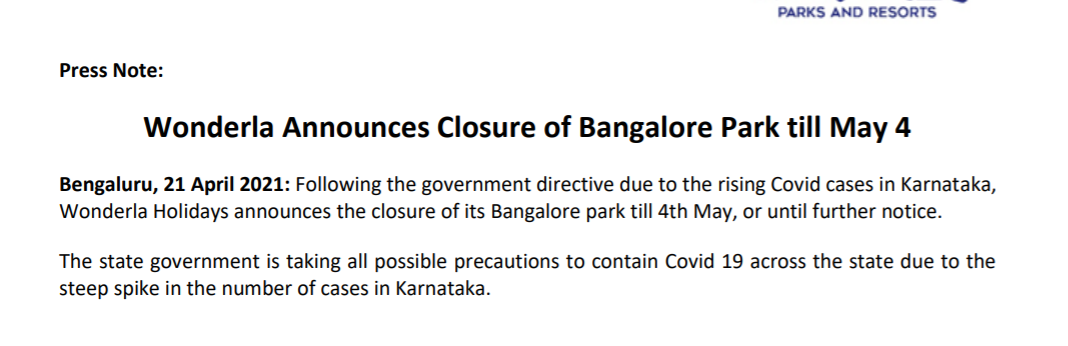

This is very alarming. If this gets into litigation mode (which mostly happens when expectations of local authorities are not met), it can take too long for it to open and still there could be frequent issues. Let’s see how this pans out but definitely doesn’t look very encouraging.

Good part is covid is still there and it anyways doesn’t make much sense to operate the part at very thin capacity utilization levels.

Disclosure: Not invested. Only for educational purpose. Personal views.

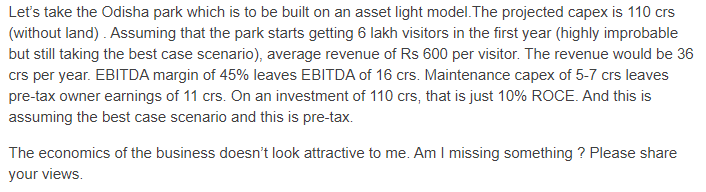

Think about it for a minute, what was the ROCE at the point of time when Cochin Park and Bangalore park were built? Check the data and I believe you will see it was not any different from your analysis of Chennai and Odissa Park currently.

How the ROCE has changed for mature parks over the last 10-15 years, is something to look at, I think that’s a better way to look at how economics of business has developed over time.

Will the same be replicated for new parks is the next question for the investor to think about?

If you look at the capex at insolation then yes it seems a low ROCE business but let’s see what Prof. Sanjay Bakshi does.

In his podcast & Relaxo lecture, he mentioned that don’t take Capex or advertising expenditure as whole just in one year. Rather treat them as how you treat depreciation.

He mentions:

Think about Owner’s earnings as true earnings.

Like Geico has been spending a lot on advertising on a business model which is growing and is taking away market share, should not be treated as advertisement. only then you get the true earning power.

Same goes for capex he mentions.

So, if we take capex as 10% of total amount getting to zero at 10th year: Rs11cr

Just wanted to tell that I spoke to some people who are familiar about the company. They mentioned that footfall levels havent reached pre-covid and its going to take a lot of time, the ticket prices too has reduced.

So Q3 & Q4 results are not going to be encouraging

It is safe to assume that. fy22 could also be washout. Wonderla could clock at. max 60% of fy20 revenue in fy22. How ever there are one positive out of this- if wonderla can comeback after two years of limited operation- isn’t it sign of survival of fittest and shows moat, strong balance sheet ?will it be winner takes all in India’s amusement park industry?

Given the news in the US about opening up and how Disney is fully booked for weeks, I wonder if that trend will rub off in a good way for Indian firms like Wonderla and hotel chains and the likes? i know we cant see the run away growth at this stage, but i guess it would take lot of guts to buy into these firms at this stage.

Wonderla has >100 crore cash in the books. They are able to manage all the expenses with 10-12 crore INR a year for their permanent and augmented staff.

There is a huge cost to setting up a new amusement park. Disney ruled out India as they spend around 25000 Crore to setup a park and it is not viable in India. Wonderla has used

They have ~60% of their land area in amusement parks unutilized. They have setup a resort kind of stay-in place in their Wonderla Bangalore place

They are also starting Wonderla kitchen in lockdown to get some revenues

Ethical management. Does not get better than this

One of the sons who runs this (other runs V-guard) choose this as he wanted to setup something on his own

Company has 0 debt

Negatives:

FY22 could be a washout as well. In this era where people are afraid to get maids come into their house, full opening seems a long way out

I think Wonderla is a buy at these prices but if corona lockdown continues and the broader market corrects, we could pick this up lower close to 120-150 INR levels. That is the thing holding me back. Because even if normalcy comes 3 years from now (in the worst case), the stock can re-test its highs of 300-400. If I buy at 120-150 INR and sell at 350-400 INR in 3 years, it is an excellent CAGR. IMO, we can get better prices on this

Well unfortunately I do not agree with you - the problem of the company is not the financial statements but the family feud and inconsistency in the management. The high of 300-400 was reached under the professional leadership of the CEO - D S Sachdeva. Who despite stellar performance resigned in just over 2 years. Revenue grew from 180Cr to around 270 Cr. There was a complete rebranding, with a professional upper management and opening of the third park.

I think he left because of family tension between the son managing director - Arun Chittilappilly and Father Mr Kochouseph Chittilappilly. They basically removed all the upper management in 2018. And Mr Arun left for a sabbatical for 2 years. Revenue is flat/declining. Wonderla stock has been declining long before covid. I think it will never reach 300-400 high with current family run attitude-they need a professional team for that to happen(like Mr Sachdeva). I bought 400 shares in 2015-after looking at positive strives toward a professional upper management- I sold in late 2017 after resignation Mr Sachdeva. Mr Arun Chittilappilly can not run it effectively he should appoint a new CEO - then I would consider investing in Wonderla Holidays. https://www.linkedin.com/in/d-s-dipy-sachdeva-3105081a/?originalSubdomain=in

Great points. Your post makes a rather convincing case to stay away from this company. Not many know that the son was on a sabbatical. Definitely out of my consideration list now. Thanks for sharing.

But now that Arun is back shouldn’t Wonderla work like previously managed company? I believe he was part of the journey right from the start and was Managing Director for 15 Long years.