Also can we get the news source saying the sabbatical was due to a family dispute and not another valid reason?

As per this document, he was supposed to be on Sabbatical for 3 months but eventually came back after 2 years, Its not mentioned anywhere why was it done though.

1 Like

Here are my notes from their concall and CNBC interview.

- Footfalls recovered to 77% of pre-covid levels (Q4FY20) across parks

- Salary cost is ~1cr./month, have been able to bring it down by 30-40%

- Chennai project put on hold until the end of FY22

- Not looking for inorganic opportunities for now

- Evaluating newer opportunities in Gujarat (Ahmedabad) and Colombo. Colombo is to take over a semi-finished park, finish and operate it (still early stage)

- Bhubaneswar park will be much smaller in size and require lesser investment compared to current parks, currently under the drawing board

- Theoretically, each park has a capacity of 8’000-10’000 people per day. But actual achievable is 5’000-6’000 visitors per day

- Look for a payback period of 7-8 years on each investment. Hyderabad park required 3-years to break even on EBITDA level

- Scaled back wonder kitchen

Disclosure: Invested

10 Likes

Been researching and tracking Wonderla for sometime, some thoughts-

1.Last three year performance although not great, have a no. of caveats attached, GST imposition, Bangalore and Kochi had higher than average rainfalls and subsequent floods, Sabarmati protests, Nipah virus, and covid, all in the space of three years.

2. The Kochi park has seen the fall in visitors,and thats expected given the age of the asset(20yrs),the management should have done a better job of monetising the land assets, to keep the visitors coming back.

3.Since FY18 (post GST imposition and revisal of rates), parks have seen improvements in the peak season, despite incremental increases in avg ticket prices, while IMO the fall in the off season has been more to do with rainfall.

4. Given the older assets seeing lower footfall,and higher cost of acquisition for newer parks, focusing on monetising existing land banks should be a priority, with a brand already established in these markets, getting customers back would be easier.

5. The nature of the business is such that they face some or the other problem every year, be it rainfall, protests, virus outbreaks, etc… The valuations should take this under consideration

Disc- Not Invested but tracking closely. Unsure on the valuations, given the risks.

p.s.- I have recently written a detailed article on Wonderla Holidays which you can read here-Wonderla Holidays Ltd - by Hemant Bubna - Value or Trap

1 Like

Signs of revival??

- Despite being operational for few weeks, wonderla came with decent numbers.

- Bottom line may be in negative but giving very positive indications.

Highlights of Q2FY22

- The second wave of Covid-19 impacted Q2 operations. All the parks remained closed till August 2021. Hyderabad Park reopened on 5th August, Bangalore Park on 12th August and Kochi Park on 1st September 2021 respectively. Bangalore Resort opened on 5th July 2021.

- Gross Revenue for the Second Quarter ended September 30th, 2021 was Rs. 18.32 crores over Rs.1.76 crores during the corresponding period of last financial year.

- EBITDA loss for the Second Quarter 2021-22 was Rs.2.38 crores against loss of Rs.7.57 crores during the corresponding period of last Financial Year.

- Loss after tax for the Second Quarter 2021-22 ended 30th September 2021 was Rs.9.28 crores as against a Loss after tax of Rs.15.79 crores during the corresponding period of last Financial Year.

- In the Second Quarter 2021-22, the Company achieved a total footfall of 1.48 Lakhs against Nil Footfalls in the corresponding period of last Financial Year (parks remained closed on account of COVID-19 Pandemic first wave).

- Resort achieved 23% occupancy during the second quarter of the Financial Year 21-22.

Commenting on the performance during the quarter, Mr. Arun K Chittilappilly, Managing Director said, “The parks were shut down in the mid of April 2021 due to the second wave of COVID-19 pandemic and the revenue was impacted. During the 2nd quarter, Hyderabad Park was opened from 5th August and Bangalore opened from 12th August whereas Kochi Park opened only on 1st September and was functional only from Thursday to Sunday in the opening month and achieved a footfalls of 1.47 L visitors.

With thanks

Be and Make

3 Likes

Surging of fears about OMRICON seems to be a big set back for wonderala for short term.

There may not be a lockdown but people hesitate to travel.

Let’s see how things will pan out.

With thanks

Be and make

2 Likes

Here are my notes from the past few management interviews.

07.09.2021 (CNBC interview)

- Breakeven at ~1000 people/day/park

11.11.2021 (CNBC interview)

- Average ticket price has increased from 780 in Q2FY20 to 840 in Q2FY22 (open question: is it due to higher contribution from Bangalore over Kochi??)

- Marketing spends are lower compared to pre-pandemic as marketing has shifted to digital mode which is lower cost

- Hope to be profitable this quarter (Q3FY22)

05.01.2022 (CNBC interview)

- Resort breaks even at 25-30% capacity and company is doing way better than that

- Q3FY22 realizations were highest in company’s history

Disclosure: Not invested

5 Likes

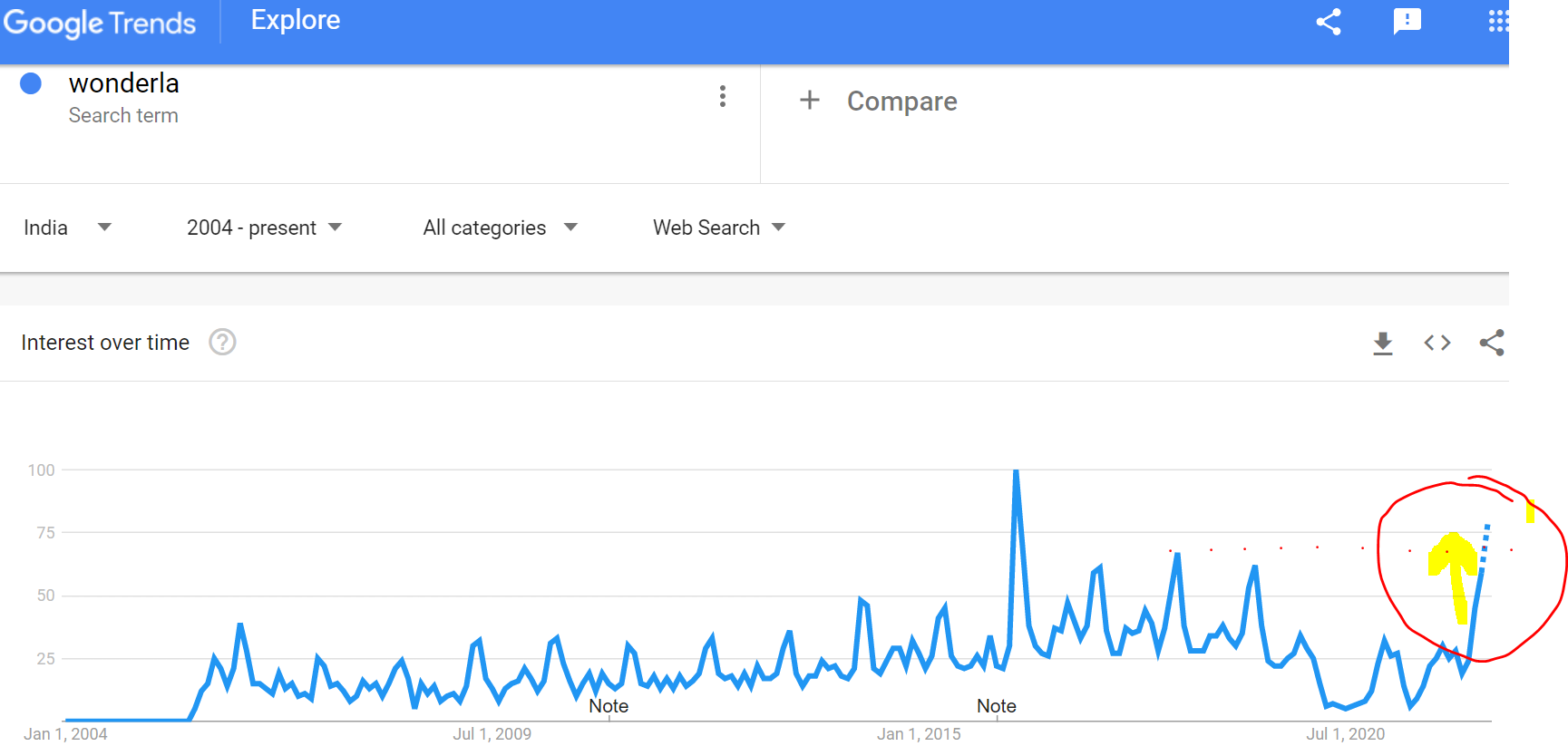

Looks like the interest is back in Wonderla - at least that’s what Google trends is suggesting - have a look.

Google trends

Company did not raise funds or dipped into leveraging during the covid times. Good times seems to be back and what they learned during the lean period should help them do better going forward. Really like the management and hope they do some innovative advertising and capture the imagination of its target customer base. If the Google trends is anything to go by, Q1 2023 will be their best ever quarter.

Disclosure: Entered today. Consider my views as biased.

9 Likes

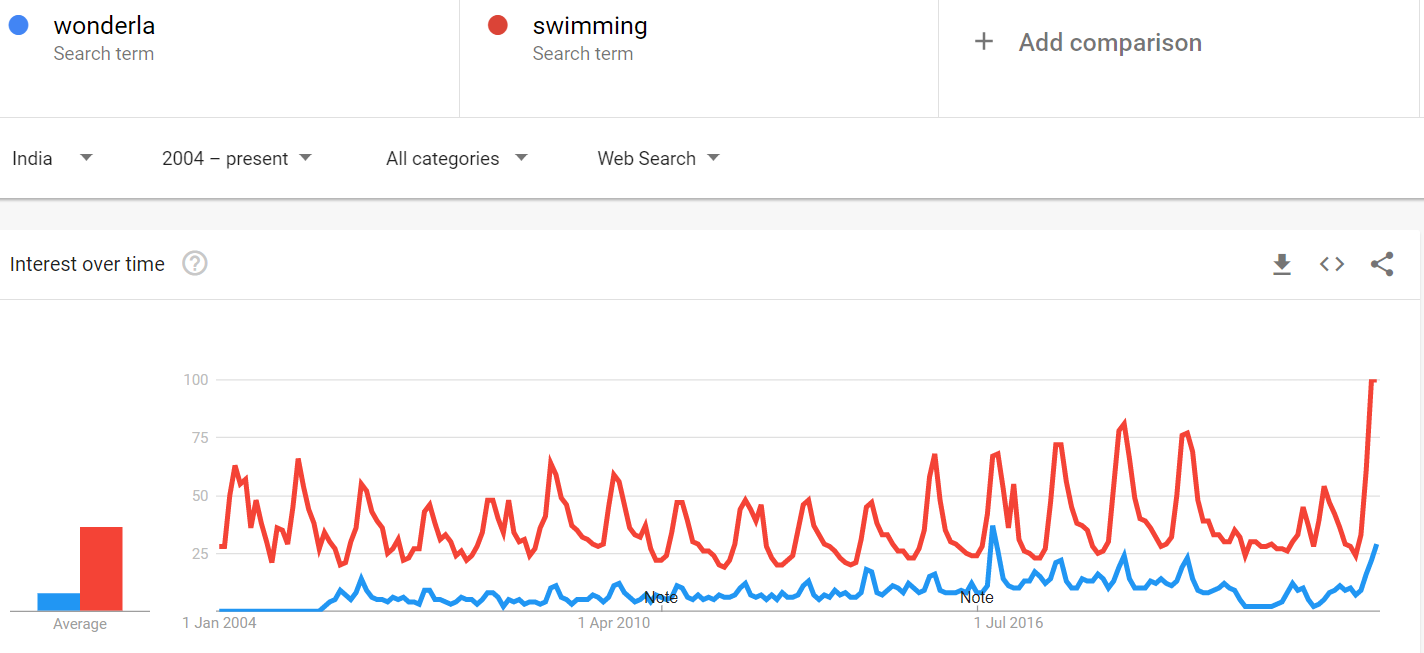

Interesting discovery, I ran one as well:

https://trends.google.com/trends/explore?date=all&geo=IN&q=wonderla,swimming

2 Likes

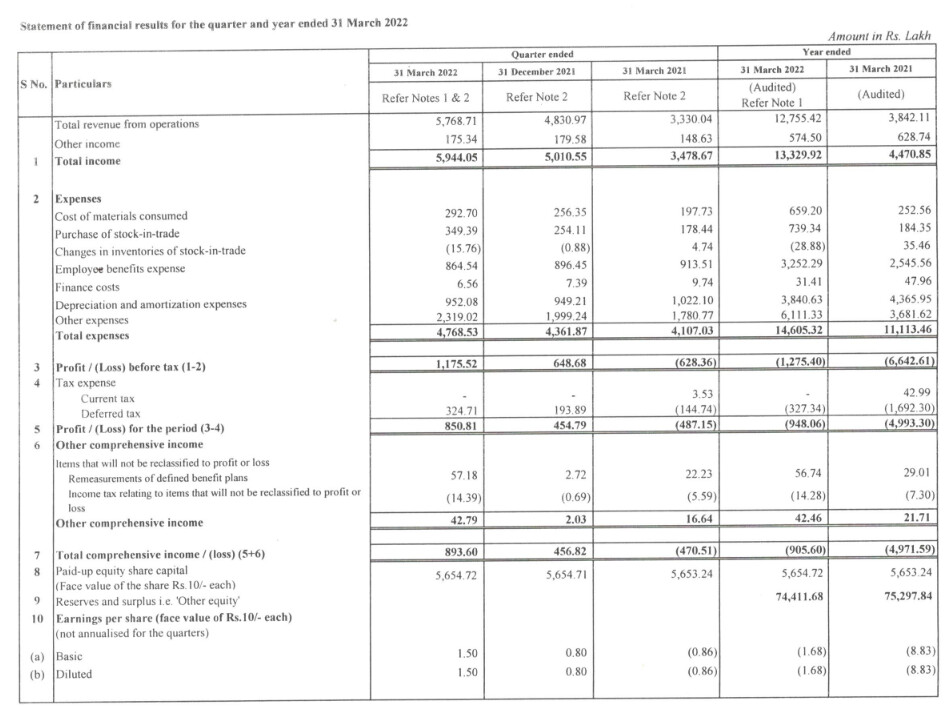

Just for comparison, they lost about two weeks in March, 2020 (onset of Covid from around March 10th onwards) and probably they lost a couple of weeks due to Omicron in Q4, 2022. So let’s compare Q4, 2020 with Q4, 2022…

EBITDA: Q4, 2020: 5.07 Cr. and Q4, 2022: 19.60 Cr. That’s the biggest takeaway for me from results. Future looks good from existing assets and if they get going on Chennai and Orissa, I would be happy. . Hoping for the best.

Disc: Invested. Position size, 3% of portfolio.

7 Likes

FY22Q4 concall notes

- Confident of starting work in Bhubaneswar in FY23, total capital outlay < 120 cr.

- Will take a decision on whether to build the Chennai park by the end of FY23

- Maintenance capex ~ 30 cr.

- Non-ticket revenue contribution is ~25% of revenues which company wants to take to 40% in medium term

Disclosure: Not invested

7 Likes

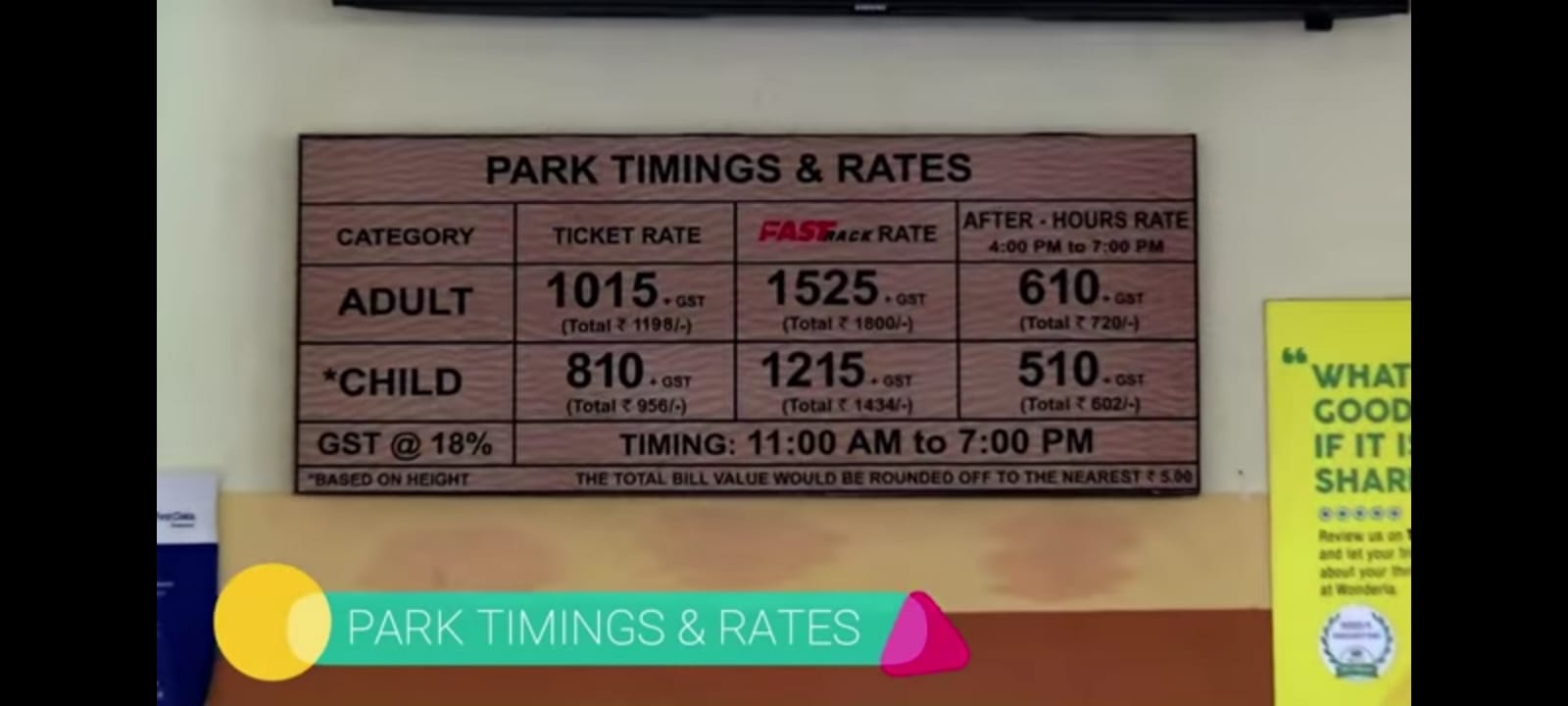

Happened to visit the hyderabad park in the weekend gone by

Here are my findings ![]()

Huge crowd, never before saw these many people during my previous visits.

Weekend footfalls around 9000-10000 as per the staff.

Weekday around 4000-5000

Ticket prices are 5% higher than pre-covid prices.

All rides are free inside.

Waiting time for each ride is around 30-40 minutes.

Food and beverages are priced very low compare to others (Customer delight) for example mineral water, tea, coffee, snacks all are priced just as you"ll be charged at local store.

Extended timings - Water park was running till 7pm which usually closes at 6 in summer.

I think its an idea whose time has come.

Disc - Invested

17 Likes

Concall:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/d48ddd12-2e01-4e57-ad70-36059a45fdcb.pdf

Some highlights:

-

Seems like footfalls are good and will get better due to the social marketing. Mgmt is very careful not to overpromise footfall. They may be wondering how far revenge tourism will take them.

-

Expecting next quarter should give good results.

So, we have completely stopped using traditional media and we use only digital marketing. We do use traditional media only as fillers unlike before, when we used to rely more on traditional media and less on digital. So, the reverse shift has happened after COVID and that has worked really well for us because our marketing spend has come down at the same time our footfalls are going up. So, I think it’s still an emerging phenomenon

-

Internal accruals for Capex

-

Invitations from Goa and Gujarat

-

Questions on the low footfall in Kochi

-

The gestation time for parks is long given the vagaries of taxation and approvals in india

-

Once question that remains in my mind is the impact of construction costs in the near future.

-

Can anyone shed light on the TN taxation issue? After spending 100C on TN land, will it lay fallow without the removal of the entertainment tax? There is a possibility of selling the land if things do not work out.

Disc: Invested.

7 Likes

Problem is they take lot of time to develop the park, if they able to do it quick then on high capex returns will improve drastically and bcoz most parks mature in 2-3 years they have to open new one every 2-3 years for decent growth.

4 Likes

Hello,

Just wanted to deep dive.

- On Ticket Prices

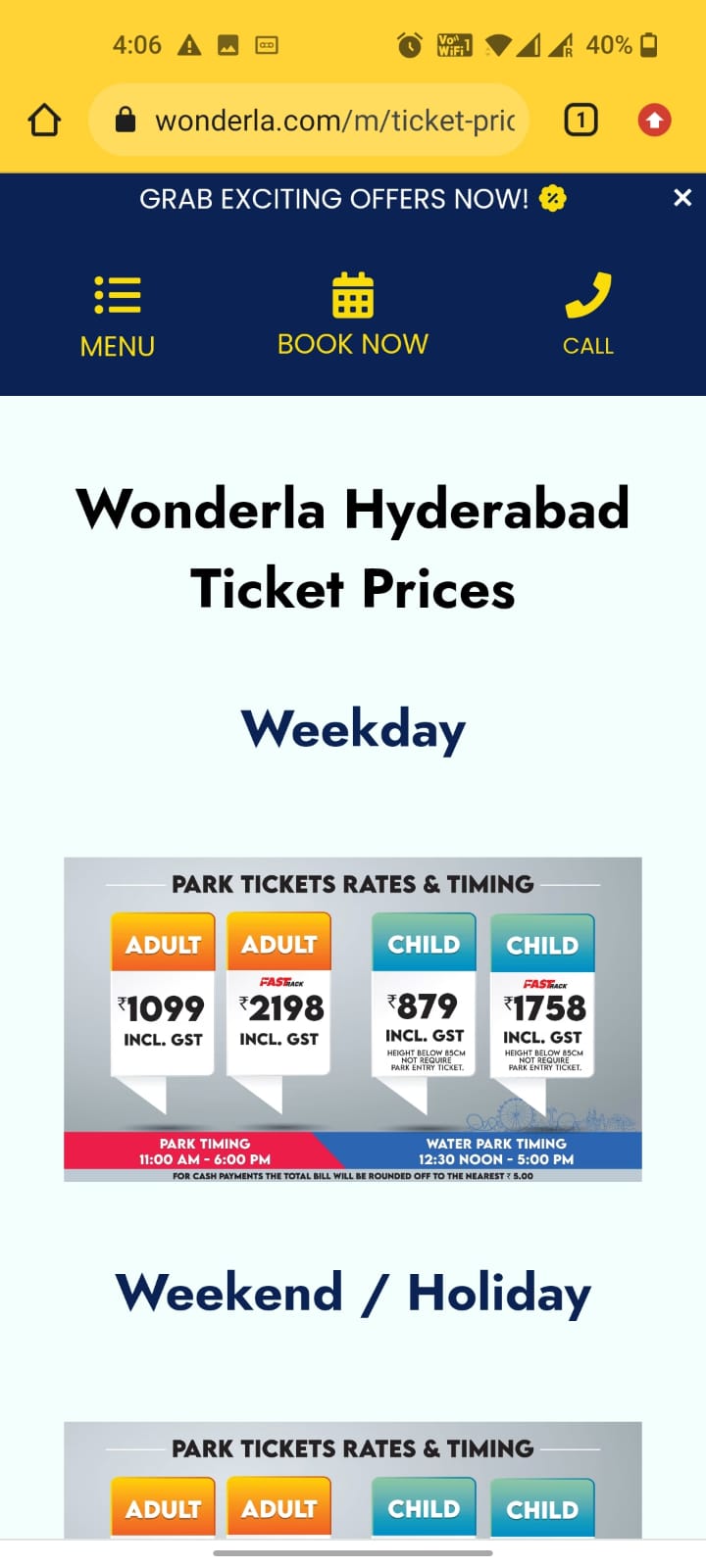

Hyderabad May 2019 Weekday Prices

Hyderabad 2022 Weekday

This actually shows the prices have decreased from 2019.

- On Footfalls

Lets assume 4500 for weekdays and 9500 for Weekends

In Q1FY23

26 days Weekend,

Weekend Footfalls:- 269500= 2.47 lacs

65 days Weekdays

Weekday Footfalls:- 654500= 2.92 lacs

Total Footfalls for the quarter = 5.39 lakhs

If these numbers are correct, Hyderabad park alone footfalls will be 5.39 lacs in Q1FY23 which is huge.

Dont think these numbers are anywhere close to the reality tbh

Peak pricing is different from non-peak pricing, comparison given is May 2019(peak) vs June 2022(non-peak), FYI May 2022 Adult ticket price was 1,249 per head.Also, if you observe Fast track tickets rates have increase by 25% even if we compare with peak and non peak period.

2 Likes

Okay…So In totality , is it safe to assume a ATP-ticketing hike of 5-7% on an overall company basis?

And wait a minute , so the footfalls you gave are also non peak numbers like 4000-5000 people weekdays and 9000-10000 people weekends?

2 Likes