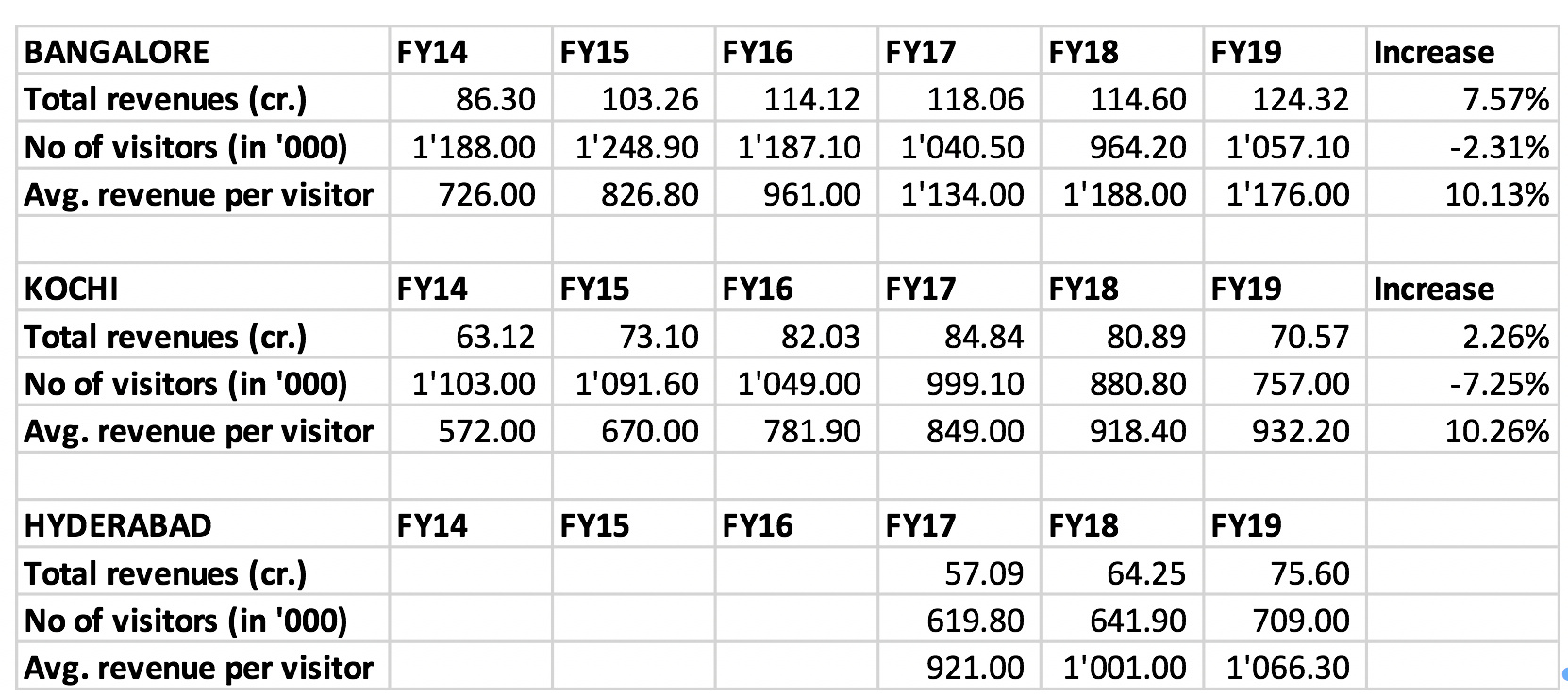

for me the major concern is the mature resorts are seeing footfall drops(blr 22%) … even new ones hyd(8%) as pre the latest q3 results… and there was no floods/endemic to blame…

Over all I see this is like economic slow down. Even you see FMCG stock they are facing same issue. I am talking about foot fall.

Secondly yes, in current qtr Q4 there will be case of Corona virus foot fall.

Over all this things will get improve over the time. Over all I can see one time capital intensive bussiness and assets light over the long term having in house skill set.

They are increasing monopoly in this segment also.

if its general economic slowdown why does PVR Q3 numbers not show any drop in footfalls. They increased their seats by 6% as compared to Q3FY2018 and income from sale of tickets also increased by 6%… I agree the fun quotient at Wonderla is definitely higher but maybe the longer distance with traffic is leading to this fall. They have recently started their own bus service, maybe it would yield returns. time only will tell… https://www.wonderla.com/pick-up-and-drop/pick-up-and-drop-from-wonderla-hyderabad.html…

what is even more strange is that even after starting the wonderpass (loyalty program) which offers 20% discounts (on resort plus park) there has been degrowth in footfalls… I dont think this loyalty program was there in Q3 last year… https://www.wonderla.com/wonderpass/wonderpass.html

Not sure whats the real issue here… Could it be that the ticket counter people are selling cash and those numbers are not reflecting in the P&L… stretched maybe but not able to digest this big drop in both Blr and Hyd Parks…

4 Likes

Crowd being more than what one would have expected to see on a weekday + cash payment = Footfalls falling by 22% in Bangalore Park?..

Investor perception of Corp Governance for the group has been high but if these cash transactions are regular, one can understand the fall in valuations… PE falling…

1 Like

Cash is generally not an issue as counters need to issue barcoded entry passes, so siphoning is very tough.

In places like Bangalore, lot of malls have small rides for Children and that generally takes care of weekend fun. Since it’s huge pain to travel so far to wonderla, personally I would prefer to go to holiday spots in similar range like Ooty, Coorg, Mysore etc.

I feel company looks like classic value trap and without growth we might see multiple derating to continue.

Disclaimer: Not invested. Not a RIA. This is not a recommendation to buy/sell.

6 Likes

interesting thoughts folks!

@vivek_mashrani in line of your holiday preferences - would mahindra holidays would be better placed compared to wonderla(rides+resort) - if we were to look at consumer experience aspects?

Mah holidays is also suffering from similar valuation treatment from market. So is broader hotel/hospitality sector with no returns in last 4-5 years. No material effect of recent taxation tinkering by govt yet.

is this somehow linked with Big money chasing “Growth” stocks at all valuations phenomena in India markets, rest all are children of lesser gods? any thoughts?

Six flag in USA also have good div yield and but lower valuations(around 10 PE type - but thats saturated US mkt unlike india) - again sales growth is low single digits.

What alternate choices one has for experiences like wonderla - esp Gen Z folks? If commute is the only issue - it can be taken care of to some extent by company(like buses etc) , also company is consistently trying to offer broader basket - new rides/food and bvg/resort - new segments such as group bookings are getting traction - mktg spends beyond Blr are being focused for new customer acquisition.

Once better sense prevail on markets (money distribution), and lower volatility in Qtrly performances (broadening base of parks across geo will help here), strong margin profile as well as brand recall and experience focus will help company re-rate upwards. Likely not to happen in near term but positive on mid term.

Irony is that opportunity cost is higher in this polarized market and patience while seeing other stocks flying past is not any easy choice.

Plan to observer atleast for few more quarters and look at annula performance rather than Qtr only. Downside is limited.

8 Likes

Sorry to say this… Unfortunately Wonderla would have the worst hit on account of Corona scare(water park with large crowd). I hope the management has already started screening the people coming into park and if not, with in no time government authorities would ask all the parks to be closed down until normalcy is restored.

AJ

4 Likes

Yes, If we check past cases like virus like Corona makes this business cyclic vulnerable in nature and this is the biggest weak point of Wonderla and I think no solution for this. But Disney also faces same problem.

As entertainment come into picture, it will work. Fundamental intact.

2 Likes

In view of the emerging situation in the State of Kerala, consequent to the reported Corona Virus cases, Wonderla Holidays Ltd has decided to temporarily close the Kochi Park from 11th March to 20th March, 2020

1st casualty

6 Likes

I also thought MHRIL should be better placed, but surprisingly Wonderla stock price is holding up much better even though its MCap is around 1/3rd of MHRIL… Is the Mgmnt increasing its stake?

1 Like

Bangalore Park closed till 20th March as pre-cautionary measure

1 Like

Hyderabad park also closed now from 15th to 21st March… While parks closure was somewhat expected, what remains to be seen is time for situation to normalize and footfalls once parks open.

2 Likes

Mr. Arun K Chittilappilly is appointed as Whole-time Director.

Mr. Kochouseph Chittilappilly has resigned as Executive ViceChairman and has taken the role of Non Executive Director.

market is factoring washout for near term, FY 20 EPS is likely to be at 2019 or lower level. Capex lined up.

Valuation and quality is superb - stock is available at book value and promoter buying it, Mr Arun is back to run the show.

slow catch-up to BAU should come back in H2 (current pandemic issue coming under control) but key triggers will be new capex and parks. Dont think stock is going anywhere for next few Qtrs and Growth visibility is not coming back anytime soon.

Was Invested but trimmed position to tracking - plan to reenter at later point.

2 Likes

That’s good news Mr .Arun is back. Most of investor was asking about him in each and every call. About two two qtr stock will be punished, but would be re rating on vision of Arun.

2 Likes

Bang on! This is a consumer discretionary business and prone to economic cyclicality. I have tried valuing this business using three different approaches:

- Long term PBT margin: 33%. Lets say the company is able to do sales ~280 cr. in FY22 (assuming FY21 is a wash-out). That will translate into a profit ~280*33%*75% ~ 70 cr. Current market valuation implies this business is available at P/E ~ 10 (implying almost no future growth).

- Replacement cost for 1 park is ~350 cr. (as per FY2018Q4 concall). They have three operational parks, replacement cost ~ 1050 cr., along with ~125 cr. in cash & equivalents. (Replacement value > 1175 cr.)

- Maintenance CAPEX for the three parks combined is ~20cr. They generate operational cash of ~100 cr. per year, so that makes FCF ~ 80cr. (which is then used for growth CAPEX). The company is available at ~10 times FCF (if management doesn’t reinvest their earnings).

Long term sustainable growth is ~12-15% (10% price increase + new parks). For higher growth (>20%), the company would need to dilute equity or raise debt. Investors were quite bullish in 2016-17. With this cyclical downturn, this reasonable growth company is available at no-growth valuations.

Cheers

Harsh

11 Likes

The value of the land at Wonderla is more than the current marketcap.

And what is the rate that you estimate for the land that it owns?

Thats a flawed assumption. Who will they sell to?. I doubt there will be too many takers. One more thing to keep in mind is that, the land is not in the city/outskirts of the city. It will be in some remote place. Usually there is plenty of supply of land there.

Note: My comment is a general one. Not related to wonderla

1 Like