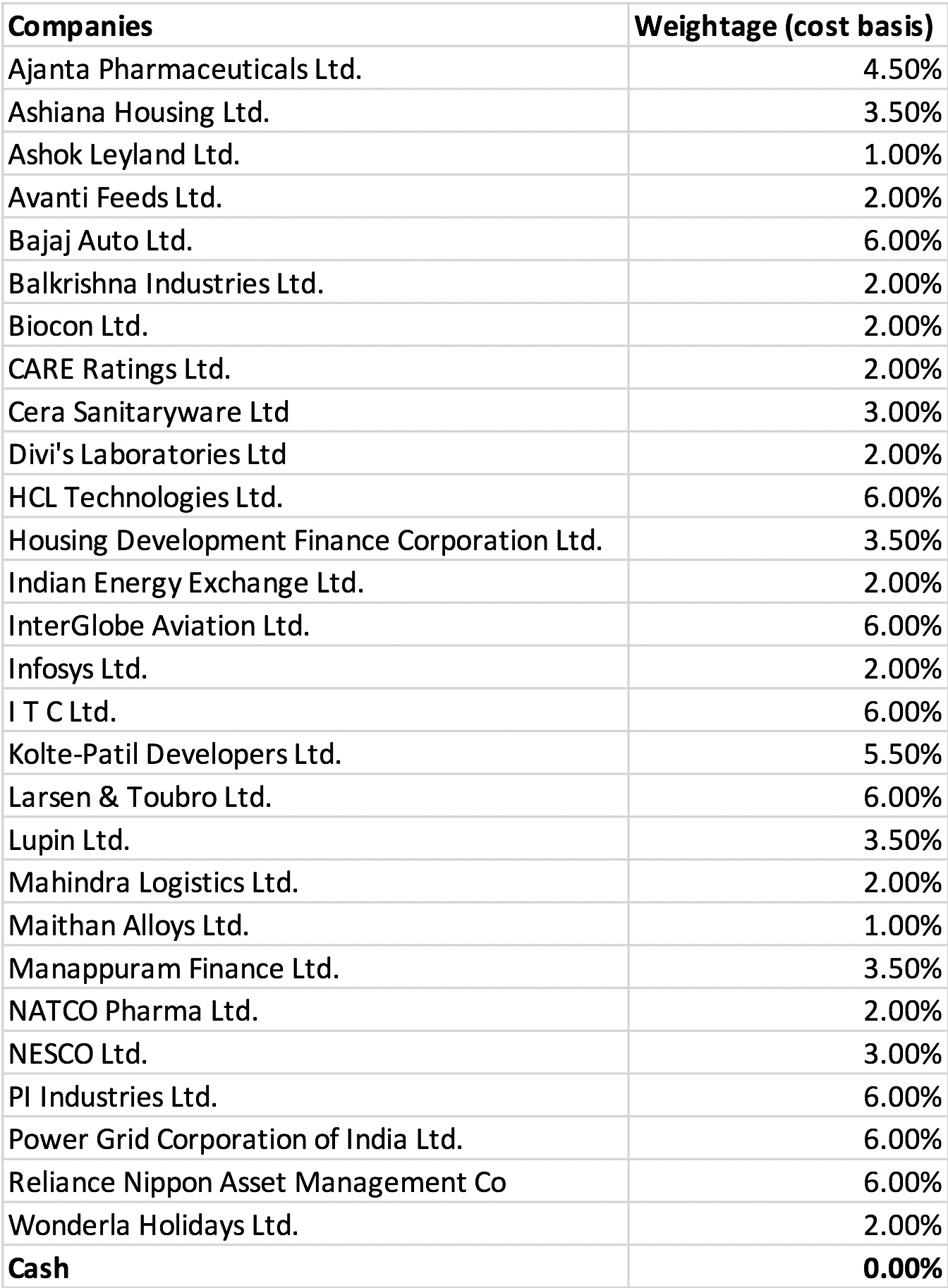

As of today, I have done a switch from AIA Engineering to Wonderla Holidays in the model portfolio, maintaining a position size of 2%. The reason for this switch is below:

- I was earlier valuing AIA on their accrual profits without realizing that AIA only converts 70-75% of their accrual profits to cash profits. This required me to revalue the business and I realized that AIA was trading at slightly higher than fair valuations

- Wonderla on the other hand is definitely undervalued in my assessment (detailed post here).

I understand that this switch may not work out in the near term as Wonderla parks are currently closed. However, over the next 5 years, with a 12% growth rate (with stabilization of Hyderabad park and start of Chennai park), I expect share price returns to be in excess of 25%. This attractive risk reward is why I have made this switch. The model portfolio is shown below