QIP at 1162.

1 Like

Chairman’s Letter on the Unaudited Financial Results of the Company for the quarter and half year ended 30th September, 2024 and an update on the business of the Company.

He discusses about the progress of clinical trials of some of the blockbuster molecules.

Very informative.

6 Likes

8 Likes

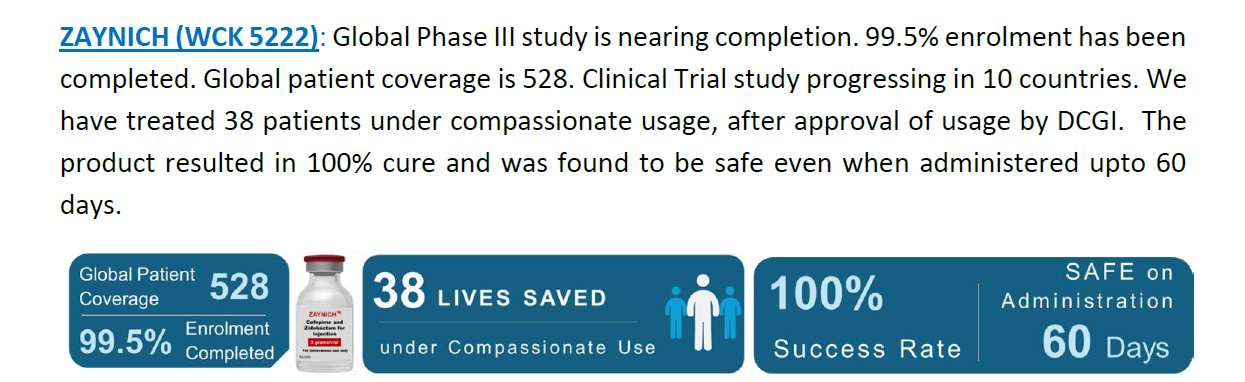

What do you mean by 90% completed? Can we see this anywhere?

As per the latest presentation… 90% recruitment for phase 3 is completed… it is expected that phase 3 is likely to be completed by March 2025…

8 Likes

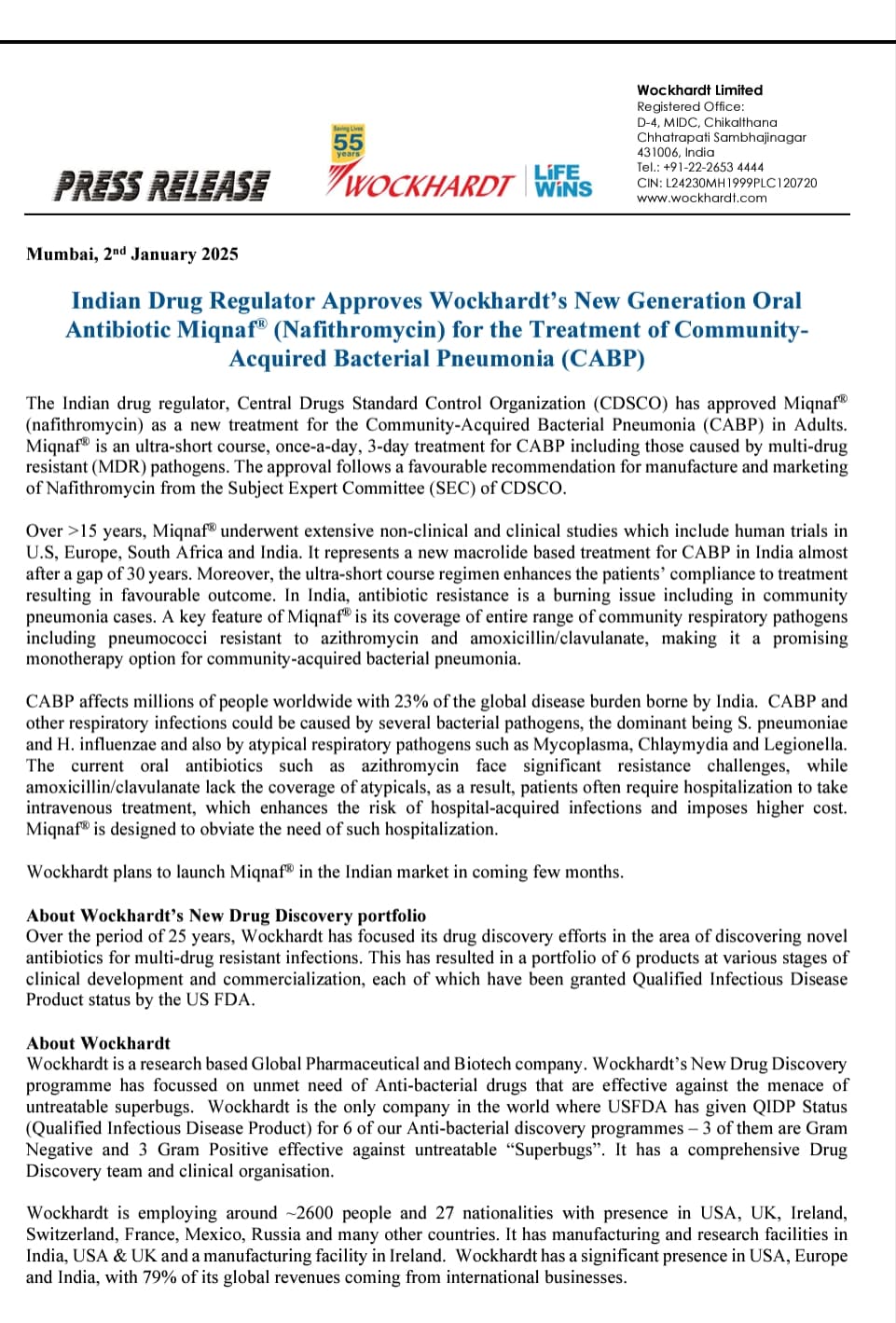

Indian Drug Regulator Approves Wockhardt’s New Generation Oral Antibiotic Miqnaf (Nafithromycin) for the Treatment of CommunityAcquired Bacterial Pneumonia (CABP)

6 Likes

This is just tip of iceberg. Micnef is first drug approved by indian regulator, globally Pneumonia is affecting 22 M population and exisiting drug Azithromycin is only 50-60% effective, indian market for this drug is 500 cr when we count globally this will go into billions. Saudi has approved the usage. More to come in coming years.

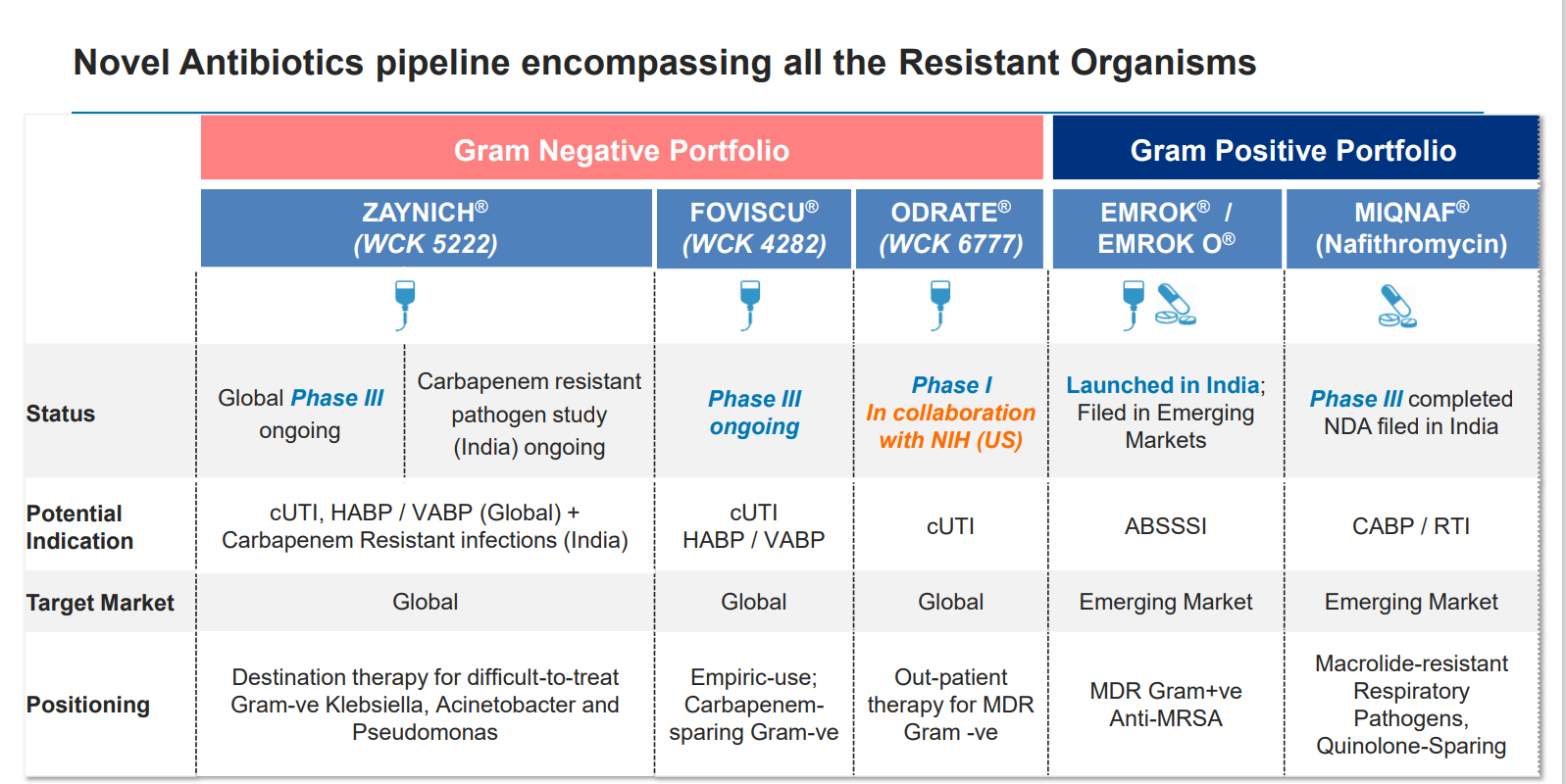

Zynich blockbuster drug phase3 is almost complete and commercial launch will be in 2026. Only US market for Zynich is 3 B USD, wordwide market is close to 25B USD.

3 other molecules are also in fast track status.

5 Likes

What I don’t understand is, why are not promoters buying?

1 Like

What will they buy with ? This company has been making loss and bleeding cash for years just to fund their R&D .Almost all their holdings were pledged just to run the company …only recently they have started reducing pledge (That too only because the stock price has increased ).Unless they have other cash generating businesses where will they get the money ?

12 Likes

Wockhardt | Pharmaceuticals firm announced that the Central Drugs Standard Control Organization (CDSCO) has approved Miqnaf (nafithromycin) as a new treatment for Community-Acquired Bacterial Pneumonia (CABP) in adults. Miqnaf is an ultra-short course, once-a-day, three-day treatment for CABP, including infections caused by multi-drug resistant (MDR) pathogens. The approval follows a positive recommendation from the Subject Expert Committee (SEC) of CDSCO to manufacture and market nafithromycin.

5 Likes

At around 20:47, Aditya speaks about his concern about Wockhardt.

I have extracted a summary using Notebook LLM:

Aditya Khemka, a fund manager, expresses uncertainty about Wockhardt’s recent Qualified Institutional Placement (QIP) where they diluted equity by 8% to 10% [1]. Khemka finds it perplexing that the company would dilute equity when they believe their profits could multiply by 5 to 10 times in the next few years if their WCK 52 drug gets commercialized [1]. He questions why the promoters would sell equity before such a potential profit surge, suggesting they should instead buy back equity to maximize their gains [1]. While acknowledging the management’s intelligence and experience, Khemka admits he struggles to understand their rationale and therefore avoids investing in the company [1].

What are your thoughts on this?

3 Likes

None as such . His opinion ,only he can explain . The management has never been financially prudent …they did make losses by dabbling in F&O in past as well .But , regarding investing more money by buying …this I have already given my opinion…where will they get the money ? . No financially prudent promoter would even try doing what Wockhardt has been doing for past 20 years…namely making losses in R&D for new drugs…no other Indian company has done what they have done . They did it because the owner is primarily a man with a vision and ready to take risks that no other Pharma businesses has taken in India . But fact remains, the company has not given a PAT positive result in donkeys years . They might turn positive after miqnaf gets traction or if Zaynich gets phase 3 clearance etc… but all said and done, the stocks price rise does not benefit the promoter unless the company distributes dividends…which they can’t do unless they are PAT positive . They can’t sell stocks to raise money either just to convince people like Khemka and Sajal Kapoor .

That video is months old,…stock was at 900 odd then. Just like Wockhardts promoter had to have vision and conviction to make it …as an investor one needs to have both of these . Fund managers can’t justify failed visions ,so as an investor , their opinions are utterly useless for stock picker’s (Because, stocks need to be picked before funds are there with their conviction) seeking to generate alpha.

Disc: 2% of portfolio when invested at avg 464.Bought between 385 to 577 .

17 Likes

They are running paid services to their customers… Now they have to give a justification why they missed a 10x rally in Wockhardt…

4 Likes

Thanks for your sharing your thoughts @Ghonarbochon . I too have huge respect for the work they are doing, and wish them grand success.

Just a minor correction: the video is 2 weeks old.

Forgot to mention my disclosure: 4% of my PF, avg price: 936.

2 Likes

Wockhardt is only pharma company which has risked 20 years for drug development, name any other indian company which has spent so much on R&D. How many drugs india has launched till now? Ask yourself. API, formulation, CDMO, bulk drug thats it. HK deserve Padam Shree for the work he has done for country. Fund Managers are baised with their own limitations. Market always reward calculated risk takers. Prashant Jain and Mashu Kela invested in QIP at 600 levels that was a testimony that things are changing. MD pledged stocks to raise funding for research, sold hopital to raise funds for research. Its a bamboo tree and outcome will be visible in coming years based on opportunity size they have. I was an early invester in wockhardt in 2016 and did a deep research, booked losses and exited due to inherent nature of durg development. Reentered around 600 levels and kept adding. Look at moat not dividend, recent QIP was done to depledge promotor stake and WC for drug launch. Views may be baised as its a conviction hold with 9%.

21 Likes

Can somebody explain Mr Khemkas rational ? I mean how can one have a buyback if the company doesn’t have much cash ?

Also maybe the promoters do NOT have much funds to buy more shares ?

I think the future is very exciting for Wockhardt ….but antibiotics can lose their efficacy so it is not without risk

I am a buyer from the 250 region a year ago so I have done well—I thought of it as a huge gamble then but I thought it was a good one…The other company I bought then was Spicejet which I bought in the high 20s…I think it is another very interesting gamble…

3 Likes

Mr Khemka seems to regret his decision not investing in this stock.

Investment in this Company is presently a gamble and I support such gambling as it gives risk capital to good Corporate for innovation which is lacking in Indian Companies.

Mentally prepared for 80% erosion in Stock price.

Disclosure : Invested.

4 Likes

@Ghonarbochon has given much of the justifications.

Just wanted to point an additional factor. They still have two more drugs at various phases of trials and development. Please look at development plan. QIP has dual purpose of deleveraging the company and fund these trials and R&D.

As regards to khemka and Sajal, i would not comment much.

Also will not like to opine on stock much because I am heavily biased.

Disclosure: 35% of pf at buy price of 400-420.

16 Likes

Perfectly said. Regardless of what happens with the company.

You need role models who invest in R&D to inspire next gen.

2 Likes