Windlas Biotech came out with its IPO in August 2021 at INR 460 per share/Market Cap ~1000 Cr. The IPO saw a good subscription response at that time at 22x

Since then, due to headwinds for Pharma, primarily normalisation of a COVID base in sales for Windlas, has led to a strong correction in stock price.

At CMP of 235, it quotes at 51% of the IPO price/market cap of 512 Cr currently. This means that the company is currently available for ~1.1x sales and sub 15 PE

Despite being a micro cap, the management has regularly held conference calls/share investor presentations since the IPO and offer good clarity on the business

Company Overview

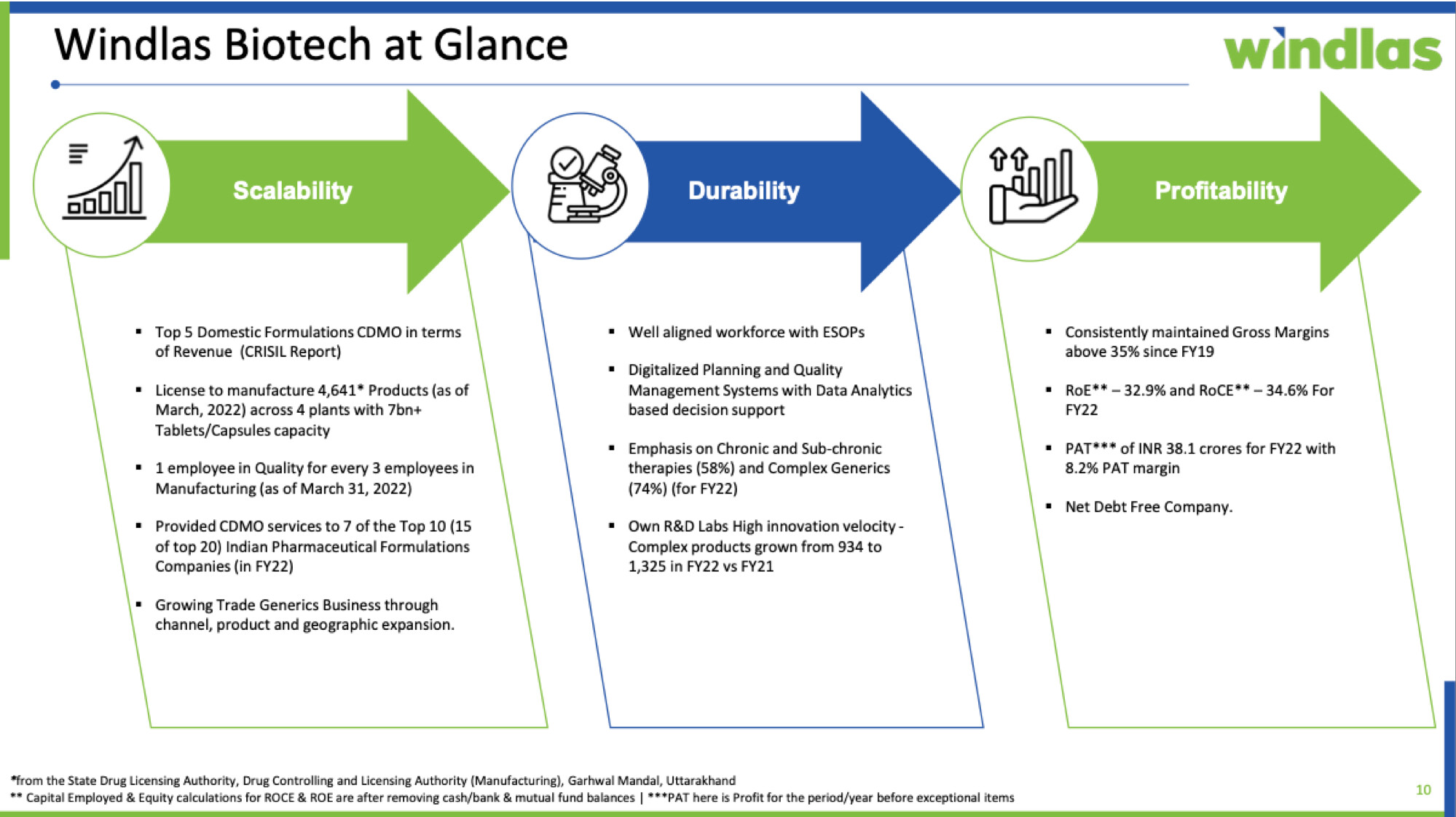

Here is a slide from the investor presentation which gives a decent company overview

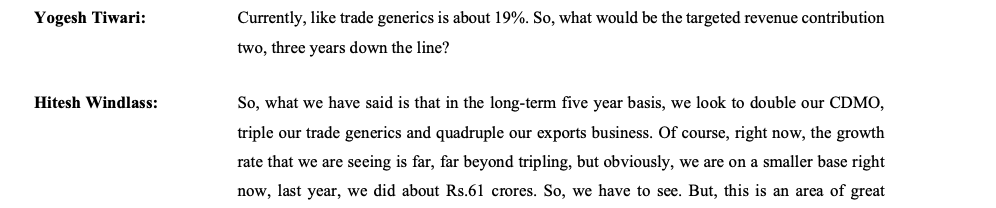

Revenue Mix :As of Q1 FY23, Windlas has ~79% of revenues coming from its CDMO vertical. ~18% revenues come in from trade generics and they have just started exports (non USA markets only) which contribute ~2% of sales

They claim to be amongst the top 5 players in the domestic CDMO space, supplying to customers like Pfizer, Sanofi, Cadila, Emcure, Eris and Intas amongst others (from DRHP - Page 134). In the latest Q1 FY’23 investor presentation, they also claim to be in all aspects of the value chain including CRO and CDMO depending on the customer, except in API manufacturing (Slide 11)

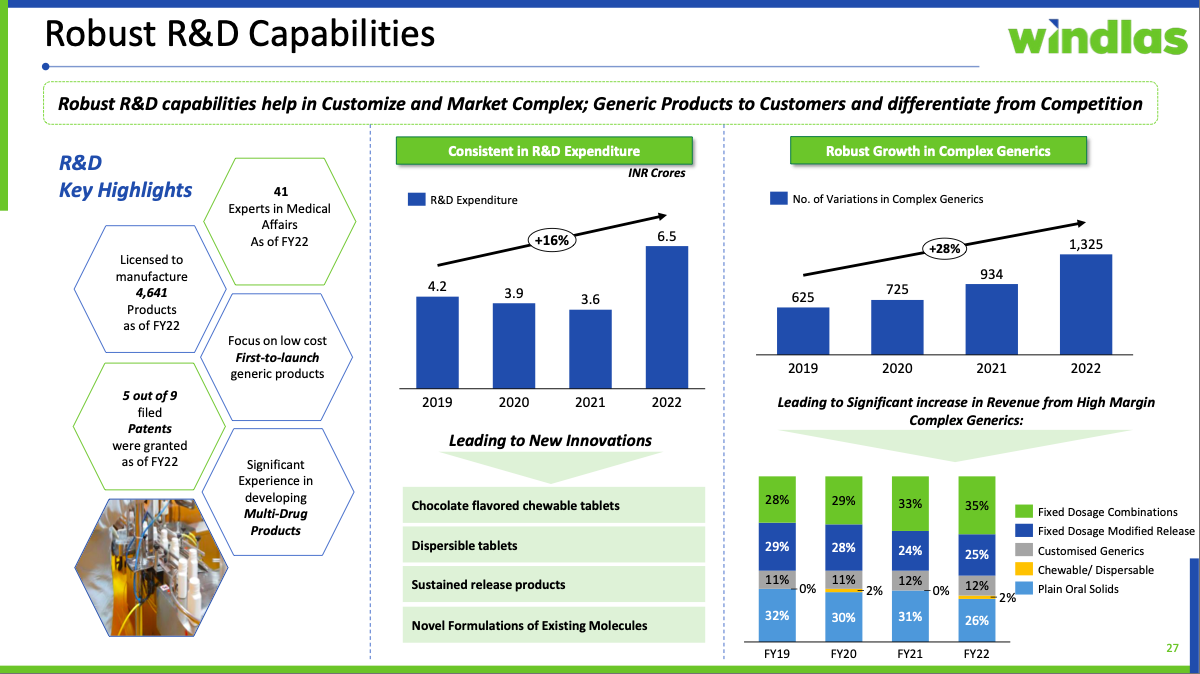

They claim to have a high product concentration in complex generics and from the chronic segment. The below slide mentions historical growth of CDMO business along with good growth in product offerings in the CDMO space coming from good R&D capability

Margin Mix : The company in different concalls claims to work on a cost plus model and hence not be largely positively/negatively affected by input prices/industry pricing interventions. Margin profile (GM ~36%, OPM ~11%) suggests a more manufacturing oriented CDMO model rather than a higher margin one based on IP/research. Interestingly, forays into the faster growing verticals of trade generics and international business are margin accreditive over the CDMO business, as can be seen from concall snippet below. These could be potential sources of margin expansion over the long term from current base apart from an upcoming foray into injectables.

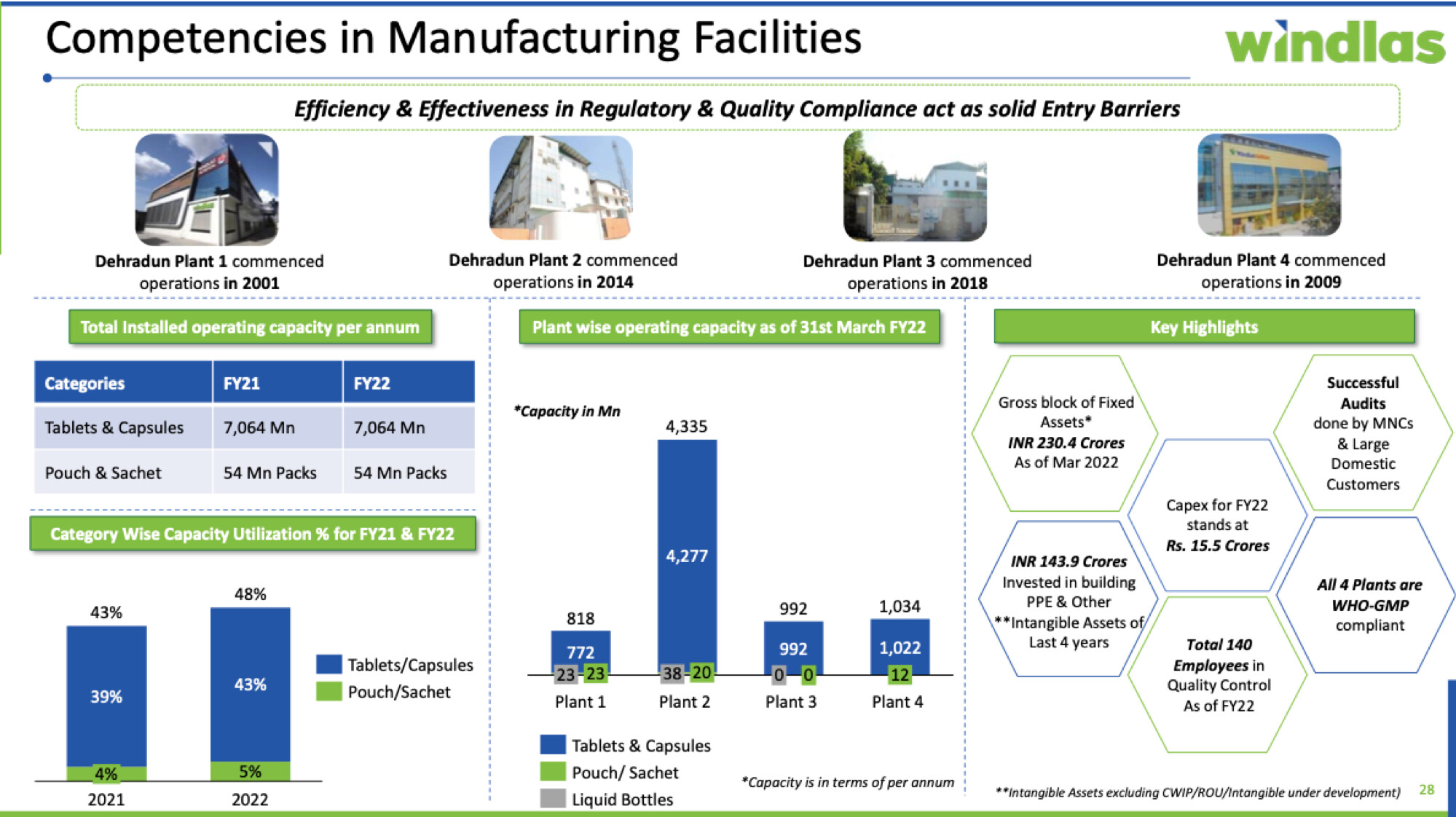

Manufacturing Footprint and Potential for Operating Leverage

Below slides from investor presentation give a good insight into manufacturing footprint (through 4 plants, all in Dehradun) and R&D focus

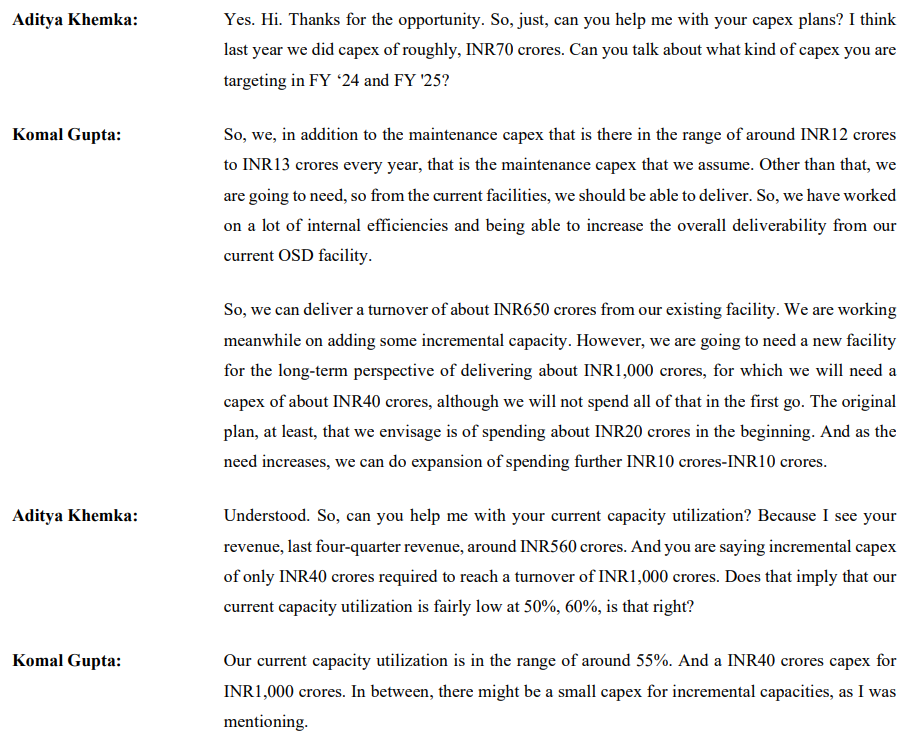

What stood out to be that they are currently only at 40% capacity utilisation, which would mean that unit economics currently would not be too favourable. If they can deliver on their growth expectations in the next 4-5 years (Q1 FY 23 concall snippet below), this could provide substantial scope for operating leverage to play out and improve return ratios

A look into shareholding pattern and management credentials

Promoters have good skin in the game (~60% promoter holding)

Key person seems to be Hitesh Windlass (MD) who has been leading the company since 2020 (earlier led by his father). Hitesh’s background from annual report is as below

There were also some good interviews with him around the IPO and he is the key person on the concalls. Link for a BQ interview below

Overall, they seem to be building a foundation for a solid senior leadership team. A cursory search on LinkedIn showed me 350+ profiles, including strong key leadership profiles including a CBO who is ex director sales at GVK Bio and a CFO who is ex DSM Sinochem

I would also like to mention anti thesis pointers I could think of:-

Management execution bandwidth still has to be proven and it remains to be seen if they do actually deliver on growth they project which will be required to deliver operating leverage and strong OCFs

Lower GM and OPM profile suggest they operate in a highly competitive space

I do not view this to be as evolved as say a Syngene with considerable IP, so possibly IPO valuations were quite demanding initially itself

The inherent nature of it being a microcap makes it a high risk investment in the current exuberant environment

My expertise in Pharma as a space is relatively limited versus other industries and hence there could be aspects I am missing

Though for my own investment purpose, the positives outweighed the negatives significantly. Key Thesis positives for me were:-

Scope for longevity of growth in CDMO space

Potential for growth triggers in trade generics and exports

Potential long margin expansion from operating leverage

Potential margin tailwinds from higher growth trade generics and exports

Management credentials with skin in the game

Reserves of 384 Cr in balance sheet currently and debt free status

Current pessimism around the space and end of IPO lock in meant current valuations at ~1.1 PS, sub 15 PE did not feel demanding at all

Would be happy to have inputs of fellow members on the business.

Disclosure : I have recently invested in the company and am biased. I have made buy transactions in the last 30 days. I am not a SEBI registered advisor and investors should do their own research

Thanks for starting this thread on Windlas.

I had come across this company few months back and was about to invest but then came across this twittr thread and it stopped me from investing in it especially when there are better opportunities available elsewhere.

I have gone through the thread, and it is a good piece of work which has come about during the IPO in August 2021. In fact I would even say that 1 year later now, the author has been proven right as valuations were very high (as usually are in several IPOs).

But then again, the situation currently is very different:-

The largest part of the thread addresses that the IPO pricing seemed aggressive and there was obviously an OFS component for the PE fund and the promoters. I would agree with the author at that time, at 50x PE it was very expensive and yes the PE fund did get an exit (even if the author thinks the IRR was not the best). I did not apply for the IPO myself inspite of liking the business then.

But currently the price is much lower then when the thread was written (INR 235 vs INR 460). My entry price is below current CMP. I felt at a sub 15 PE and 1.1 PS the risk reward was favourable taking into account these aspects.

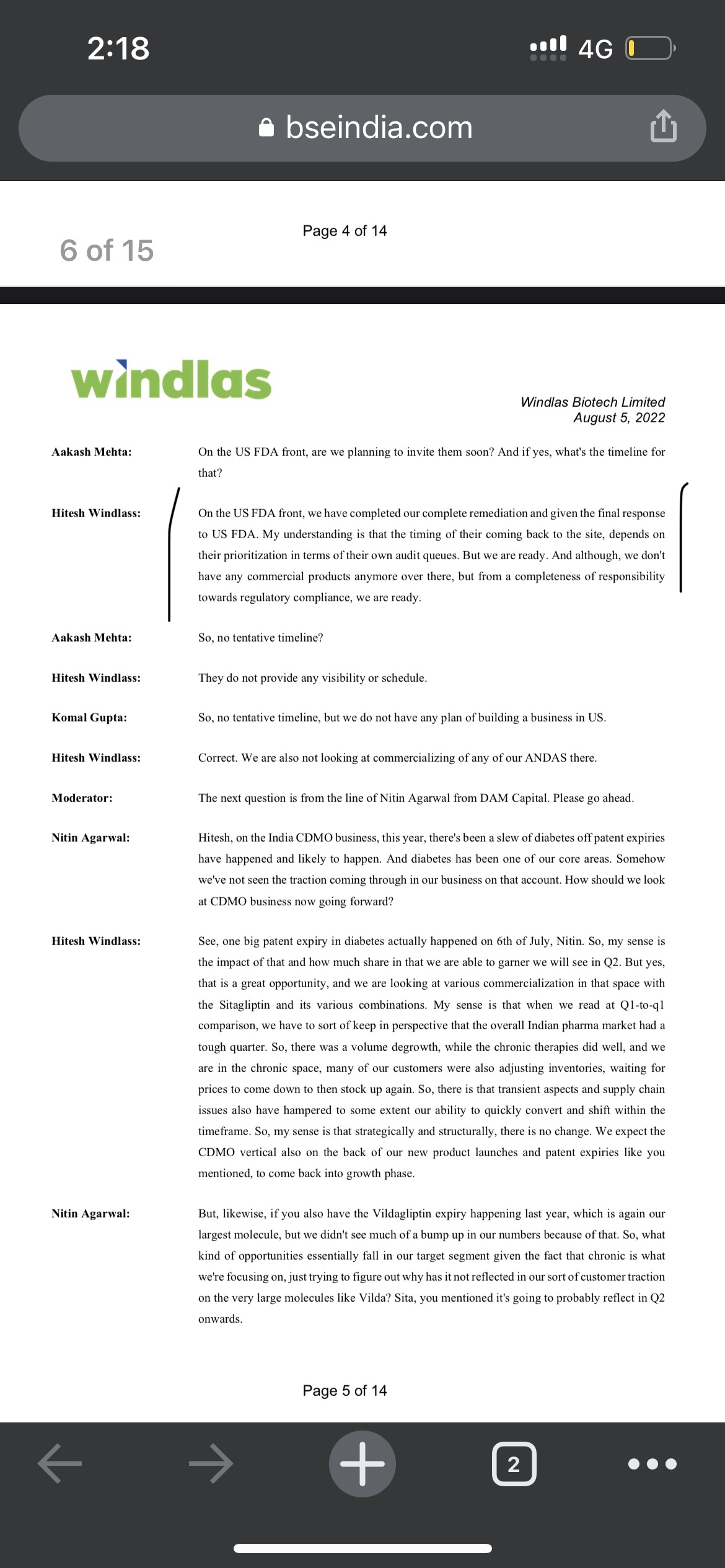

The USFDA inspection was a big issue. But since then in concalls, the management has mentioned that after this issue, they have not really pursued the US markets as an active strategy for expansion but are instead focusing on growth through the core business of CDMO and trade generics in India, and some other export markets like South Africa. Inspite of questions on US growth, the management does not seem too keen to pursue the market. I do not mind the management not pursuing the US markets currently, I think the opportunities they are focusing on are large enough for a company their size

The author has mentioned some aspects with proprietorship firms and related party transactions. I am not sure if we can find a definite red flag in doing business with proprietorship firms. But the point on related party transactions is one point which would still be worth digging into.

That said, this is eventually a microcap with a limited history in the markets and as with most of them, there are risks and we will need to gauge with time if management delivers. There are also other potential anti thesis aspects, ones which I could think of I have already mentioned above.

1 Cons I see is that,

Most of all the board members are from windlas family only. Don’t know, whatever the organizational decision was made are biased or not.

Exports is the highest margin business ~margin wise Exports (+4-5%) > Trade Gens (5-7%) > CDMO. For CDMO they mostly work on formulations for MNCs which is eventually sold under MNC brand name. Are CDMO businesses meant to be a 10% OPM game? Possibly lower because they don’t add much value and serve as a low cost mfg resource for the big guys (unlike say Syngene, Laurus, etc).

Keeping current PE in mind, a possibility of a future re-rating cannot be ruled out (if nothing goes too wrong). If they are successful in doubling the revenues in 5 years and PE rationalizes to ~20, ROI could be around 3-3.5x - the risk-reward scenario needs a closer look to weed out any reg flags.

i have recently taken position in this stock. Looks undervalued to me. They seem to be doing right things, but i guess street is not recognizing cause it was expensive when listed. Reminds me of BSE ltd, which corrected substantially after listing but went on to become multibagger from lower levels.

Injectible facility to be commerialized by end of FY24 and scaleup in FY25.

Current quarterly revs at 160 crs. Potential upto 650-750 Crs/yr at existing capacity.

Growth is good in trade generics and CDMO business.

CDMO business is picking pace. No lumpy revenue here.

Want to grow quarter on quarter (QoQ). Shows consistency in growth.

Growing faster than Pharma industry.

Based in Dehradun. Focus on North Indian markets.

Exports are currently slow.

Positive on all 3 verticals- CDMO, Trade generics & exports.

Focus on sustainable and efficient operations.

Higher employee expenses, lowering of margins due to ESOP scheme.

Schedule M impact is to seen across CDMO players, as non-compliant facilities will be under crackdown.

Edit: Thanks @narenarora for correcting the post. Made the changes. Also going through the Q2 FY24 concall, management spoke about how they will develop capacities for 1000 cr revenue with small incremental capex of about 40 cr. Is the capex being referred to is the injectables facility?

Its not 600-750 cr per quarter it is 700-750 per year as against current TTM revenue of 600 cr.

Your statement indicates a 4-5 fold increase in revenue which is not the case.

Please see the concall extract below.

Komal Gupta: Yes, so, Nitin, as I mentioned, the current capacities we had increased and we have been

consistently working on. So we are comfortable delivering INR700 crores to INR750 crores with

some incremental expansion internally that we have been working on. We have been adding it

as needed. So we are able to do that. So we should be able to deliver INR700 crores to INR750

with that. And there is other work going on for further runway…

From Akums Drugs DRHP. Akums is the largest domestic formulations CDMO player in India. With Akums, there will be 3 formulations CDMO cos listed now - Windlas, Innova Captab and Akums.

The Q1 results were a testimony to the abilities of the management. While the employee cost had been a one off high expense which should get streamlined accompanied by the depreciation of the new facility, the prospects for the year seem to be rosy.

CDMO business consistently hitting above 100 Cr mark

The injectibles facility on track to add to the business margins

The trade generic business poised to be a strong business

Management that seems to be good capital allocator

2-3 years down the line the prospect of exports once they gain momentum with filings

One of the most important things is that the facilities are compliant with the strictest of Norms and in case some policy comes out, Windlas might become an indirect beneficiary.

Is one of the biggest holdings and have done transaction in last 30 days