I came across this podcast on Windlas Biotech

I hope you find it useful.

dr.vikas

I came across this podcast on Windlas Biotech

I hope you find it useful.

dr.vikas

14-15% stake will be holding by Mr. Utpal seth, erstwhile mgr at RARE enterprises …not by RARE ENTERPRISES of Rakesh jhunjhunwala

Please do mention the source of this information.

dr.vikas

Good read with red flag : Windlas Biotech | IPO Analysis | SPTulsian.com

For existing investors, what is the potential return expectation from the stock? The management has guided for ₹1,000 crore in revenue once the capex is fully operational, along with a 2-3% improvement in margins. In a best-case scenario, the company could achieve a PAT of ₹110 crore with 15% ebidta margins. Based on this, what price-to-earnings (P/E) multiple would be reasonable to attribute to the stock?

You can take the Industry median of around 35x but PAT margin can’t get 15% that would be 10% max, 15% is EBITDA margin guidance

can u share the pdf version of this as same is paid blog

Injectibles-The company is preparing for audits by several large customers, which are scheduled for Q4 of FY25, with potential additional audits in Q1 of FY25. These audits will follow the company’s GMP certification process. Meanwhile, the company has an existing order book, with ongoing production and commercialization of products from stability batches. While it is difficult to predict when peak performance will be reached, there is positive momentum, strong responses from audits, and increased customer interest in the product portfolio. ATO 1.1 to 1.2.

Schedule M with heightened stringency. -Surprise audits are being conducted across the industry, and the company has successfully cleared them. Several smaller companies in contract manufacturing hubs like Baddi and Uttarakhand have faced shutdowns due to non-compliance.

intellectual property (IP) advantage - Unlike firms that merely provide manufacturing capacity and job work, companies with strong IP ownership can sell their formulations to multiple customers with variations in packaging and tablet design. This approach enables higher EBITDA margins compared to businesses that rely solely on contract manufacturing.

Capex and ROCE-The capex for Plant-3 is expected to be fully utilized within FY25. Additionally, Plant-6 is being developed to help the company scale up to ₹1,000 crore in oral solid revenues. Anticipates continued capital investments to support expansion, which will impact the denominator in financial ratios. However, it expects to maintain a Return on Capital Employed (ROCE) of 27%–28% in the long run despite periodic fluctuations.

Expected increase in adoption of trade generics with regulatory tailwinds through initiatives such as Schedule M etc could usher extended period of purple patch for Windlas (& some of their peers).

To me, this could be the strongest of all the tailwind for Windlas.

IP advantage, will be able to cater to multiple pharma companies

So basically all these three companies will be getting benefiting from PM Jan Aushadhi yogna , am I correct as these generic market is expanding very fast I am seeing long queue in these shops, please correct me if I am thinking in wrong direction.

Windlas Biotech is a pharmaceutical company which is present in all segments of generics value chain (Generic formulations, Generic CDMO, Clinical trials, packaging, marketing)

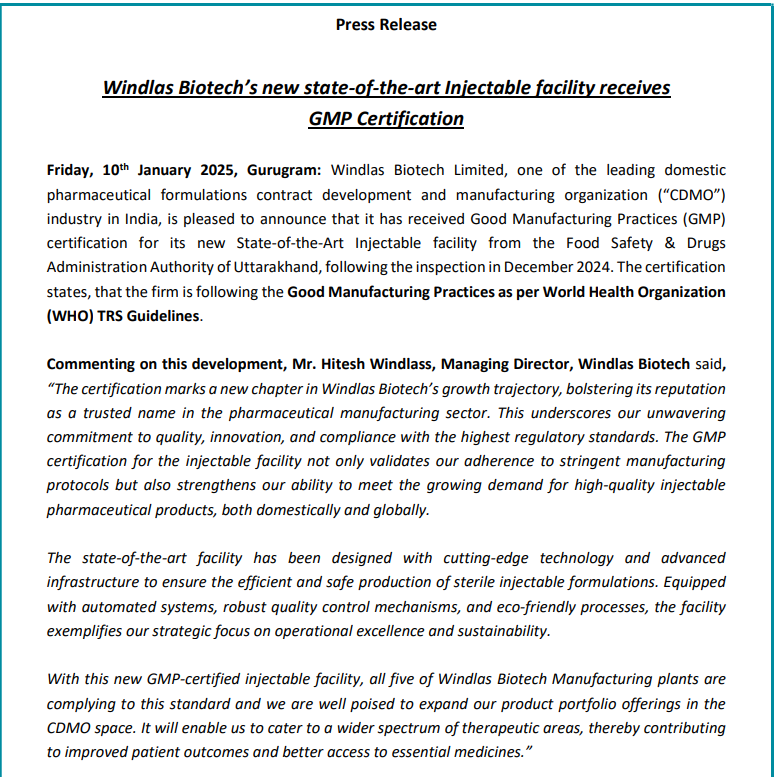

Is anyone closely following the business? It seems there haven’t been many updates on this forum. Windlas Biotech’s injectable facility has already received Good Manufacturing Practice (GMP) certification from Uttarakhand’s Food Safety & Drugs Administration Authority, confirming compliance with WHO TRS Guidelines. While it has not yet contributed to revenue, it is expected to significantly boost it’s earnings (add ₹100 or so crore in revenue) and improve margins to 18%-20%. So looks like it is poised to be a key growth driver in the near future.

Does anyone know when it will become operational and start contributing to revenue?

Hi Sumit,

As mentioned by the management in the previous concall, “large customers have scheduled audits of our injectable facility in Q4 of FY25,” which suggests that the facility is likely to begin contributing meaningfully to revenue from H1FY26 onwards. However, the company has already recorded some minimal revenue from the facility during H2FY25.

While this is expected to support margin expansion, it may not be to the extent you’ve indicated. Based on my understanding, the injectable segment can generate EBITDA margins of around 18–20% at steady state. However, given that a substantial portion of the business still comes from CDMO and generics, which typically yield ~13% margins, the overall EBITDA margin profile could see an improvement of about 150–200 bps over the next three years reaching towards 14.5-15% mark.

Thanks.

Conservative mgt, as usual no guidance for fy26..adding plant VI, peak cap rev would be 1000cr excl Inj (90cr).. Declared dividend. They are waiting for Inj plants to stabilise to plan future capex .. open for M&A too.. PAT/OPM not grew as much due to higher employee cost and higher dep..Remg all similar to FY 24 with TG and Exp grew much higher than GFC. Indian IPM grew 8% (vol flat) but windlabs grew 20%. Tech chart (started learning) not encouraging.

The management guidance can be summarised as follows as per concall Q4 FY 2025;

Windlas Bio -

Q4 and FY 25 results and concall highlights -

Q4 outcomes -

Revenues - 203 vs 171 cr, up 18 pc

EBITDA - 25.5 vs 22 cr, up 16 pc ( margins @ 12.6 vs 12.8 pc, due sharp increase in employee expenses - up 50 pc YoY )

PAT - 16 vs 17 cr, due sharp increase in depreciation expenses

FY 25 outcomes -

Revenues - 760 vs 631 cr, up 22 pc

EBITDA - 94 vs 78 cr, up 20 pc ( employee expenses @ 123 vs 87 cr YoY )

PAT - 61 vs 58 cr ( depreciation @ 28 vs 14 cr YoY - attributable to two new facilities )

Segmental breakup of sales for FY 25 -

CMO - 555 vs 481 cr, up 15 pc

Trade generics + Institutional sales - 172 vs 122 cr, up 41 pc

Exports - 32 vs 27 cr, up 19 pc

IPM grew by 8.4 pc in FY 25, largely driven by price hikes. Volume growth was @ 0.4 pc

In Jan 25, company’s new Injectable facility received regulatory clearances from Indian regulators and WHO. Also increased the Oral Solids capacity via brownfield expansion @ Plant - 2

Cash on Books @ 223 cr ( Liquid MFs + FDs ). Company is debt free

Revenue contribution from top 10 customers ( wrt CMO business ) @ 35 pc vs 57 pc in FY 20

In the trade generics segment, brand ownership remains with Windlas. Three focus therapies for the company in this space are - GI, respiratory and Anti-Diabetics. This segment has been growing @ 42 pc CAGR for last 5 yrs and now contributes to 23 pc of Company’s topline. Company’s products are sold directly via distributors and not promoted via MRs. Govt Schemes like Jan Aushadhi are a big tailwind for the company

All of company’s 6 manufacturing facilities are located @ Dehradun ( with plant 5 going live and plant 6 being acquired in FY 25 ). Company’s overall capacity utilisation stood @ 63 pc for FY 25

The injectables facility operationalised in Q4 is capable of making dosage forms like - Ampoules, Liquid Vials, Lyophilised Vials - thereby facilitating company’s entry into critical care, other specialised therapies

The Injectables facility contributed to 6 cr of revenues in Q4. Looking to ramp up this facility in FY 26. Making all efforts towards the same. Refrained from giving guidance on the potential sales from this facility in FY 26

Given all the fixed costs wrt the Injectables facility are already in the P&L, ramp up in Injectables + normal growth in CMO, Trade generics and Exports business should lead to descent margin expansion in FY 26 + FY 27

Cipla and Alkem are the biggest companies in the trade generics mkt in India ( each clocking annual sales > 2000 cr in this segment )

Once plant 6 is ready ( should happen within FY 26 ), company shall be able to do an oral solids peak revenues of 1000 cr + 100 cr of revenues from the newly commissioned Injectables plant ( so a total peak revenue of 1100 cr from existing facilities )

The scope for growth for the company in Trade generics segment is huge ( as is evident from the size of Cipla and Alkem’s size of this segment )

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

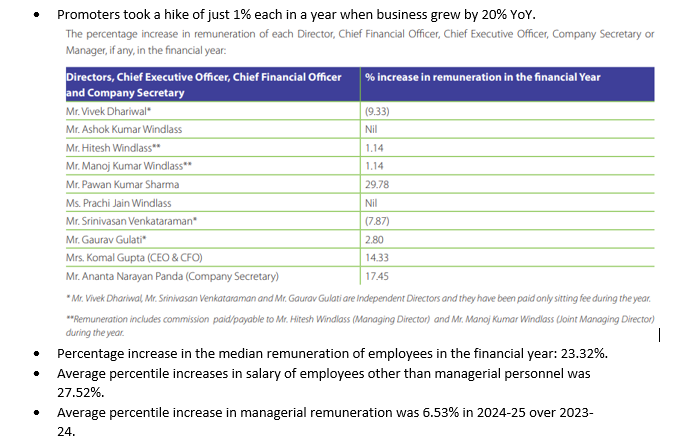

A noteworthy move by Windlas in FY25 was to grant significantly higher salary increases to non-managerial employees (average 27.5%) compared to managerial staff (6.5%). In a market facing a talent crunch, this proactive step reflects the management’s commitment to retaining and motivating its core workforce.

Source: Windlas FY25 Annual Report