Before buying any stock ask the following question to yourself

-

If the company is not profit making in the operation level,then I just through away the company from my list of thinking.I just don’t want to even think to take their names.The Indian unicorns Zomato,Paytm,BYJU etc…etc…all are loss making companies as on date.

-

People argue that these are cutting their losses day by day and will be profitable by 2-3 years.I don’t buy stocks of the company which is supposed to post less loss.I am not interested in companies which can make profit in future.I am interested in those companies which are making profits and will make profits in future.

-

I judge the companies in its ability to remain profitable and not just only profitability.Check if the company is profitable today ,and whether it will able to remain profitable for next 20 years.If you have doubt then simply discard the name.

-

A loss making company means simply a no from my side.

-

Do you really understand the business of the company or you are just buying because everyone else is buying that stock.

-

If you understand the business,then is it wise to put money in that business ? Yes ,you must ask this question to yourself.I am telling you my choice I don’t put my money in capital intensive businesses like Steel,Telecom,Automobile,Airlines,Energy companies etc.These companies need Rs.100 for running their business and earn Rs.10/- profit.Now even if they earn Rs.10 profit,they can’t give you back this Rs.10 entirely.Because ,they will need money for running their business.Lets say they can give you back Rs.2/- as dividend.Check the dividend paid by these type of companies,you will understand what am I saying.Don’t consider PSUs are exceptional ,just because they are paying good dividends.Look at their balance sheets.They are carrying huge debts.It just doesn’t make any sense.Its like someone who takes blood from the blood bank every month in order to be alive, but donating blood to others.Its simple economics if you have debt …pay the debt first…don’t pay dividends.They just pay dividends because their boss needs money.

-

Always judge the company by its ability to throw cash from its profits,to the shareholders as dividends.IT companies like TCS,Infosys etc. FMCG companies like ITC,HUL,Britannia,Marico etc can pay you almost all the profits as dividends.Because these companies are debt free and they do not need more capital for running their business.

-

Dividends are the only hard cash which an investor gets in his bank account.Ask yourself whether the company is paying dividends regularly.If yes,then the company must have very negligible debt.Because if debt is there,then there is no point in giving dividends to the shareholders.

-

If the company is not paying dividend,then ask yourself why is it not paying dividends? Remember that ,the very purpose of a company is to make money for its shareholders and the company creates it in terms of profit with hard cash.The only way it can reward its shareholders is by sharing profit with its shareholders by paying dividends and the capital appreciation in terms of rising stock price is a by product only and it is not in the control of the company.So,if a company is not paying dividend to its shareholders ,then it is like an unwritten promise to the shareholders that, dear shareholders I am not giving you the profits today,because I can use this money to make more profits for you in future.So,you have to check whether ,the company is actually retaining your profits for making more profits or it is just retaining it for its survival only.

-

My No List

- A loss making company.

- Capital Intensive company (Infra,Energy,Telecom,Steel,Cement,Automobile etc.).

- Public Sector Undertakings.

- The Business I don’t understand.

This is my learning …and it will be refined over time …because investing is an art…

18 Likes

Some of these tenets are being turned on their head. The PSUs are all the rage. Despite long gestation period, PSUs building ships and planes are all the rage. Coal India is every body’s darling.

I have long avoided the PSUs because they are inefficient. Defence PSUs because of high PEs. The Public Sector banks? The ROEs/ROCEs are pathetic 4 or so.

But where have most investors made money? Do you have the courage to stand on the side-lines and watch that?

Logic says ‘yes’, but watching others carry moolah in sacs, and not rushing out to join must take a strong heart.

3 Likes

Sir the credit cycle is turning. Even the worst run banks will probably make good money till the wheels come off in a few years. And some PSUs were too cheap to not go up now.

2 Likes

Sir…why I stay away from PSUs…1000 reasons not to buy…But if I have say it in one line,the leaders in the PSUs are chosen according to the sequence number (First in First Serve) in which they have joined in the organisation and where as other companies choose their leaders in merit.

So,a company having underlying process based on sequence number can’t beat a company having merit based process.

The low PE,Book value,Dividend yield of PSUs are just there to fool ourselves.

PSUs are like a cricket team…with following qualities

-

The most senior player will be the captain and will remain captain till age of 60.

-

You have a pre-defined bowling/batting schedule of players which you can’t change depending upon the match condition ,which is dynamic in nature.

-

The owner of the team is not interested in winning matches.

-

If virat kohli would have been in this team,he would be batting in no.8 perhaps.

-

Team owner can any time tell the players to hit wicket…just like oil marketing companies are selling petrol/diesel in below manufacturing price and taking losses.

4 Likes

Banks are the type of businesses …which can show profits but can’t share with shareholders.

So the only way shareholders can make money ,is by selling the shares .In other words, for making money in the banking stocks,you need to find another guy to put your shares in his demat account.

Because ,banks can’t give the profits as dividends.

What I value is ,the ability of the business to share profits to the shareholders from the EPS.

Banks,steel ,infra,energy,airlines,telecom companies etc. can’t share significant portion of their EPS with you.Because they need money for surviving.Here profits are illusionary.

2 Likes

To me the idea of investing is to beware of potholes even in a good road. One has to be careful while selecting a PSU/Public Sector Bank.

My dilemma is: I would rather buy a company with proven profit making history. But then when the market is chasing some companies, by the time these companies prove themselves, they may be too costly.

3 Likes

What I think…one rule works in stock market…the rule is “LOGIC”.If PSUs r carrying debt …then there is no point in giving dividends…

High dividend yield is bad after the abolition of dividend distribution tax. (Earlier companies were paying 10% tax on the amount distributed as tax, but now it is taxed at the hands of investors at their peak tax rate).

Now the sole beneficiary of the dividend distribution is the promoter and the govt. Promoter still pays tax but at lesser rate (10% ??) that too after deducting expenses and if promoter is govt (PSU co) who are they paying taxes to? To themselves?

Retail investors lose out in dividend play, unless you’re someone who doesn’t have any other source of income and hence below any meaningful tax slab.

3 Likes

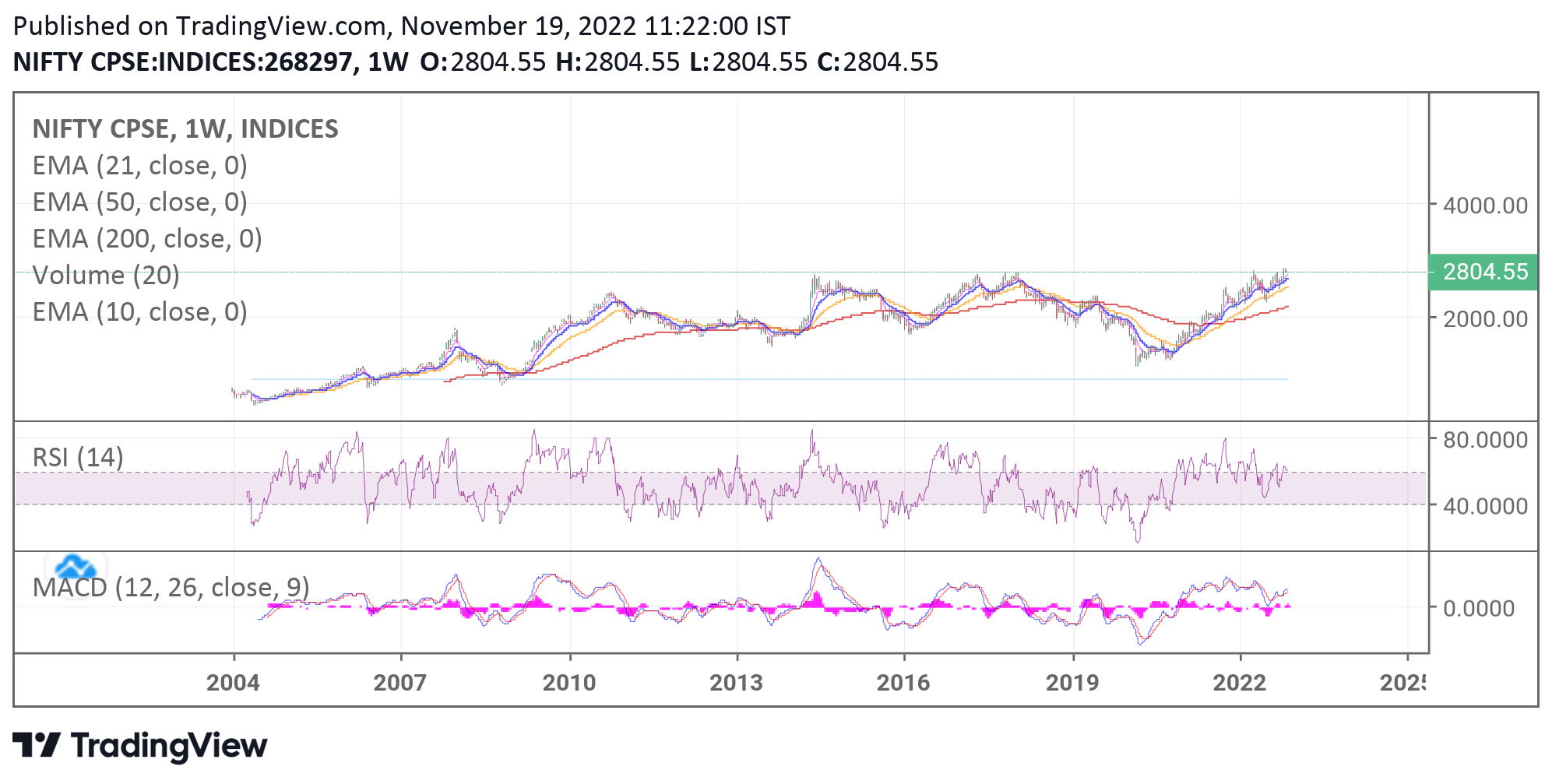

Whatever we might say about the PSUs with their obvious inefficiencies, the CPSE index is at an all time high breakout level on the weekly charts. If it can sustain for some weeks above this level, we will see much higher levels in the index. It may sound counterintuitive right now but market’s wisdom cannot be discounted. The markets clearly sees something here that we are oblivious to.

4 Likes