This data is taken from Screener.in. It is of Pincon Spirit. It shows that Operating Profit is rising but Working Capital Changes are eating the profit. It is increasing fast.

1 ) Is it fine? or this is a problem for business!

Any exception for this continuous negative working capital change.

Negative number implies that money is going out of the company…Not OK.

Negative number for Taxes: Good sign considering the fact that company does pay money to the Govt and profits declared by the company are real.Preferred number is around 33% as that is the norm for corporate taxes.

Negative Number for WC in the image you have shown: Not a Good Sign although negative working capital is a good sign. As major factors contributing to WC are Inventory and Receivables on asset side and Payables on Liability side…If company pays the suppliers faster (that is not able to hold on to suppliers money) and uses it’s own money in inventory (to buy raw material as well as produce the finished products) and in turn sells the product at credit (Receivables), it would lead to higher amount of working capital. That is companies own money is tied up in the business and ballooning of the same is not a healthy sign. Trust this helps.

FCF is negative - Increase in inventories also because of increase in Finished Goods. It might be possible that this is due to rejection of goods .

The managing director has given himself an unsecured loan of 60+ crores . Comparing with the PAT which is approx 25 crores , this amount cannot be ignored.

They have done an acquisition for 19 crores . Details of this needs to be understood.

Disclosure: No expert…Trying to learn and just crossed the phase of getting info from data. Hence, shared for the fellow Valuepickr. There might be mistakes or loopholes in my understanding and open for others help for course correction.

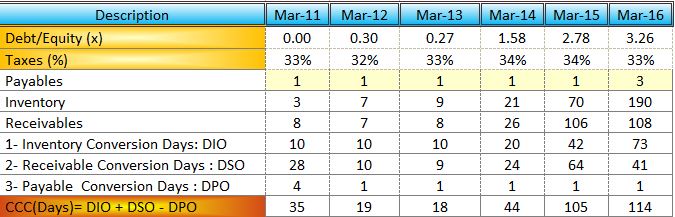

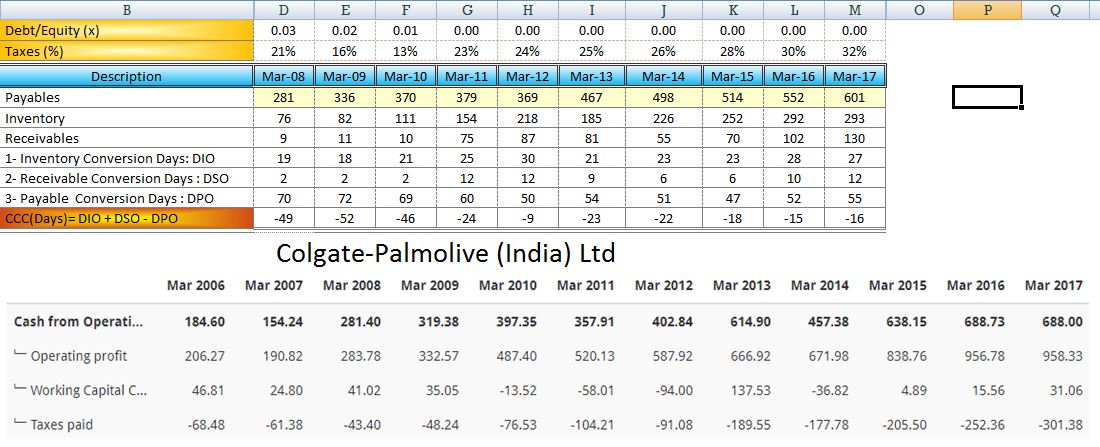

Below Image for Colgate shows an example for a better business-

Thank you @Surender for your reply. Refreshing the basic.

I know that Pincon spend lots of expansion. It has FMCG too. So, what to know if there can be any exception where negative WC can be good! Can capex make WC negative?

(Because we active investor looks for some exceptional stocks, we need to know all exceptions as well.)

Pincon revenue almost quadrupled in last 3 years (almost 60 CAGR). Net profit too quadrupled during the same period. This is unprecedented growth which can’t be possible without stress in working capital and debt. However, receivable days of 45 is in line or better than industry standard ( Radico Khaitan had 130 receivable days in FY16). It will be interesting to see the cash flow when growth slows down to 20 to 25% (60% CAGR is not possible all time).

@satya61229 Rather than just looking at any of the statements in isolation lets try to look at all the P&L,Balance Sheet & cash Flow as they tell the story in details.

Given below is the cash flow statements for last 3 years.

If you watch closely the cash Flow statements of PinCon (3 years from 2014-2016) you see that they have a -ve 186 Cr from Operations + they made around 44 Cr for Investing Activity.So 186+44 gives us 230 Cr approximately. Now that we know Cash equivalent of 230 Cr has gone out of the vault/company you look for the source for this cash.Now I need you to check the “cash from financing” figure which is exactly almost 230 Cr which shows that all the growth they are showing is funded through Debt. Now you might ask - how can we verify that ? Let me take you to the balance sheet of the company for proof of this

From the Balance sheet you see that the Total Debt has increased from 6 Cr (2012) to 253 Cr (2016) which tallies with what you saw on the Cash Flow from Financing for last 3 years.

I don’t want to emphasize Pincon Spirit here but today’s SEBI ban on Shell companies has made market tumbles. This company is in 331 companies that banned by SEBI.

@satya61229 Satya,

Working Capital and Capex are not related and both are bucketed under different categories in the Balance Sheet. In the balance sheet, Working Capital is arrived by calculating the difference b/w Current Assets and Current Liabilities whereas Capex is recorded under Fixed Assets(PPE) and CWIP. Also, working capital is the money needed to run the day today operations of the company.

Now, Working capital becomes negative whenever Current Assets are lesser than Current Liabilities.Ironically, liabilities as a name is Misnomer if you wear the hat of an investor.How? Just imagine a company that has the power to delay the payment to Govt (Deferred Taxes), Employees(Gratuity, Pension Plan, accumulated leaves etc) and suppliers (trade Payable). As a result, the business holds Other People Money without any collateral and uses this free money without paying interest or charge, which is needed in case of a Debt. As per accountant, it’s a liability as the company has to repay in future, but if the business can hold on to such money for indefinite period of time and the kitty keeps ballooning, the kitty is more of an asset than a liability. Hope this is as clear as muddy water

Regards.

Dear @Surender ,

Do you recommend any book for understanding financials of a company as investors. I am bearing the hat of investors and I want to understand that way.

Point is I read online but that much is not enough. I forget. I need to go above than the required so that i can retain the required.

In this context, I highly recommend-in case you missed it till now- the below articles from Professor Sanjay Bakshi that need to be read again and again as and when you pause for a moment after learning from various sources:

If you need to hone basics, I read and liked the book:

Another book that I would love to finish when time permits, midway right now, is from Jana Vembunarayanan who has the blog http://janav.wordpress.com

disclaimer: i am a learner of Financial Statement Analysis (FSA).

Personally I have taken the following approach in understanding these three statements, though I had some elementary exposure in my finance Mba. Mba is usually rushed through so the absorption and internalization didn’t happen for me honestly. Non CA folks were more worried their balance sheets would not balance!

If you are absolutely new to FSA then spend a weekend reading “The Interpretation of Financial Statements” by Benjamin Graham. Caution: its outdated. Objective is to get a peek into what these nomenclatures are all about.

You can skip the above book and go to what Surender has said “How to read financial reports by Tracy and Tracy”. This is the book which should give you confidence and form a base for further studies. Objective: to form a base for further understanding and serve as base. I keep revisiting certain things regularly. In my honest opinion this is a must read book for anyone interested in investing and I regret I did not know of this before.

Then the next book I think one must read is “Financial Statement Analysis by Fridson and Alvarez”. At the end of this I am sure you will be very confident.

But I keep referring back and forth to these.

Frankly I would recommend a valuation book in conjunction too and that is McKinsey on Valuation. You can try Damodaran on Valuation too but I had studied Damodaran in school and now feel McKinsey should be a must read first.

Other good/popular books which are recommended include:

Financial Shenanigans by Howard Schilit

Quality of Earnings by Thornton O’glove

Financial Statement Analysis and Business Valuation, Accounting for Value both by Stephen Penman

I have not read any of these 4 books yet.

Thanks Deepak.

Yes, reading a book on valuation is a must as that forces one to start thinking about a business. As of now, I am reading Accounting for Value by Stephen Penman and find it difficult to understand but stimulating enough to continue the struggle.The book is definitely not for a newbie as it not only demands the accounting know-how of the income statement and balance sheet but also written in a dense and incoherent language at least for my skillset.

On the other hand, I find this as an excellent book as it provides a good anchor on which valuation should be based without considering the Price established by the Mr. Market or the Cash flow of a company. Also, it provides various tools and techniques to an analyst to challenge the prices set by market while describing the shortcomings of commonly used valuation methods such as DDM, DCF, P/E etc.

On a lighter note, a wise man has said that trust on counter party (read as management) matters more than Balance Sheet, Income Statement or cash flow statement in a developing economy.

Basant Maheshwaris thoughtful investor is also very nice. You can also use the search string “link:forum.valuepickr.com” in google to hunt for interesting sites that reference valuepickr and you will find a goldmine of little known blogs full of useful info