Established in 1985, Welspun India today, it is one of the top three home textile manufacturers globally and the largest home textile company in Asia. It has modern manufacturing facilities at Anjar and Vapi in Gujarat where it produces an entire range of home textiles for bed & bath category. The company has state‐of‐the‐art completely vertically integrated plants, right from spinning to confectioning.

Welspun has been ranked No.1 among home textile suppliers in the US (Source: Home Textile Today). It has a distribution network in over 32 countries including US, UK, Europe, Canada and Australia.

In addition to manufacturing facilities, which predominantly supply to private labels, the company also maintains its own brands Christy, Hygrocotton, Welhome and Spaces ‐ Home and Beyond; it also has a tie up with Nautica for North American markets

Story in charts:

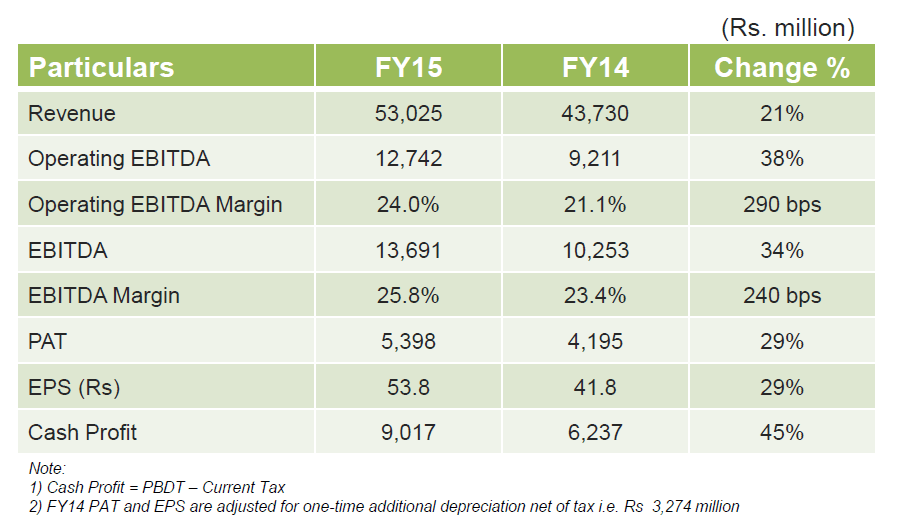

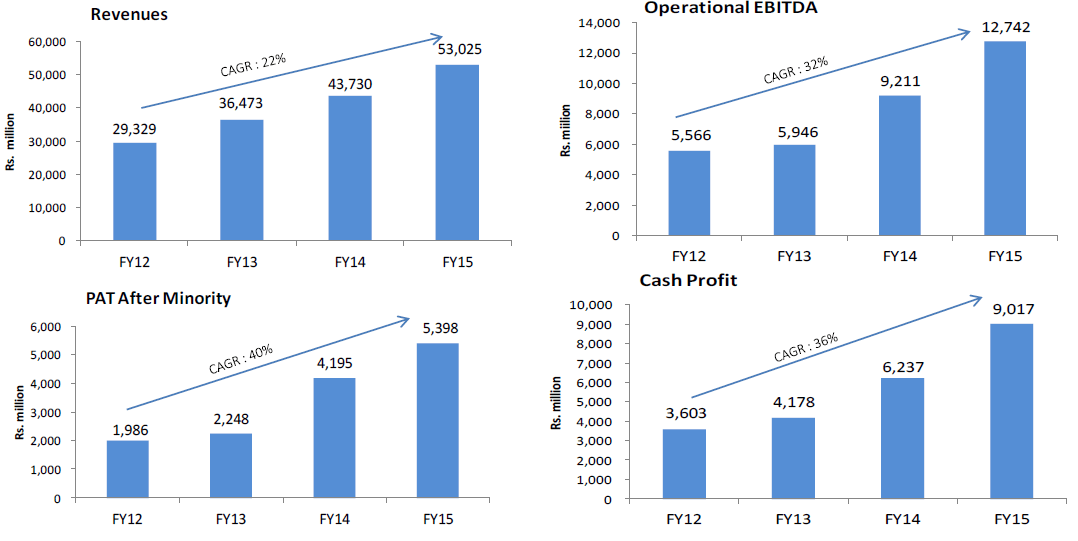

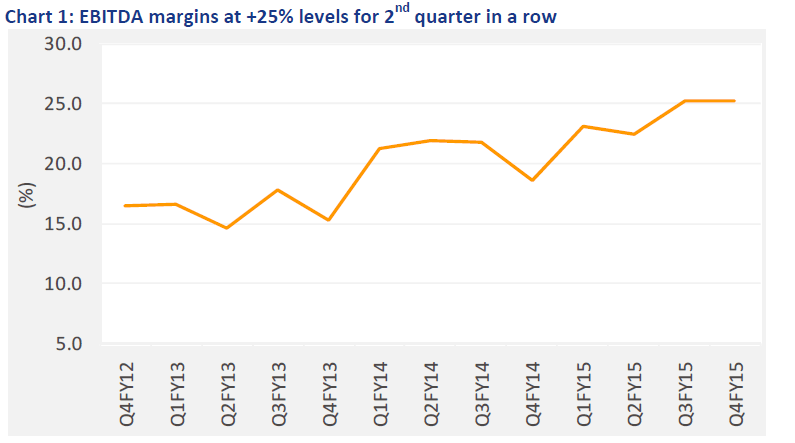

As we can see from the above charts - the financials have showed steady upward trend in last 3-4 years. Most striking feature has been the margins - now clocking upwards of 25%. Management have in conference calls and TV interviews have rigorously mentioned that they will surely maintain atleast 22% margins. I have had few rounds of Q&A with the investor relations team - they have mentioned that 22% is bare minimum which they will achieve in coming years. This 22% is after considering that govt. takes back some of TUF incentives (textile co’s get loans at reduced rates and company thinks that these and other similar incentives might be taken back in few years). If one goes through company presentation - there they mention share of branded (high margin category) is at 11% and growing rapidly (40% CAGR over 2 years). Innovative products accounts for 31% of revenue.

They are also backward integrated to a large extent (75%) and will be spending total of c2300 cr for modernization/capacity expansion/backward integration. Of this 2300 cr., 50% is already spent and other 50% will be spent in coming 1-2 years. After my interaction with company - I really dont feel that margins would fall below 22% in next 2-3 years atleast.

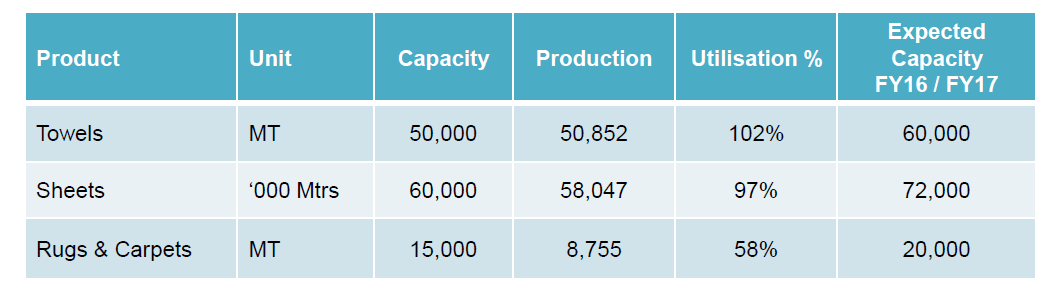

Sales - Company have guided for ~15% growth in sales for foreseeable future. (next 2-3 years atleast) One can get a fair bit of idea about growth looking at their capacity/utilization and future capacity expansion plans.

Here also, management has suggested that for current year 80-90% of sales is pre booked. We can see that both towels and sheets are operating at full capacity - in rugs and carpets they are slowly increasing capacity,this is new product segment launched last year - the IR team mentioned that they see high growth in it and expect the utilisation to increase in coming quarters. For Towels and sheets - they have visibility for 2-3 years and expect the increased capacity will be fully utilized as well.

Hedging - as 95%+ revenue is from exports, the company have a policy of hedging 60% of its next 12 months revenues. As per IR the hedged rate currently for next 12 months is at 64+

If one looks at income statement - the power fuel and water charges has remained almost at same levels in FY 15 vs FY 14, even after 20%+ jump in revenues. Figures for last 3 years - FY 13 figure was 263 cr, FY 14 at 117 cr and FY 15 stood at 119 cr. This is because the company have own captive power plant of 80MW which is providing electricity to all manufacturing units in Gujarat. This power plant is jointly owned by other Welspun group company. Welspun India owns 68% in it (the figure can be cross checked from AR, dont remember the exact %). Thus, this captive power plant would further help to control costs.

Also, its interesting to note that capacity would be increased without increase in headcount. Hence, saving in manpower cost.

Pricing with customers - The Company has a price variance Index with clients which includes Cotton, Currency, Dyes and Chemicals etc. The threshold level of increase and decrease is +/- 5% on overall basis which decide the price cut or price appreciation with the clients once in 6 months. Thus, if the price of cotton rises or falls - the same would be passed on to the clients.

Now comes the only negative point which I can sense (would be happy if others can point out any other negatives) - Debt - Current net debt stands at 2600 cr and management have suggested they wont let it increase further from 3100-3200 levels at time. Interesting part about the debt is that ~60% of this debt is low cost (TUF and Gujarat benefit). Current blended cost of long term loans is 7% and after Gujarat govt benefits it can come down to 3% levels. If debt is available at 3% and company can manage even 10-15% ROE - I believe its rational to have debt. However, in this case company is earning much higher ROEs. The IR team suggested that they don’t plan to pre pay low cost debt (which makes complete sense) - however, after 2 years when the capex is done with - debt levels should come down significantly.

Dividend policy - the company recently announced dividend policy of 25% of PAT - this I believe is a great positive - even after having debt (though low cost) and planned capex, having stated dividend policy shows confidence in sustainability of profits/margins/cash flows.

Valuations - the stock trades at relatively lower levels compared to peer such as Indo Count. The only major point of difference between both being debt. In terms of margin profile/backward integration/scale - Welspun India fares much better than Indo Count.

Views are invited. Its safe to assume Welspun India forms part of my portfolio. The charts are taken from company presentation here and here (which I believe is self explanatory in terms of Industry tailwinds and financials, etc) and 1 from edelweiss report. Introductory paras taken from edelweiss report.

This link is also good to know more about the company and future plans.