Welspun launched its online platform in India & US

The results were tad below expectations on topline front but was more or less compensated by the continued momentum in bottom line.

Reason for just 4% growth in top line was mainly due to capacity constraints - full year top line growth guidance of mid teens ~15% is maintained (implying higher growth in second half). Also, this ~15% growth is not for this year, but for next 4-5 years. If one goes back and read previous conf call transcripts - management have always maintained that they see mid teens growth for next many years. They don’t want to guide for a year or few quarters - they want to guide whats sustainable. Also, they don’t want to expand and wait for demand - would rather want demand to chase capacity (indirectly hinted towards Trident who have possibly done huge capex in Towels and have supposedly idle capacity)

Important points in call -

TPP will have no impact on Welspun (this was mentioned in Q1 call as well)

TUF loans - ~80% of capex have TUF benefits and will continue to have benefits till these loans are paid off. Thus the noise on TUF being taken back wont impact Welspun.

Current levels of debt are almost peak levels - may be 100cr here and there. From next year onwards debt levels would fall.

Overall, their target is to reach $2.5bn in revenue by 2020 (implying >20% CAGR in revenue), however Mr. Rajesh Mandawewala suggested to base expectations/forecast on the basis of ~15% CAGR in revenue for time being. He suggested company is doing many exciting stuff and will disclose at appropriate time the new avenues/segments of growth.

Dividend - it will be 25% of standalone profit.

Overall, it was very good conf call. Don’t see any reason why Welspun should trade at discount to its peers - given the visibility and leading position they have in industry.

Disc: Invested

2 Likes

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/B3FA9655_4FDA_4DD2_BDA4_91B97C11F387_131453.pdf

Very decent uptick in every measure

EPS 17.33 vs 14.3 (Y on Y)

Gross sales 1490 cr vs 1345 cr (Y on Y)

Plus 1:10 split as well

Concall today evening

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=4d780566-57ca-44d5-95e9-822e01814e8f

1 Like

Q3 results were mixed - with topline growth being slightly below expectations, though bottomline saw adequate growth aided by margin expansion & reduction in interest expense.

Main takeaway from the conf call was increase in guidance in terms of operating EBITDA margin - from ~22% to 23-24% range - this is due to increasing share of innovative products in its portfolio.

Also, reiteration of topline growth of mid teens for next few years. However, given the current environment - management said they are giving a bit cautious guidance of 13-14% revenue growth for next year.

Debt levels would also start reducing gradually from next FY - this will add to bottom line growth as interest expense reduces.

Broadly, the initial thesis around the idea seems to be working out as expected. Revenue growth visibility, favorable industry environment for most Indian players, Welspun’s leadership position in the segment, gradual reduction in leverage leading to comfortable debt levels & some re rating.

Recent update report by Edelweiss for Q3 result covers all the points/facts in nice detail and is a good read.

Disc: Welspun India is top holding for me. Views will be biased.

1 Like

- 20% YOY Q4 profit. Rs 193.29 cr

- Vertical integration and commissioning of spinning unit has driven EBITDA margins

- Innovation and Branded products to drive margin forward - around 20-24%

- CAPEX of 800 cr planned in FY 17 which includes 300 cr carried forward from FY 16

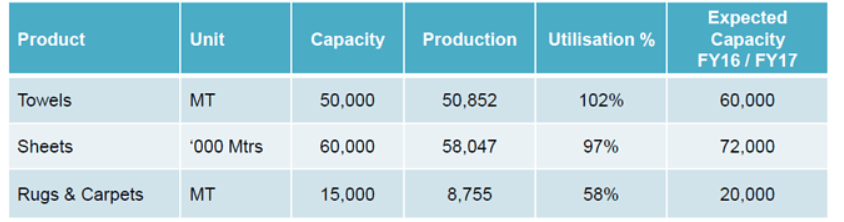

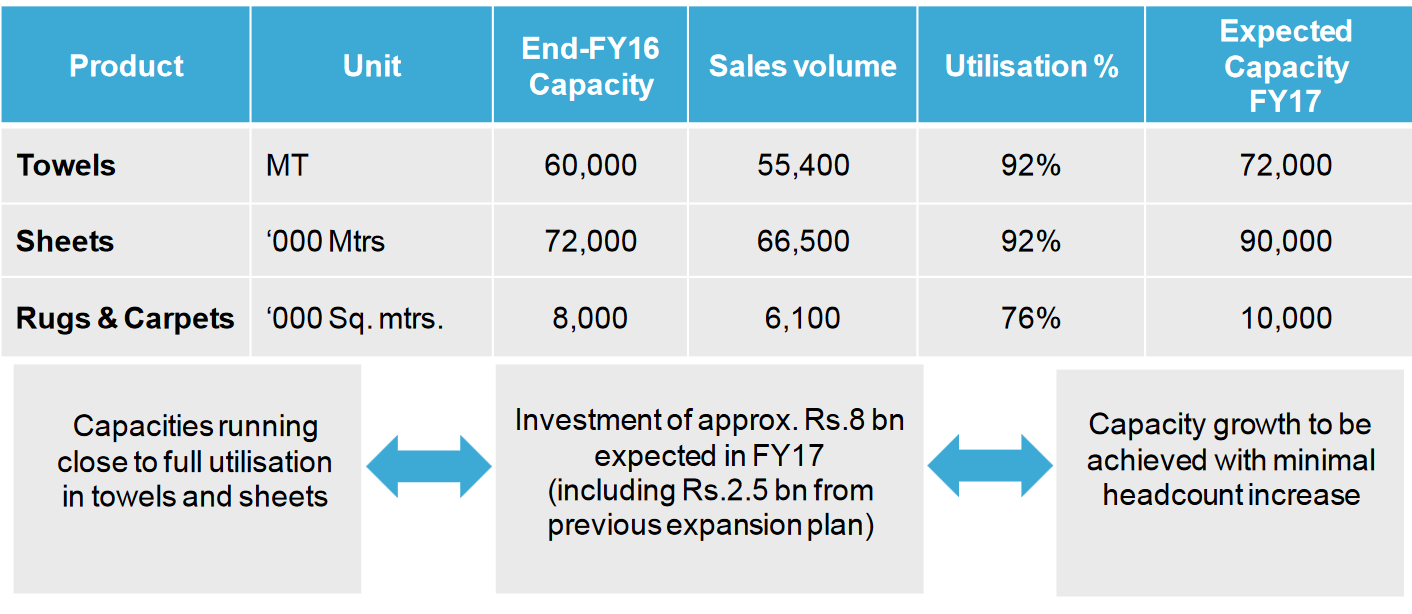

- Company looking to expand production capacity. Towel capacity to go up from 60000 to 70000 tonnes, Sheet capacity from 72 to 92 lakh metres

- Net Debt gone down by 500 cr, company aims to be debt free by 2020

- Focus on domestic market as well from now onwards apart from US

Disc : hold some shares since Aug 15, planning to invest more.

Major Source :http://m.moneycontrol.com/news/results-boardroom/vertical-integration-spinning-unit-helped-marginswelspun_6389621.html

How much profit growth can be attributed to INR depreciation. What would be the growth if INR was at 62?

Q4 results were very good and overall the story looks very much on track.

The annual investor conference webcast was also good wherein the company for the 1st time outlined their vision for 2020. Would suggest everyone to have a glance at the presentation - its available on company website & exchanges. During the conference the management suggested their focus is on ROCE and not just on increasing sales - all investments made by the group is made keeping in mind this metric.

@Vijayk - in FY16 the company did volume growth of 12% while revenue grew by 13%. Realisations in USD terms were down 2% but INR depreciation of 3% overall helped to increase realisations by 1%. INR depreciation had no role to play - The Company has a price variance Index with clients which includes Cotton, Currency, Dyes and Chemicals etc. The threshold level of increase and decrease is +/- 5% on overall basis which decide the price cut or price appreciation with the clients once in 6 months.

If INR were at 62 - then we would have got similar growth numbers cz then there would have been no need to revise down USD realisation in first place.

1 Like

If INR Had appreciated by 3%. Realizations would have been down 4%. Right? And any change on top line without effecting cost directly affects bottom line. Right?

I dont think we can assume changes in realisations by ourselves assuming movements in FX. As mentioned earlier - they follow index based approach and it has many things included in it - and not just FX.

As per me broader picture is this -

-

they have been growing volumes in double digits historically, will continue to do so over next 3-4 years- this is validated by their historical and future capex plans and utilization levels.

-

Indian (home) textile industry is facing some nice sustainable tailwinds - also given govt’s push on textile front - there are bound to be some winners

-

Welspun is without doubt industry leader by some distance and deserves premium/good valuation.

-

Gradual reduction in debt, consistent performance, good dividend payout - all these should result in some more rerating. Current valuations don’t discount even 20% earnings growth --> low downside.

-

Any breakthrough in technical textile/smart textile space can be additional upside to the story - and this is the bridge to their $2bn USD revenue goal by 2020 - already many things can be found on internet regarding this and one can try to connect the dots.

I would not be much concerned about FX - if you are hinting towards competition from China - then relative movement has to be more than 10% for any change to happen in competitive scenario. Or if there are concerns about rupee going to 55-60 levels - then I believe we might see some good correction across the board in all export related stories and margins might come under pressure for all such players.

1 Like

Disclosure - Welspun is among my largest position.

1 Like

Their Vision 2020 is to have revenues of $2BN by 2020. Revenues for FY16 stands at less than a Billion $.

Looking at revenues for last 4 years they have grown 85.62% at a CAGR of 16.72%.

To achieve that they have to grow at CAGR of around 21% in top line. With most of the growth already occurred (India’s share stands at 38% in towels & 48% in sheets which increased at very good rate of 21% in last six years - I have to find out what Welspun’s share in that.) how realistic is that goal can be? On top of that they have a debt of around 2600 cr. that they are planning to make it Zero by 2020 (Once capex requirements is done they probably try to clear the debt).

Their domestic market revenues has grown at an excellent 40% in last two years. Does anyone has idea of with what all retailers they collaborated domestically? One of my friend has looked it in Reliance retail and he didn’t personally liked the towels. Also, is the pricing in India is attractive to a common man? I see they have patents in patterns and stuff, does that play a vital role in Indian market? Who will in India buy a towel just because it’s pattern has a patent. I think domestic revenues will play a major role in achieving that task.

What I personally like is their CSR activities. Management is showing very good interest in these activities. Dipali has talked about the change they want to see in a TED talk here (though it’s 4 years old video): TedxTughlaqRdChange - Dipali Goenka - YouTube

Also, their capacity expansion plans are on track. Whatever they aimed for FY16 is fully achieved and more expansion is on cards for FY17.

Plan for FY16:

Plan for FY17:

Most of the data is taken from their Q4F16 presentation: http://corporates.bseindia.com/xml-data/corpfiling/AttachHis/C642C6A5_9001_4128_9CDC_04CE2A707F25_121418.pdf

Disc: I have bought few shares at avg price of 97.44. It is about 9% of my very small portfolio.

Note: This is my first post in Valuepickr, I am assuming I have conveyed the message that I want to.Views are welcome.

1 Like

3 Likes

Seems like a serious offense given Target was #2 client for Welspun India. Since Target has snapped ties with it can possible have following repercurssions:

-

Contagion effect: Other clients might also investigate the issue and possible couple of more clients may snap ties with Welspun.

-

Competitors to gain: Competitors like Indo Count and GHCL might just capitalise on this opportunity and gain market share.

In both the conditions its a lose-lose situation for Welspun. We just might see Indo Count benefitting from this news.

What next:

This event IMO has changed investment thesis for Welspun India given target was on of its Top 3 clients and Cheating clients dent managements credibility significantly. New business might not come easily from hereon or might come at competitive price (affecting margins). One needs to evaluate the risk reward ratio from hereon.

Discl: No investment in Welspun. Exited ICIL before its entry into F&O

1 Like

Target severs ties with Welspun

Stock in LC

PS - invested and cringing

1 Like

Welspun India gets tangled in knots

(Target terminates contract with Welspun India because the firm, according to Target, substituted Egyptian cotton with a cheaper variant while supplying bedsheets)

This appears to be such a blunder on part of Welspun to risk reputation which could have huge consequences. Could loss of Welspun mean gain for competitors like ICIL, HimatSingka or It could affect them as well? Well, I’m not sure so let’s wait and watch the developments.

On the other side, how much a single client, though being second largest and accounting for about 10% of total revenue shall matter in the long run to large supplier like Welspun? The stock is already down by 20% and looking at the seller’s queue looks like more pain is in the offing.

It would be interesting to know how the mgmt responds. If anyone attended today’s concall, kindly share the notes. Thanks.

Disc: Invested in ICIL and HimatSingka

Welpsun conducted a conference call after Target announced to end its business relationship with Welspun. The key takeaways from the call were:

The external audit will be completed by 6-8 weeks.

Target found issues with only 10 percent of products supplied by Welspun.

The company acknowledged that fault is likely to be with their own systems.

There were no quality or safety issues with the finished product supplied; the problem was with the origin of the raw material.

The company supplied the same product to several other clients. Total sales of similar products constituted 3-6 percent of Welspun’s sales over the past few years.

The sales from U.S. account for two-thirds of Welspun’s sales.

Apart from Target, Welspun is a major supplier of towels, sheets, rugs and carpets to 18 of the top 30 global retailers, including Bed Bath & Beyond Inc., Wal-Mart Stores Inc., J.C. Penney Co. and Macy’s Inc.

Source: Bloomberg

2 Likes

This is definitely a blow on management credibility to not supply as per contracts and not keeping the customers happy. Indo count and others might have an advantage here. But my only concern is i hope its not an industry wide practice to replace/dilute expensive raw material with non expensive one, since the leader of the pack is doing it, why cant others? Although it boils down to individual management qualities.

Disc. hold indo count.

Sheer greed by mgmt. or what else?Now other big clients will be suspicious too!May go into deeper crisis n other Companies also come under review too!!!

I am not sure any management (however dumb it may be) will take a conscious decision to do something like this, especially to make paltry additional money by using a cheaper raw material. Quite possible that due to production target pressure a material that was available was used instead of waiting for the right raw material to be available. This happens quite often in manufacturing, while the intent is not to cheat but to meet the production targets. Of course it has now impacted the credibility however personally I think this is a one off event specific to welspun and should not impact other companies.

3 Likes