Kirloskar Electric has collaborated with the Nuclear Power Corporation of India (NPCIL) to develop special motors.

May be there’s a lot promised in budget speech but much less done on papers … hence, subdued growth.

2 Likes

can you share a link of it? Thanks

It’s given on their website in Nuclear section.

1 Like

February 06, 2025, approved the Un-audited (Reviewed) Financial Results for the Quarter and

Nine Months ended on December 31, 2024

When I entered the company, I thought it will be a turn around after restructuring as initially the losses are narrowing. However the recent results are kept disappointing. I believe, I’m being lucky to enter early rather than convinced about the exact time frame of structural turnaround. The recent QIP and no commentary from the management is not adding any confidence. Further, the recent drawdown in micro cap companies and hot themes is reminder to learn more. So I decided to admit my luck and exit the counter. May be the real turn around happens in coming quarters.

Disc: No holdings

3 Likes

In terms of seeing a turnaround, one usually sees himself few quarters ahead of time. If both conviction and margin of safety is high, it usually pays off to wait for a few quarters more.

1 Like

Pls check the facts. AK has not reduced the stake. It’s coz of the warrants conversion, the stake %age has reduced.

Yes, Ajay Upadhaya has exited.

Subhkam Ventures group have added up quantities.

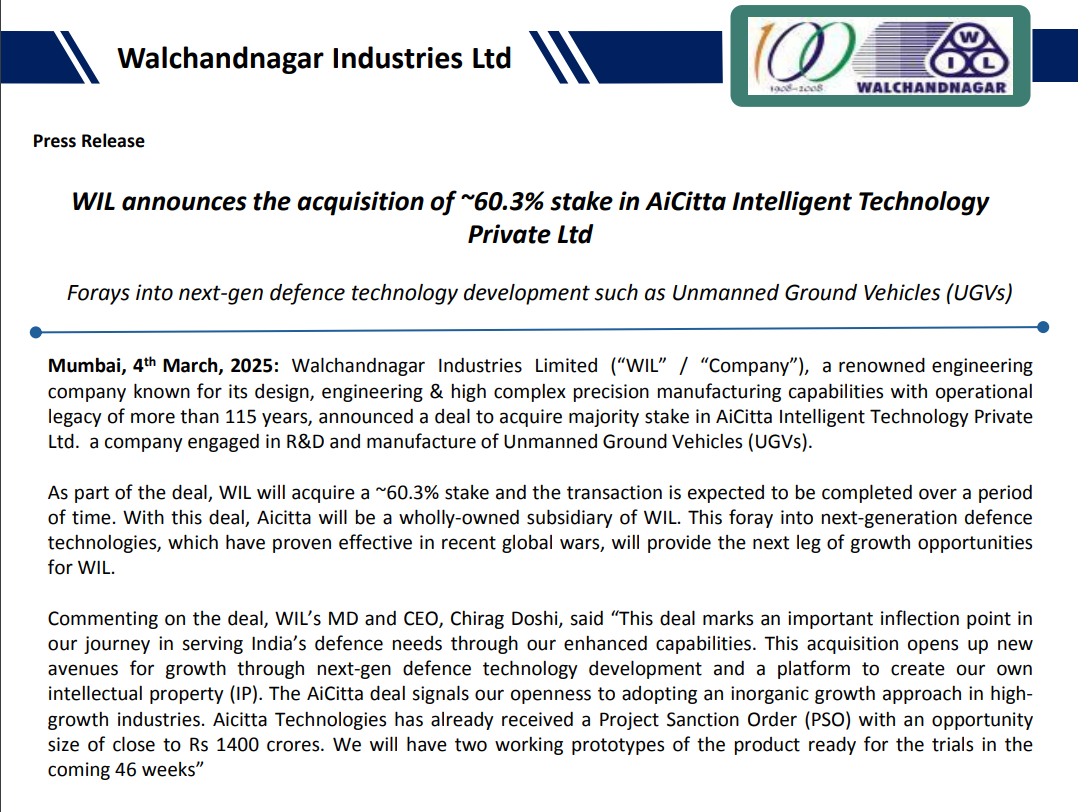

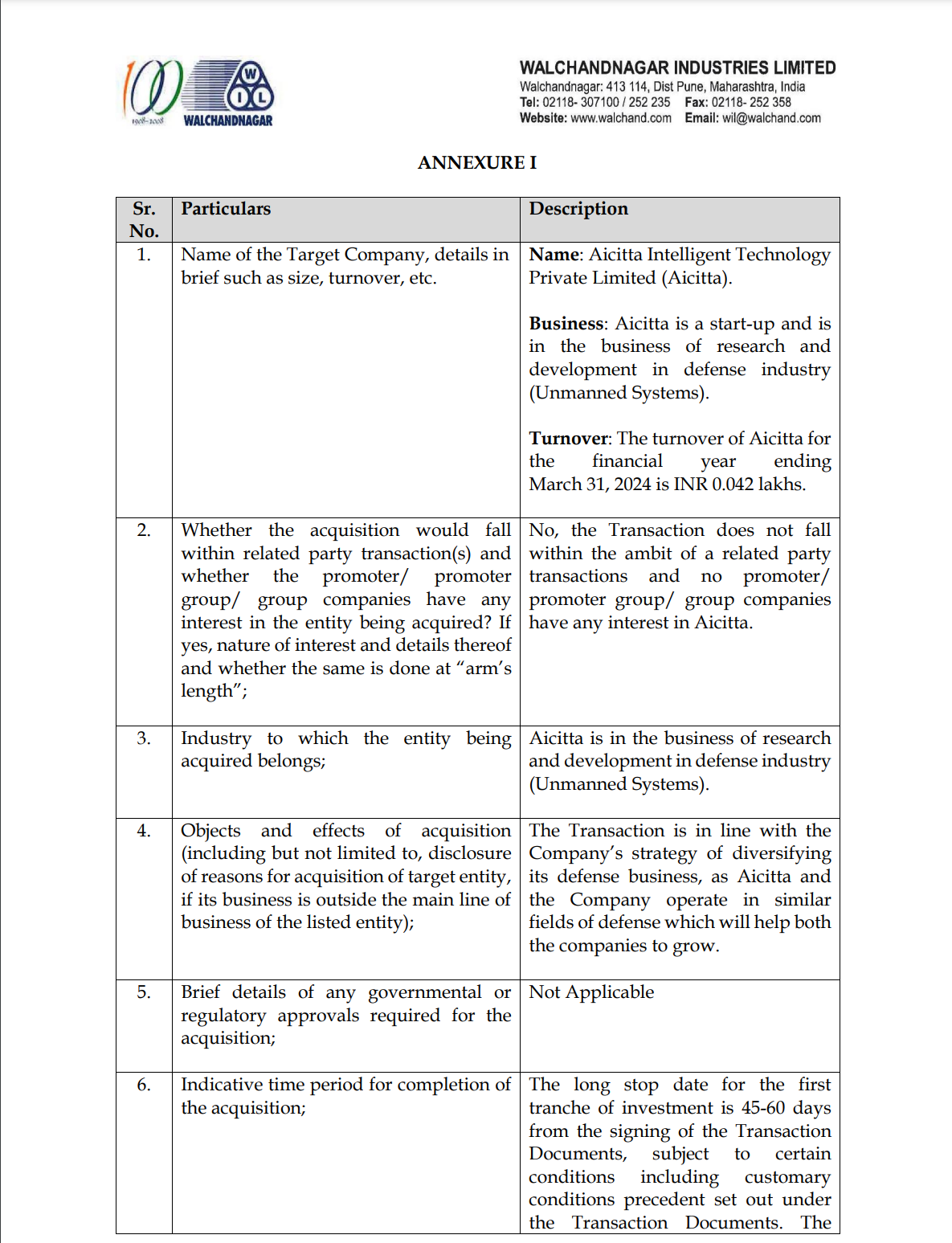

Walchandnagar Industries approved acquiring a 60.3% stake in Aicitta Intelligent Technology, a defense R&D firm, for up to ₹16 crore.

The investment, via equity and preference shares, will be completed in tranches over 31 months.

→ Acquiring Aicitta to diversify defense business and expand in unmanned systems.

→ Aicitta specializes in R&D for the defense industry.

→ Financials:

- FY22: ₹1.15 Lakh

- FY23: ₹82,823

- FY24: ₹4,250

→ Strategic move to enhance capabilities and drive future growth.

2 Likes

Yes, but couldn’t find a website or LinkedIn corp page for AICITTA INTELLIGENT TECHNOLOGY.

They should have some online presence.

https://www.zaubacorp.com/AICITTA-INTELLIGENT-TECHNOLOGY-PRIVATE-LIMITED-U72900KA2018PTC116004

Founded in 2018 it seems.

Peer Analysis by Company…not seen by any other companies doing so..especially for defence and aerospace.

One thing, I couldn’t understand, How to decide the valuation of this company that has same capabilities as L&T. Or it’s Just an record from the history, because the last **Acquisition of Aicitta doesn’t seem well for me, as they accquired company that is degrowing or with no revenues for 16Cr.

Disc: No holdings.

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/2640d907-f72c-4def-89ed-87458b612ee8.pdf

1 Like

The acquisition may be for the technology rather than adding to their income statement. Not sure but just my thoughts.

Walchandnagar Industries’ Growth Push: ₹38.49 Cr Capex & Clean Fund Utilization | MCap 1,434.19 Cr

- ₹38.49 crores allocated for capital expenditure, signaling growth plans.

- Total funds raised: ₹247.59 crores (₹213.54 crores from investors, ₹31.59 crores adjusted against loans).

- Funds raised via Fully Convertible Equity Warrants on November 03, 2023.

- Utilization as of March 31, 2025: ₹31.59 Cr (promoter loan repayment), ₹45 Cr (term loan repayment), ₹38.49 Cr (capex), ₹60.90 Cr (working capital), ₹20 Cr (general purposes).

- Audit Committee review on May 14, 2025, confirmed no deviations in fund usage.

1 Like

Horror show continues…

I have few friends who worked in this company in the late 90s and early 2000’s and they said that working there felt like working in a large PSU company. Product technical complexity is fairly high but no focus on cost budgets and timelines. Its relic of the past era and financials bear that truth time and again.

Company continues to disappoint its ardent followers and dreams of investors have turned into nightmares… ![]()

7 Likes

I have been following this company as well as this thread for more than a year. It is heartening to see the overall positive commentary by investors following this company. Capabilities and profile is top-notch. However, it has failed miserably on growth vis a vis prospects. Why it is so?

I do not prescribe to the view that if it had semi Govt culture 20 years back( big if), it continues in the same state.None the less it has consistently failed to live upto it’s potentiality. So I have serious misgivings about the company grabbing recent opportunities on developments on nuclear front. It is high time it’s management to deliver or cede ground to fresh bones.

Presently have no holdings.

3 Likes

While going through the company: WALCHAND NAGAR

More than 4 decades of experience in the critical and precision equipment segment.

Walchandnagar Industries is a long-standing supplier to ISRO.

They are providing critical launch vehicle hardware such as motor casings, booster segments, and nozzles.

Over 50 years of collaboration with ISRO, starting with SLV-3 in 1973, supplying for ASLV, PSLV, GSLV Mk II/Mk III, and SSLV programs.

Delivered 200 S139 segments integrated into PSLV and GSLV Mk II flights. WIL is the only Indian manufacturer of Head End Segment (HES) and Nozzle End Segment (NES) for these.

WIL is the only player in the country manufacturing Head End Segment (HES) and Nozzle End Segment (NES).

Head End Segment (HES)

Forward/top (near igniter/forward closure). Interfaces with vehicle structure. Houses fittings/attachments. Withstands initial pressure surge.

Uses : Star-lobed (multi-point star shape) for high initial burning surface to rapid thrust buildup.

WIL’s specialty: Only Indian maker. Delivered in S139/PSLV sets. Part of Chandrayaan/Mangalyaan missions

Nozzle End Segment (NES)Aft/bottom (connects to nozzle). Supports nozzle mountings, bearings (for gimbaling/TVC), seals. Handles high thermal/structural loads during burn.

Cylindrical bore (with taper) for sustained/tail-off burn. Often includes floating piston for casting/proofing.

WIL’s specialty: Only Indian maker. Includes nozzle hardware integration. 200+ S139 segments supplied by WIL.

Also WIL is a key player who supplies critical components to the nuclear ecosystem with over 40 years partnering DAE (Department of Atomic Energy).

Pre-qualified for Class 1 nuclear components (highest safety class).

Focus: PHWRs (Pressurized Heavy Water Reactors, India’s mainstay).

Key Customers

NPCIL (Nuclear Power Corporation of India Ltd.): Primary for power plants.

BARC (Bhabha Atomic Research Centre).

BHAVINI (Bharatiya Nabhikiya Vidyut Nigam Ltd.): Fast Breeder Reactors.

DAE: Overall strategic partner.

Partnered with the Department of Atomic Energy (DAE) for over 40 years.

Pre-qualified to supply Class I nuclear components.

Specializes in manufacturing and supplying core equipment for nuclear power plants.

Reference Company Presentation (May 2025).

What is PHWR?

PHWR stands for Pressurized Heavy Water Reactor, a type of nuclear power reactor commonly used in countries like Canada (CANDU design) and India (IPHWR variants).

Why financial is not strong ??

WIL has strong credentials in nuclear (PHWR components like calandrias, end shields, moderator heat exchangers) and space/ISRO (e.g., Rs 30.75 crore VSSC contract in March 2025), but persistent operational disruptions, high debt, execution delays, and losses have eroded profitability.

Recurring Plant Disruptions at Satara Facility.

Recent adverse event in 2025 :

Temporary suspension due to worker unrest (Announcement).

Impact : Production halt = dent in profit

Some orange flag for me not red flag :

Recurring labor unrest eroding profits/capacity

Satara PlantSuspension Mar 20, 2025 (“violent acts”); lockout Apr 12–Nov 24, 2025. ₹27 Cr revenue loss; phased restart Dec 20.

Impact : Foundry rev down 53% FY25; EBITDA drag.

WalchandnagarStrike FY24 (prior).Credit report: Foundry slowdown key rev decline factor.

Benefit Walchandnagar Industries Ltd (WIL)

Recent Catalysts (Dec 2025):

SHANTI Bill (Sustainable Harnessing & Advancement of Nuclear Energy for Transforming India): Passed Lok Sabha Dec 17, 2025. Opens civil nuclear to private players (licensing for reactors/fuel fabrication/transport/import-export); caps liabilities; strengthens regs/fund. Rajya Sabha pending.

Nuclear Energy Mission (Budget 2025): ₹20,000 Cr for indigenous Bharat Small Reactors (BSR/SMRs); 5 operational by 2033; supports 100 GW nuclear by 2047 (from 7.5 GW).

Direct Benefits to WIL .

Direct Benefits to WIL (Pre-qualified Class-I supplier to NPCIL/BARC/BHAVINI; 50+ yrs legacy).

5 Likes