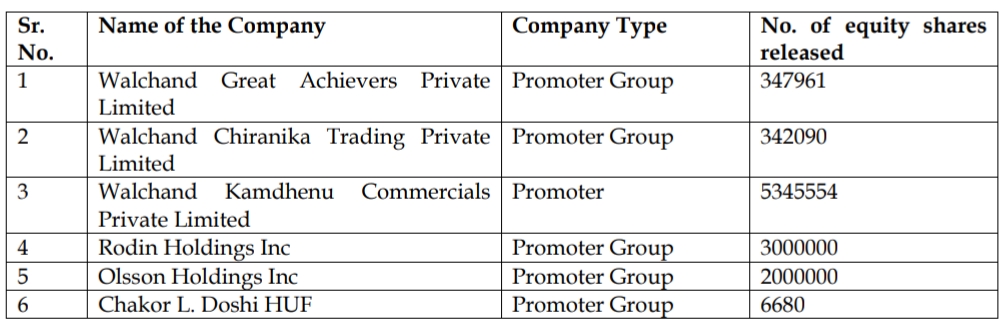

The promoter and promoter group has notified Release of Pledged shares totalling 17,006,331 shares on 29th July 2024.

5 Likes

Rating Update

2 Likes

I don’t think the results are that great.

-

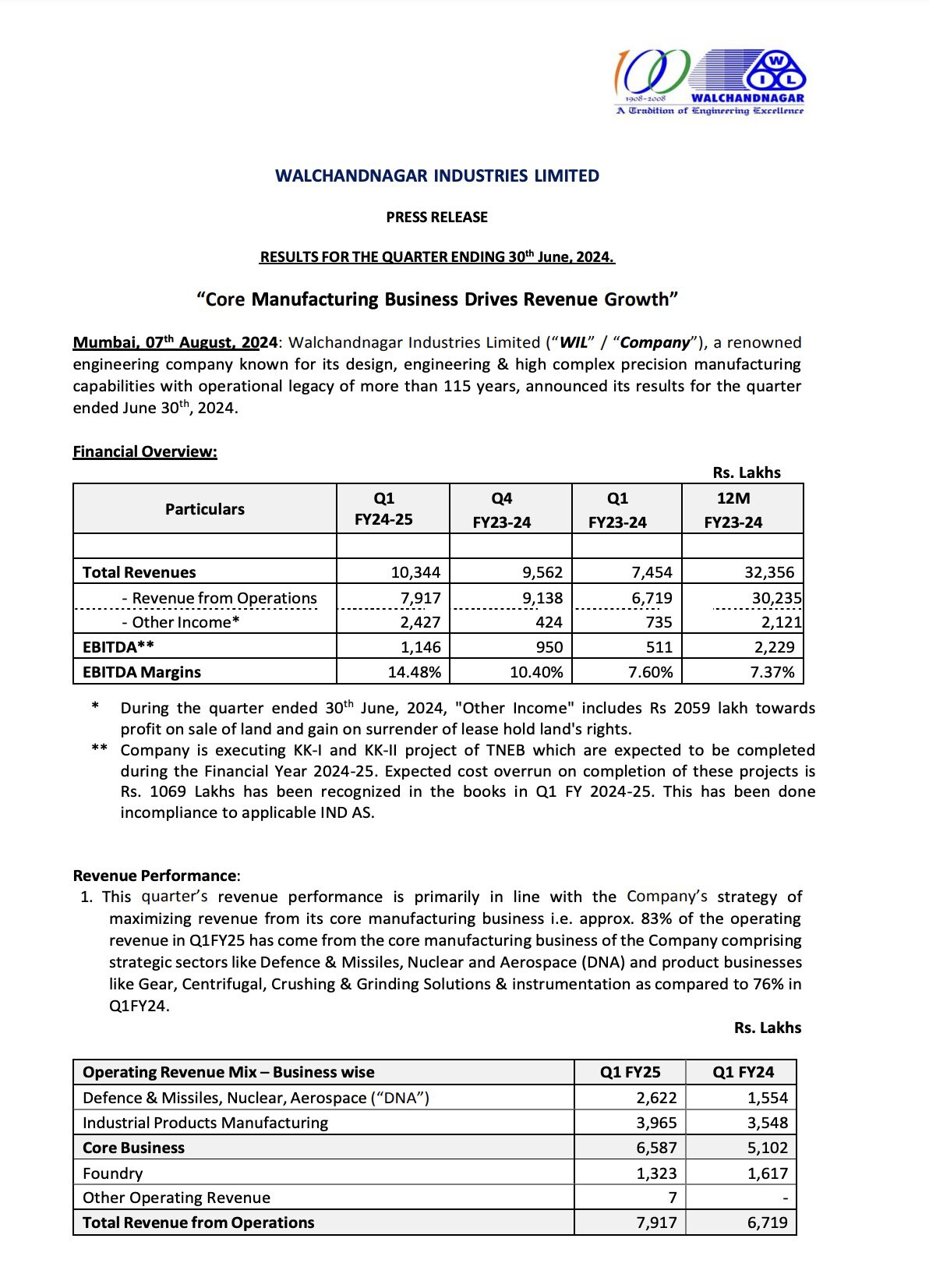

The operating costs of the company seem out of control. The expense to operating revenue ratio has surged to 1.32 ( 1.28 in Q1-24). The effect is not visible due to high other income on sale of land (2059 lakhs) which is exceptional in nature.

-

Ignoring the impact of exceptional other income, the Loss stands at 2232 lakhs ( 1141 lakhs in Q1-24)

That is widening of 95% approx. -

The revenue of Foundry business has taken a hit of 18% yoy. No particular reason provided by the management for this variation.

-

Order book of 33,930 lakhs is on hold from customers end. No visibility of materialisation of the same.

Ofcourse the impact of finance cost savings on loan is will be visible from the next quarter.

Inviting everyone’s views on this.

3 Likes

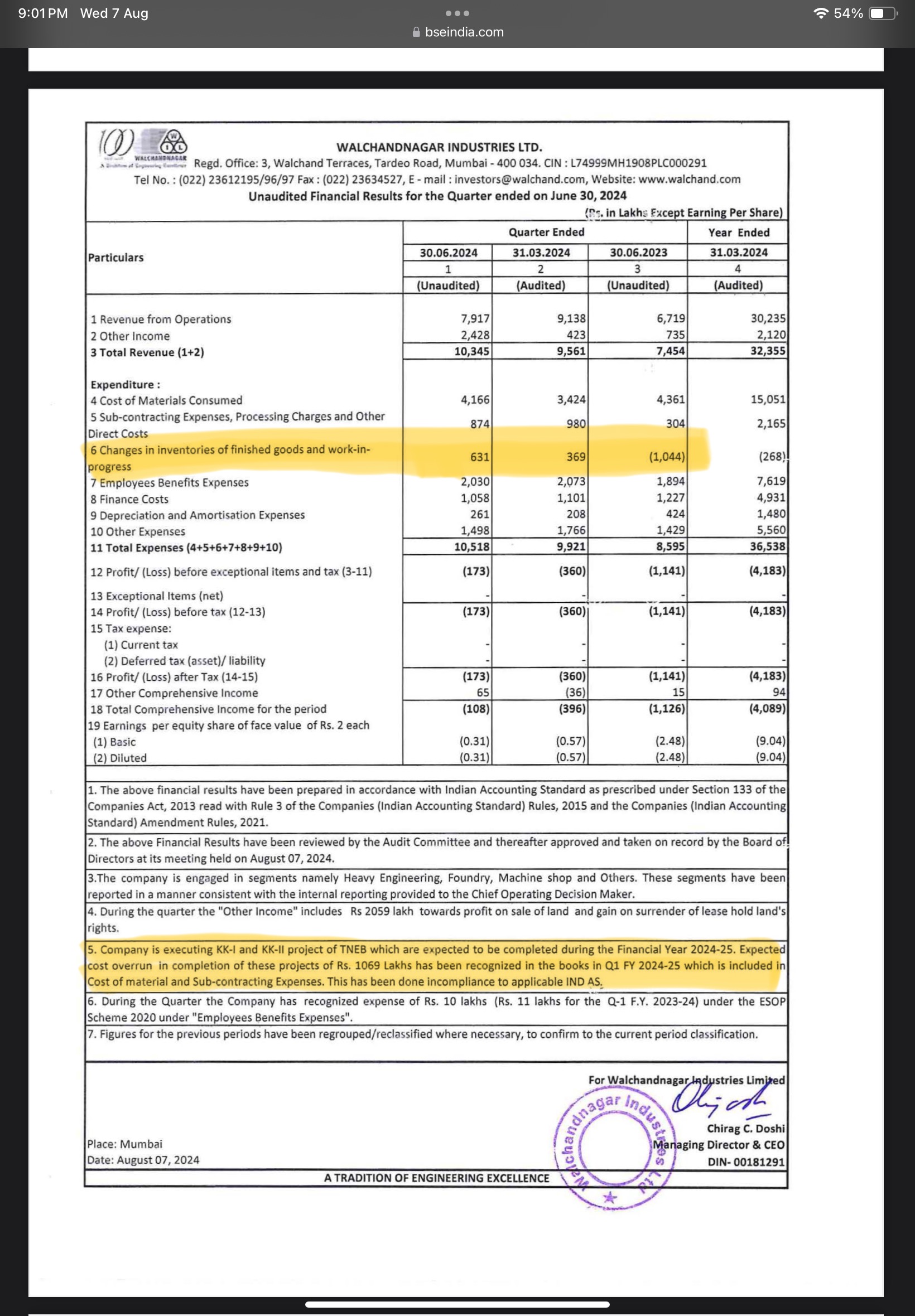

No… you have ignored two things marked in yellow …

The inventory change and cost overrun( you may interpret this as exception or risk according to your pov)

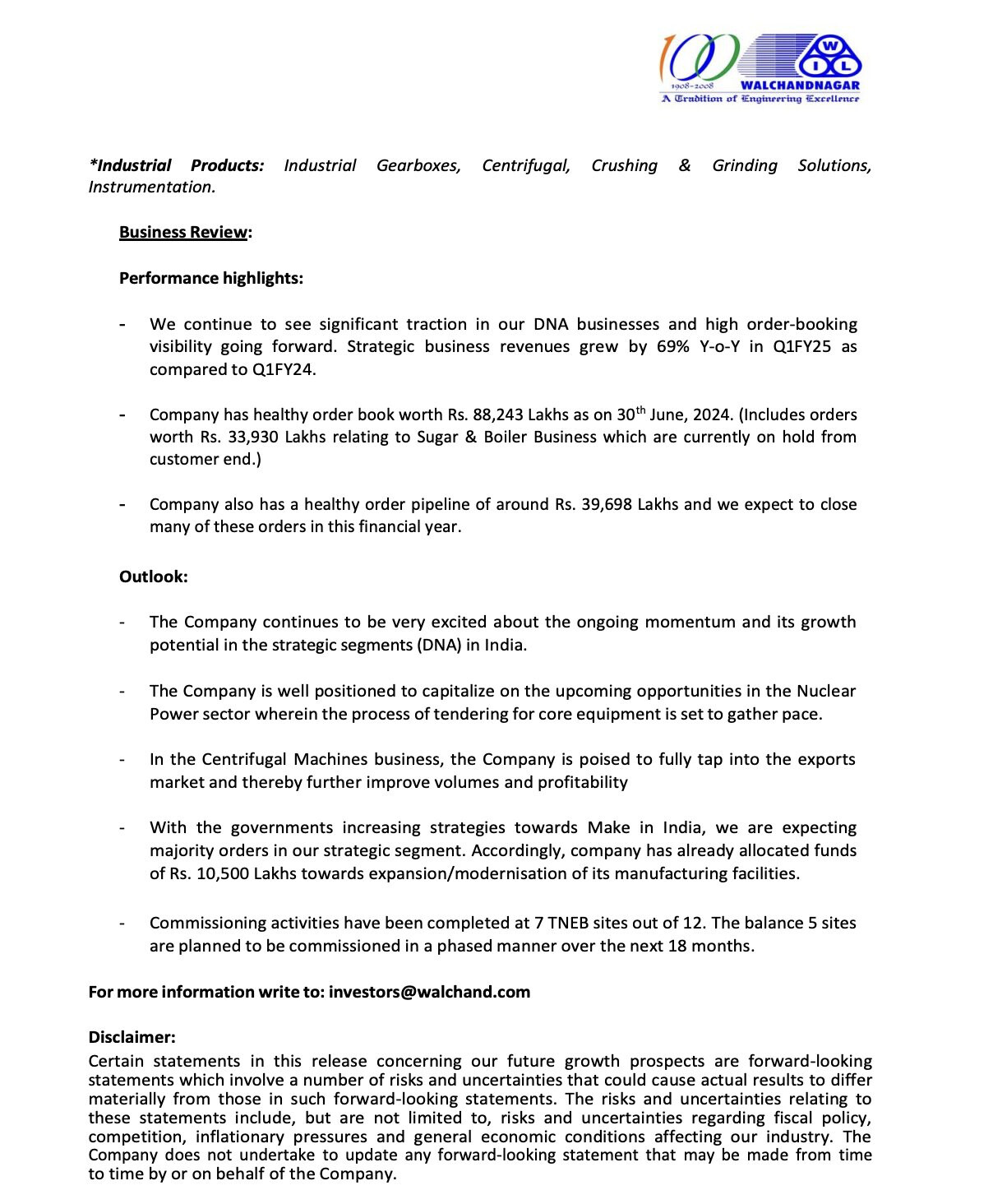

Also foundry business is not the area of focus and mgmt has said so in the presentation …

Cost overrun can not be considered as exceptional as it has been incurred in operational nature.

As I said ,it depends on your P.O.V. Frankly this is turnaround story and it is not complete yet .There is an element of hope based on recent working capital availability and tailwind due to government policies . There is no clear valuation metric either . In these type of companies it’s very futile to expect A grade consistent financial metrics . Also , the business usually is low margin, highly capital intensive and lumpy because of irregular and one-off kind of products(chadrayan things and that cement kiln for example ) . But tailwinds on a turnaround company can be a wonderful thing if one gets in early ….

Disc: Invested barely 1.5% of portfolio at 220 levels.

4 Likes

You cannot look at WIL solely with a financial lens. Not for now at least. Even small changes and improvements may not be appreciated, nor fully understood.

This is a legacy company which has suffered an unfathomable amount of misery & torture for years, and finally finds itself with one last chance, propelled with domestic tailwinds, government needs, nuclear power demand (very few can produce what WIL can), and equipped with astute investor backing.

Turnarounds like these are very difficult to stomach, as they aren’t straightforward and they take their own time.

@Ghonarbochon has explained well. The story is far from complete. If the picture all the investors have in their minds, manifests to even 50% - it’ll be a fantastic story. A fairytale & worthy of a case study.

Early entrants may get a long ride but it will require a lot of patience, government & industry support, and managerial execution.

8 Likes

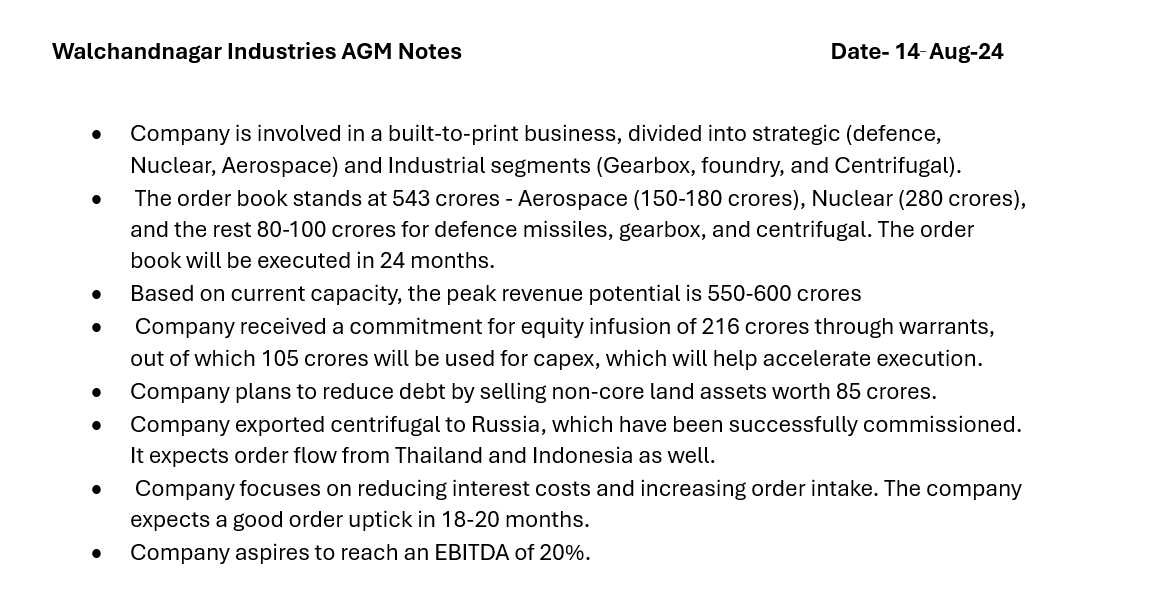

Anyone attended AGM today ? please share notes. Thanks in advance

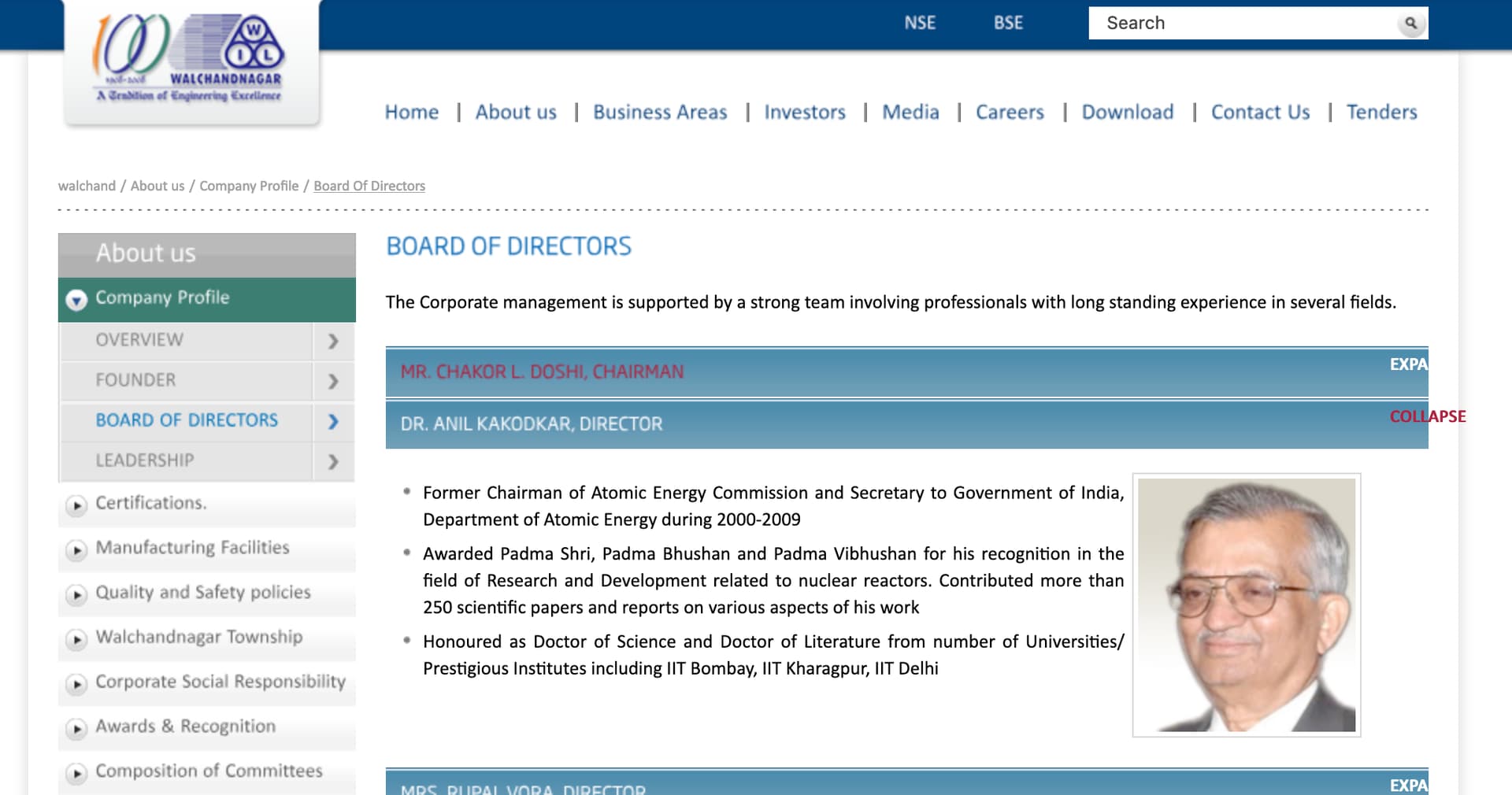

On the Board of Directors, we have Dr. Anil Kakodkar, The former Chairman of the Atomic Energy Commission (2000–2009) was awarded the Padma Shri, Padma Bhushan, and Padma Vibhushan for his contributions to nuclear research. He authored over 250 scientific papers and received honorary doctorates from prestigious institutions, including IIT Bombay, IIT Kharagpur, and IIT Delhi.

https://walchand.com/about-us/company-profile/board-of-directors-2/

5 Likes

First Corporate Presentation After preferenctial issue

Walchand-.pdf (4.5 MB)

…

6 Likes

The Latest and last credit rating from India Ratings & Research (Fitch Group), Summary of possible Risks and past events.

2 Likes

Anyone tracking this business?

Curious to know about the downtrend and recent businesses updates which might be the causes this downtrend? Can someone help me here please

Thanks in advance.

Fund raising approved through issuance of equity shares/QIP

7be6f509-5392-449a-96d6-7c1892d6eab2.pdf (333.0 KB)

2 Likes

Intimation of receipt of major Purchase Order from “Fluorine Korea Co. Ltd.”

for HF Reactor for FK Fischer Project.

5 Likes

Partial redemption of Non-convertible Debentures

1 Like

Budget announced focus on nuclear power plants. Inspite of such a positive development it could not even climb 10% today.They failed to deliver their revenue projections for FY24. Ajay Upadhyay has exited, Ashish Kacholia is reducing this stake. I wanted to understand what is plaguing the company? They have capability but they havent been able to scale up defence and aerospace inspite of large defence orders given out in last few years. Is this a management capability issue or lack of ambition? This is a turnaround story with sector tailwinds and yet they are not able to make most if it

1 Like

My current thoughts

- Nuclear target of 100GV by 2047 & 20,000cr for SMRs (TDPower / KECL too)

- Ajay Upadhayaya got in very early and has already done 4-5x … he may have dipped just below 1% or exited completely, we won’t know. Mahima (Kela driven) has increased their stake – It’s best to not follow what these HNIs do as we don’t know their reasoning and they often reduce/increase over time.

- https://walchand.com/wp-content/uploads/2025/01/WIL%20SHP%2001.01.2025.pdf - unable to find public shareholder names

Perhaps, Chirag Doshi should consider hiring a CEO to run the shop. If they’re able to show a change of financials, the stock will hit the roof.

Personally, I will be waiting a bit longer.

4 Likes

How is KECL to benefit from that budget in nuclear segment?