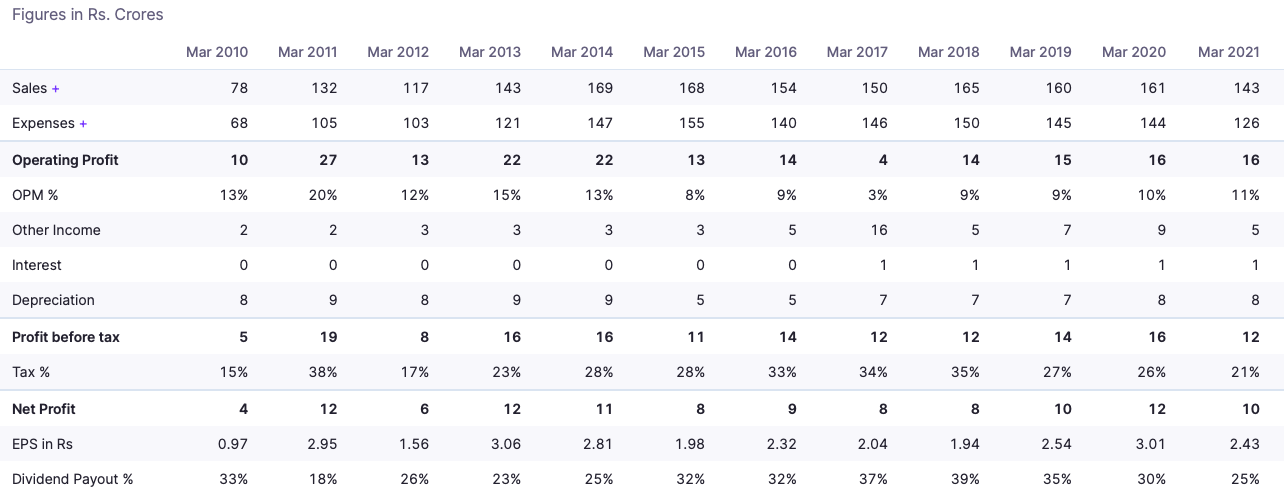

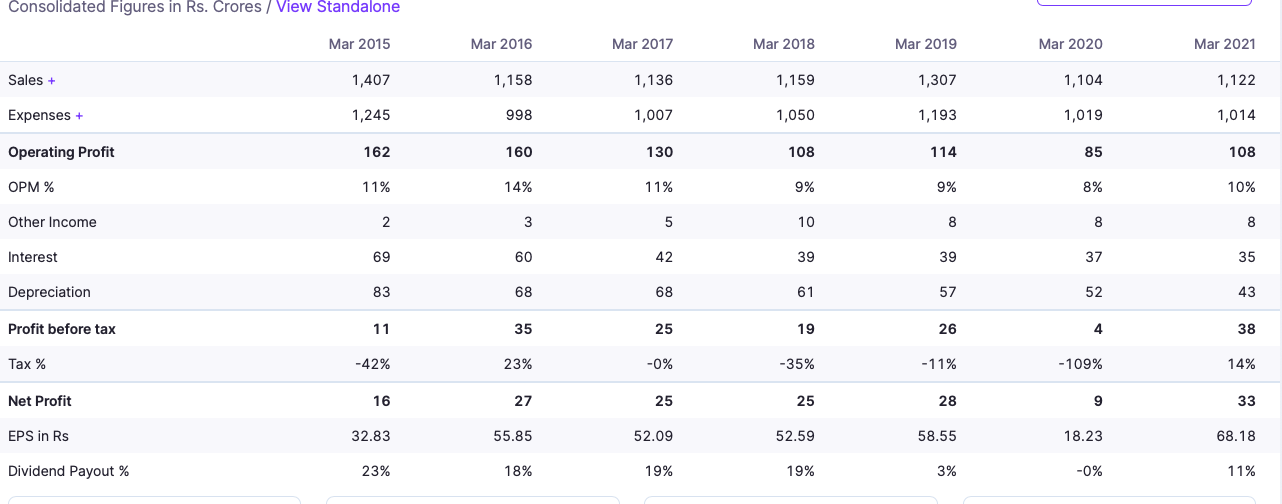

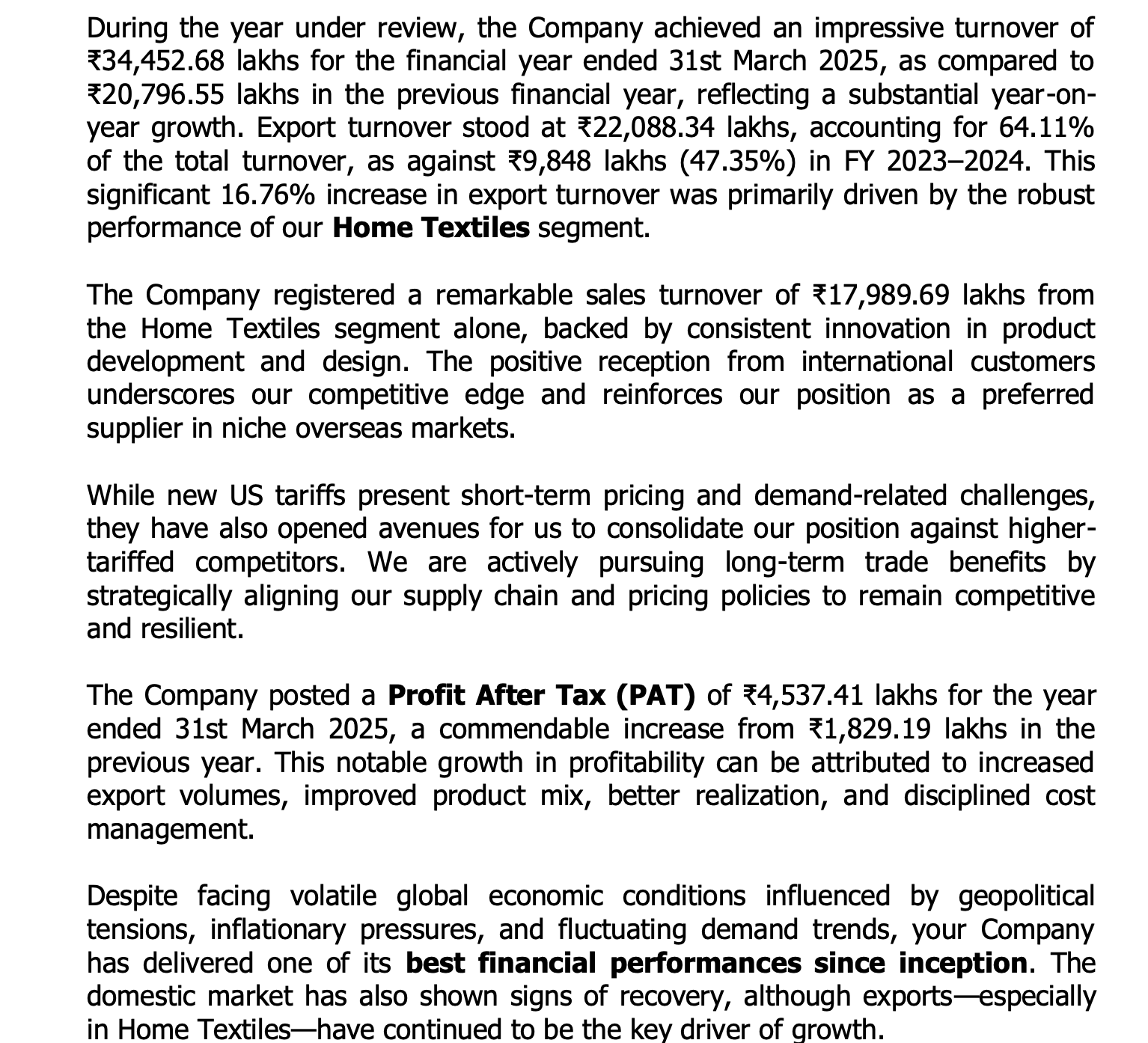

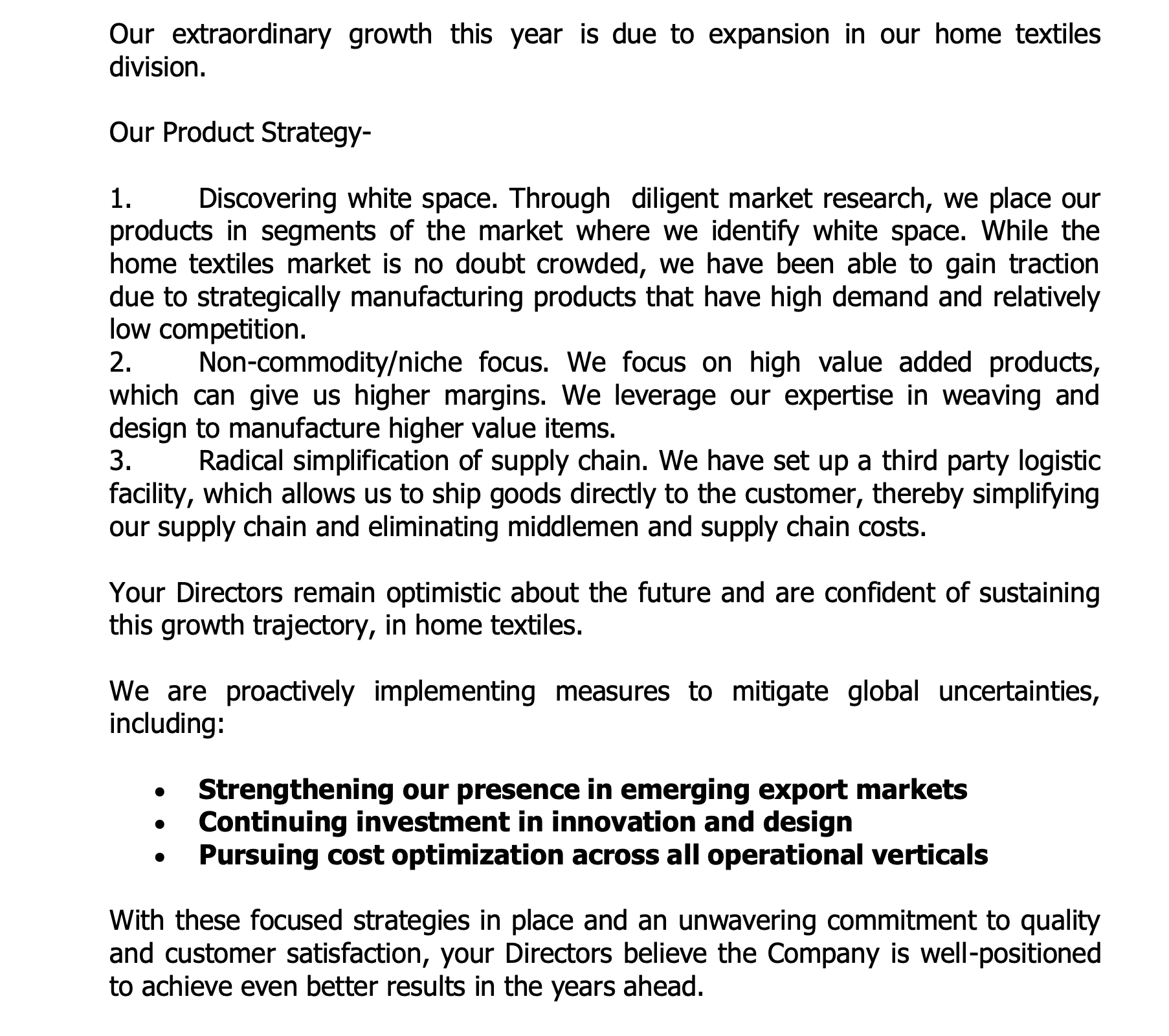

VTM Limited after being stagnent for many years is now posting very impressive results. These results don’t seem to be one-off.

VTM were basically into high-quality grey weaving and custom fabric production.

Their entry into super luxury home-textile division for developed market, led by Ms. Sala Kannan ( https://www.linkedin.com/in/sala-kannan-6b7a9a183/ ) is really changing the fortunes for the company. The same is being reflected in their gross margins. All we need to do is just check their annual reports for last 3 years, LinkedIn post of the company and Ms. Kannan, about the development happening (VTM Limited: Leading the Way in Sustainable Home Textiles - The Textile Magazine) (Strategy, Social Impact and Superior Quality: VT Mills thrives under Sala Kannan's Business Mantra - The Textile Magazine), interviews (https://www.youtube.com/watch?v=6ywcXeEvh-Q&pp=ygULdnRtIGxpbWl0ZWQ%3D),

Here we are thinking that this is one-off but the management is quite excited about the future and they are doing large capex to build new state of the art one lakh sft facility.

(https://www.youtube.com/watch?v=3LpJgA2KiTQ&pp=ygULdnRtIGxpbWl0ZWQ%3D).

They are totally vertically integrated for their super luxury eco-friendly home-textile products. Check out their B2C e-commerce pacific-cotton.com

Events like Heimtextil and Bharat Tex have been big blessings for them apart from entry of Ms. Kannan.

Posting an AI generated journey of VTM’s home textile division:

# TM Limited and Pacific Cotton: Chronological Evolution of Sustainable Home Textiles Leadership

## Foundational Phase (2015–2019)

## 2015: Sala Kannan’s Leadership Entry

** March 2015: Sala Kannan joins Thiagarajar Mills (parent company of VTM Limited) as Director, bringing expertise from her economics degrees at the University of Cambridge35.*

** Strategic Vision: Focuses on vertical integration, leveraging the group’s 80-year legacy in spinning and weaving to explore higher-value textile segments34.*

## 2016: Pacific Cotton’s Inception

** January 2016: Sala founds Pacific Cotton as a subsidiary of VTM Limited, targeting luxury home textiles. Initial operations focus on design and small-batch production for niche markets35.*

** Early Strategy: Combines Thiagarajar Mills’ fabric expertise with eco-conscious materials like organic cotton and bamboo, testing prototypes with European buyers4.*

## Growth Phase (2020–2022)

## 2020: Post-COVID Pivot to Home Textiles

** Market Opportunity: Identifies surging demand for sustainable home textiles during the pandemic. VTM Limited shifts focus from apparel to home textiles, capitalizing on eco-conscious consumer trends14.*

** Operational Integration: Begins processing gray fabric from Thiagarajar Mills’ spinning units into finished home textiles at partner facilities, reducing reliance on external suppliers14.*

## 2021: Heimtextil Frankfurt Breakthrough

** Global Debut: Pacific Cotton showcases its inaugural collection at Heimtextil Frankfurt, securing partnerships with U.S. and UK retailers. The “undyed organic cotton” line gains traction for its minimalist aesthetic45.*

** Certifications: Achieves Global Organic Textile Standard (GOTS) and OEKO-TEX certifications, validating chemical-free production claims1.*

## 2022: Infrastructure Expansion

** Madurai Facility Groundbreaking: Initiates construction of a 100,000 sq. ft. LEED-certified plant to consolidate stitching, packaging, and R&D under one roof. Slated for completion in 202414.*

** Revenue Milestone: Pacific Cotton contributes ₹320 crores (19% of VTM’s total revenue), with 68% from U.S. exports of organic bedsheets and duvet covers15.*

## Maturation Phase (2023–2025)

## 2023: Circular Economy Initiatives

** QR Traceability: Partners with Green Story to implement QR codes on products, enabling customers to track carbon footprint and water usage14.*

** Waste Recycling: Launches “ReCotton” program, repurposing 12% of production waste into insulation materials and industrial wipes4.*

## 2024: Leadership & Market Recognition

** Sala Kannan’s Accolades: Featured in The Textile Magazine for blending “family legacy with disruptive sustainability”5. Pacific Cotton’s EBITDA margin reaches 18.7%, outperforming industry averages1.*

** Heimtextil 2024: Debuts tactile luxury fabric line, featuring temperature-regulating Tencel-bamboo blends. Secures $22 million in pre-orders, primarily from EU luxury retailers45.*

## 2025: Capacity Scaling & Diversification

** Facility Commissioning: The Madurai plant becomes operational, boosting production capacity by 40% and reducing lead times from 8 to 5 weeks14.*

** Indian Market Entry: Launches “Pacific Living” sub-brand for domestic consumers, adapting global designs to local preferences like Ayurvedic-dyed bedsheets15.*

## Strategic Pillars of Pacific Cotton’s Success

## 1. Vertical Integration

** Fabric Sourcing: Utilizes Thiagarajar Mills’ GOTS-certified organic cotton yarns, ensuring supply chain control and cost efficiency14.*

** In-House Innovations: Developed proprietary dyeing techniques using neem and turmeric extracts, reducing synthetic chemical use by 92%5.*

## 2. Sustainability-Led Branding

** Carbon Neutrality Pledge: Achieves 70% renewable energy usage via solar farms and wind turbines. Targets 100% by 202614.*

** Compostable Packaging: Shifts to plant-based wrappers, eliminating 28 tons/year of plastic waste1.*

## 3. Leadership & Global Outlook

** Sala’s Cross-Industry Insights: Integrates retail analytics from her prior finance career to optimize inventory turnover (6.2x in 2024 vs. 4.1x in 2021)35.*

** Geographic Diversification: Expands to Australia and UAE, reducing U.S. revenue dependency to 54% in 202414.*

## Challenges & Adaptive Strategies

** Tariff Risks: Mitigates potential U.S. duty hikes (6.7% baseline) via premium pricing and lobbying through CITI (Confederation of Indian Textile Industry)14.*

** Cotton Price Volatility: Maintains 4-month inventory buffers and forward contracts with organic farms in Gujarat5.*

## Conclusion: Redefining Ethical Luxury

From its 2016 origins as a boutique brand to a ₹1,200+ crore export powerhouse, Pacific Cotton exemplifies VTM Limited’s agility in aligning tradition with global sustainability trends. Sala Kannan’s leadership—rooted in technical expertise and ESG pragmatism—positions the company to capture 5–7% of the $42 billion organic home textiles market by 2030. With infrastructure scaling and circular innovations, VTM is poised to cement India’s role as a leader in ethical textile manufacturing.

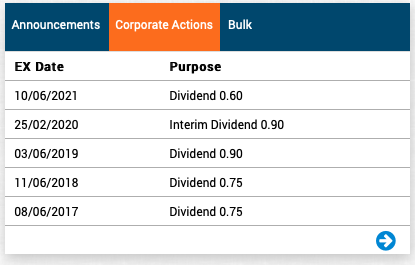

Apart from all this, company’s balance sheet is super strong is this debt ridden sector, they are zero debt with around 100 crores of cash on the balance sheet and consistently paying dividend.

With all this the company is trading at very cheap valuation despite steep rise recently given the expertise, growth and hunger they have.

Threats of US Tariffs:

Assuming VTM Limited exports organic cotton and 100% organic bedsheets to the US, the tariff rate for HS code 63041910 is 15.9%, as per the US Harmonized Tariff Schedule Harmonized Tariff Schedule. There are no differential tariffs for organic products, posing a challenge given the US market’s importance.

Challenges:

- Raw material pressure on the margins (however, the increasing proportion of luxury sales can mitigate it somehow)

- Excessive dependency of one person

- Degloblisation

Disclaimer: Invested, biased