With these focused strategies in place and an unwavering commitment to quality

and customer satisfaction, your Directors believe the Company is well-positioned to achieve even better results in the years ahead

excerpt from annual report

With these focused strategies in place and an unwavering commitment to quality

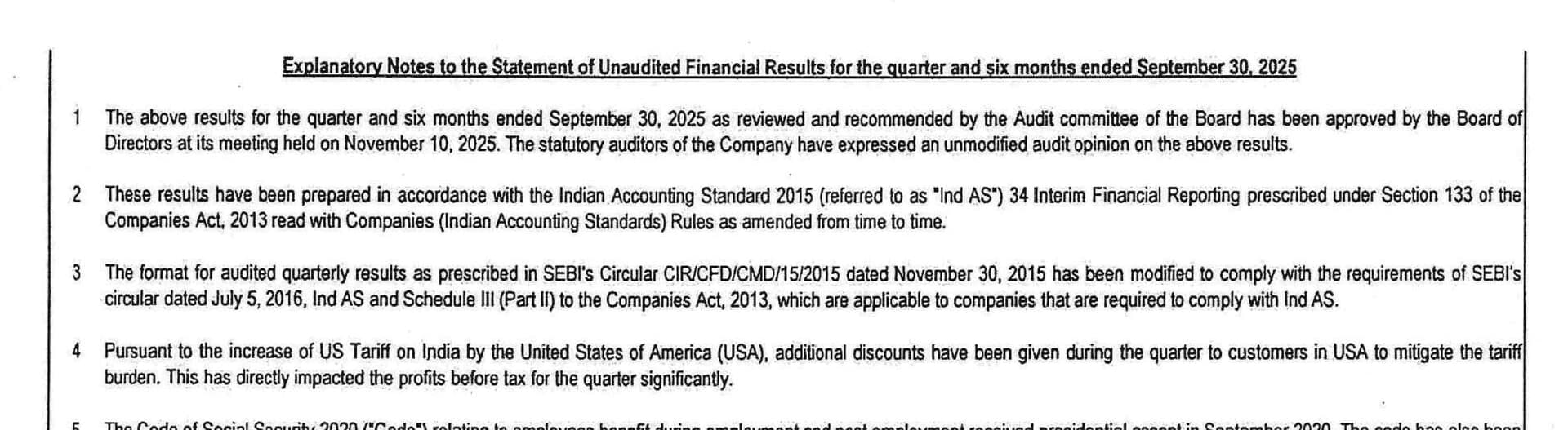

and customer satisfaction, your Directors believe the Company is well-positioned to achieve even better results in the years ahead

excerpt from annual report

Hey, but isnt ebitda and margins based on good sold. I dont think there is any effect of inventories here.

How would you differentiate capital used to do sales and capital used to make goods that went into inventory? The raw material must have been bought in some quarter. I would too like some clarification who has more understanding in this topic.

Hi I am planning to attend the AGM , anyone else interested pls DM me

Long term credit rating increased to A-

edit - @varunm2112 do share details after the vist, will love to hear about promoter’s commentary

VTM AGM Notes

Guidance

Topline 18-20% next 3 years

Bottomline 25-27% next 3 years

Payables days are low as do cash&carry to get better pricing but that increases wc days

We looking at customer diversification by getting into UK

FY25 Capex - 60 new machines in Alampatti

We don’t need warehouses in the USA as we are D2C

Reduced inventory from 5-6 months to 3 months using inhouse software developed with the help of our engineering college

New Products - Window curtains & bath textiles

Utilisation - 75-80%

FY26-28 Capex - 23cr this will increase our capacity by 25-30%

We have surplus land we can increase additional capacity based on customer demand in 5-6 months using Pre-Fab buildings

Expansion of One lakh sqft at Alampatti is for garments

Carborundum business is good because of ADD on China imports

Q3 is high margin because of festival season. In Q4FY25 margin came down due to increased RM prices

Shareholding pattern is published for the quarter ending June-25, here are some pointers;

ESM is best to shake out retail investors

Margins contracted significantly, definately does not resonate with the guidance given in AGM. Hopefully next quarters are executed well

Upcoming quarters might be worse due to the elevated tariffs. The contribution of exports to their topline is above 60%.

Textiles in general operate on thin margins and a tariff situation with one of their major export countries can be very damaging.

I would sit on the fence and watch how it plays out. If it corrects significantly from here and the value looks attractive, then ill think about taking a position.

Right now, it looks like too much downside risk with very minimal upside potential. Hope things change.

Not all of it is to USA though ..they export a lot to Europe because thats where they got their breakthrough .And because of FTA with EU and UK, there is advantage as well .

What about domestic demand? It’s going to have spiral effect. Let’s wait and watch.

The scrip is out of ESM 2 and now in ESM 1.

No more periodic auctions and circuit limits set to 5%.

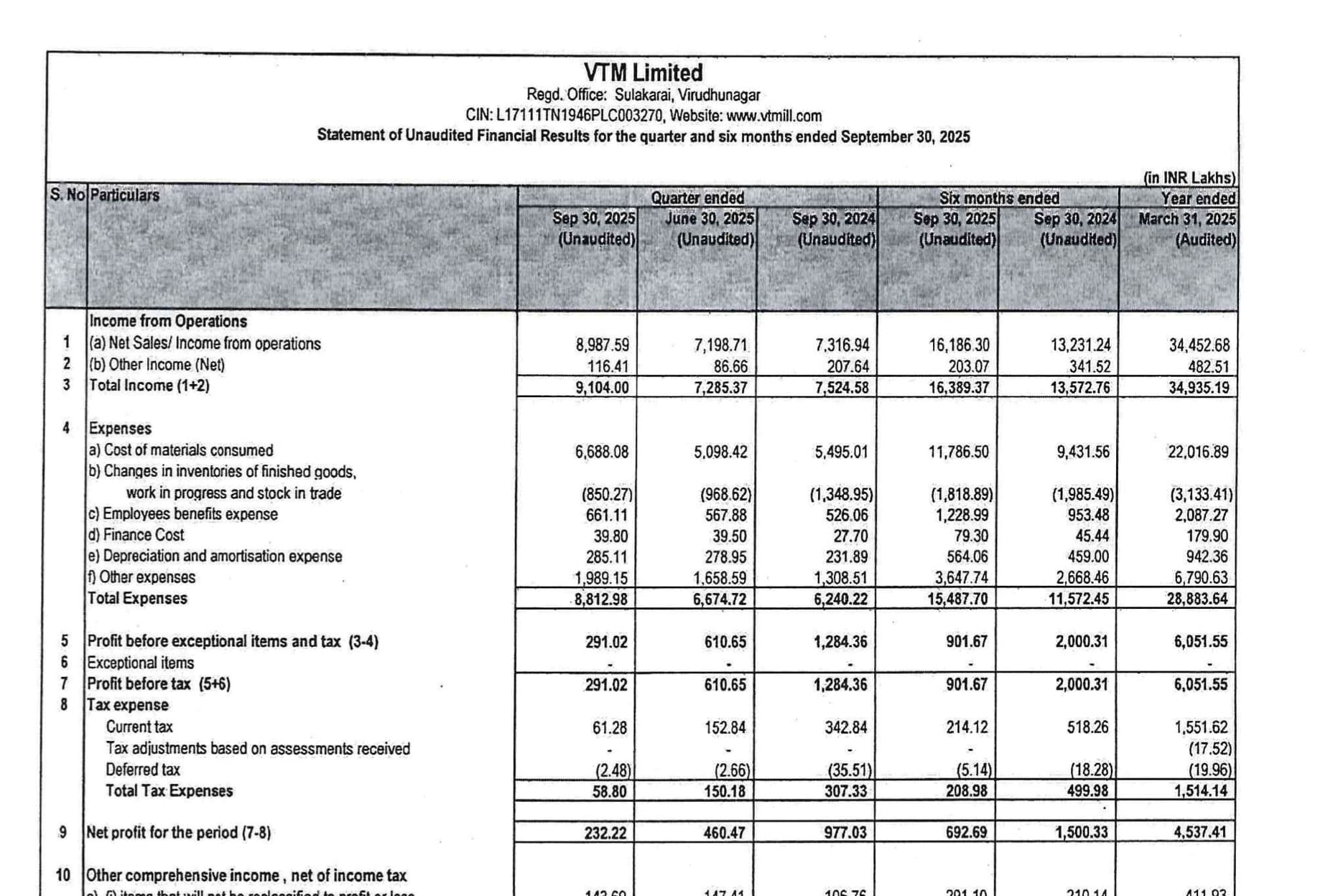

VTM declared Q2 results today.

Revenue from Operations: ₹89.88 Cr (QoQ 24.85% up, YoY 22.84% up)

EBITDA: ₹5 Cr (QoQ 28.86% down, YoY 55.16% down)

PAT: ₹2.32 Cr (QoQ 49.57% down, YoY 76.25% down)

While the revenue has gone up handsomely, profitability and the margins went down drastically.

Looks like tariffs have hit hard. Notes to results says that company gave additional discounts to US customers to mitigate the tariff burden and that has directly impacted the profits.

Question is how much profit is attributable to tariffs?

Let me try to guess.

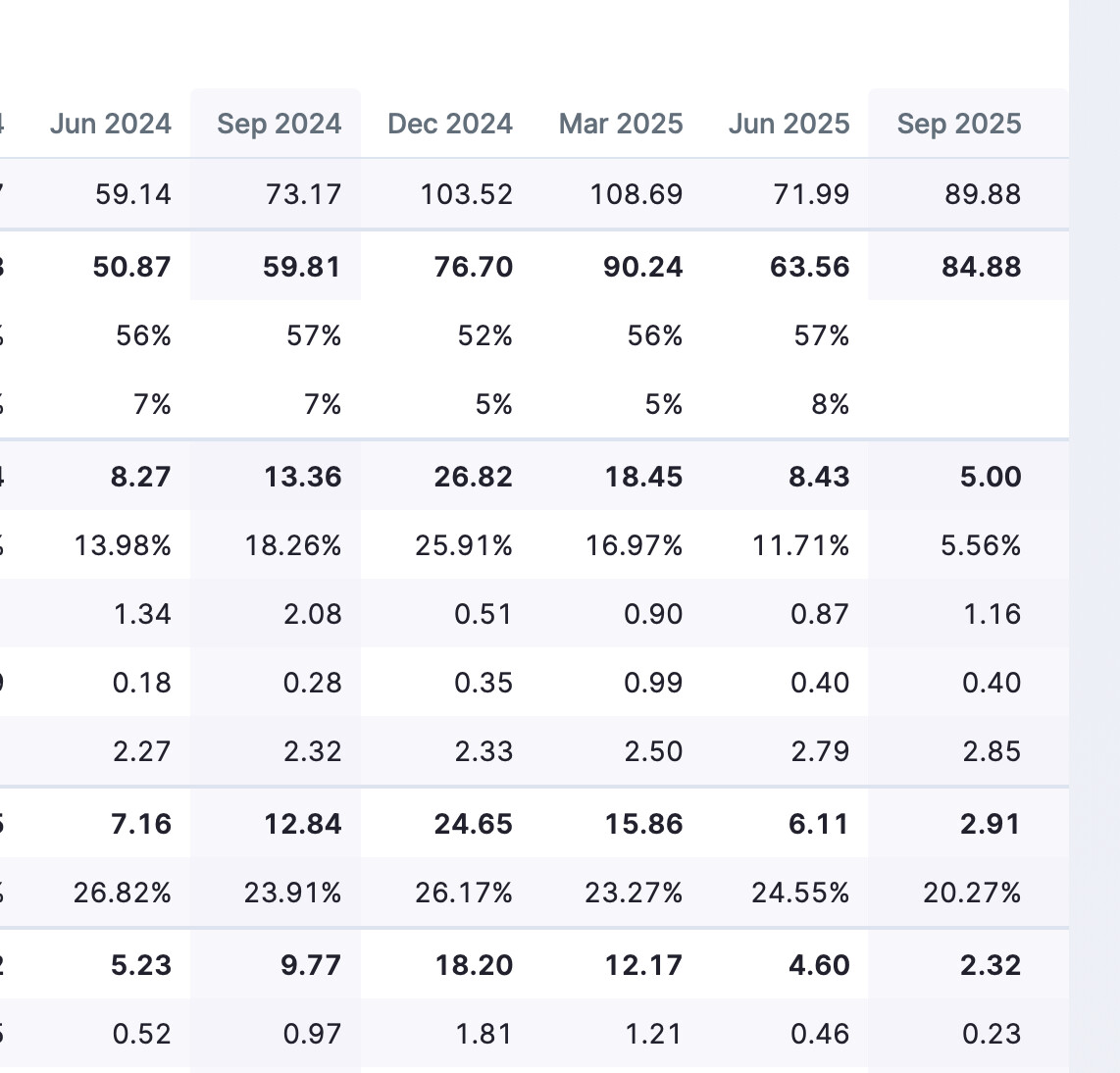

Above picture shows the financials of the company since the home textiles for the company has taken off. Cost of material has been mostly around 56% to 57% (even in Q1 when 10% tariffs were there). But for this quarter, material went up to 65% (₹5,837.8L), which is significantly higher.

I think if it was not for discount to USA buyers, the revenue would have been significantly higher.

If we calculate revenue at 57% of material cost, it would be around ₹103 crores (90/57*65) against present 90 crores. I think in case of discount other components of P&L remain same. Looks like tariffs discount has cost atleast ₹13 crores for VTM in this quarter alone, if we factor this discount, PAT would be around ₹12 crores.

This is just an random thought and an opinion, there could be other reasons too.

For me, big positive is the revenue, which is up handsomely even after discounts, which means VTM has not lost customers for the short term margins pressure, this affirms their relations with the customers specially with quince, there might be new product launches as well. Cash Flows has been good, balance sheet remains robust.

Risk continues to be tariffs, dont know how long they will last. I think pressure on the bottom line will continue till tariffs dont fall below 20%. Hoping for trade deal with USA soon and also EU-India FTA.

Looks like VTM has also hired Investors’ Relations agency recently.

Time for better investors communications.

Disclaimer: Invested, biased

As per VTM’s Investor Relations agency, the company will arrange concall or presentation starting from next quarter.

@ayushmit Sir, if possible , could you please post here the ppt/pdf ,that you presented for the alpha ideas recently ?

Quince announced today a $500M Series E led by ICONIQ Capital at $10.1B post-money valuation- more than double the $4.5B from just 8 months ago. Other investors include Baillie Gifford, DST Global, Wellington Management among others.

VTM’s FY25 annual report disclosed ₹159.43 Cr revenue from their single largest customer out of ₹179.90 Cr home textile revenue (88.6% concentration). In the recent concall, Sala Kannan confirmed Quince is about 40-45% of total VTM revenue and guided 20-25% growth going forward from this customer.

As per Quince CCO Matt Lippert, they’ve launched in Canada and see “a ton of potential in Europe, both UK and continental Europe.” Quince has been hiring for UK roles since Feb 2026. Also started hirings for Germany and France. They framed it as scaling an operating system built around AI-driven demand forecasting, direct factory integration, material verification, and real-time production planning, with the goal of reducing inventory cycles from quarters to weeks.

Worth noting that Quince’s M2C model relies on deep factory integration- In the recent investors’ call management highlighted that VTM doesn’t just supply product, they warehouse and ship individual parcels to end consumers, a 3PL setup built over 2-3 years. On the trade side, India-UK FTA ( gives 0% duty on textiles, India-EU FTA negotiations are progressing similarly. Interestingly, VTM’s new one lakh square feet facility for home textiles is also going live this quarter. It would be interesting to see whether VTM remains the choice of Quince expansion.

Disc: Invested, biased.